Aircraft Strut Market Size, Share & Industry Analysis, By Type (Landing Gear Struts, Wing Struts, Drag and Side Struts, Support & Utility Struts), By Operation (Hydraulic, Pneumatic, and Mechanical) By Platform (Fixed Wing Aircraft and Rotary Wing Aircraft), By Material (Titanium Alloys, Composites/Hybrid Structures, High-Strength Steel Alloys, and Aluminum Alloys), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

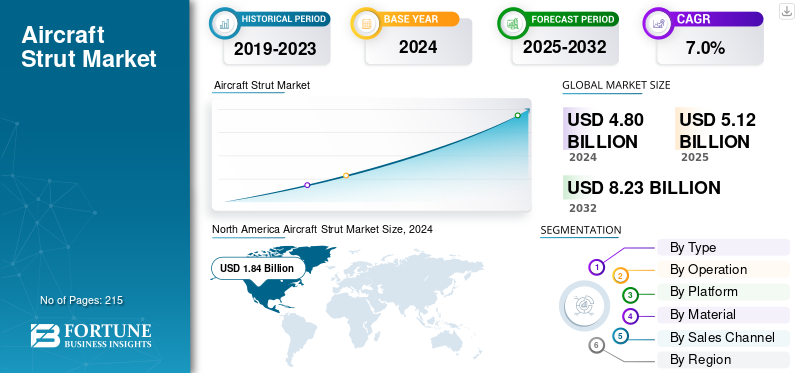

The global aircraft strut market size was valued at USD 5.12 billion in 2025. The market is projected to grow from USD 5.47 billion in 2026 to USD 9.26 billion by 2034, exhibiting a CAGR of 6.80% during the forecast period. North America dominated the aircraft strut market with a market share of 38.30% in 2025.

An aircraft strut is an axially loaded structural component engineered primarily to carry compressive forces (and, where required, tension) to support and stiffen airframe assemblies. By providing a direct load path, struts reduce bending moments in wings, tails, and fuselage frames, enabling lighter, more fatigue-resistant structures. Typical materials include high-strength aluminum and steel alloys, with titanium and advanced composites adopted where weight, corrosion resistance, or life-cycle durability are critical.

Government and defense agencies including the FAA, EASA, and the U.S. DoD govern the design, qualification, and continued airworthiness of aircraft struts through the type-certification basis for each aircraft (14 CFR/CS Parts 23, 25, 27, and 29 for structural and ground-load requirements).

Leading industry participants include Safran Landing Systems, Collins Aerospace (RTX), Liebherr-Aerospace, Héroux-Devtek, and Triumph Group for large commercial and defense programs, supported by forging and machining houses and seal/actuation specialists (e.g., Parker, Trelleborg). Airframers such as Airbus, Boeing, Embraer, Bombardier, Dassault, and Textron Aviation integrate struts into landing-gear assemblies and, in the general-aviation segment, as external lift struts.

Download Free sample to learn more about this report.

Aircraft Strut Market Key Takeaways

- 2025 Market Size: USD 5.12 billion

- 2026 Market Size: USD 5.47 billion

- 2034 Forecast Market Size: USD 9.26 billion

- CAGR: 6.80% from 2026–2034

- North America dominated the aircraft strut market with a 38.30% share in 2025.

- The landing gear struts segment is expected to account for 46.77% of the market share in 2026.

- The fixed-wing aircraft segment is projected to hold 74.70% of the global market share in 2026.

North America

North America generated USD 1.96 billion in revenue in 2025 and is projected to reach USD 2.10 billion in 2026.

Europe

Europe accounted for 27.80% of the global market in 2025 and is expected to reach USD 1.52 billion in 2026.

Asia Pacific

Asia Pacific captured 26.30% of global revenue in 2025 and is projected to reach USD 1.45 billion in 2026.

U.S.

The U.S. aircraft strut market is projected to reach USD 1.70 billion by 2026.

Japan

Japan’s aircraft strut market is projected to reach USD 0.29 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Aircraft Production and Replacement of Aging Fleets Driving Market Growth

The sustained increases in new-aircraft production and the replacement of older fleets are the single most direct demand engine for aircraft, struts especially landing-gear (oleo) struts. Every delivery requires a full shipset of main and nose-gear struts, so higher build rates translate almost one-for-one into OEM strut demand.

