Aircraft Turbofan Engine Market Size, Share & Industry Analysis, By Platform (Commercial Aviation (Narrow-body, Wide-body, and Regional Jets), Fighters, Military Transport, and Other Aircraft) , By Component (Compressor, Turbine, Fan, Gear Box, and Others), By Turbofan Engine Type (Low Bypass (Non, Afterburning Low-Bypass Turbofan, Afterburning Low-Bypass Turbofan, and others) and High Bypass (Conventional High-Bypass Turbofan, Geared Turbofan (GTF), Separate-Flow High-Bypass Turbofan, and others), and By Sales Channel (Linefit and Retrofit), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

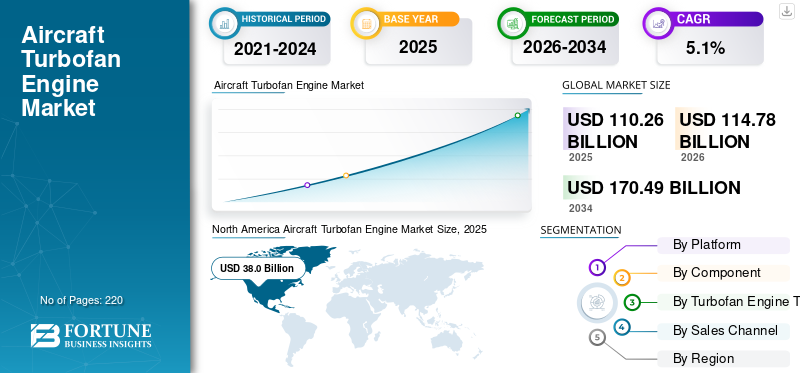

The global aircraft turbofan engine market size was valued at USD 110.26 billion in 2025. The market is projected to grow from USD 114.78 billion in 2026 to USD 170.49 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period. North America dominated the global market with a market share of 34.46% in 2025.

The global market is expected to experience steady and strong growth, driven by increasing aircraft deliveries, rising demand for fuel-efficient propulsion systems, and continuous fleet modernization programs across commercial and military aviation. Turbofan engines remain the preferred engine type in modern fixed-wing aircraft due to their high thrust-to-weight ratio, fuel efficiency, and lower noise emissions compared to older engine technologies. In addition, the advancements in engine designs and propulsion architecture is driving market growth.

- For instance, Pratt & Whitney launched Hot Section Plus (HS+), an upgrade for PW1100G-JM engines on Airbus A320neo aircraft, offering up to 95% of the GTF Advantage engine’s durability benefits.

Furthermore, many key industry players, such as GE Aerospace, Rolls-Royce Holdings plc, and Safran, and others are focused on developing advanced engine propulsion and expanding their global presence and gaining competitive edge through collaborative programs, technology partnerships, and expanded MRO service networks.

Download Free sample to learn more about this report.

AIRCRAFT TURBOFAN ENGINE MARKET TRENDS

Advancements in Engine Technology is a Prominent Trend Market Observed

Advancements in engine technology have emerged as a prominent trend in the global aircraft turbofan engine industry. Manufacturers are developing high-bypass ratio engines, hybrid-electric propulsion, and Geared Turbofan (GTF) upgrades to achieve superior fuel efficiency, reduced emissions, and extended durability. In addition, key players are constantly developing and testing advanced engine technology to reduce cost and weight across multiple platforms.

- In September 2025, Pratt & Whitney completed critical testing on its small turbofan engine family which was originally designed for commercial aircraft. The engine testing confirms a 20% thrust increase for next-generation Collaborative Combat Aircraft (CCA).

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increase in Aircraft Production and Deliveries is Expected to Drive Market Growth

A key driver for the aircraft turbofan engine market is the steady rise in global aircraft production and deliveries, fueled by strong recovery in passenger traffic and expanding airline fleets. Major airframers such as Airbus and Boeing are increasing the manufacturing rates to meet growing demand for commercial aircraft, directly driving engine procurement volumes in the aviation industry.

- According to the International Air Transport Association (IATA), the total full-year traffic in 2024, rose 10.4% compared to 2023. Moreover, as per International Civil Aviation Organization (ICAO), global passenger traffic is forecast to exceed 12 billion by 2030.

As the air traffic rises, there is an increase in the development of new-generation single-aisle and wide-body models further supporting demand for high-performance turbofan engines.

