C-RAN Market Size, Share & COVID-19 Impact Analysis, By Network (2G/3G, 4G and LTE, and 5G and 5G NR), By Enterprise Type (Small and Medium Enterprises (SMEs) and Large Enterprises), By Type (Centralized-RAN and Virtual RAN (vRAN)), By Industry (Telecommunication, Manufacturing, Healthcare, Transport and Logistics, and Mining and Energy), and Regional Forecast, 2026-2034

C-RAN Market Size

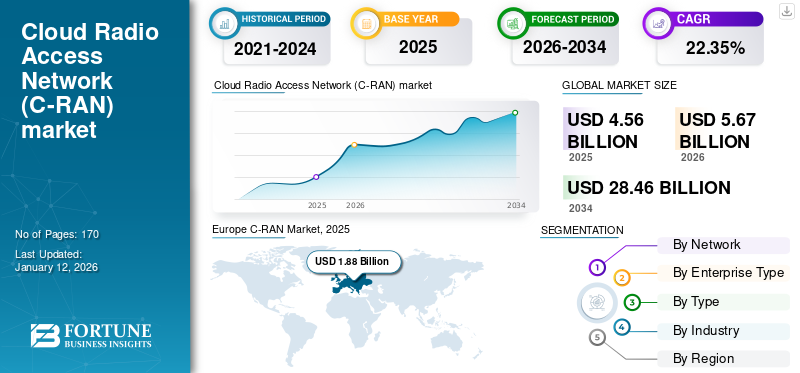

The global C-RAN market size was valued at USD 4.56 billion in 2025. The market is projected to grow from USD 5.67 billion in 2026 to USD 28.46 billion by 2034, exhibiting a CAGR of 22.35% during the forecast period. Europe dominated the global market with a share of 30.53% in 2025.

Cloud RAN (C-RAN), an abbreviation for cloud radio access network, is a network architecture in the field of wireless telecommunications. It transforms traditional cellular network infrastructure by centralizing the baseband processing functions of multiple remote radio heads (RRHs) or small cells into a centralized cloud data center. This centralized approach enables more efficient resource allocation, dynamic scalability, and advanced network optimization techniques, as well as facilitating the deployment of 5G and beyond, making it a pivotal technology for the future of wireless communication.

The increasing deployment of cloud RAN in telecommunications networks is primarily driven by its scalability, cost efficiency, and network optimization capabilities. Cloud RAN's virtualized architecture enables operators to efficiently scale their infrastructure, reduce operational costs, and enhance network quality, making it a future-proof and environmentally friendly choice for accommodating the growth in data traffic, supporting 5G and beyond, and achieving centralized network intelligence and control. According to industry specialists, the total costs of infrastructure ownership was reduced by 40%, after the transformation and adoption of cloud technology.

COVID-19 IMPACT

Supply Chain Disruptions and Increased Demand for Reliable Connectivity Had a Mixed Impact

The COVID-19 pandemic both disrupted and accelerated the market growth. It caused delays in deployments due to supply chain disruptions and increased costs while simultaneously amplifying the demand for reliable connectivity as remote work and online services surged. Cloud RAN's centralized architecture proved beneficial for remote network management and resilience, meeting the increased data traffic demands. Some operators adjusted their investment priorities, but overall, the pandemic highlighted the importance of C-RAN in addressing the challenges and opportunities presented by the evolving telecommunications landscape.

For instance, according to IHS Technology, in May 2020, the server market experienced a rebound in Q1 2020, with a 27% increase in global server shipments compared to 2019. The surge was driven by heightened demand from cloud service providers and enterprises adapting to increased reliance on cloud services due to the pandemic.

C-RAN Market Trends

Increasing Demand for Low Latency and High-speed Data in 5G Network to Propel the Market Growth

With an increasing need for data capacity due to the growing internet data traffic, 5G technology is designed to significantly enhance data communication speed, offering upto three times the performance compared to 4G and LTE. The primary objective behind the development of 5G is to provide substantial improvements in mobile broadband services. It is made possible through the introduction of cloud RAN, which facilitates the opening of wireless base station network capabilities via virtualized containers.

