Aircraft Tugs Market Size, Share & Industry Analysis, By Type (Towbar Tugs and Towbarless Tugs), By Towing Capacity (Light (Less than 15 tons), Medium (15 -75 tons), Heavy (75 to 150 tons), and Extra Heavy (More than 150 tons)), By Aircraft Type (Commercial Aircraft (Narrow-body Aircraft and Wide-body Aircraft), General Aviation, Regional Aircraft, and Military Aircraft), By Propulsion (Diesel, Battery Electric, Hybrid Electric, and Gasoline), By Application (Pushback Operations, Hangar Towing, Ground Handling & Safety, and Others), By End User, and Regional Forecast, 2026-2034

Aircraft Tugs Market Size and Future Outlook

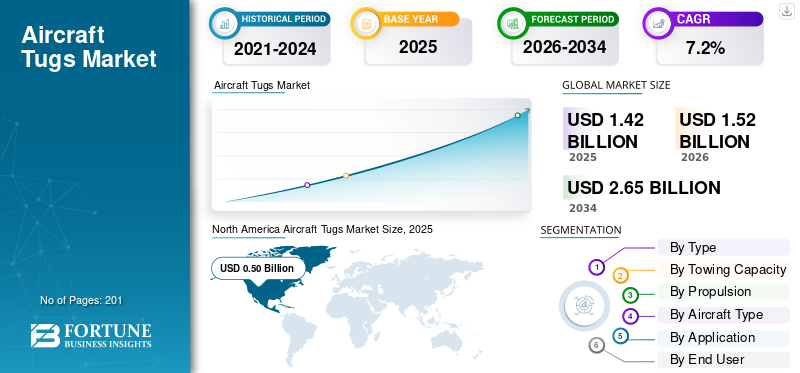

The global aircraft tugs market size was valued at USD 1.42 billion in 2025. The market is projected to grow from USD 1.52 billion in 2026 to USD 2.65 billion by 2034, exhibiting a CAGR of 7.2% during the forecast period. North America dominated the aircraft tugs market with a market share of 35.21% in 2025.

Aircraft tugs are specialized ground support vehicles engineered to tow and position fixed-wing aircraft on aprons, taxiways, and within hangars without engine power. They are equipped with towbar or towbarless coupling systems, they optimize fuel efficiency, reduce engine wear, and enhance ramp safety. The global market is experiencing strong growth, driven by airport expansions across the globe, stringent emission-reduction regulations accelerating the shift to electric and hybrid models, and surging air traffic volumes requiring efficient ground handling.

- For instance, in December 2025, the U.K. Ministry of Defence directly awarded Terberg DTS (U.K.) a USD 7.24 million contract (including VAT) for maintenance, repair, and spare parts support of Medium Aircraft Towing Support (MATS) and Large Aircraft Towing Support (LATS) tractors.

Key players such as Textron Ground Support Equipment Inc. (TUG Technologies), JBT AeroTech Corporation, TLD Group (Alvest Group), and Tronair Inc. are focused on innovations such as electric powertrains for zero-emission operations, autonomous towing systems for reduced labor, and high-capacity pushback designs.

Download Free sample to learn more about this report.

AIRCRAFT TUGS MARKET TRENDS

Rapid Shift Toward Fully Electric Aircraft Tug Models is a Prominent Market Trend

Rapid shift toward fully electric aircraft tug models is driving the aircraft tugs market growth as airports prioritize sustainability during stringent emissions regulations. Diesel-powered tugs face phase-out pressures due to their high emissions and noise levels, prompting a surge in electric models that deliver zero tailpipe emissions and much quieter operations. Falling battery costs and other operational costs enable high-capacity packs with extended towing ranges for wide-body jets, eliminating refueling downtime. Moreover, there is an increase in the development of electric aircraft to cut emissions, fuel costs, and operational expenses.

- For instance, in January 2020, Holloman AFB tested TowFLEXX Miltech's electric aircraft tug with Evitado's LiDAR anti-collision under a Phase II SBIR contract.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stringent Environmental Regulations and Sustainability Mandates to Drive Market Growth

Global aviation authorities such as ICAO and regional bodies such as the EU enforce strict emissions targets for airport operations. Stringent environmental regulations and sustainability mandates drive the market by promoting airports to transition from diesel to electric models. Global standards from ICAO and EU Green Deal policies set strict emissions limits for ground operations, eliminating tolerance for high-polluting diesel tug solutions. Moreover, the net-zero commitments by major aviation hubs further accelerate adoption, positioning electric tugs as essential for maintaining competitive sustainability credentials and driving market growth.

