Video Surveillance Market Size, Share & Industry Analysis, By Component (Hardware, Software, and Video Surveillance as a Service (VSaaS)), By End-User (Commercial, Industrial, Residential and Government), and Regional Forecast Report 2026-2034

Video Surveillance Market Size and Industry Overview

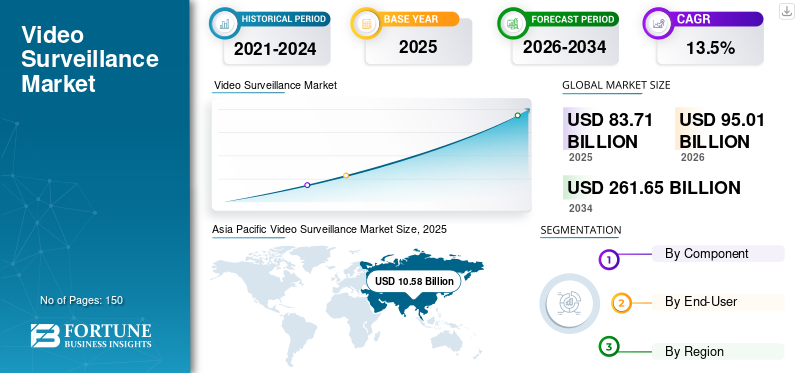

The global video surveillance market size was valued at USD 83.71 billion in 2025. The market is projected to grow from USD 95.01 billion in 2026 to USD 261.65 billion by 2034, exhibiting a CAGR of 13.50% during the forecast period. Asia Pacific held the largest market share, accounting for 55.33% of the global market in 2025.

Video surveillance is driven by rising security requirements and rapid digital infrastructure expansion. Deployment is no longer limited to high-risk environments but has become a foundational layer across commercial, industrial, residential, and public-sector settings. The current Video surveillance market size reflects sustained global investment rather than cyclical demand, with a strong presence across both developed and emerging economies.

Historically, market expansion was driven by analog camera deployments and basic monitoring needs. This shifted as Internet Protocol–based systems, high-definition imaging, and networked storage reshaped system capabilities. Growth accelerated as surveillance platforms evolved from passive recording tools into active intelligence systems. The market has now moved into a scaling maturity stage, where replacement demand, system upgrades, and feature expansion outweigh first-time installations.

Short-term Video surveillance market growth is supported by infrastructure modernization, urban security initiatives, and enterprise risk management priorities. Medium-term momentum is expected to strengthen as analytics, cloud connectivity, and artificial intelligence become standard rather than optional. Over the long term, the market outlook remains structurally positive as surveillance data integrates more deeply with operational, safety, and compliance frameworks.

Applications of artificial intelligence (AI) and deep learning algorithms are likely to impact the market growth. Similarly, the integration of video analytics is likely to create lucrative market opportunities in the coming years. According to the AI global surveillance index, 51.0% of liberal democracies, such as the United States, Canada, and others, deployed advanced surveillance systems. Hence, the emergence of AI-enabled surveillance systems is anticipated to surge the market growth. However, the current COVID-19 pandemic is likely to restrict the video surveillance market growth for a specific interval of time.

Furthermore, the market is entering a critical stage of digital convergence, in which AI-powered analytics, cloud computing, and edge processing are redefining surveillance performance benchmarks. Enterprises prioritize interoperability, cybersecurity, and energy-efficient camera systems that adhere to global standards established by organizations such as the International Energy Agency (IEA) and the United States Department of Energy (DOE). The implementation of carbon-neutral and low-power surveillance systems promotes corporate sustainability while lowering the total cost of ownership. Furthermore, advancements in 5G infrastructure allow for seamless connectivity between decentralized devices, improving responsiveness and data transfer efficiency in high-density urban environments.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

VIDEO SURVEILLANCE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 83.71 Billion

- 2026 Market Size: USD 95.01 Billion

- 2034 Forecast Market Size: USD 261.65 Billion

- CAGR: 13.50% from 2026–2034

- Asia Pacific dominated the video surveillance market with a 55.33% share in 2025.

- The hardware segment accounted for the largest share by component in 2025.

- The commercial segment held the leading share by end-user in 2025.

Asia Pacific

Asia Pacific led the global market, driven by smart city projects, rapid urbanization, and large-scale government surveillance initiatives.

North America

North America is witnessing strong growth due to increasing adoption of AI-enabled surveillance, cloud-based platforms, and critical infrastructure protection.

Europe

Europe continues to expand steadily, supported by public safety investments and growing demand for privacy-compliant surveillance solutions.

U.S.

Rising deployment of advanced surveillance systems, facial recognition technologies, and cybersecurity-hardened platforms is supporting market growth.

Japan

Strong investments in AI-powered surveillance technologies and smart infrastructure development are driving market expansion.

Read More

What major trends in the Video surveillance market?