According to GSMA, the percentage of global 5G connections is expected to increase upto 54% in 2030, as compared to 12% in 2022. Mobile internet users are also increasing exponentially, with a penetration rate of 64% and 5.5 billion mobile users in 2030. These statistics underscore the undeniable momentum of 5G technology, demonstrating its pivotal role in shaping the future of telecommunications and meeting the demand for fast, efficient, and cost-effective networking services. Thus, the escalating demand for low-latency and high-speed data in 5G networks is driving C-RAN market growth in the industries.

Download Free sample to learn more about this report.

C-RAN Market Growth Factors

Rising Adoption of Higher Bandwidth and Cost-Efficient Telecom Devices to Drive the Market Growth

The escalating adoption of higher bandwidth and cost-efficient telecommunication devices is poised to exert a substantial influence on the market share of 4G and 5G devices. The demand for higher bandwidth solutions has grown significantly as a result of the emergence of applications that require a large amount of data, such as high-definition video streaming, augmented reality (VR) applications, and IoT devices. The major cloud providers are addressing the rising demand by integrating advanced technologies such as multi-band carrier aggregation, beamforming, and massive MIMO into their offerings. These integrations efficiently utilize available spectrum resources, enhancing data transfer rates and reducing latency.

In August 2023, Telkomsel renewed its partnership with Ericsson to expand its 4G/5G network presence in Indonesia, with Ericsson deploying its energy-efficient 5G cloud RAN solutions in multiple regions such as Northern Sumatra, Aceh, and Kalimantan, among others.

Thus, the symbiotic relationship between the demand for higher bandwidth and cost-efficient C-RAN solutions is poised to enhance cloud utilization by enabling a diverse range of applications ranging from augmented reality (AR) to autonomous vehicles, among others.

RESTRAINING FACTORS

Stringent Regulations on Applications and Lack of Fronthaul Capacity to Limit the Market Growth

Cloud RAN faces technical challenges that encompass latency, network synchronization, higher initial investments, and fronthaul capacity. The centralized processing of cloud RAN, where Baseband Units (BBUs) are concentrated in base stations and data centers, can introduce undesirable latency in communications between BBUs and Remote Radio Heads (RRHs). This latency may not meet the stringent requirements of applications such as 5G, autonomous vehicles, and real-time Internet of Things (IoT), hindering the network's effectiveness.

Moreover, the cloud RAN architecture necessitates a substantial initial investment. Building and maintaining data centers to host BBUs and deploying the necessary high-capacity fiber optic fronthaul connections can be financially burdensome for network operators. This upfront cost can deter some operators from adopting cloud RAN, impacting its widespread deployment. In addition, the capacity of the fronthaul network, which connects RRHs to the centralized BBU pool, is crucial for network performance. Inadequate fronthaul capacity can restrict the number of RRHs that can be supported and, subsequently, the overall network capacity, impeding its ability to handle growing data demands and high traffic loads effectively.

C-RAN Market Segmentation Analysis

By Network Analysis

Global Proliferation and Increasing Impact of 5G Speeds and Efficiency to Aid in Market Growth

By network, the market is divided into 4G and LTE, 5G and 5G NR, and 2G/3G.

The 5G and 5G NR segment is projected to dominate the market with a share of 46.39% in 2026. The 5G and 5G NR network segment accounted for the fastest growing network system and is poised to experience the most rapid growth during the forecast period. This growth is attributed to the explosive surge in data traffic, accompanied by a substantial power consumption burden in existing network architectures.

4G and LTE networks to dominate the market during in the forecast period. Given that 4G and 5G networks offer high-speed connectivity and low latency, they present a more efficient framework and technical architecture for cloud RAN operations. Furthermore, the global proliferation of 5G networks has become a pivotal trend, playing a major role in propelling the growth of this segment.