MARKET RESTRAINTS

High Development and Maintenance Costs to Limit Market Expansion

The design, certification, and lifecycle management of advanced turbofan engines involve high capital and technical complexity. OEMs are required to invest heavily in R&D expenditures to build engines that meet stringent efficiency and emission targets. Moreover, operators face high maintenance costs due to specialized parts and digital monitoring systems. These cost factors prolong return-on-investment timelines and deter new entrants, hampering the aircraft turbofan engine market growth.

MARKET OPPORTUNITIES

Advancements in Sustainable and Hybrid Propulsion Presents Growth Opportunities for Market Growth

The global push toward sustainable aviation is creating significant opportunities for turbofan engine innovation. Manufacturers are investing in hybrid-electric propulsion, hydrogen-fueled engines, and advanced materials to enhance performance while reducing carbon footprint. These advancements align with ICAO and IATA sustainability goals, encouraging collaborative R&D and funding initiatives for sustainable solutions. Major players in the industry are focusing on the development of sustainable engine technology that burns significantly less fuel, cuts CO2 and noise, which presents lucrative opportunities for the market.

- In April 2025, Rolls-Royce launched the UltraFan demonstrator that uses geared architecture, composite fan blades, and lean-burn combustion. It operates on 100% SAF, and targets step-change efficiency and emissions reductions.

MARKET CHALLENGES

Supply Chain and Raw Material Volatility Acts a Challenge for the Market

Persistent supply chain disruptions and raw material shortages remain critical challenges for engine manufacturers. The availability of titanium, nickel-based alloys, and composite materials has been affected by geopolitical tensions, logistics delays, and capacity restraints. Such constraints disrupt production schedules, increase procurement costs, and limit OEMs’ ability to meet delivery timelines.

Segmentation Analysis

By Platform

Rise in Global Air Passenger Traffic And Fleet Expansion Propel Commercial Aviation

Based on platform, the market is divided into commercial aviation, fighters, military transport, business jets, regional jets, special-mission, and other aircraft.

The commercial aviation segment is anticipated to account for the largest market share. The dominant position is due to surging global air passenger traffic and expanding airline fleets. Moreover the segment’s growth is driven by high-volume production of single-aisle and wide-body aircraft by major OEMs such as Airbus and Boeing.

- For instance, in October 2025, Boeing is ramping up 737 MAX production from 38 to 42 jets per month pending FAA approval, with plans to reach 53 by late next year at its Renton facility.

The business jet segment is anticipated to rise with a CAGR of 6.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Critical Role in Energy Extraction and Engine Tech Advancement Drives Demand for Turbines

By component, the market is segmented into compressor, turbine, fan, gear box, combustor, and others.

The turbine segment holds the largest aircraft turbofan engine market share due to its essential function in extracting energy from hot gases to drive the compressor and fan. Ongoing innovations in cooling technologies and additive manufacturing to reduce weight and enhance durability is expected to drive segment growth. Moreover, various countries are strengthening the domestic aero-engine ecosystem with advancement in engine technology for multiple platforms which helps in market expansion.

- In October 2024, Gas Turbine Research Establishment (GTRE), proposed building a new and more powerful jet engine. This non-afterburning twin-spool turbofan, is expected to feature a four-stage axial compressor, annular combustor, and single-stage turbine.

The gearbox segment is projected to grow at a CAGR of 7.6% over the forecast period.

By Turbofan Engine Type

Superior Fuel Efficiency and Regulatory Compliance Push High Bypass Segment Growth

Based on turbofan engine type, the market is segmented into low bypass and high bypass.

High bypass accounts for the largest market share due to superior fuel efficiency and regulatory compliance. High-bypass ratios deliver superior fuel efficiency and reduced noise, making them ideal for modern commercial airliners. Moreover, regulatory pressures for lower emissions continue to favor high-bypass architectures over alternatives.

The low-bypass segment is expected to grow with a steady CAGR of 3.9% over the forecast period.

By Sales Channel

OEM Integration in New Aircraft Production & Deliveries Support Conventional Control System Segment Growth

Based on sales channel, the market is segmented into linefit and retrofit.

The linefit segment is forecast to capture the largest market share. Linefit engines are integrated during original aircraft manufacturing, benefiting from OEM design optimization and volume procurement by airframers for new deliveries.