Growing Trend of Deep Learning in Video Surveillance Software

Deep learning is the fastest-growing application of artificial intelligence. There is a substantial availability of deep learning algorithms and deep learning infrastructure for pattern analysis in the surveillance industry. The new versions of graphics processing units (GPUs) offered by vendors such as Nvidia Corporation provide deep learning algorithms for cameras and recorders. The capabilities of deep learning technology to facilitate video analytics and reduce calibration of algorithms drive a huge leap in the future use of video surveillance software. As a result, deep learning in surveillance systems is currently trending in the market.

The ongoing shift toward self-learning surveillance models that can recognize adaptive behavior and detect anomalies is transforming operational efficiency. Manufacturers are incorporating neural networks directly into system-on-chip architectures, allowing for local data inference while reducing reliance on cloud services. This method reduces latency, energy consumption, and security risks while meeting the growing demand for real-time video analytics in critical infrastructure and smart-city applications (IEA, 2024).

The Video surveillance market is being reshaped by a decisive shift toward software-defined, intelligence-led architectures. Surveillance systems are no longer designed solely for visual monitoring. They are increasingly embedded within broader digital ecosystems that support automation, analytics, and real-time decision-making. This transition is redefining how organizations extract value from video data.

Artificial intelligence has become a central force behind evolving Video surveillance market trends. Advanced video analytics now enable facial recognition, behavior analysis, object detection, and anomaly identification. These capabilities reduce reliance on manual monitoring while improving response accuracy and speed. Edge-based processing is also gaining traction, allowing analytics to occur closer to the data source and reducing latency and bandwidth demands.

Integration of Video Analytics in a Network Camera is Gaining Momentum

In recent years, there has been a growing trend of video analytics integration in network cameras. As advanced microprocessors are becoming available to the video surveillance system manufacturers, there is a substantial increase in the integration of analytics capabilities with the cameras. Surveillance using cameras integrated with intelligent analytics facilitates early detection and identification of criminal events. Owing to the advancements in analytics, crowd detection, people-counting, facial recognition, automated number plate detection, and other such technologies can be easily incorporated with the surveillance software. As a result, the integration of video analytics with network cameras would contribute to expanding the video surveillance market size in the coming years.

Furthermore, next-generation network cameras are designed to comply with international cybersecurity frameworks such as ISO/IEC 27001 and NIST standards, which ensure data integrity across connected systems. The industry is seeing rapid deployment in the transportation, energy, and urban planning sectors, where AI-based video feeds improve operational reliability and sustainability (DOE, 2024).

Business models are evolving in parallel. Video Surveillance as a Service is gaining acceptance across commercial and small enterprise segments, driven by demand for scalability, predictable costs, and remote system management. This model shifts value from hardware ownership toward recurring software and service revenues, altering competitive dynamics across the value chain.

Regulatory compliance and sustainability considerations are also shaping future direction. Organizations increasingly demand privacy-by-design architectures, secure data handling, and energy-efficient hardware. Buyers now evaluate solutions based on long-term compliance readiness and operational resilience. Collectively, these trends signal a market moving toward intelligent, service-oriented platforms that integrate security, analytics, and operational insight into a unified surveillance strategy.

What are the key drivers accelerating growth in the Video surveillance market?

Emergence of AI Surveillance Technology Would Ensure to Drive Growth

Artificial intelligence technology has gained traction in recent years. According to a paper published by the Carnegie Endowment for International Peace, in 2019, out of a total of 176 countries, 75 countries are actively leveraging artificial intelligence capabilities for surveillance purposes, including facial recognition systems, smart cities, and others. This data reflects that the growing smart city initiatives & developments and facial recognition applications are likely to drive the adoption of surveillance systems using cameras during the forecast period.

Furthermore, government-backed investments in digital safety infrastructure and carbon-efficient public monitoring networks are encouraging adoption in both developed and emerging markets. Many city governments are linking their surveillance projects with the IEA and UNDESA's smart-energy and data-governance initiatives. This integration ensures that surveillance networks contribute to both environmental and public safety goals, transforming AI-powered security infrastructure into a dual enabler of sustainability and governance resilience.

Growth in the Video surveillance market is being driven by a convergence of security imperatives, digital transformation, and evolving risk management practices. On the demand side, organizations face heightened exposure to physical security threats, operational disruptions, and compliance obligations. Video surveillance systems are increasingly viewed as essential infrastructure for loss prevention, safety assurance, and real-time situational awareness rather than discretionary security investments.

Customer buying behavior has shifted toward intelligence-driven solutions. Enterprises now prioritize systems that move beyond recording to deliver actionable insights through analytics, automation, and remote monitoring. This shift is evident across commercial facilities, industrial sites, and public spaces, where surveillance supports operational efficiency, employee safety, and asset protection. Residential adoption is also expanding as consumers seek integrated smart security ecosystems.

