Animal Health Market Size, Share and Industry Analysis By Product (Drugs, Vaccines, Feed, and Diagnostics), By Animal (Livestock Animals and Companion Animals), By End User (Veterinary Hospitals & Clinics, Animal Care & Rehabilitation Centers, Diagnostic Centers) and Geography Forecast 2026-2034

Animal Health Market Size and Industry Overview

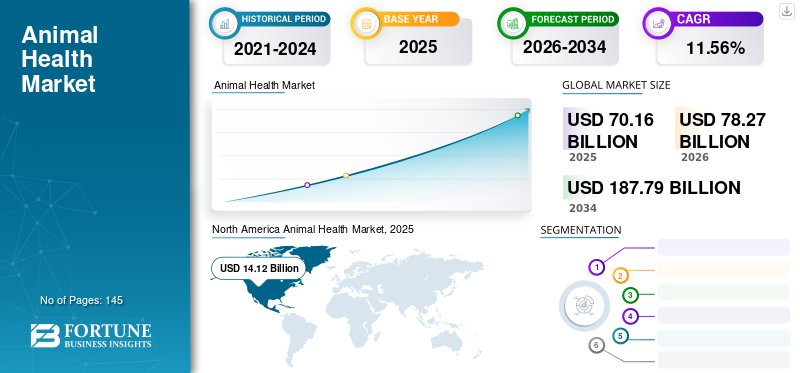

The global animal health market size was valued at USD 70.16 billion in 2025. The market is projected to grow from USD 78.27 billion in 2026 to USD 187.79 billion by 2034, exhibiting a CAGR of 11.56% during the forecast period. North America dominated the global market with a share of 34.02% in 2025.

Animal healthcare involves taking care of animals with the appropriate use of drugs, vaccines, medicated animal feeds, and diagnostic products to treat the medical conditions related to them. Animals hold great importance in human life. They provide food, protection, as well as companionship to humans.

The animal health market is expanding steadily as veterinary care becomes integral to food security, public health protection, and companion animal well-being. Animal health encompasses pharmaceuticals, vaccines, diagnostics, and nutritional solutions designed to prevent, detect, and manage diseases across livestock and companion animals. Growth reflects structural demand rather than short-term cycles, supported by rising protein consumption, urban pet ownership, and stricter biosecurity frameworks.

Livestock animals account for a substantial share of market revenue due to their economic importance and exposure to disease risk. Producers increasingly invest in preventive health programs to reduce mortality, improve feed conversion, and stabilize output. Vaccination, parasite control, and herd diagnostics are prioritized as cost-effective alternatives to reactive treatment. These practices directly influence the animal health market size by improving productivity across cattle, poultry, swine, and aquaculture systems.

Companion animals represent the fastest-growing segment. Pet humanization continues to reshape spending behavior, particularly in North America, Europe, and parts of the Asia-Pacific. Owners seek advanced therapeutics, chronic disease management, and routine diagnostics that mirror human healthcare standards. This shift supports premium pricing and higher lifetime value per animal, strengthening overall animal health market growth.

Pharmaceuticals remain the largest product category, driven by antiparasitics and anti-infectives, although regulatory pressure is gradually reshaping portfolios. Vaccines gain momentum as disease prevention aligns with regulatory, economic, and sustainability goals. Diagnostics increasingly guide treatment decisions, enabling earlier intervention and more targeted therapy.

Regionally, North America leads in innovation intensity and per-animal spending, while Asia-Pacific contributes significant volume growth due to expanding livestock populations and rising pet ownership. Europe emphasizes preventive care and antimicrobial stewardship, influencing product mix and adoption patterns.

Moreover, animals serve as models in biological research, such as genetics and drug testing. The growing awareness about animal diseases, increasingly stringent regulations, and growing focus on preventing diseases that originated from animal epidemics are expected to increase the demand for animal healthcare products.

Owing to these factors, the veterinary healthcare market is significantly growing across all regions. The market is mainly driven by a substantial rise in pet adoption, increased incidence of zoonotic diseases, food-borne diseases, and growing demand for protein-rich food globally. Moreover, technological expansions in the market and the advent of information systems are boosting the growth of the animal health market.

