Alumina Short Fiber Market Size, Share & Industry Analysis, By Application (Thermal Insulation For Refractories, Composite Materials, Exhaust Gas Catalyst Mat, Filtration, Glass Protection, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

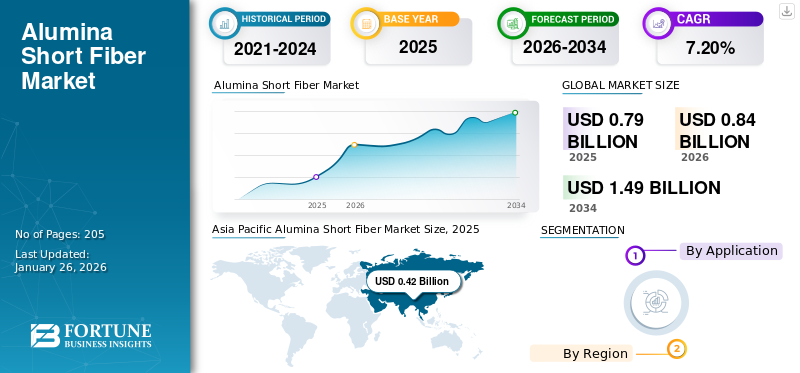

The global alumina short fiber market size was valued at USD 0.79 billion in 2025. The market is projected to grow from USD 0.84 billion in 2026 to USD 1.49 billion by 2034, exhibiting a CAGR of 7.20% during the forecast period. Asia Pacific dominated the alumina short fiber market with a market share of 53% in 2025.

Alumina short fiber is a high-performance ceramic material composed primarily of aluminum oxide (Al₂O₃) in a short, fibrous form. It is characterized by exceptional thermal stability, high strength, low density, and excellent resistance to corrosion, wear, and oxidation. Additionally, these fibers also exhibit good electrical insulation and low thermal conductivity, making them suitable for demanding environments. Widely used in industries such as aerospace, automotive, electronics, and metallurgy, they serve applications such as thermal insulation, reinforcing composites, and improving material performance under extreme conditions. Their lightweight, durability, and adaptability make them critical for advancing energy efficiency and technological innovation.

The COVID-19 pandemic disrupted the alumina short fiber market, causing supply chain interruptions, reduced industrial activities, and delays in key sectors such as manufacturing, aerospace, and automotive. Declining demand and logistical challenges further impacted production and distribution. However, post-pandemic, the market has recovered significantly due to an increased focus on advanced manufacturing driven by sustainability-driven innovations.

Download Free sample to learn more about this report.

Alumina Short Fiber Market Key Takeaways

- 2025 Market Size: USD 0.79 billion

- 2026 Market Size: USD 0.84 billion

- 2034 Forecast Market Size: USD 1.49 billion

- CAGR: 7.20% from 2026–2034

- Asia Pacific dominated the market with a 53.00% share in 2025.

- The Thermal Insulation for Refractories segment is projected to account for 47.62% of the market in 2026.

- The Exhaust Gas Catalyst Mats segment is expected to witness strong growth, driven by stringent emission standards and automotive catalyst demand.

Asia Pacific

Asia Pacific recorded USD 0.42 billion in 2025 and is expected to grow to USD 0.45 billion in 2026.

North America

North America reached USD 0.13 billion in 2025 and is projected to grow to USD 0.14 billion in 2026.

Europe

Europe generated USD 0.17 billion in 2025 and is projected to reach USD 0.18 billion in 2026.

U.S.

U.S. market is estimated to reach USD 0.12 billion by 2026.

Japan

Japan market is estimated to reach USD 0.03 billion by 2026.

Read More

ALUMINA SHORT FIBER MARKET TRENDS

Rising Emphasis on Sustainable Manufacturing to Create Market Growth Opportunities

The growing emphasis on sustainable manufacturing is driving new market trends in the alumina short fiber industry. As industries across the globe adopt greener practices, there is a rising demand for materials that align with sustainability goals while delivering high performance. With their durability, recyclability, and ability to improve energy efficiency, these fibers are gaining popularity as a sustainable material choice in various applications. Their use in lightweight composites helps reduce fuel consumption and emissions in the automotive and aerospace sectors, aligning with global carbon reduction targets. Moreover, advancements in environmentally friendly production methods, such as using renewable energy sources and reducing waste during manufacturing, further enhance their appeal. Companies adopting circular economy principles and offering sustainable material solutions are likely to gain a competitive edge. This shift toward sustainability is driving innovation and creating new growth opportunities for the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Investments in Advanced Manufacturing Technologies to Drive Market Growth