- For instance, in June 2025, Rolls-Royce secured a USD 2.5 billion linefit contract for Trent XWB engines on 100+ Airbus A350 orders from Middle Eastern carriers.

Retrofit is projected to emerge as the fastest-growing segment at a CAGR of 5.4% over the forecast period.

Aircraft Turbofan Engine Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

North America

North America Aircraft Turbofan Engine Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025 valuing at USD 38.0 billion and is also expected to hold a leading share in 2026 with USD 39.7 billion due to the rise in aircraft deliveries, fleet modernization programs, and strong aftermarket service activity across both commercial and defense aviation segments. The presence of leading OEMs such as GE Aerospace and Pratt & Whitney and heavy investment in advanced propulsion technologies is further driving the aircraft turbofan engine demand in the region.

U.S Aircraft Turbofan Engine Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 36.4 billion in 2025. The country maintains its leading position due to high commercial aircraft production, and large military modernization budgets.

- In January 2025, US Air Force expanded funding for its Next Generation Adaptive Propulsion (NGAP) program, adding up to USD 2.5 billion and raising the potential value for both Pratt & Whitney and GE Aerospace to USD 3.5 billion each in R&D for future air-dominance engines.

Europe

Europe is projected to record a growth rate of 4.6% during 2026 to 2034, which is the second highest among all regions. The growth is supported by an expanding aircraft backlog, particularly in the A320neo and A350 programs, along with rising adoption of new-generation geared turbofan engines. In addition, the stringent emission regulations imposed by the European Union are accelerating innovation in low-noise, fuel-efficient engines and sustainable propulsion research.

- In December 2025, the European Union passed a new climate law requiring a 90% cut in greenhouse gas emissions by 2040 compared to 1990 levels.

U.K Aircraft Turbofan Engine Market

The U.K. aircraft turbofan engine market in 2025 is estimated at around USD 6.7 billion, representing roughly 6.1% of global aircraft turbofan engine revenues.

Germany Aircraft Turbofan Engine Market

Germany’s market is projected to reach approximately USD 5.6 billion in 2025, equivalent to around 5.1% of global aircraft turbofan engine sales.

Asia Pacific

Asia Pacific reached USD 27.0 billion in 2025 and secured position of the third-largest region. India and China accounted for USD 5.6 billion and USD 9.0 billion, respectively in 2025.

Japan Aircraft Turbofan Engine Market

The Japan aircraft turbofan engine market in 2025 was valued at USD 4.0 billion, accounting for roughly 3.6% of global aircraft turbofan engine revenues.

Japan’s aerospace sector actively collaborates with major engine manufacturers through joint development programs for advanced civil and defense platforms.

- In May 2025, Honeywell proposed its high-performance F124 turbofan engine for Japan's T-4 trainer replacement and Collaborative Combat Aircraft programs.

China Aircraft Turbofan Engine Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues at around USD 9.0 billion, representing roughly 8.2% of global aircraft turbofan engine sales.

India Aircraft Turbofan Engine Market

The Indian market in 2025 was around USD 5.6 billion, accounting for roughly 5.0% of global aircraft turbofan engine revenues.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 5.7 billion in 2025, driven by rise in commercial aircraft procurement in Brazil and Mexico and modernization of regional fleets. In the Middle East & Africa, Saudi Arabia is set to reach a value of USD 2.90 billion in 2025.

Saudi Arabia Aircraft Turbofan Engine Market

The Saudi Arabia aircraft turbofan engine market is projected to reach around USD 2.90 billion in 2025, representing roughly 2.6% of global aircraft turbofan revenues. The airline industry in Saudi Arabia is significantly increasing engine procurement with major orders to support the surging air traffic.

- For instance, in November 2025, Riyadh Air ordered 120 CFM International LEAP-1A engines to power its new fleet of 60 Airbus A321neo aircraft to handle 330 million passengers and 4.5 million tons of cargo annually.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Next-Generation Engine Development by Key Players to Propel Market Progress

The global aircraft turbofan engine market is dominated by major OEMs such as GE Aerospace, Pratt & Whitney (RTX Corporation), and Rolls-Royce Holdings plc. These companies hold significant market share through strategic investments in advanced propulsion technologies, and collaboration with various countries.