MARKET RESTRAINTS

High Initial Costs to Limit Market Expansion

Aircraft tugs, also known as pushback tugs or tow tractors, face several key restraints that limit market growth. Advanced electric and hybrid tugs in the aviation sector require substantial upfront investment, deterring smaller airlines and airports from upgrades. Charging stations for electric tugs remain scarce, especially at smaller or developing airports, causing operational delays during peak hours. This limits the adoption of sustainable models driven by emissions regulations and restrains market growth.

MARKET OPPORTUNITIES

Rise in Air Traffic and Expansion of Airport Presents Market Growth Opportunities

Rise in air traffic and airport expansions represent key market opportunities for the aircraft tugs sector, driving demand for efficient ground support equipment. Global passenger and cargo volumes continue to surge post-pandemic, with airlines expanding fleets and prioritizing faster aircraft towing to minimize turnaround times. This necessitates more high-capacity tugs capable of handling wide-body jets, boosting sales across conventional, electric, and hybrid models. Airport infrastructure growth, especially new terminals and runways in high-growth regions such as Asia Pacific, requires larger tug fleets to support increased operations. Such factors are expected to create lucrative opportunities for the market.

MARKET CHALLENGES

Supply Chain Disruptions Act as a Challenge for Market

Supply chain disruptions represent a significant challenge for the market. Geopolitical tensions, semiconductor shortages, and lingering post-pandemic effects are delaying critical component deliveries, such as batteries and engines. This leads to production bottlenecks for manufacturers and to extended lead times for airports that need urgent fleet expansions. Smaller suppliers in the tug ecosystem face difficulties and regional availability issues in high-growth areas.

Segmentation Analysis

By Type

Eliminated Towbar Handling and Faster Turnarounds to Propel Towbarless Tugs Segment Growth

Based on type, the market is divided into towbar tugs and towbarless tugs.

The towbarless tugs segment leads the market as it eliminates towbar coupling/handling, reduces turnaround minutes per movement, and lowers the probability of towbar-related aircraft damage. For high-frequency commercial stands, this translates into higher asset utilization and faster gate release outcomes that airlines and handlers directly fund. Additionally, modern towbarless platforms are engineered to cover a wide aircraft envelope, enabling fleet standardization across multiple aircraft families, which strengthens procurement.

- For instance, in December 2025, KLM commissioned electric Goldhofer PHOENIX AST-2E tow tractors at Amsterdam Schiphol, explicitly emphasizing pushback/tow flexibility up to Boeing 777 class aircraft while replacing diesel units.

The towbar tugs segment is anticipated to rise with a steady CAGR of 6.0% over the forecast period.

By Towing Capacity

Efficient Towing Capabilities for Regional and Narrow-Body Aircraft Boosted Medium (15-75 tons) Segment Growth

By towing capacity, the market is segmented into light (less than 15 tons), medium (15-75 tons), heavy (75 to 150 tons), and extra heavy (more than 150 tons).

The medium (15-75 tons) segment held the largest market share in 2025. Segment growth is driven by surging demand for efficient towing of regional jets, business aircraft, and narrow-body planes amid rising air traffic and airport expansions. This segment benefits from its versatility in general aviation airports, fixed-base operators (FBOs), and maintenance facilities, where compact design, low maintenance, and ease of operation reduce operational costs. Increasing adoption of electric and hybrid variants supports global green airport initiatives and drives segment growth.

The heavy (75 to 150 tons) segment is projected to grow at a steady CAGR of 6.5% over the forecast period.

By Propulsion

High Torque for Heavy Wide-Body Towing at Lower Upfront Costs Propelled Diesel Segment Growth

By propulsion, the market is segmented into diesel, gasoline, battery electric, and hybrid electric.

The diesel segment held the largest market share in 2025. The segment is growing significantly in the market, as diesel tugs are widely used for their high torque and power-to-weight ratios, which are ideal for towing heavy wide-body aircraft, ensuring minimal downtime in high-intensity operations. Lower upfront costs compared to electric/hybrid alternatives make diesel tugs accessible for budget-constrained regional airports and smaller handlers.