Growing Adoption of Body-worn Cameras Across Several Industries, such as Healthcare & Retail, to Drive Growth in the Video Surveillance Industry

The increasing use of body-worn cameras by the security forces or law enforcement agencies has led to the adoption of these cameras across other industries, such as healthcare and retail. Body-worn cameras have several benefits in industries such as healthcare, retail, and hospitality to improve customer relations, enhance workforce protection, and help prevent unusual activities. A body-worn camera enables employees to capture real-time events and send real-time threat alerts and notifications to the security authorities.

AI-powered body cameras are being outfitted with thermal sensors and health-data interfaces, which have proved useful during post-pandemic recuperation. Integration with cloud-based management platforms enables large-scale enterprises to safely study behavioral patterns and compliance metrics, promoting data-driven decision-making and operational transparency across industries.

Hence, considering the above-mentioned factors, the video surveillance market players are integrating body-worn cameras and video analytics capabilities to address the requirements of the end-users. For instance, in March 2020, Avigilon Corporation, a Motorola Solutions company, announced the integration of its video analytics and security portfolio of VideoTag enterprise bodyworn cameras and Avigilon Control Center (ACC) video management tools.

Supply-side enablers have strengthened market momentum. Advances in camera resolution, edge computing, and video compression have improved performance while reducing bandwidth and storage constraints. Cloud-native architectures and Video Surveillance as a Service models have lowered deployment complexity and upfront investment requirements. Talent availability in artificial intelligence and data analytics has further accelerated innovation across software platforms.

Government-led smart city initiatives and infrastructure modernization programs continue to expand surveillance deployments. Regulatory emphasis on safety, workplace monitoring, and public accountability has increased institutional demand. Macroeconomic pressure to automate security operations and reduce labor dependence further supports sustained Video surveillance market growth across diverse end-user segments.

What challenges and constraints impact market expansion?

Despite sustained Video surveillance market growth, several structural challenges continue to shape adoption and investment outcomes. Privacy and data protection concerns represent a primary constraint, particularly in regions with strict regulatory oversight. Organizations must balance security objectives with compliance obligations related to data collection, storage, and individual rights. These requirements increase legal exposure and raise implementation complexity.

Operational challenges also affect scalability. Large-scale deployments generate significant data volumes, creating pressure on network bandwidth, storage infrastructure, and system maintenance. Legacy systems often lack interoperability with modern Internet Protocol–based platforms, increasing integration costs. For smaller organizations, technical complexity and ongoing system management remain deterrents to adoption.

From a financial perspective, pricing pressure has intensified. Hardware commoditization has reduced margins for camera manufacturers, shifting value toward software and services. However, transitioning to software-centric revenue models requires sustained investment in development, cybersecurity, and customer support. Supply chain volatility, particularly in semiconductor availability, introduces additional cost uncertainty and delivery risk.

Technology-related risks are increasingly prominent. Cybersecurity vulnerabilities expose surveillance networks to unauthorized access and data breaches, undermining trust and increasing liability. Rapid innovation cycles also heighten the risk of system obsolescence, forcing buyers to evaluate long-term upgrade paths carefully. As competitive intensity increases, differentiation becomes harder to sustain, placing pressure on the Video surveillance market share and long-term profitability for undifferentiated vendors.

VIDEO SURVEILLANCE MARKET SEGMENTATION ANALYSIS

By Component Analysis

By Hardware Analysis

Surveillance Hardware Segment is Expected to Hold a Major Share in the Market

Based on component, this market has been segmented into hardware, software, and video surveillance as a service (VSaaS).

The hardware segment is expected to account for a major video surveillance market share during the forecast period. Despite the high cost, there is a growing demand for advanced hardware with embedded video analytics solutions and deep-learning applications. The research and development investments by the software startups, surveillance systems vendors, and chip manufacturers have boosted the advancements in hardware.

The hardware segment is further bifurcated into camera, storage devices, and others. The other segment comprises video encoders and other network devices. Among these sub-segments, cameras are projected to have the largest video surveillance market share. Integration of deep learning applications and video analytics fuels the demand for surveillance cameras for various uses across end-users. Subsequently, the growing adoption of cloud-based surveillance solutions by the end-users has encouraged the market players to leverage resources such as compute power and storage devices. These factors are driving the demand for data storage devices in the market.

Manufacturers are increasingly using renewable power sources in remote infrastructure projects, such as solar-powered monitoring stations. This trend represents the convergence of physical security with sustainable infrastructure, particularly in developing countries where energy efficiency and connectivity are critical drivers of long-term growth.

Hardware includes cameras, recorders, storage devices, and networking equipment. This segment remains essential but increasingly commoditized. Competition is intense, pricing pressure is high, and differentiation is limited to image quality, durability, and form factor. Hardware contributes volume but delivers lower margins.

The camera segment in this market is further categorized into hybrid cameras, analog cameras, and IP cameras. The hybrid camera sub-segment is expected to have a significant share in the global video surveillance market.