- For instance, Boeing Commercial Market Outlook 2025 projects 43.6k aircraft deliveries and a 49.6k-unit fleet by 2044. Therefore, the rise in aircraft production and deliveries is expected to increase the demand for aircraft struts.

As legacy aircraft approach life limits, landing-gear (oleo) struts face tighter inspection intervals and more overhauls (seals, bushings, surface restoration), lifting near-term aftermarket spend.

MARKET RESTRAINTS

High Manufacturing and Maintenance Costs to Limit Market Expansion

The aircraft strut market growth faces a key obstacle in the form of high production and lifecycle maintenance costs. Strut assemblies, particularly oleo struts, require precision forging, high-tolerance machining, specialized surface treatments (such as chrome-free or HVOF coatings), and certified hydraulic components all of which increase manufacturing expenses. Additionally, the need for periodic overhauls, fluid servicing, and replacement of seals and bushings adds to long-term operational costs for airlines and operators. These cumulative expenses often pressure procurement budgets, delay replacement cycles, and limit adoption of advanced lightweight and eco-friendly materials.

MARKET OPPORTUNITIES

Adoption of Smart and Lightweight Strut Technologies Create Space for Market Expansion

A major opportunity in the aircraft strut market lies in the integration of smart monitoring systems and growing emphasis on lightweight material technologies. The ongoing shift toward digital and data-driven maintenance is creating demand for intelligent struts equipped with embedded pressure, load, and temperature sensors that enable real-time health monitoring and predictive maintenance. This reduces unplanned downtime, improves fleet reliability, and lowers lifecycle costs for operators. Simultaneously, advancements in titanium, high-strength aluminum alloys, and carbon-composite structures are allowing strut manufacturers to achieve significant weight reductions without compromising strength or durability.

AIRCRAFT STRUT MARKET TRENDS

Integration of Additive Manufacturing and Near-Net-Shape Forging

A growing trend in the aircraft strut market is the adoption of additive manufacturing (AM) and near-net-shape forging to optimize operational efficiency and component performance. Strut manufacturers are increasingly leveraging 3D printing for fittings, end-caps, and complex internal geometries, reducing material waste and machining time compared to traditional subtractive processes. Similarly, near-net-shape forging allows for precise material distribution, minimizing the buy-to-fly ratio and improving structural integrity.

MARKET CHALLENGES

Supply Chain Constraints and Long Lead Times to Present Challenges for the Market

A key challenge in the aircraft strut market is the persistent supply chain bottleneck affecting the availability of high-grade alloys, forgings, and precision-machined components. Strut production depends on certified aerospace suppliers for titanium, high-strength steel, and hydraulic subcomponents, all of which require stringent quality assurance and traceability. Global shortages of raw materials, limited forging capacity, and extended certification cycles have led to long lead times and delayed deliveries for both OEM and aftermarket demand.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Primary Load-Bearing Function and High Replacement Frequency Drive Landing Gear Struts Segment Growth

On the basis of type, the market is classified into landing gear struts, wing struts, drag and side struts, support & utility struts.

The landing gear struts segment will accounting for the largest share of 46.77% in 2026, as it is a primary shock-absorbing and load-bearing component during landing and taxi operations. Their high unit value, complex engineering, and regulated maintenance cycles ensure consistent OEM and aftermarket demand. Rising global aircraft production rates and fleet renewals is expected to contribute to the segment growth.

Support and utility struts are witnessing accelerated growth due to the surge in lightweight composite airframe designs and the adoption of gas-spring and smart strut technologies in doors, cowlings, and access systems. The emergence of eVTOL and unmanned aerial platforms, which rely on compact, low-maintenance strut mechanisms, adds new high-growth applications.

By Operation

Superior Damping Efficiency and Reliability Propel Hydraulic Struts Segment Growth

Based on operation, the market is segmented into hydraulic, pneumatic, and mechanical.

Hydraulic struts is estimated to dominate by accounting for the majority of market share of 32.95% in 2026. These systems combine hydraulic fluid and compressed gas to absorb and dissipate high-impact loads during takeoff and landing, making them indispensable for virtually all commercial, business, and military aircraft. Reliability, superior damping capability, and compliance with stringent airworthiness standards are driving factors for the growth of the segment.

Pneumatic struts are witnessing fastest growth due to their increasing adoption in light aircraft, UAVs, and next-generation trainers. Unlike hydraulic systems, pneumatic struts offer simpler design, reduced leakage risk, and easier servicing, making them attractive for smaller platforms and personal aviation.

