Algae-based Bioplastics Market Size, Share & Industry Analysis, By Type (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polyethylene (PE), Polyethylene Terephthalate (PET), and Others), By Application (Packaging, Consumer Goods, Textile, Agriculture, Automotive, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

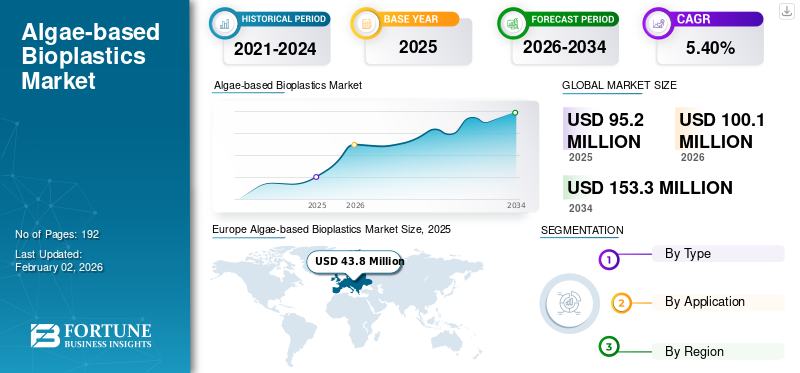

The global algae-based bioplastics market size was valued at USD 95.2 million in 2025. The market is projected to grow from USD 100.1 million in 2026 to USD 153.3 million by 2034 at a CAGR of 5.40% during the forecast period. Europe dominated the algae-based bioplastics market with a market share of 46.00% in 2025.

Algae-based bioplastics are a type of bioplastics material derived from algae biomass. Unlike traditional petroleum-based plastics, algae-based bioplastics are made by cultivating algae, harvesting their biomass, extracting valuable biopolymer compounds (such as starches and polyhydroxyalkanoates), and processing these into plastic resins or composites.

Demand for algae-based bioplastics is rising rapidly in the global market, driven by sustainability priorities, regulatory actions, and advancements in algae cultivation and processing. Notpla Limited, Lifeasible, BZEOS, and Eranova are the key players operating in the market.

Download Free sample to learn more about this report.

Algae-based Bioplastics Market Trends

Regulatory Pressure & Sustainability Mandates To Boost Market Growth

Regulatory pressure (single-use bans, plastic packaging taxes, and EPR schemes) combined with corporate sustainability mandates is creating a concrete commercial pathway for algae/seaweed-based bioplastics. These policies raise the cost of non-compliant packaging, prioritize compostable/biobased options in procurement, and unlock public/private funding for scale-up, all of which reduce adoption barriers for algae-derived films and resins, as evidenced by policy texts (EU Single-Use Plastics Directive), industry guidance (European Bioplastics), and accelerating startup activity.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Sustainability & Carbon Neutrality Driving Market Growth

Sustainability and carbon neutrality are central to the advancement and demand for algae-based bioplastics, making them attractive alternatives to conventional plastics for companies and regulators focused on climate goals and environmental impact reduction.

Algae-based bioplastics are considered highly sustainable as they avoid competition with food crops and do not require arable land or freshwater for cultivation. Algae can be grown in a variety of environments, including saline, brackish, and wastewater, minimizing resource burden and environmental degradation. Their rapid growth rate and high biomass yield further support a sustainable feedstock model, capable of scaling without displacing food systems.

Market Restraints

High Production Costs Are Restraining Market Growth

Algae demand to control the environment’s light, temperature, and nutrients often in photobioreactors or open ponds. These systems are energy-intensive and capital-heavy, pushing up baseline costs.

Current methods to isolate biopolymers from algae involve multi-step, low-yield procedures such as cell disruption, purification, and drying. Each step adds cost and complexity, and the yield per kg of biomass remains low. The market is still nascent, with few large-scale facilities. Low production volumes prevent cost degression, keeping per-unit prices several times higher than conventional plastics.