Rising investments in advanced manufacturing technologies are expected to significantly drive demand for alumina short fibers, owing to their critical role in enhancing material performance across high-tech applications. Advanced manufacturing processes, such as composite fabrication, require materials that can withstand extreme conditions while offering superior strength-to-weight ratios, thermal stability, and durability. These fibers, with their exceptional properties, are integral to the production of next-generation components in the aerospace, automotive, electronics, and energy sectors. For instance, in the aerospace industry, these fibers are used to reinforce lightweight composites, improving fuel efficiency and performance. In electronics and energy, they enhance thermal management and insulation for cutting-edge devices. Additionally, as industries increasingly adopt smart manufacturing systems and prioritize sustainability, these fibers are gaining prominence for their ability to improve energy efficiency and reduce waste. This surge in technological advancements and the shift toward lightweight, durable, and high-performance materials are likely to play a critical role in shaping the future of modern manufacturing driving market growth in tandem.

The increasing demand for high-performance materials in the aerospace and automotive industries is another factor driving market growth. These fibers enhance lightweight composites by improving strength, thermal stability, and durability, which are critical for fuel efficiency, reduced emissions, and performance under extreme conditions, making them irreplaceable in advanced vehicle and aircraft manufacturing.

MARKET RESTRAINTS

Competition from Alternative Materials to Restrict Market Growth

Competition from alternative materials, such as carbon fiber and glass fiber, presents a significant challenge to the alumina short fiber market growth. These alternatives are widely used due to their lower cost, widespread availability, and established manufacturing processes. Carbon fiber offers excellent strength-to-weight ratios, making it a preferred choice in aerospace and automotive applications. In contrast, glass fiber is favored for its affordability and versatility across various industries. Additionally, the high production costs of high-purity alumina short fibers and limited awareness of their unique advantages also contribute to their restricted adoption. As industries prioritize cost-effectiveness, particularly in mass-market applications, these fibers face difficulties in competing with these well-established alternatives. Overcoming this challenge requires focused efforts in cost optimization, strategic marketing, and spreading awareness of alumina fiber's benefits.

MARKET CHALLENGES

High Production Complexity and Cost of Advanced Alumina Short Fibers to Pose Challenges

The high production complexity and cost of advanced fibers present significant challenges to market growth. Manufacturing these fibers involves intricate processes, such as precise chemical synthesis and thermal treatments, which require specialized equipment and expertise. This results in higher production costs compared to alternative materials such as carbon and glass fibers. Additionally, the energy-intensive nature of production further increases operational expenses, limiting the scalability and affordability of these fibers. These cost constraints hinder adoption in price-sensitive markets, making it difficult for manufacturers to compete effectively. Manufacturers require innovations in production efficiency and cost optimization strategies to address these challenges.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy to Create Market Growth Opportunity

The emerging applications of these fibers in the renewable energy sector are poised to create significant market growth opportunities. As the global shift toward sustainable energy solutions accelerates, the demand for high-performance materials capable of operating under extreme conditions is increasing. These fibers, known for their thermal stability, corrosion resistance, and durability, are ideal for critical components in renewable energy systems such as wind turbines, solar panels, and energy storage devices. For instance, these fibers enhance the performance and longevity of composite materials used in turbine blades and insulation components in energy storage systems. As investments in renewable energy technologies continue to rise, the unique properties of these fibers position them as essential materials, driving innovation and growth in this sector.

SEGMENTATION ANALYSIS

By Application

To know how our report can help streamline your business, Speak to Analyst

Growing Focus on Enhancing Energy Efficiency Boosted Thermal Insulation For Refractories Segment Expansion

On the basis of application, the market is segmented into thermal insulation for refractories, composite materials, exhaust gas catalyst mat, filtration, glass protection, and others.