Download Free sample to learn more about this report.

Animal Health Market Key Takeaways

- 2025 Market Size: USD 70.16 Billion

- 2026 Market Size: USD 78.27 Billion

- 2034 Forecast Market Size: USD 187.79 Billion

- CAGR: 11.56% from 2026–2034

- North America dominated the global animal health market with a 34.02% share in 2025.

- Drugs accounted for the largest product segment share, representing 45.5% of the market in 2025.

- Companion animals held the largest share among animal segments in 2025.

North America

North America generated USD 14.12 billion in revenue in 2025 and remained the leading regional market.

Europe

Europe held the second-largest market position, supported by strong animal health regulations and preventive care adoption.

Asia Pacific

Asia Pacific is expected to witness healthy growth driven by expanding veterinary infrastructure and rising protein consumption.

U.S.

The country leads the regional market due to large-scale livestock operations and a highly developed companion animal ecosystem.

Japan

Market growth is supported by advanced veterinary care, preventive healthcare adoption, and increasing demand for chronic disease management in pets.

Read More

Key Market Dynamics

Animal Health Market Trends

Download Free sample to learn more about this report.

- North America witnessed a growth from USD 13.34 billion in 2025 to USD 14.12 billion in 2026.

Increasing Adoption of Pets by People for Companionship

The adoption of pets is a significant market trend. People largely adopt pets for companionship, and there has been a momentous swing in trend from pet holders to pet parentages. According to the American Pet Products Association (APPA) in 2019, 67% of U.S. households own a pet. Hence, the increase in the pet owners’ population is propelling the veterinary health market growth.

Public-Private Partnerships for Animal Health

Public-private partnerships continue to strengthen the demand for animal care products due to increased awareness and availability. According to the OIE-World Organization of Animal Health survey 2017, Public-Private Partnership (PPP) in the veterinary health domain has the potential to improve the quality of veterinary services worldwide. This is likely due to the restructuring of dynamic and sustainable systems contributing to the health and welfare of human inhabitants.

Preventive care is reshaping the animal health market’s product mix. Vaccines and diagnostics gain prominence as stakeholders prioritize disease avoidance over treatment. This shift aligns with regulatory goals, cost containment, and sustainability objectives. Producers increasingly adopt structured health programs rather than episodic interventions.

Diagnostics are becoming central to veterinary decision-making. Rapid testing, molecular assays, and point-of-care tools enable earlier detection and precise treatment selection. These capabilities reduce unnecessary drug usage and improve outcomes, especially in herd environments. Diagnostic-driven care models also enhance data collection and health surveillance.

Digitalization represents another defining trend. Practice management software, remote monitoring tools, and data analytics platforms support veterinarians and producers in tracking animal health metrics. These tools improve compliance, scheduling, and treatment accuracy while strengthening client engagement.

Companion animal care continues to mirror human healthcare trends. Chronic disease management, personalized nutrition, and preventive wellness plans gain traction. Pet insurance adoption supports higher utilization of advanced services, reinforcing revenue stability for veterinary providers.

Sustainability considerations increasingly influence product development. Manufacturers invest in alternatives to traditional antimicrobials, including biologics and immunomodulators. Feed additives supporting gut health and immunity also attract attention.

Market Drivers

Increasing Incidence of Zoonotic Diseases to Drive Market

An increase in the incidence of zoonotic diseases is likely to drive the veterinary healthcare market. The increasing adoption of pets for companionship is resulting in growing contact with the disease, spreading animal-borne diseases across the world. Rise in the awareness about preventive measures and growing availability of treatment options are likely to drive the demand for animal care products during the forecast period. According to the Centre for Disease Control (CDC), each year, thousands of Americans get ill from disease transmission from animals.

Increasing R&D Activities in Veterinary Medicine to Provide Lucrative Growth Opportunities

Animals play a vital role in the development of healthcare products by serving as test subjects for drugs and medical devices. The use of animals as a subject in drug discovery is important because research on many genetic and prolonged diseases of humans cannot be approved for testing on humans. In the U.S. alone, thousands of mice and monkeys are used as test subjects in research laboratories each year.