Market Opportunities

Innovation in Blends & Composites Creates an Opportunity for Market

Blending algae-derived biomass with established bioplastics such as PLA and starch, as well as fossil-based polymers such as LDPE, improves the mechanical, thermal, and barrier properties of the final composites. Algae-starch blends, for instance, increase biodegradability and film-forming characteristics, with higher starch ratios quickening the degradation rate and reducing environmental impact. Algae-PLA composites maintain high tensile strength, making them suitable for packaging and agriculture.

Composite innovation helps reduce production costs and improve sustainability. Using microalgal biomass produced in wastewater treatment ponds lowers feedstock and energy costs, making algae-based bioplastics more economical.

Market Challenges

Competing with Established Feedstocks Challenging Market

The market faces substantial challenges competing with established feedstocks, primarily conventional plastics and crop-based bioplastics including those derived from corn or sugarcane. Algae-based bioplastics have higher production costs compared to conventional plastics, largely due to complex cultivation and processing requirements. This price gap restrains their competitiveness in cost-sensitive applications.

Trade Protectionism and Geopolitical Impact

Protectionist Policies and Trade Barriers to Restrict Market Growth

Tariffs and import-export restrictions impact the cost and availability of raw materials and bioplastic products globally, affecting the competitiveness of algae-based bioplastics in different regions. Countries and regions are increasingly investing in local algae cultivation and bioplastic manufacturing to reduce dependence on imports and mitigate risks related to trade barriers.

Research And Development (R&D) Trends

Government Funding for New Technology to Create Opportunities for Market Growth

Increasing efforts in pilot and demonstration-scale projects worldwide, including EU-funded initiatives such as the Nenu2PHAr project, which develop microalgae-based PHA bioplastics as sustainable alternatives to petrochemical plastics.

Startups and specialized companies (Eranova, Notpla, Sway Innovation) are advancing the commercialization of algae-based films, coatings, 3D printing filaments, and injection-molded products.

Segmentation Analysis

By Type

Polyhydroxyalkanoates (PHA) Segment Dominates Market Due to Its Biodegradable Ability

On the basis of type, the market is segmented into Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polyethylene (PE), Polyethylene Terephthalate (PET), and others.

The Polylactic Acid (PLA) segment is projected to dominate the market with a share of 40.56% in 2026. PLA is highly demanded for its biodegradability, clarity, and rigidity, widely used in packaging, consumer goods, textiles, and more. Also, regulatory support for the product is positively impacting the market growth.

The Polyhydroxyalkanoates (PHA) segment registers a notable growth during the forecast period. PHA is favored for biodegradability and versatility, used in packaging and agriculture films. Advances in production bolster growth potential.

Others types will also register a positive growth during the forecast period. It includes novel blends and composite bioplastics developed for specialized applications.

By Application

To know how our report can help streamline your business, Speak to Analyst

Packaging Segment Dominates Market Due to Product’s Use As A Sustainable Feedstock In Numerous Applications

On the basis of application, the market is segmented into packaging, consumer goods, textiles, agriculture, automotive, and others.

The packaging segment is projected to dominate the market with a share of 49.24% in 2026. Driven by demand for eco-friendly, biodegradable packaging in various applications. Innovations focus on barrier properties and shelf-life extension, which also positively demand the market.

The consumer goods segment will register a notable growth during the forecast period. The market growth is fueled by rising consumer sustainability awareness and demand for biodegradable alternatives. Similarly, the automotive application is also positively growing in the near future. Its uses include biodegradable interior components and parts. The product adoption is driven by sustainability initiatives in automotive manufacturing and the potential for weight reduction.

Others applications attributed positive growth in the study period. Niche applications such as electronics, healthcare, coatings, adhesives, and 3D printing filaments are covered in this sector. These areas are expanding through innovation in material properties and bioplastic formulations.

Algae-based Bioplastics Market Regional Outlook

By region, the market is segmented into North America, Europe, Asia Pacific, and Rest of the World.