The hybrid security camera system is based on the digital video recorder (DVR). Hybrid surveillance cameras consist of high megapixel image sensors, interchangeable lenses, and use organic light-emitting diodes (OLED) or liquid crystal display (LCD) screens. Some of the market players, such as Panasonic Corporation, are offering a comprehensive product portfolio of hybrid cameras, which includes the Lumix GH4 series and HD camcorder HC-W580 series. These cameras are also capable of recording 4K videos and can be used for several cases, including surveillance. All the above factors are likely to fuel the demand for hybrid surveillance cameras.

Similarly, the analog cameras are ideal for those industries that require pan–tilt–zoom camera (PTZ camera) surveillance continuously. Analog cameras are generally used in traditional CCTV camera systems. These cameras have a limited resolution and can only cover a limited site range, due to which analog cameras are expected to observe a steady growth rate. The advantage of an analog camera over an IP camera is that the former performs better in low-light conditions. Market players such as Pelco offer Spectra Analog V cameras. These cameras encompass a wide range, low light capabilities, and can withstand in -40 degrees Celsius to 60 degrees Celsius.

Furthermore, IP cameras are likely to showcase an increasing demand during the forecast period. Cisco Systems, Inc. offers video surveillance cameras. These cameras exhibit high-quality video capabilities and efficient network utilization. Similarly, Honeywell International, Inc. provides performance series IP cameras, including micro dome IP cameras, IP bullet cameras, and many others. These cameras provide affordable surveillance solutions to cater to the security demands of the end-users.

The development of smart sensors that combine environmental monitoring (such as temperature and air quality) with visual analytics is a growing trend in component innovation. This multi-utility method improves the operational value of monitoring systems in power plants, transportation networks, and huge buildings. Vendors are pursuing modular hardware designs to decrease waste and increase lifespan value, which supports corporate ESG objectives.

By Software

Video Analytics Software is Likely to Have Unprecedented Growth in the Coming Years

The software segment is expected to have a significant video surveillance market growth owing to the increasing penetration of network security cameras. The established market players develop their own software, while the emerging market players can embed surveillance software from the independent software vendors (ISVs) in the market.

Software represents the primary value engine. Video management systems, analytics platforms, and artificial intelligence-driven applications command stronger pricing power. Software enables advanced capabilities such as real-time alerts, behavioral analysis, and system orchestration. Margins are structurally higher due to licensing models and recurring upgrades.

The software segment is further divided into video management software and video analytics software. Video management software enables users to view multiple camera footage, manage camera and recording settings, and set alerts for motion detection and unusual activities. For instance, Dahua Technology Co., Ltd. provides Easy4ip, a cloud-based video management software for small-scale enterprises or as a mobile application. In December 2019, Avigilon Corporation announced the upgrade of its video management software Avigilon Control Center (ACC) 7.4. The upgraded version incorporates facial recognition technology based on the applications of artificial intelligence.

Digital twins and simulation models are now being used in software platforms to forecast population flow and optimise energy consumption in smart-city contexts. Cloud-native software ensures scalability and interoperability, allowing for real-time insights in vital industries like defense, logistics, and energy distribution.

Video analytics software for surveillance cameras is projected to experience a significant growth rate in the coming years. Deploying advanced video analytics software is likely to create lucrative market opportunities for surveillance systems to deliver actionable insights and hindsight across a range of use cases. Video analytics software features can be integrated with the existing video management software (VMS). Honeywell International Inc. offers a wide range of video analytics solutions, including active alert and Alarm Management Server (AMS) for video analytics.

By Video Surveillance as a Service (VSaaS)

The VSaaS segment is anticipated to exhibit a high growth rate during the forecast period. This service refers to a complete cloud-based solution for surveillance. It includes cybersecurity solutions, video recording, remote viewing, and other services. VSaaS can be integrated with the existing video management solutions. For instance, Milestone Systems (Axis Communications AB) provides integrated Arcules VSaaS with its on-premise video management software XProtect. This integrated solution enables organizations to manage dispersed surveillance systems through a centralized platform.

VSaaS is the fastest-growing component. Cloud-based deployment, remote management, and subscription pricing appeal to organizations seeking scalability and predictable costs. This segment concentrates on long-term value through recurring revenue and customer lock-in.

By End-User Analysis

To know how our report can help streamline your business, Speak to Analyst

The Commercial Sector to Experience Significant Adoption of Video Surveillance Products and Services

Based on end-user, the market has been segmented into commercial, industrial, residential, and government. The commercial sector is estimated to hold a major market share. At the same time, the industrial sector is forecasted to experience a high CAGR as compared to the other end-users.