In 2026, the thermal insulation for refractories segment is projected to lead the market with a 47.62% share. Several factors drive the demand for alumina fibers for thermal insulation in refractories. Their exceptional thermal stability, high melting point, and resistance to thermal shock make them ideal for use in high-temperature environments such as furnaces, kilns, and reactors. Additionally, these fibers improve the energy efficiency of refractories by reducing heat loss, which is crucial for industries such as steel, cement, and glass manufacturing. Their lightweight nature enhances handling and installation, while their durability in extreme conditions extends the lifespan of refractory linings, ultimately reducing maintenance costs and improving overall operational performance.

In the exhaust gas catalyst mats segment, the demand for these fibers is driven by their ability to enhance thermal stability, improve strength, and resist chemical degradation under high temperatures. These fibers help maintain catalyst integrity, reduce emissions, and improve engine efficiency. The continued demand for internal combustion engine vehicles, particularly in developing regions, is sustaining the need for automotive catalyst mats in the short to medium term. Additionally, stricter emission regulations in key markets are driving higher catalyst efficiency requirements, which, in turn, leads to greater demand for advanced materials such as alumina short fiber, driving market growth.

ALUMINA SHORT FIBER MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Alumina Short Fiber Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 53.00% of the global market in 2025, generating USD 0.42 billion in revenue, and is projected to reach USD 0.45 billion in 2026, owing to rapid industrialization, particularly in China, Japan, and India. The growing automotive manufacturing, steel production, and electronics industries require materials with offer high thermal stability, which alumina fibers provide. Furthermore, increasing environmental concerns and the push for energy-efficient, sustainable manufacturing practices are further enhancing the demand for these fibers across key sectors in the region, driving market growth. The Japan market is estimated at USD 0.03 billion by 2026, the China market is estimated at USD 0.3 billion by 2026, and the India market is estimated at USD 0.05 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

North America contributed approximately USD 0.13 billion to the global market in 2025, accounting for 16.00% share, and is expected to reach USD 0.14 billion in 2026. Market growth in North America is driven by advancements in the aerospace, automotive, and energy sectors. Increased investments in high-performance materials for electric vehicles, renewable energy systems, and fuel-efficient aircraft fuel demand for these fibers. Strict environmental regulations further promote their adoption, as alumina fibers enhance energy efficiency and help reduce emissions in key industries, contributing to sustainable growth. The U.S. market is estimated at USD 0.12 billion by 2026.

Europe

In 2025, the Europe market stood at USD 0.17 billion, representing 22.00% of global demand, and is projected to grow to USD 0.18 billion in 2026. Europe’s demand for these fibers is propelled by its focus on sustainable manufacturing and green technologies. The automotive and aerospace industries, particularly in Germany and France, use alumina short fibers to reduce weight and improve performance in vehicles and aircraft. Additionally, growing investments in renewable energy, such as wind and solar power, are fueling the need for high-temperature resistant materials, further driving the demand for alumina fibers. The UK market is estimated at USD 0.01 billion by 2026, while the Germany market is estimated at USD 0.04 billion by 2026.

Latin America

Latin America recorded a market size of USD 0.04 billion in 2025, capturing 5.00% of the global market share, and is projected to reach USD 0.04 billion in 2026. In Latin America, demand for these fibers is growing due to expanding manufacturing capabilities in the automotive and construction sectors. Countries such as Brazil are focusing on reducing carbon footprints in industrial processes, and alumina short fibers help achieve this goal by improving energy efficiency and material performance. Additionally, rising interest in renewable energy technologies, particularly in solar and wind power, is boosting the need for high-performance materials in these applications.

Middle East & Africa

In 2025, Middle East & Africa generated USD 0.03 billion, contributing 4.00% to global market revenue, and is projected to grow to USD 0.03 billion in 2026. In the Middle East & Africa, demand for alumina fibers is driven by the region’s heavy reliance on the oil and gas industry, where these fibers are used for thermal insulation in high-temperature environments. Additionally, increasing investments in renewable energy and infrastructure development, particularly in UAE and Saudi Arabia, are creating opportunities for alumina fibers in energy storage, composite materials, and construction, among other sectors.

TRADE PROTECTIONISM & REGULATORY CHALLENGES

Global Supply Chain Challenges and Pricing Fluctuations to Impact Product Demand

The global supply chain and pricing of these fibers significantly affect their demand. Limited availability of high-purity raw materials, coupled with the energy-intensive production process, leads to supply chain disruptions and fluctuating costs. Dependence on specialized suppliers further amplifies vulnerability to geopolitical tensions and trade restrictions. High production costs result in elevated pricing, restricting adoption in cost-sensitive industries. Additionally, supply chain inefficiencies can result in delays, impacting project timelines for end-users. To sustain demand, manufacturers are focusing on diversifying raw material sources, improving production efficiency, and stabilizing pricing through strategic partnerships and supply chain optimization initiatives.