By Platform

Sustained Commercial Aircraft Production and Fleet Renewal Support Fixed-Wing Aircraft Segment Growth

Based on platform, the market is segmented into fixed wing aircraft, and rotary wing aircraft. Fixed wing aircraft includes commercial aircraft, business aircraft, general aviation aircraft, and military aircraft. Rotary wing aircraft comprises military helicopters and civil helicopters.

Fixed-wing aircraft will hold the maximum aircraft strut market share of 74.70% in 2026, due to sustained global production of commercial and business jets and continuous fleet renewals by major airlines. Expansion in narrow-body programs (A320neo, 737 MAX) and emerging regional aircraft (Embraer E2, COMAC C919) is expected to drive the segment growth.

Rotary-wing platforms are experiencing the fastest growth in strut demand, due to modernization of defense helicopter fleets and expansion of civil utility missions (EMS, offshore transport, and firefighting). The increasing procurement of multi-role and heavy-lift helicopters (NH90, AW149, and CH-47F) creates recurring demand for durable landing and support strut assemblies.

By Material

High Strength-to-Weight Ratio and Corrosion Resistance Drive Titanium Alloys Segment Growth

Based on material, the market is segmented into titanium alloys, composites/hybrid structures, high-strength steel alloys, and aluminum alloys.

Titanium alloys will maintain the largest share of 41.26% in 2026, due to their superior strength-to-weight ratio, fatigue life, and corrosion resistance. The titanium struts act as primary load-bearing structures. Moreover, the continuous efforts toward aircraft lightweighting and compatibility with composite materials in new-generation programs drive sustained adoption.

Composites and hybrid structures are the fastest-growing material category, driven by the pursuit of the aerospace industry for fuel efficiency and emission reduction. These materials enable significant weight savings while maintaining high stiffness and fatigue resistance, making them ideal for auxiliary struts and control linkages.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

Rising Aircraft Production Backlogs and System Integration Expansion Reinforce OEM Segment Growth

Based on sales channel, the market is segmented into OEM and aftermarket.

The OEM segment dominates revenues due to continuous aircraft production ramp-ups and inclusion of strut systems during the manufacturing phase. Major aircraft manufacturers such as Airbus, Boeing, Embraer, and HAL are scaling output to meet backlogs which support consistent OEM deliveries. Increasing adoption of integrated landing and structural assemblies that combine sensors and lightweight materials also reinforces OEM-driven growth.

The aftermarket segment is the fastest-growing sales channel, propelled by the aging global fleet, high aircraft utilization rates, and mandatory maintenance cycles for critical strut components. Airlines and MRO providers are prioritizing cost-effective overhauls and retrofits, especially for hydraulic and composite struts in regional and military fleets.

Aircraft Strut Market Regional Outlook

North America Aircraft Strut Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America represented USD 1.96 Billion, accounting for 38.30% of the worldwide market, and is projected to grow to USD 2.1 Billion in 2026. North America holds the largest share of the aircraft strut market, driven by the presence of major OEMs such as Boeing, Lockheed Martin, and Gulfstream. The region benefits from a robust commercial aircraft production base, continuous fleet modernization, and strong defense procurement programs supporting fighter and rotary-wing platforms. The MRO network density across the U.S. and Canada ensures consistent aftermarket replacement demand. The U.S. market is projected to reach USD 1.7 billion by 2026.

Europe

The Europe market generated USD 1.42 Billion in 2025, representing 27.80% of the global market landscape, and is expected to reach USD 1.52 Billion in 2026. Europe’s market expansion is underpinned by aircraft manufacturing hubs in France, Germany, and the U.K., led by Airbus, BAE Systems, and Leonardo. The region’s focus on sustainable aviation and carbon-neutral programs is encouraging the adoption of advanced composite and hybrid struts. Significant R&D funding under EU initiatives such as Clean Aviation and Horizon Europe is accelerating innovation in low-weight, high-durability materials. The UK market is projected to reach USD 0.31 billion by 2026, while the Germany market is projected to reach USD 0.39 billion by 2026.