Animal studies are used in developing new surgical techniques (e.g., organ transplantations), testing new drugs for safety, and nutritional research. Animals are mainly valuable in research involving long-lasting, deteriorating diseases because such diseases can be studied in animals with comparative ease, hence promoting the overall expansion of the market size.

Rising global demand for animal-derived protein remains a foundational driver for the animal health market. Livestock producers face increasing pressure to maximize productivity while minimizing disease-related losses. Preventive veterinary care, including vaccination and routine health monitoring, has become central to modern herd management strategies. These practices directly improve yield stability and operational efficiency, reinforcing sustained investment in animal health solutions.

Companion animal ownership continues expanding across urban and semi-urban regions. Pets are increasingly viewed as family members, shifting owner expectations toward higher standards of medical care. This behavioral change drives demand for advanced pharmaceuticals, diagnostics, and long-term disease management therapies. Veterinary clinics respond by expanding service offerings, further strengthening market demand.

Regulatory emphasis on food safety and zoonotic disease prevention also supports market growth. Governments and international bodies promote structured animal health programs to mitigate risks associated with disease transmission. Compliance requirements encourage adoption of approved vaccines, diagnostics, and treatment protocols.

Technological advancements reinforce these drivers. Improvements in biologics, molecular diagnostics, and formulation science enhance treatment efficacy and safety. These innovations enable earlier detection and targeted intervention, reducing overall disease burden.

Market Restraints

Stringent Government Regulations on Approval for Animal Drugs to Restrict the Market Growth

Strict government regulations on the approval of animal drugs are likely to hinder the market growth. All animal drugs require approval from the U.S. Food and Drug Administration for sale in the U.S. According to the Animal Health Institute, the development of a new animal drug can take up to 10 years and cost more than USD 100 million before approval.

A new vaccine takes three to five years to develop and costs around USD 80 million. Animal health product manufacturers support the FDA approval process through user fees authorized by the Animal Drug User Fees Act (ADUF) and the Animal Generic Drug User Fee Act.

Despite favorable demand fundamentals, the animal health market faces several structural constraints. Regulatory scrutiny around antimicrobial usage remains a significant challenge. Governments increasingly restrict antibiotic use in livestock to address antimicrobial resistance concerns. While necessary, these policies complicate treatment protocols and limit product availability, particularly in developing regions with limited alternatives.

Cost sensitivity among livestock producers also restrains adoption. Margins in commercial farming remain volatile, influenced by feed prices, climate variability, and trade dynamics. Producers may delay investments in premium animal health products during periods of economic stress, prioritizing short-term survival over long-term health optimization.

Access disparities further constrain market expansion. Veterinary infrastructure remains uneven across rural and emerging markets. Limited availability of trained professionals, diagnostic facilities, and cold-chain logistics reduces penetration of advanced animal health solutions. These gaps slow adoption despite the underlying disease risk.

Product development costs represent another restraint. Research, clinical validation, and regulatory approval require long timelines and substantial capital. Smaller manufacturers face barriers to entry, reducing competitive diversity in certain therapeutic areas. Additionally, vaccine hesitancy and limited disease awareness persist in some regions. Without adequate education, farmers may underutilize preventive solutions, relying instead on reactive treatment.

Market Opportunities

Emerging markets present substantial growth opportunities for the animal health industry. Expanding livestock populations, rising incomes, and improving veterinary awareness support increased adoption of formal health programs. As infrastructure improves, demand for vaccines, diagnostics, and nutritional solutions is expected to accelerate.

Companion animal segments offer strong upside potential. Growing middle-class populations in the Asia-Pacific and Latin America drive pet ownership and discretionary healthcare spending. Tailored products addressing regional disease profiles and affordability constraints can unlock new revenue streams.

Innovation creates additional opportunity. Development of novel biologics, recombinant vaccines, and precision diagnostics enables differentiation in crowded therapeutic categories. Companies that align innovation with regulatory priorities, such as antimicrobial stewardship, gain a strategic advantage.

Service-based models represent another opportunity. Integrated offerings combining diagnostics, treatment, and advisory support strengthen customer retention. Veterinary service providers increasingly value end-to-end solutions rather than standalone products.