Europe

Europe Algae-based Bioplastics Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The Europe market was valued at USD 43.8 million in 2025, capturing 46.00% of global revenue, and is estimated to reach USD 46.2 million in 2026. The strong environmental regulations (e.g., EU single-use plastic directives) and robust circular economy frameworks make it more demanding in the region. Stringent policy measures and increasing consumer preference for green products support Europe's algae-based bioplastics market growth. The UK market is projected to reach USD 6.85 million by 2026, while the Germany market is projected to reach USD 19.54 million by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

North America accounted for USD 25.4 million in 2025, representing 27.00% of the global market share, and is projected to reach USD 26.6 million in 2026. North America is a significant player in the market, with strong government support and advanced technological infrastructure contributing to its growth. The U.S. and Canada are prominent players, with startups and established firms advancing commercialization and innovation in algae bioplastics. The U.S. held the largest revenue share within North America in 2024, fueled by demand from the packaging and consumer goods sectors. The U.S. market is projected to reach USD 21.1 million by 2026.

Asia Pacific

In 2025, Asia Pacific held 23.00% of the global market, reaching a valuation of USD 22.1 million, and is projected to grow to USD 23.2 million in 2026. Asia Pacific is also a positive contributor to the market. Growth is supported by abundant algae resources, government environmental initiatives, and increasing industrial investments, especially in China, India, and Japan. The Japan market is projected to reach USD 3.53 million by 2026, the China market is projected to reach USD 9.67 million by 2026, and the India market is projected to reach USD 7.14 million by 2026.

China leads with strong R&D and manufacturing infrastructure, favorable government policies, and subsidies promoting bioplastic development.

Rest of the World

Rest of the world contributed approximately USD Rest of World - 3.9 million to the global market in 2025, accounting for Rest of World - 4.1% share, and is expected to reach USD Rest of World - 4.1 million in 2026.Latin America registers notable growth due to rising environmental awareness, growing waste-management concerns, and regulatory pressure on single-use plastics. Similarly, the Middle East & Africa region is exploring growth in the market. Growth is prompted by increased sustainability investment, environmental legislation, and new market entrants focused on green solutions.

Competitive Landscape

Key Market Players

Key Players Adopted an Expansion Growth Strategy to Maintain Their Dominance in Market

In terms of the competitive landscape, the market represents the presence of emerging and established companies. UPM Biofuels, Chevron, Mitsui Chemicals, and Neste Oil Corporation are the major players in this market. These companies possess substantial production capabilities and manufacture products for industry-specific applications. They are also expanding their manufacturing capacity and sales and distribution network across the globe.

List of Key Algae-based Bioplastics Companies Profiled

- Notpla Limited (U.K.)

- Algix LLC (U.S.)

- Lifeasible (U.S.)

- Evoware (Indonesia)

- BZEOS (Spain)

- FLEXSEA (U.S.)

- Eranova (France)

- Sway Innovation Co. (U.S.)

- ALGBIO (Turkey)

- PT Seaweedtama Biopac Indonesia (Indonesia)

KEY INDUSTRY DEVELOPMENTS

- September 2024: Waste2Plastic project at Umeå University was awarded approximately USD 1.54 million from the Swedish Energy Agency and industrial partners. The project focuses on developing biodegradable plastics, specifically polyhydroxyalkanoates (PHA), using locally sourced Nordic microalgae as feedstock.

- February 2024: Somater, a leading French packaging manufacturer, partnered with biotech start-up Eranova to launch ALGX, a 100% bio-based polymer packaging material made from green algae harvested at the Étang de Berre lagoon in France.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, types, compositions used to produce products, and applications. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, it encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million) and Volume (Kiloton) |

|

Growth Rate |

CAGR of 5.40% from 2026 to 2034 |

|

Segmentation |

By Type, Application, and Region |

|

By Type |

|

|

By Application |

|

|

By Region |

North America (By Type, By Application, By Country)

Europe (By Type, By Application, By Country)

Asia Pacific (By Type, By Application, By Country)

Rest of the World (By Type, By Application, By Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 95.2 million in 2025 and is projected to record a valuation of USD 153.3 million by 2034.

In 2025, the Europe market value stood at USD 43.8 million.

Recording a CAGR of 5.40%, the market will exhibit steady growth during the forecast period.

In 2026, packaging is the leading segment in the market by application.

Sustainability & carbon neutrality is a key factor driving the growth of the market.

Europe is poised to capture the highest market share during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 192

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us