5G NR, a key component of 5G, further enhances higher frequencies and advanced modulation techniques, enabling ultra-reliable low-latency communication (URLLC) for mission-critical applications, including industrial automation and smart grids. The driving factor for every generation of networks are their individual evolving demands of connectivity and technology, with 5G NR being at the forefront of the latest innovations in wireless communication, offering highest speed, capacity, and lower latency to support a wide range of futuristic applications.

To know how our report can help streamline your business, Speak to Analyst

By Enterprise Type Analysis

Financial Capabilities of Large Enterprises to Propel the Adoption of C-RAN Solutions

The Large Enterprises segment is expected to lead the market, contributing 76.84% globally in 2026. Based on enterprise type, the market is divided into large enterprises and small and medium enterprises (SMEs). The large enterprises segment is projected to dominate the C-RAN market share during the forecast period as they possess greater financial capabilities and complex network demands and utilize cloud RAN for its scalability, flexibility, and ability to support massive data traffic. It enables large enterprises to achieve superior network performance, accommodating the demands of IoT, and future-proofing their infrastructure to seamlessly integrate emerging technologies such as 5G, AI, machine learning, and cloud computing.

SMEs are often characterized by more constrained budgets and resources are increasingly drawn to cloud RAN due to its cost-effective nature. Cloud RAN's ability to centralize network processing and reduce on-site hardware requirements aligns with the budget-conscious approach of SMEs, enabling them to leverage advanced wireless technologies while minimizing capital expenditures.

By Type Analysis

Utilization of vRAN in Network Slicing and Edge Computing to Boost the Segment Growth

The Centralised-RAN segment will account for 60.98% market share in 2026. By type, the market is bifurcated into centralized RAN and virtual RAN (vRAN). vRAN virtualizes network functions and decouples them from proprietary hardware, offering flexibility and scalability. The vRAN segment is projected to dominate the market during the forecast period owing to its advanced ability, which enables operators to deploy radio access functions as software on commodity hardware, which can be dynamically allocated based on traffic demands. This makes vRAN well-suited for network slicing, edge computing, and catering to diverse use cases in 5G and IoT.

Centralized RAN centralizes baseband processing in data centers, reducing on-site hardware at cell sites, which leads to cost savings, efficient resource allocation, and easier network management. It is particularly suited for high-capacity, densely populated urban areas.

By Industry Analysis

Rising Adoption of C-RAN in Telecommunication Sector due to its Cloud Capabilities to Drive Segment Growth

The Telecommunication segment is expected to account for 54.30% of the market in 2026. Based on industry, the market is classified into telecommunication, manufacturing, healthcare, transport and logistics, and mining and energy sector. The telecommunication segment is expected to dominate the market share during the forecast period till 2030. In the telecommunications sector, cloud radio access network enables network operators to enhance coverage, capacity, and performance, especially in densely populated urban areas. The segment growth can be attributed to the demand for higher data speeds, reduced latency, and cost-effective network expansion.

In manufacturing, C-RAN offers the potential to enable smart factories through improved connectivity and low-latency communication. This is crucial for real-time monitoring and control of industrial processes, predictive maintenance, and automation, driven by the need for increased efficiency and reduced downtime.

In healthcare, C-RAN supports telemedicine, enabling remote patient monitoring, real-time video consultations, and the secure transmission of large medical data sets.

In the transport and logistics sector, C-RAN aids in tracking and managing shipments, optimizing route planning, and facilitating real-time communication between vehicles and control centres.

REGIONAL INSIGHTS

Regionally, the market is classified into North America, Europe, the Asia Pacific, and the rest of the world. These regions are further categorized into several countries and sub-regions.