Strong Environmental Regulations Significantly Influence the Production and Disposal of These Fibers

Environmental regulations impacting the production and disposal of alumina short fibers primarily focus on minimizing waste, reducing energy consumption, and ensuring safe disposal practices. Regulations such as the EU’s REACH and the U.S. Environmental Protection Agency's policies require manufacturers to limit hazardous emissions and use environmentally safe chemicals during production. Additionally, proper disposal practices are essential to prevent contamination from waste by-products. As these fibers are non-biodegradable, their recycling and disposal must adhere to guidelines that minimize environmental impact, promoting circular economy practices in industries where these fibers are consumed.

LATEST INDUSTRY DEVELOPMENTS & RESEARCH

Incorporation of Products in Next-Gen Technologies to Offer Substantial Growth Opportunities

The development of specialized applications for alumina short fibers in batteries, fuel cells, and high-performance composites is driving innovation across various industries. In batteries, alumina fibers enhance thermal stability and conductivity, which is crucial for high-performance energy storage systems. In fuel cells, they improve the efficiency and durability of components by reinforcing materials exposed to extreme conditions. In high-performance composites, thermal-resistant alumina fibers are used to enhance the strength-to-weight ratio and overall structural integrity, benefiting industries such as aerospace and automotive. These advancements in specialized applications are positioning these fibers as critical materials for next-generation technologies, offering substantial growth opportunities.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Compete Over Pricing and Product Differentiation to Gain Higher Market Share

The market is highly consolidated, with limited players accounting for the majority of the market share. Rivalry in the market is intense, driven by increasing demand for high-performance materials and competition to capture niche markets. A few of these key players include MAFTEC Group Co., Ltd., Denka Company Limited, Isolite Insulating Products Co., Ltd., Rath-Group, and Shandong Dongheng Sinofibre New Material Co., Ltd. Established players focus on innovation and expanding applications in renewable energy sector. Price sensitivity, coupled with competition from substitutes, further intensifies efforts to optimize production efficiency and differentiate products.

LIST OF KEY ALUMINA SHORT FIBER COMPANIES PROFILED:

- CHONGQING CHAL PRECISION ALUMINIUM CO., LTD. (China)

- Denka Company Limited (Japan)

- Luyang Energy-saving Materials Co., Ltd. (China)

- MAFTEC Group Co., Ltd. (Japan)

- Shandong Dongheng Sinofibre New Material Co., Ltd (China)

- Shandong Sinoshine Advanced Materials Co., Ltd (China)

- Vulcan Shield Global Pte Ltd (Singapore)

- ZIRCAR Ceramics (U.S.)

- Rath-Group (Austria)

- Isolite Insulating Products Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2024 – RATH Group announced that it had acquired a 33% stake in Avanee Refsol India. The move is part of the company’s Evolution 2030+ strategic growth plan. The company plans to build a production capacity of 20,000 tons of refractory products and is projected to begin its production at the beginning of 2025.

REPORT COVERAGE

The market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, applications, and products. The report also offers market insights into key trends and highlights vital industry developments. In addition, the report encompasses various factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

CAGR |

CAGR of 7.20% during 2026-2034 |

|

Unit |

Value (USD Billion), Volume (Ton) |

|

Segmentation |

By Application

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 0.79 billion in 2025 and is projected to reach USD 1.49 billion by 2034.

In Asia Pacific, the market value stood at USD 0.42 billion in 2025.

Registering a significant CAGR of 7.20%, the market will exhibit considerable growth over the forecast period.

By application, the thermal insulation for refractories segment led the market in 2025.

Rising investments in advanced manufacturing technologies to drive market growth

Asia Pacific held the dominant share of the market in 2025.

MAFTEC Group Co., Ltd., Denka Company Limited, Isolite Insulating Products Co., Ltd., Rath-Group, and Shandong Dongheng Sinofibre New Material Co., Ltd. are the leading players in the market.

Rising emphasis on sustainable manufacturing is a key factor driving product adoption.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us