Asia Pacific

Asia Pacific contributed 26.30% to the global market in 2025, with a valuation of USD 1.35 Billion, and is projected to reach USD 1.45 Billion in 2026. Asia Pacific is the fastest-growing region, propelled by the rapid expansion of the commercial aviation industry in China, India, and Southeast Asia. Indigenous programs are boosting local strut manufacturing and supplier networks. Rising defense budgets and the development of new multi-role helicopters and transport aircraft further stimulate demand. Increasing maintenance repair and overhaul MRO infrastructure investment and airline fleet renewals is expected to present opportunities for the market. The Japan market is projected to reach USD 0.29 billion by 2026, while the China market is projected to reach USD 0.51 billion by 2026, and the India market is projected to reach USD 0.29 billion by 2026.

Rest of the World

Latin America’s aircraft strut market is growing steadily, driven by rising air passenger traffic and modernization of regional aircraft fleets. The market in Latin America reached USD 0.22 Billion in 2025, representing 4.30% of total market revenue, and is projected to reach USD 0.23 Billion in 2026. Brazil’s Embraer plays a central role in sustaining OEM-level demand, while expanding MRO operations in Mexico and Chile strengthen the aftermarket segment. The Middle East & Africa market was valued at USD 0.17 Billion in 2025, capturing 3.00% of global revenue, and is estimated to reach USD 0.17 Billion in 2026. The Middle East & Africa market is supported by strong defense procurement programs and the continued expansion of civil aviation infrastructure. The UAE and Saudi Arabia are investing heavily in modern fighter and transport fleets, driving OEM demand for strut systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Landing-Gear Systems, Digital MRO Integration, and Lightweight Design Innovation Drive Competitiveness

The aircraft strut market is moderately consolidated, characterized by a limited number of global OEMs and Tier-1 suppliers that dominate both the manufacturing and maintenance value chains. Competition is primarily driven by technological capability, certification pedigree, lifecycle cost efficiency, and aftermarket service coverage.

Prominent market participants include Safran Landing Systems, Collins Aerospace (RTX), Liebherr-Aerospace, Héroux-Devtek Inc., Triumph Group, and UTC Aerospace Systems, which collectively maintain extensive global production and repair networks. The key players are engaging in partnerships with leading OEMs such as Airbus, Boeing, Embraer, Bombardier, and Lockheed Martin, ensuring recurring demand for both new installations and lifecycle support contracts.

LIST OF KEY AIRCRAFT STRUT COMPANIES PROFILED

- Safran S.A. (France)

- Collins Aerospace (RTX Corporation) (U.S.)

- Liebherr-Aerospace Lindenberg GmbH (Germany)

- Héroux-Devtek Inc. (Canada)

- Triumph Group, Inc. (U.S.)

- LISI Aerospace (France)

- Parker Hannifin Corporation (U.S.)

- Woodward, Inc. (U.S.)

- Spirit AeroSystems (U.S.)

- Moog Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Safran Landing Systems renewed its partnership agreement with Revima at the Paris Air Show to support landing gear including struts repair and overhaul operations in France and Thailand.

- February 2025, Air Industries Group secured a follow-on contract valued at over USD 11 million to supply landing-gear assemblies (which include strut systems) for the E‑2D Advanced Hawkeye aircraft of the U.S. Navy.

- December 2024: GA Telesis, LLC signed a definitive agreement to acquire AAR CORP.’s Landing Gear Overhaul business and its Wheels & Brakes unit, bolstering its MRO capacity in strut/gear system.

- October 2024: AEC Engineered Composites announced the launch of its “AIRSTRUT® Lightweight Composite Struts” product line, targeting structural-strut applications in both fixed-wing and rotary-wing aircraft.

- October 2024: Ametek MRO signed a contract with Liebherr-Aerospace for landing gear maintenance, repair and overhaul for the Embraer E-Jet E1 series across the EMEA region.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.80% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type, Operation, Platform, Material, Sales Channel, and Region |

|

By Type |

|

|

By Operation |

|

|

By Platform |

|

|

By Material |

|

|

By Sales Channel |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.12 billion in 2025 and is projected to reach USD 9.26 billion by 2034.

In 2025, the market value stood at USD 1.96 billion.

The market is growing at a CAGR of 6.80% during the forecast period of 2026-2034.

The fixed wing aircraft segment led the market by platform.

The key factors driving the market are increasing aircraft production and replacement of aging fleets.

Safran S.A. (France), Collins Aerospace (RTX Corporation) (U.S.), Liebherr-Aerospace Lindenberg GmbH (Germany), and Héroux-Devtek Inc. (Canada) are some of the prominent players in the market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 215

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us