In November 2025, Safran committed to co-developing a brand-new jet engine from scratch with India, moving beyond its earlier M88 derivative proposal to meet the performance needs of future Indian combat aircraft.

Other notable players include Safran Aircraft Engines, MTU Aero Engines AG, and CFM International. These firms are prioritizing joint ventures, R&D collaborations, and production scale-ups to increase aircraft turbofan engine market share.

LIST OF KEY AIRCRAFT TURBOFAN ENGINE COMPANIES PROFILED

- GE Aerospace (U.S.)

- Pratt & Whitney (U.S.)

- Rolls-Royce (U.K.)

- Safran (France)

- CFM International (U.S.)

- MTU Aero Engines (Germany)

- Honeywell Aerospace (U.S.)

- IHI Corporation (Japan)

- Kawasaki Heavy Industries (Japan)

- Aviadvigatel (Russia)

KEY INDUSTRY DEVELOPMENTS

- November 2025: India signed a deal with General Electric to procure 113 engines for the Tejas Mk-1A fighter jets, strengthening its indigenous aircraft program amid deepening defense ties with the U.S.

- October 2025: GE Honda Aero Engines announced that it is assessing the business aviation market for a potential new turbofan engine larger than its current HF-120, which powers the HondaJet VLJ.

- October 2025: GE Aerospace plans to deliver its 500th Passport turbofan engine to power Bombardier’s Global 8000 business jet

- June 2025: Pratt & Whitney received nearly 1,100 GTF engine orders and commitments since early 2025 from airlines including Aegean, Air Niugini, ANA, Frontier, LOT Polish, and Wizz Air, plus two undisclosed customers. The geared turbofan now totals over 12,000 orders from more than 90 global customers.

- June 2025: Wizz Air has selected Pratt & Whitney’s PW1100G-JM geared turbofan engines to power 177 additional Airbus A321neo aircraft.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.1% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform, Component, Turbofan Engine Type, Sales Channel, and Region |

|

By Platform |

· Commercial Aviation o Narrow-body o Wide-body o Regional Jets · Fighters · Military Transport · Business Jets · Regional Jets · Special-Mission · Other Aircraft |

|

By Component |

· Compressor · Turbine · Fan · Gear Box · Combustor · Others |

|

By Turbofan Engine Type |

· Low Bypass o Non-Afterburning Low-Bypass Turbofan o Afterburning Low-Bypass Turbofan o Mixed-Flow Low-Bypass Turbofan · High Bypass o Conventional High-Bypass Turbofan o Geared Turbofan (GTF) o Separate-Flow High-Bypass Turbofan o Ultra-High-Bypass / Open Rotor (Advanced Concept) |

|

By Sales Channel |

· Linefit · Retrofit |

|

By Geography |

· North America (By Platform, Component, Turbofan Engine Type, Sales Channel, and Country) o U.S. (By Platform) o Canada (By Platform) · Europe (By Platform, By Component, Turbofan Engine Type, Sales Channel, and Country) o U.K. (By Platform) o Germany (By Platform) o France (By Platform) o Russia (By Platform) o Rest of Europe (By Platform) · Asia Pacific (By Platform, Component, Turbofan Engine Type, Sales Channel, and Country) o China (By Platform) o Japan (By Platform) o India (By Platform) o South Korea (By Platform) o Rest of Asia Pacific (By Platform) · Latin America (By Platform, Component, Turbofan Engine Type, Sales Channel, and Country) o Brazil (By Platform) o Mexico (By Platform) o Rest of Latin America( By Aircraft Type) · Middle East & Africa (By Platform, Component, Turbofan Engine Type, Sales Channel, and Country) o UAE (By Platform) o Saudi Arabia (By Platform) o Rest of the Middle East & Africa (By Platform) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 110.26 billion in 2025 and is projected to reach USD 170.49 billion by 2034.

In 2025, North Americas market value stood at USD 38.0 billion.

The market is expected to exhibit a CAGR of 5.1% during the forecast period of 2025-2034.

By platform, the commercial aviation segment is expected to lead the market.

The increase in aircraft production and deliveries due to rising air traffic are driving market expansion.

GE Aerospace (U.S.), Pratt & Whitney (U.S.), Rolls-Royce (U.K.), and Safran (France) are some of the major players in the global market.

North America dominated the market in 2025 in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us