The battery electric segment is projected to be the fastest-growing segment with a CAGR of 8.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Aircraft Type

Fleet Growth and Airport Expansions Boosted Commercial Aircraft Segment Expansion

Based on aircraft type, the market is segmented into commercial aircraft, general aviation, military aircraft, and regional aircraft.

The commercial aircraft segment dominated the market in 2025. Rising air traffic and airport expansions create increasing opportunities for market growth by increasing the need for reliable ground handling. Moreover, the commercial aircraft fleet growth, particularly narrow-body jets, fuels this demand as airlines expand short-haul fleets for high-frequency routes at busy hubs, driving segment growth.

The regional aircraft segment is expected to grow with the fastest CAGR of 6.3% over the forecast period.

By Application

Rising Air Traffic and Frequent Gate Departures Supported Pushback Operations Segment Growth

Based on application, the market is segmented into pushback operations, hangar towing, ground handling & safety, and others.

The pushback operations segment held the largest share of the market in 2025. Rising air traffic drives pushback tug demand as airlines handle more frequent gate departures requiring swift, reliable aircraft positioning. Airport expansions and new terminal constructions multiply pushback operations, necessitating larger fleets of conventional and towbarless tugs for simultaneous movements.

The ground handling & safety segment is projected to grow at a CAGR of 4.2% over the forecast period.

By End User

Standardization and Safety Upgrades to Boost Ground Handling Operators Segment Growth

On the basis of end user, the market is segmented into airlines, airports, ground handling operators, and others.

The ground handling operators segment is expected to acquire major market share in the coming years. Ground handling operators as end-users drive significant growth in the market through their operational demands and modernization needs. Standardization efforts among major handlers favor bulk tug purchases of compatible models for seamless multi-airport operations. Safety regulations mandate upgraded tugs with advanced braking and collision avoidance, replacing older equipment during fleet refresh cycles.

The airports segment is projected to emerge as the fastest-growing at a CAGR of 9.5% over the forecast period. Airports as end-users drive aircraft tug market growth through massive infrastructure expansions and new terminal constructions, necessitating larger tug fleets for handling surging passenger volumes and aircraft movements.

- For instance, in June 2025, Malé Velana International Airport is incorporating towbarless towing vehicles into its ground handling operations as part of a comprehensive equipment modernization program. The new tugs complement recently deployed passenger buses, aircraft stairs, loaders, and baggage tractors aimed at improving overall operational efficiency.

Aircraft Tugs Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Aircraft Tugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the aircraft tugs market share in 2025 with a valuation of USD 0.50 billion, growing to USD 0.54 billion in 2026, driven by extensive airport infrastructure, high air traffic volumes, and major fleet modernization programs at key U.S. hubs. Demand surges from pushback operations for narrow-body and wide-body fleets, alongside the adoption of electric and hybrid tugs to meet stringent emissions standards at urban airports.

U.S. Aircraft Tugs Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be approximated at around USD 0.48 billion in 2025. The U.S. dominates the regional market, fueled by capacity expansions at major carriers and ground handlers prioritizing rapid turnaround efficiency. Investments in sustainable ground equipment align with federal sustainability goals, sustaining strong demand for both conventional and advanced tug configurations.

Europe

Europe is projected to record a growth rate of 5.3% during 2026 to 2034. Europe exhibits robust growth in the market, propelled by airport expansions across the continent and regulatory pressure for low-emission ground operations. Major hubs modernize tug fleets to handle increased intra-European short-haul traffic while complying with EU environmental directives.

U.K. Aircraft Tugs Market

The U.K. market in 2025 was valued at USD 0.08 billion, representing roughly 5.5% of global revenues.

Germany Aircraft Tugs Market

The German market was valued at USD 0.06 billion in 2025, equivalent to around 4.5% of global sales.

Asia Pacific

The Asia Pacific market was valued at USD 0.43 billion in 2025 and secured the position of the second-largest region in the market. Asia Pacific is experiencing rapid expansion in the market, propelled by a rise in airport infrastructure investments across China, India, and other countries. Government-backed modernization programs prioritize electric tugs to address urban air quality concerns, which is anticipated to drive market growth.

Japan Aircraft Tugs Market

The Japan market in 2025 was valued at USD 0.04 billion, accounting for roughly 2.7% of global revenues.