Europe

Europe C-RAN Market, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The United Kingdom market is projected to reach USD 0.92 billion by 2026, while the Germany market is projected to reach USD 0.34 billion by 2026. Europe dominated the market with a valuation of USD 1.88 billion in 2025 and USD 2.34 billion in 2026. Europe also dominated the global C-RAN market with a share of 41.37% in 2023 due to the region's emphasis on environmental sustainability and the presence of key players operating in the market. European countries, particularly those with stringent environmental regulations, are attracted to cloud RAN’s energy-efficient centralized processing, which aligns with their green initiatives. In addition, the continent’s heterogeneous network requirements, spanning urban, suburban, and rural areas, are met by cloud RAN’s dynamic resource allocation and network optimization capabilities, ensuring efficient spectrum utilization and coverage extension. Moreover, the drive toward low-latency communication in applications such as autonomous vehicles and Industry 4.0 is accelerating cloud RAN deployment, as it enables edge computing and precise synchronization crucial for real-time data processing.

To know how our report can help streamline your business, Speak to Analyst

North America

The United States market is projected to reach USD 0.92 billion by 2026. North America market for C-RAN is expected to showcase the highest CAGR due to the confluence of technical factors that cater to the region's diverse and demanding telecommunications landscape. The evolution toward 5G is a paramount driver, necessitating the adoption of cloud RAN to enable the ultra-low latency and high bandwidth required by applications such as autonomous vehicles and smart cities. The region’s vast geography, ranging from densely populated urban centers to remote rural areas, calls for cloud RAN’s flexibility to efficiently allocate resources where needed, reducing operational costs and optimizing network performance. Moreover, North America’s commitment to network security has bolstered cloud RAN adoption as it offers centralized control and monitoring, enhancing cybersecurity measures.

Asia Pacific

The Japan market is projected to reach USD 0.19 billion by 2026, the China market is projected to reach USD 0.35 billion by 2026, and the India market is projected to reach USD 0.12 billion by 2026. In the Asia Pacific region, the market is witnessing healthy growth driven by the proliferation of 5G networks as a key driver, with countries such as China aggressively deploying 5G infrastructure to support high-capacity applications including IoT, cloud, and AR. Furthermore, the region’s dense urban areas necessitate efficient spectrum utilization, making cloud RAN’s centralized processing and coordinated management of resources crucial. In addition, the challenging geographical terrain in parts of Asia Pacific, such as mountainous regions and archipelagos, underscores the importance of cloud RAN’s fronthaul network optimization to minimize signal loss and enhance network coverage.

KEY INDUSTRY PLAYERS

Business Expansion through Innovative Solutions and Rising Security Concerns to Propel the Market Share of Key Players

Key players across several domains gain operational benefits by offering innovative cloud RAN solutions. Ericsson and Nokia Corporation are at the forefront of cloud RAN deployments and integrations with manufacturing companies such as Intel and HPE have enhanced the capabilities of cloud-based RAN solutions. For instance, in July 2023, Ericsson and Intel partnered to leverage Intel's 18A manufacturing and process technology for Ericsson's new-generation 5G optimized infrastructure. Under the agreement, Intel manufactured custom 5G SoCs for the company, resulting in highly distinctive products for future 5G infrastructure. Moreover, these companies expanded their partnership to enhance 4th Gen Intel Xeon Scalable processors with Intel vRAN Boost, enhancing Ericsson's cloud RAN solutions. This collaboration aimed to help communication service providers enhance network capacity and energy efficiency while achieving greater flexibility and scalability.

However, other companies such as ZTE and Huawei, being dominant players in several regions such as China, South Korea, and the Middle East, were banned from expanding their infrastructure and cloud RAN solutions in the U.K., the U.S., New Zealand, and Australia, due to the stringent regulations imposed by the governing entities. This has led to the creation of enhanced opportunities for local players such as Nokia, Ericsson, Mavenir, and Airspan, among others.