The commercial sector comprises industries such as retail, IT and telecommunication, BFSI, and healthcare. Retailers leverage the surveillance systems to analyze the activities of customers throughout the stores, enhance store management, and detect loitering in the store. Installing retail security cameras ensures a safer workplace, provides customer analytics, and offers a superior security performance. These factors contribute to the adoption of surveillance cameras in the retail industry.

Commercial users include retail, offices, hospitality, and transportation hubs. This segment emphasizes theft prevention, customer analytics, and operational visibility. Adoption of analytics-driven solutions is accelerating.

Similarly, the adoption of surveillance using cameras has gained traction in the healthcare industry. Hospitals that have embraced the network-based surveillance systems intend to combine cameras with audio systems and access networks over their IT networks. This integration would enable the hospitals to leverage surveillance cameras that would capture real-time data, generate real-time alerts, streamline the process, and analyze large volumes of data. These factors would ensure to facilitate the deployment of surveillance systems across the healthcare industry.

Furthermore, the use of AI-enabled surveillance in power utilities, oil refineries, and renewable energy farms is increasing, ensuring system dependability and environmental compliance. Public agencies are also using surveillance to support smart transportation, environmental monitoring, and urban safety projects, demonstrating the cross-sector impact of visual intelligence systems.

The industrial sector includes the manufacturing & construction industry, the automobile industry, and others. The manufacturing industry is prone to a range of security issues, including vandalism, theft of expensive machines, and raw materials such as optical fibers, copper wires, and steel. As a result, deploying organized surveillance systems using cameras throughout the manufacturing plant is likely to ensure safety and security across the industry. Industrial users focus on critical infrastructure, manufacturing plants, logistics centers, and energy facilities. Reliability, system resilience, and integration with safety systems drive purchasing decisions.

REGIONAL MARKET INSIGHTS

Asia Pacific Video Surveillance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific to Dominate the Market Throughout the Forecast Period

The global market has been analyzed across five major regions, including North America, Europe, Asia Pacific, the Middle East and Africa, and Latin America. These regions are further categorized into countries.

Asia-Pacific

Asia-Pacific represents the most dynamic regional growth environment. Rapid urbanization, large-scale infrastructure projects, and government-led smart city initiatives are major demand catalysts. Surveillance deployment is often embedded within broader public safety and urban management platforms. Price sensitivity remains higher in parts of the region, encouraging the adoption of scalable and locally manufactured solutions. Competitive intensity is elevated, with strong participation from regional vendors alongside global players.

The Asia Pacific market is expected to emerge as dominant during the forecast period. China holds a major share of the market. The government of China has been taking active initiatives for surveillance systems. In 2015, the government initiated a project named ‘Sharp Eyes’, an organized project for surveillance systems. In 2017, it completed the ‘Skynet video surveillance program’, which resulted in the largest video-surveillance network globally. Such active initiatives are likely to drive the video surveillance market growth in the region.

Furthermore, Asia Pacific's market expansion is fueled by national digital transformation agendas like China's "Digital Silk Road" and India's "Smart Cities Mission," both of which use AI-enabled monitoring to improve civic management and infrastructure resilience. Countries such as South Korea and Singapore are boosting their investments in cloud-native and energy-efficient surveillance systems that correspond with the International Energy Agency's (IEA) sustainability goals.

The region's expanding 5G infrastructure also allows for speedier data transmission, low-latency video analytics, and real-time threat detection capabilities. Furthermore, increased regulatory focus on data localization and cybersecurity, notably in Japan and India, is driving companies to develop compliance frameworks and local data centers to meet sovereign cloud needs.

Several major market players in China, including Huawei Technologies Co., Ltd., Hangzhou Hikvision Digital Technology Co., Ltd, Dahua Technology Co., Ltd, and ZTE Corporation, provide AI surveillance technology globally. Japan’s NEC Corporation is one of the major suppliers of AI surveillance technology, following the Chinese players. As a result, the presence of key market players in the region would boost market growth.

North America

North America represents a mature and technologically advanced market. Adoption is driven by enterprise security requirements, critical infrastructure protection, and strong penetration of cloud and analytics-based solutions. Replacement demand and system upgrades account for a growing share of activity, as organizations transition from legacy closed-circuit television systems to software-centric platforms. Regulatory scrutiny around privacy and data governance influences solution design, favoring vendors with strong compliance capabilities.

The North America market for video surveillance is anticipated to experience significant market growth in the coming years. In the United States, many cities have adopted advanced surveillance systems. For instance, as per a report, in 2018, after the Baltimore riots, the local police deployed advanced facial recognition cameras to identify and arrest protestors. The above data illustrates that the increasing external and internal human threats are likely to drive the need for advanced surveillance cameras in the region.

North America's growth is also being fueled by investments in smart infrastructure upgrades and energy-efficient surveillance technology integration. The US Department of Energy (DOE) has stressed the importance of intelligent monitoring systems in enhancing grid reliability and resilience, particularly in important facilities like data centers, airports, and energy networks.