Public-private collaboration also supports market expansion. Government-led disease eradication programs and food security initiatives create large-scale procurement opportunities. Participation in such programs enhances volume stability and market visibility.

SEGMENTATION ANALYSIS

By Product Analysis

To know how our report can help streamline your business, Speak to Analyst

Drugs Segment to Hold Largest Share During Forecast Period

Based on product, the market segments include drugs, vaccines, feed, and diagnostics.

The drugs segment accounted for the largest market share in the year 2025. The segment is projected to continue its dominance throughout the forecast period. This is attributable to the growing prevalence of various diseases in animals and the growing number of prescriptions to treat them. The drugs are required for the prevention, control, and eradication of animal diseases. Diseases of animals remain a concern primarily because of the economic losses they cause and the possible transmission of the causative agents present in their bodies to humans. The Drugs segment is expected to hold a 45.5% share in 2025.

Drugs represent the largest product category within the animal health market, driven by consistent demand for therapeutics addressing infectious diseases, parasitic infestations, and chronic conditions. Antibiotics, antiparasitics, anti-inflammatory drugs, and pain management therapies remain essential across both livestock and companion animal care. However, regulatory oversight increasingly influences formulation and usage patterns.

Manufacturers focus on optimized dosing, targeted delivery, and alternatives to traditional antimicrobials to align with resistance mitigation goals. In livestock operations, drugs remain critical for disease containment and productivity protection, while in companion animals, long-term treatment for dermatological, metabolic, and orthopedic conditions sustains demand.

Vaccines form a rapidly expanding segment as preventive care gains prominence. Livestock producers rely on vaccination programs to protect herd health, reduce mortality, and stabilize output. In poultry and swine farming, vaccines play a central role in biosecurity strategies. Companion animal vaccination schedules continue evolving, incorporating broader disease coverage and combination formulations. Advances in recombinant and vector-based vaccines improve efficacy and safety profiles. Regulatory encouragement of vaccination over treatment reinforces long-term growth across this segment.

Feed products, including medicated feed and nutritional supplements, occupy a strategic position between prevention and performance enhancement. Feed additives supporting gut health, immunity, and growth efficiency attract increasing attention. Livestock producers adopt functional feed solutions to improve feed conversion ratios while complying with antimicrobial restrictions. In companion animals, premium nutrition formulations address age-specific and condition-specific needs. The feed segment benefits from rising awareness of nutrition’s role in disease prevention and overall health optimization.

The diagnostics segment is projected to expand at a significantly high growth rate during the forecast period, owing to the launch of a large number of new products and techniques observed in the market. Diagnostics represent one of the most transformative product segments. Rapid diagnostic tests, molecular assays, and imaging tools enable earlier disease detection and targeted intervention.

Veterinary practices increasingly integrate diagnostics into routine care, reducing reliance on empirical treatment. In livestock systems, diagnostics support surveillance, outbreak control, and compliance reporting. Companion animal diagnostics expand alongside rising expectations for advanced care. This segment underpins precision medicine trends and strengthens demand for integrated animal health solutions.

By Animal Analysis

Companion Animal Segment to Gain Momentum During Forecast Period

By animal, the market segments include livestock animals and companion Animals.

Livestock animals account for a substantial share of the animal health market due to their direct link to food production and economic output. Cattle, poultry, swine, and small ruminants require structured health management to ensure productivity, disease control, and food safety compliance. High-density farming environments increase disease transmission risks, elevating demand for vaccines, diagnostics, and preventive therapeutics. Governments and industry bodies emphasize livestock health to protect food supply chains, reinforcing stable long-term demand. Investment decisions in this segment often prioritize cost efficiency, scalability, and regulatory compliance.

The companion animals segment held the largest veterinary healthcare market share in 2025 due to the increasing trend of keeping pets at home. Moreover, this segment is likely to grow rapidly by the end of 2026, attributed to the growing rate of pet adoption to aid the elderly & physically challenged people and shift in tendency from pet owners to pet nurturing. Companion animals represent a faster-growing segment driven by demographic and cultural shifts. Dogs, cats, and other pets increasingly receive healthcare comparable to human standards.