China Aircraft Tugs Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 0.24 billion, representing roughly 16.7% of global sales.

India Aircraft Tugs Market

The India market in 2025 was valued at USD 0.04 billion, accounting for roughly 2.9% of global revenues.

Latin America and Middle East & Africa

The Latin America market registers modest yet steady growth, driven by regional security concerns and modernization programs. The Latin America market is growing steadily, anchored by tourism recovery and regional connectivity improvements across Brazil, Mexico, and Colombia. Moreover, in the Middle East & Africa region, Gulf carriers invest in advanced tug fleets for flagship wide-body operations, while African nations modernize ground handling to support continental connectivity initiatives and cargo growth.

COMPETITIVE LANDSCAPE

Emphasis on Electric Propulsion, Automation, and Fleet Standardization to Accelerate Market Expansion

The global aircraft tugs market centers on established ground support equipment manufacturers and innovative propulsion technology providers delivering efficient, operationally flexible towing solutions. The players in the market are focusing on electric powertrain integration, automated guidance systems, and standardized towbar interfaces compatible across diverse aircraft fleets. Leading participants such as TLD Group, Douglas Corporation, Mototok, and Kalmar deliver production-proven models through rigorous airport certification programs. Ongoing adoption of lithium-ion battery advancements, remote operation capabilities, and predictive maintenance analytics signals a transition from conventional diesel dominance to sustainable, digitally enabled ground-handling ecosystems.

LIST OF KEY AIRCRAFT TUG COMPANIES PROFILED

- TLD Group (France)

- Kalmar Motor AB (Sweden)

- Textron GSE (U.S.)

- Goldhofer AG (Germany)

- Oshkosh AeroTech (U.S.)

- TREPEL Airport Equipment (Germany)

- MULAG Fahrzeugwerk (Germany)

- Mototok International (Germany)

- Tronair (U.S.)

- ZAGtruck GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Arrobot, a DeepTech subsidiary of Raghu Vamsi Aerospace Group, unveiled autonomous ground tugs for aircraft and helicopters at India Wings 2026 in Hyderabad. It is designed to boost airside efficiency, safety, and turnaround times through intelligent operator-assisted and fully autonomous operations.

- January 2025: TLD Group accelerated electric aircraft tractor development across its range, replacing diesel models with efficient battery-powered versions that deliver both environmental and performance gains.

- August 2024: Goldhofer AG signed a framework agreement with EFM GmbH to deliver 14 Phoenix E electric towbarless tractors to Munich Airport by 2028, marking the company's largest order to date. The battery-electric Phoenix E handles aircraft up to 352-tonne MTOW at speeds of 32 km/h, matching diesel performance with zero emissions and lower operating costs.

- August 2024: Japan Airlines introduced Japan's first electric towing tug for narrow-body aircraft at Naha Airport in Okinawa, deploying TLD's TMX-150-E model optimized for Boeing 737s through A321neo and COMAC C919.

- January 2024: Aurrigo International established its first U.S. office at Cincinnati/Northern Kentucky International Airport (CVG) to deploy the Auto-DollyTug, a fully electric autonomous vehicle for cargo and baggage handling. The innovative tug combines tractor and dolly functions, towing four trailers with five ULDs for 30% higher capacity and 60% carbon reduction versus diesel models.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size & forecast by all the aircraft tugs market segmentations included in the report. It includes details on the market dynamics, market trends, and regional analysis expected to drive the market over the forecast period. The market report includes a Porter's Five Forces analysis, which illustrates the power of buyers and suppliers in the market. Market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers & acquisitions. The market analysis also includes a detailed competitive landscape, with information on market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, By Propulsion, By Towing Capacity, By Aircraft Type, By Application, By End User, and Region |

| By Type |

|

| By Towing Capacity |

|

| By Propulsion |

|

| By Aircraft Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.42 billion in 2025 and is projected to reach USD 2.65 billion by 2034.

In 2025, the market value of North America stood at USD 0.50 billion.

The market is expected to exhibit a CAGR of 7.2% during the forecast period of 2025-2034.

By propulsion, the diesel segment led the market.

Rise in air traffic, stringent environmental regulations, and sustainability mandates are driving market expansion.

TLD Group, JBT AeroTech, and Textron GSE are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 201

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us