AI-enabled cameras and edge analytics are increasingly being used in industries such as logistics, utilities, and healthcare to improve operational efficiency and compliance. Furthermore, there is a growing demand in the United States and Canada for cybersecurity-hardened surveillance platforms that meet National Institute of Standards and Technology (NIST) and Federal Information Processing Standards (FIPS) certification requirements, demonstrating the convergence of physical and cyber resilience in infrastructure protection.

Europe

Europe exhibits a fragmented but stable market structure. Western Europe shows consistent demand across transportation, commercial real estate, and public safety, supported by strong regulatory frameworks. Data protection regulations significantly shape procurement decisions, driving demand for privacy-by-design architectures and on-premise or hybrid deployments. Central and Eastern Europe present higher growth potential, supported by infrastructure modernization and increasing urban security investments, though budget constraints can moderate adoption speed.

The European video surveillance market is expected to exhibit a higher growth rate. In 2016, France, ZTE Corporation, and the port city of Marseille partnered to establish big data public tranquility projects. The project refers to a public surveillance network including several CCTV cameras and an intelligent operating center.

Similarly, in 2017, Huawei launched a surveillance system in the northern French town of Valenciennes, including high-definition CCTV surveillance and a smart command center to identify and detect undesired crowd formations and activities. The above data reflects that there is growing adoption of surveillance solutions for several purposes across the region. As a result, these factors are expected to fuel the market growth in the region.

Furthermore, Europe's adoption is heavily influenced by privacy legislation and ethical AI frameworks established by the European Union's General Data Protection Regulation (GDPR) and upcoming AI Act. To ensure compliance, vendors in the region prioritize privacy-by-design architectures and on-premise data storage strategies. The region is also working to improve public safety infrastructure, with the European Commission pushing the integration of monitoring networks with smart energy and green transportation projects. Markets in Germany, the Netherlands, and the Nordics are moving toward carbon-neutral video analytics platforms, with power consumption falling in line with IEA energy-efficiency standards.

Middle East and Africa

The Middle East and Africa region is at an earlier stage of adoption but holds strategic significance. Government-led infrastructure development, smart city programs, and large public events drive high-value deployments. Regulatory frameworks vary widely, and skills availability can constrain implementation. Long-term outlook remains positive as digital infrastructure investment expands.

The Middle East and Africa markets are expected to show moderate growth in the global market. Saudi Arabia is likely to be a business hub for many market players. Huawei is supporting the governing authorities of Saudi Arabia in building safe cities. BAE Systems plc., a U.K.-based arms manufacturer, sold mass surveillance systems in Saudi Arabia. Whereas, NEC Corporation is vending advanced facial recognition cameras in the region. All the above factors contribute to the fact that there are unprecedented video surveillance market opportunities in the region due to a smaller share of market players.

Latin America

Latin America remains an emerging market with uneven adoption. Demand is concentrated in metropolitan areas, transportation hubs, and commercial facilities. Public safety concerns and infrastructure development drive investment, though economic volatility and funding constraints can delay large-scale projects. Flexible financing models and managed services play a critical role in expanding market access.

Large-scale "Safe City" and "Vision 2030" programs in countries such as Saudi Arabia and the UAE are driving market growth in the Middle East, emphasizing AI-driven surveillance as part of national digital transformation. Energy companies in the Gulf are using advanced video analytics to monitor oil and gas facilities, balancing operational safety and environmental compliance. In Africa, smart infrastructure adoption is gradually increasing, particularly in South Africa and Kenya, where cloud-based surveillance and renewable-powered monitoring systems are gaining favor. The region's focus on protecting crucial energy and transportation infrastructure is projected to open up long-term potential for integrated AI-video solutions.

Latin America's video surveillance market is likewise steadily growing. Brazil, Mexico, and Chile are investing in urban security and public transportation surveillance networks. Smart infrastructure expansion in cities like São Paulo and Mexico City is improving operational safety and emergency response capacities through partnerships with technology suppliers. However, political instability and budgetary constraints continue to limit large-scale adoption, making cost-effective cloud monitoring options more appealing to both public and private enterprises.

Which industries are driving demand?

Demand within the Video surveillance market is being shaped by a widening range of industry-specific use cases that extend beyond traditional security monitoring. Adoption patterns differ markedly between large enterprises and small and medium-sized businesses, reflecting variations in risk exposure, operational complexity, and capital availability. Across both groups, surveillance is increasingly positioned as an operational intelligence tool rather than a standalone security function.

Large enterprises remain the primary demand drivers. Multisite organizations in retail, logistics, transportation, and critical infrastructure rely on video surveillance to manage complex operations at scale. These users prioritize centralized monitoring, advanced analytics, and integration with access control, building management, and incident response systems. Their use cases emphasize loss prevention, compliance enforcement, and operational optimization.