Pet owners seek early diagnosis, chronic disease management, and preventive wellness services. This behavior supports demand for advanced drugs, vaccines, diagnostics, and specialty nutrition. Urbanization and rising disposable incomes further strengthen this segment, particularly in emerging economies. Emotional attachment to pets reduces price sensitivity, enabling adoption of premium animal health products.

By End-User Analysis

Veterinary Hospitals & Clinics to Continue Dominating Market

Global animal health market segments based on end-user include veterinary hospitals & clinics, animal care and rehabilitation centers, diagnostic centers, and others.

The veterinary hospitals & clinics segment accounted for the largest share in the market in 2018. An increasing number of pet hospitals and clinics, along with the awareness regarding the spread of zoonotic diseases, have supported the segment growth. The diagnostic centers segment is likely to grow rapidly during the forecast period, owing to the rise in awareness about the welfare and significance of precautionary care in pets among companion animal holders.

Veterinary hospitals and clinics constitute the primary end-user segment within the animal health market. These facilities serve as central access points for diagnosis, treatment, and preventive care. Growth in this segment reflects expanding service offerings, including imaging, laboratory diagnostics, and specialized treatments. Clinics increasingly adopt integrated practice management systems, improving workflow efficiency and patient outcomes. Companion animal clinics, in particular, benefit from rising pet insurance coverage and higher client engagement.

Animal care and rehabilitation centers play an important supporting role. These facilities focus on recovery, physiotherapy, long-term care, and behavioral rehabilitation. Their relevance grows alongside increased awareness of post-treatment quality of life for animals. Rehabilitation services support orthopedic recovery, neurological conditions, and chronic pain management. Demand in this segment aligns closely with trends toward holistic animal care and extended treatment cycles. Moreover, the introduction of molecular diagnostic tests like ELISA and PCR now accounts for a major part of the animal healthcare center, which is also driving the market.

Diagnostic centers represent a specialized and rapidly expanding end-user category. Independent diagnostic laboratories and imaging centers support veterinarians with advanced testing capabilities. These centers invest in high-throughput analyzers, molecular diagnostics, and pathology services. Outsourcing diagnostics allows clinics to access advanced tools without high capital expenditure. In livestock management, centralized diagnostic centers support surveillance programs and large-scale disease monitoring. Growth in this segment reflects the broader shift toward data-driven decision-making in animal health.

REGIONAL ANALYSIS

North America Animal Health Market, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Animal Health Market Analysis:

North America is expected to hold the largest share in the global animal health market during the forecast period. North America, being technologically advanced in terms of research and development of therapeutics and diagnostics, shows indications of dominant geography. Moreover, the significant rise in pet adoption and an increase in incidences of zoonotic diseases are widespread in the region.

North America represents a mature and highly structured animal health market, supported by advanced veterinary infrastructure and strong regulatory oversight. High livestock productivity standards and sophisticated companion animal care drive steady demand. Preventive healthcare adoption remains high, particularly for vaccines and diagnostics. Strong research activity and rapid commercialization of new therapeutics reinforce market stability. Companion animal spending continues rising, supporting premium product penetration.

United States Animal Health Market:

The United States dominates the regional market share due to large-scale livestock operations and a highly developed companion animal ecosystem. Veterinary service utilization remains high, supported by pet insurance growth and advanced clinical capabilities. Regulatory scrutiny around antimicrobial use shapes product development strategies. Innovation in diagnostics and biologics remains concentrated in the United States, reinforcing its leadership within the global animal health market.

Europe Animal Health Market Analysis:

The European region is expected to hold the second position in this market by witnessing consistent growth in the long-term period. Increased consumption of animal-based food, as well as strong animal health regulations, are responsible for market expansion.

The European animal health market is shaped by stringent regulatory frameworks and strong emphasis on preventive care. Livestock health policies prioritize disease surveillance and antimicrobial reduction, supporting vaccine and diagnostic demand. Companion animal care benefits from high veterinary access and growing pet ownership. Sustainability considerations increasingly influence product formulation, packaging, and supply chains, affecting procurement decisions across the region.