List of Top C-RAN Companies:

- Telefonaktiebolaget LM Ericsson (Sweden)

- Nokia Corporation (Finland)

- Huawei Technologies Co., Ltd. (China)

- Zhongxing New Telecommunications Equipment Co., Ltd. (China)

- Qualcomm Incorporated (U.S.)

- NEC Corporation (Japan)

- Mavenir Systems, Inc. (U.S.)

- Samsung Group (South Korea)

- Airspan Networks, Inc. (U.S.)

- Telefónica, S.A. (Spain)

KEY INDUSTRY DEVELOPMENTS:

- August 2023 – Nokia was selected by Cellfie Mobile for a nationwide network modernization project covering 4G and 5G readiness. Nokia's 5G-ready AirScale portfolio, featuring energy-efficient ReefShark System-on-Chip (SoC) technology, was used to upgrade existing LTE sites and add new 5G-ready ones following a successful spectrum auction. Nokia's MantaRay Network Management system enhanced network monitoring and management. The deployment is set to commence in November, solidifying Nokia's position as the sole RAN supplier and increasing its market share in the country.

- July 2023 – Telstra partnered with Ericsson to launch Australia's first Ericsson Cloud Radio Access Network on Telstra's 5G commercial network. The initial 55 Cloud RAN technology sites, located in the Gold Coast, Queensland, marked a significant milestone in Telstra's quest to offer nationwide 5G services. This deployment included migrating carrier frequencies 3600MHz and 2600MHz to the Cloud RAN infrastructure, enhancing network capacity, intelligence, and speed.

- June 2023 – India-based operator Reliance Jio capitalized on recent technological agreements between India and the U.S., which paved the way for the export of its domestically developed end-to-end 5G radio and stack. This created an additional revenue stream for the company and advanced the focus on Open RAN, part of the broader collaboration between the countries in research and development of 5G/6G technologies, facilitated by organizations such as India's Bharat 6G Alliance and the U.S. Next G Alliance.

- June 2023 – Qualcomm Technologies acquired Cellwize Wireless Technologies Pte. Ltd., a network management and automation solution provider, in a move to accelerate the adoption of the 5G Radio Access Network (RAN). This acquisition enhanced the company’s 5G infrastructure solutions, enabling the digital transformation of industries, supporting the growth of the cloud economy, and powering the connected intelligent edge.

- March 2023 – U.K.-based operator Virgin Media O2 was among the early European adopters of Ericsson's cloud radio access network product as part of a broader network expansion agreement. Ericsson provided equipment for Virgin Media O2's U.K. network, including the energy-efficient multi-band 5G mMIMO radio Air 3258 platform, with small cell deployments in key cities to boost capacity and speed.

REPORT COVERAGE

Our analysis of this market provides leading business insights on global regions to improve business decisions and judgments considering the market. Furthermore, the research report provides key insights into the recent developments of the market trends and industry, as well as a thorough review of emerging technologies that are being adopted worldwide. It also emphasizes the major growth-stimulating factors and elements, which allows the reader to obtain an in-depth perception of the market.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Growth Rate |

CAGR of 22.35% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Network

By Enterprise Type

By Type

By Industry

By Region

|

Frequently Asked Questions

The study by Fortune Business Insights Inc. says that the global market is projected to reach USD 28.46 billion by 2034.

In 2025, the market stood at USD 4.56 billion.

The market is projected to grow at a CAGR of 22.35% during the forecast period (2026-2034).

The 4G and LTE segment is expected to lead the market in 2025.

The rising adoption of higher bandwidth and cost-efficient telecom devices is expected to drive the market growth.

Telefonaktiebolaget LM Ericsson, Nokia Corporation, Huawei Technologies Co., Ltd., Zhongxing New Telecommunications Equipment Co., Ltd., Qualcomm Incorporated, NEC Corporation, and Mavenir Systems, Inc. are the top players in the market.

Europe held the largest market share in 2025.

By network, the 5G and 5G NR is expected to grow with a remarkable CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 170

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us