Small and medium-sized businesses are adopting surveillance for more focused objectives. Cost-effective systems and Video Surveillance as a Service offerings have lowered barriers to entry. Typical use cases include premises security, employee safety, and liability management. Simplicity, remote access, and predictable pricing drive purchasing decisions in this segment.

How competitive is the market?

Investments in Research and Development by Zhejiang Dahua Technology Co., Ltd. to Empower Technological Innovations

Zhejiang Dahua Technology Co., Ltd. is a provider of video-based smart IoT solutions and a service provider. Dahua Technology offers complete security systems, solutions, and services. The company’s surveillance product portfolio includes network video recorders (NVRs), network cameras, and HD cameras. For the upliftment of its business, the company has adopted some of the business strategies, such as:

- Increase investments in R&D to facilitate technological innovations in cloud computing, big data analytics, artificial intelligence, and other core technologies.

- Expand and upgrade the product portfolio, intending to offer comprehensive solutions and services in the video surveillance industry. For instance,

- September 2019 - Zhejiang Dahua Technology Co., Ltd. announced the integration of 5 Megapixel IP cameras in its Lite series. The company has also incorporated smart motion detection (SMD) technology for enhanced accuracy and reduced false alarms.

- June 2019 - Zhejiang Dahua Technology Co., Ltd. launched the StereoVision camera. StereoVision camera is a people-counting camera consisting of a 3MP dual sensor that incorporates artificial intelligence (AI) capabilities.

Dahua has recently expanded its R&D footprint beyond China, establishing innovation centers in Europe and North America to build global relationships and adhere to regional cybersecurity and privacy regulations. The company is increasingly focusing on energy-efficient chipsets and edge AI solutions that minimize data processing burdens while meeting environmental performance targets.

The Video surveillance market is highly competitive, with a mix of global incumbents, regional specialists, and technology-focused entrants shaping market structure. Market leadership is concentrated among vendors with broad product portfolios, strong software capabilities, and established distribution networks. These players typically compete on system reliability, analytics sophistication, cybersecurity resilience, and long-term service support.

Large incumbents leverage scale advantages in manufacturing, research, and channel partnerships to defend their Video surveillance market share. Their strategies increasingly emphasize platform-based ecosystems that integrate cameras, analytics, storage, and cloud services. Differentiation is shifting away from hardware specifications toward software intelligence, interoperability, and lifecycle management.

Challengers and new entrants focus on specific niches, such as artificial intelligence-driven analytics, cloud-native surveillance platforms, or vertical-specific solutions. These firms often demonstrate faster innovation cycles and greater flexibility, but face constraints in global reach and regulatory navigation. Competitive pressure is particularly intense in price-sensitive segments, where commoditization has lowered barriers to entry.

The market continues to see active merger and acquisition activity. Acquisitions frequently target software firms, analytics providers, and regional distributors to strengthen capabilities and accelerate expansion. Strategic partnerships between hardware vendors, cloud providers, and system integrators are also increasing, reflecting the growing importance of ecosystem depth over standalone offerings.

Key Market Players Strengthening Market Position through Strategic Partnerships

In September 2019, Hangzhou Hikvision Digital Technology Co., Ltd. partnered with Scylla Technologies Inc., a provider of Smart Suspect Identification Systems (SSIS), vehicle identification and tracking (VIT), and preventive threat detection (PTD). This partnership aims to integrate Scylla Technologies’ AI-powered systems with Hikvision cameras and NVRs (network video recorders).

Similarly, in April 2018, Pelco collaborated with IBM Corporation to develop 'Pelco Analytics driven by IBM'. This collaboration aims to integrate IBM‘s deep learning analytics solutions with the video management system (VMS) offered by Pelco. The strategic partnerships are likely to encourage the market players to exploit new technology, access new customers, expand business across geographic markets, and extend their product portfolio.

In addition to these alliances, multinational manufacturers are forming cross-industry partnerships with telecom providers, cybersecurity organizations, and cloud service platforms to create unified security ecosystems. The strategic emphasis is turning toward open architecture approaches that allow for interoperability across devices and software. This method is designed to speed up AI integration, improve data exchange, and encourage compliance with sustainability and data protection regulations. Furthermore, regional firms specializing in AI-based surveillance software, mostly in Israel, Singapore, and the United States, are emerging as innovation hubs, attracting venture capital investment and altering the industry's competitive dynamics.

Top Companies In The Video Surveillance Industry:

- Avigilon Corporation

- Axis Communications AB

- BCDVideo

- Bosch GmbH

- Dahua Technology Co., Ltd

- FLIR Systems, Inc.

- Hangzhou Hikvision Digital Technology Co., Ltd

- Honeywell International, Inc

- Huawei Technologies Co., Ltd.

- Panasonic Corporation

- Pelco

How are technology and digital transformation shaping the market?

Innovation is redefining the competitive logic of the Video surveillance market. Artificial intelligence and machine learning are now central to system value, enabling real-time threat detection, behavioral analysis, and automated incident response. These capabilities reduce manual oversight while increasing accuracy and scalability.