Germany Animal Health Market:

Germany reflects a highly regulated and technologically advanced animal health environment. Livestock producers emphasize compliance, traceability, and disease prevention, supporting consistent vaccine adoption. Companion animal care benefits from well-established veterinary networks and high client expectations. Diagnostic utilization continues expanding as veterinarians adopt precision approaches. Germany’s strong manufacturing base supports domestic production and export of animal health products.

United Kingdom Animal Health Market:

The United Kingdom animal health market balances livestock productivity requirements with advanced companion animal services. Biosecurity and disease monitoring remain central to livestock health strategies. Pet ownership growth supports steady demand for diagnostics, therapeutics, and wellness products. Veterinary practices increasingly integrate digital tools to improve care delivery. Regulatory alignment with European standards continues to influence product approvals and clinical protocols.

Asia-Pacific Animal Health Market Analysis:

As per our market research Analysts, the Asia Pacific is expected to witness healthy growth in terms of animal health care products. Countries in the Asia Pacific, such as China, Japan, and India, have diverse classes of economic development, which results in a growing number of biopharma companies focusing on animal health to modernize the drug discovery process. Latin America and the Middle East & Africa are expected to register a slightly higher growth owing to the increasing demand for technologies.

Asia-Pacific represents one of the fastest-expanding animal health markets, driven by rising protein consumption and improving veterinary infrastructure. Livestock disease management remains a priority in densely populated production systems. Companion animal ownership grows rapidly in urban centers, supporting demand for modern veterinary services. Market growth reflects increasing investment in diagnostics, vaccines, and professional veterinary education.

Japan Animal Health Market:

Japan’s animal health market emphasizes quality, safety, and preventive care. Livestock health programs focus on disease control and productivity optimization within limited agricultural land. Companion animals receive advanced care, supported by high veterinary standards and diagnostic adoption. Aging pet populations increase demand for chronic disease management. Regulatory consistency supports predictable market development and long-term investment.

China Animal Health Market:

China’s animal health market continues to expand as livestock modernization accelerates and regulatory enforcement strengthens. Disease prevention remains critical within large-scale poultry and swine operations. Companion animal healthcare grows rapidly in urban regions, driving demand for diagnostics and therapeutics. Domestic manufacturers expand capabilities, while international firms target partnerships to navigate regulatory complexity and regional distribution networks.

Latin America Animal Health Market Analysis:

The Latin America animal health market is closely linked to its role as a major livestock exporter. Cattle and poultry health programs prioritize disease prevention and productivity enhancement. Veterinary service access varies across countries, influencing adoption rates. Companion animal care grows steadily in urban areas. Market expansion depends on improving veterinary infrastructure and consistent regulatory enforcement.

Middle East & Africa Animal Health Market Analysis:

The Middle East & Africa animal health market develops gradually, supported by livestock dependency and food security initiatives. Disease surveillance and vaccination programs remain essential in pastoral systems. Companion animal care grows selectively in urban centers. Limited veterinary access in some regions constrains adoption, but public-sector programs support baseline demand for essential animal health products.

Competitive Landscape

Zoetis Focusses on Acquisition of Innovative Laboratories to Strengthen Its Comprehensive Diagnostics Portfolio

Companies in the market include top players engaged in the development of animal drugs, vaccines, medicated animal feed, and novel diagnostic tests. Several key strategies adopted by leading market players include the introducing of new products in specialty disease areas and the expansion of footprints across geographies with mergers, acquisitions, and partnerships.

The animal health market features a concentrated competitive structure led by multinational pharmaceutical and biotechnology companies, supported by a growing ecosystem of regional specialists and diagnostics-focused firms. Market leaders maintain broad portfolios spanning pharmaceuticals, vaccines, diagnostics, and feed additives, allowing them to serve both livestock and companion animal segments at scale. Their competitive strength derives from extensive research pipelines, global manufacturing footprints, and long-standing relationships with veterinary professionals and distributors.

Leading vendors prioritize lifecycle management of core products through formulation improvements, combination therapies, and expanded indications. Investment in biologics, preventive vaccines, and advanced diagnostics remains central to sustaining market share. These companies also benefit from strong regulatory expertise, enabling faster approvals and consistent compliance across regions. Brand trust among veterinarians and producers reinforces pricing power, particularly in mature markets.

Niche players occupy strategically important segments, including specialty diagnostics, parasiticides, aquaculture health, and precision nutrition. Many focus on targeted therapeutic areas where agility and technical specialization outweigh scale advantages. Diagnostic-focused firms differentiate through rapid testing platforms, molecular diagnostics, and data-driven disease monitoring tools. Smaller innovators increasingly address unmet needs in antimicrobial alternatives, immunomodulators, and species-specific formulations.

Partnerships shape competitive dynamics across the animal health industry. Large vendors collaborate with biotechnology startups to access novel platforms such as recombinant vaccines, monoclonal antibodies, and genomic diagnostics. Strategic alliances with veterinary hospital chains and diagnostic laboratories support integrated care models. Distribution partnerships remain critical in emerging markets, where local expertise facilitates regulatory navigation and market access.

Competitive differentiation increasingly depends on:

- Depth and sustainability of innovation pipelines

- Integration of diagnostics with therapeutic offerings

- Ability to support preventive and precision healthcare models

- Strength of veterinary education and technical support programs

- Geographic reach and supply chain resilience

LIST OF KEY COMPANIES PROFILED:

- Zoetis

- Intervet International B.V.

- Elanco

- Ceva

- Virbac

- Merck & Co., Inc.

- Novartis AG

- Emergent BioSolutions, Inc.

- CSL Limited

- IDEXX Laboratories, Inc.

- Bayer AG

- Boehringer Ingelheim International GmbH

- Other Prominent Players

Animal Health Industry Key Developments

- March 2025: Zoetis expanded its companion animal portfolio through the launch of a next-generation monoclonal antibody therapy aimed at chronic pain management in dogs, leveraging biologics engineering to improve long-duration efficacy and treatment compliance.

- January 2025: Elanco Animal Health completed a strategic acquisition of a specialty diagnostics company to strengthen its disease detection capabilities, integrating rapid immunoassay platforms and cloud-enabled diagnostic data workflows into its preventive care ecosystem.

- October 2024: Boehringer Ingelheim Animal Health introduced an advanced multivalent vaccine for livestock disease prevention, developed using recombinant technology to enhance immune response consistency while reducing administration frequency in large-scale production environments.

- July 2024: Merck Animal Health deployed a digital herd health monitoring solution combining wearable sensors and predictive analytics, designed to support early disease detection, reproductive management, and productivity optimization across commercial dairy operations.

- April 2024: Ceva Santé Animale launched a novel parasiticide formulation for poultry health management, utilizing sustained-release delivery technology to improve bioavailability and reduce treatment cycles in intensive farming systems.

FUTURE OUTLOOK

The field of animal health is shifting towards building smart health monitoring devices to monitor health remotely. Due to the trend of the Internet of Things (IoT), technology is surging in every sector, including animal health. Private and public partnerships could make this technology affordable and animal-friendly.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The Animal Health Market report offers qualitative and quantitative insights on animal healthcare industries and a detailed analysis of market size & growth rate for all possible segments in the market.

Along with this, the report provides an elaborative analysis of the market dynamics, restraints, competitive landscape, regional analysis, and opportunities. It further offers the pipeline analysis of veterinary drugs, the regulatory scenario for key countries, key industry developments such as mergers & acquisitions, an overview of animal diseases by key countries, a snapshot of the novel & upcoming therapies, and an overview of treatment plans for different animal diseases.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product

|

|

By Animal

|

|

|

By End-user

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the market was worth USD 70.16 Bn in 2025 and is projected to reach USD 187.79 Bn by 2034.

In 2025, the market value was USD 70.16 Bn.

Growing at a CAGR of 11.56%, the market will exhibit a steady growth during the forecast period (2026-2034)

The drugs segment is the leading segment in the global market.

Increase in incidences of zoonotic diseases and growing research & development activities in are driving the growth of the market

Zoetis, Boehringer Ingelheim, and Intervet are the top players in the animal health market.

North America is expected to hold the highest market veterinary healthcare market share.

Growing animal ownership and public-private partnerships for animal health are some of the animal health market trends.

- 2021-2034

- 2025

- 2021-2024

- 145

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us