Cloud computing is transforming deployment and operating models. Cloud-based and hybrid architectures support centralized management, remote access, and rapid system updates. This shift lowers infrastructure complexity and enables Video Surveillance as a Service models that appeal to organizations seeking operational flexibility and predictable costs.

Edge computing complements this transition by enabling analytics at the camera level. Processing data closer to the source reduces latency, improves resilience, and addresses bandwidth constraints. Combined with advances in video compression and storage optimization, these technologies improve overall system efficiency.

Digital transformation also reshapes cost structures. Automation reduces labor dependency, while predictive maintenance extends system lifespan. As video data becomes integrated with enterprise platforms and operational workflows, surveillance evolves into a strategic data asset. Long-term competitive advantage will favor vendors that unify intelligence, security, and operational insight within scalable digital architectures.

What are the growth opportunities?

The most attractive opportunities in the Video surveillance market lie in segments undergoing structural transformation rather than simple volume expansion. Software-driven analytics, cloud-based surveillance platforms, and managed services represent the strongest long-term value pools. These segments benefit from recurring revenue, higher margins, and stronger customer retention.

Underserved opportunities persist among small and medium-sized enterprises, residential multi-unit properties, and emerging urban infrastructure projects. Video Surveillance as a Service models are particularly well-suited to these segments due to lower upfront costs and simplified deployment. Geographic expansion in emerging economies also presents long-term upside as digital infrastructure investment accelerates.

Adjacent growth opportunities include integration with access control, building automation, traffic management, and safety systems. Surveillance data increasingly supports operational optimization, not just security outcomes. This broadens monetization pathways beyond traditional security budgets.

From an investment perspective, short-term strategies favor software enhancement and ecosystem partnerships. Long-term value creation depends on platform scalability, regulatory adaptability, and the ability to convert video data into actionable intelligence. Organizations that align innovation with evolving compliance and operational demands are best positioned to capture sustained Video surveillance market growth.

KEY INDUSTRY DEVELOPMENTS:

- In July 2021, Axis Communications AB announced that its selected camera offerings are ONVIF Profile M conformant. These cameras enable standardized streaming of events and metadata from edge-based analytics use cases in a multi-vendor surveillance arrangement. Conformance to Profile M facilitates integration of events and metadata with ONVIF Profile M conformant users, like video management software and services.

- In May 2021, FLIR Systems, Inc. won a USD 15.4 million agreement from the United States Army to provide its Black Hornet PRS. PRS is the Airborne Personal Reconnaissance System for dismounted soldiers. Under the Army's Soldier Borne Sensor program (SBS), the Black Hornet nano-unmanned aerial vehicles, also called UAVs, are deployed to augment reconnaissance capabilities, and squad & unit-level surveillance.

- In April 2021, BCDVideo partnered with Wasabi, a hot cloud storage company headquartered in Boston, Massachusetts. Through this partnership, the companies aim to offer video surveillance storage in the cloud. Also, the partnership expands the ability of the companies to offer a comprehensive package of BCDVideo’s on-premises, purpose-built storage alternatives and Wasabi Technologies' hot cloud storage solutions.

- In February 2021, Motorola Solutions established a new video security & analytics manufacturing center in Texas. The new facility is a part of the company’s expansion of shipping and production capabilities and continuous investment in manufacturing in North America to strengthen the development of its video security offerings.

- In March 2020, Axis Communications launched body body-worn camera solution specifically designed for private security and law enforcement. The Axis body-worn camera solution includes a docking station, a robust camera, and a system controller designed on an open architecture. The solutions allow integration with a wide range of evidence management systems (EMS) and video management systems (VMS).

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The video surveillance market report highlights leading regions across the world to offer a better understanding of the user. Furthermore, the report provides insights into the latest video surveillance industry trends and analyzes technologies that are being deployed at a rapid pace at the global level. The report examines various paradigm shifts associated with the transformation of hardware and software. It further highlights some of the growth-stimulating factors and restraints, helping the reader to gain in-depth knowledge about the video surveillance market.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021 - 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2034 |

|

Historical Period |

2021 - 2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Component

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market was valued at USD 83.71 billion in 2025

Fortune Business Insights says that the market is expected to reach USD 261.65 billion in 2034

Growth of 13.5% CAGR will be observed in the market during the forecast period (2026-2034)

In terms of end-user, the industrial sector segment is expected to lead during the forecast period

Growing adoption of body worn cameras and the emergence of AI surveillance systems are some of the key market drivers

Hangzhou Hikvision Digital Technology Co., Ltd, Dahua Technology Co., Ltd, FLIR Systems, Inc., and Avigilon Corporation are some of the top companies in the market

Asia Pacific is expected to hold a major market share

The revenue of the market in Asia Pacific in 2025 was USD 10.58 billion

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us