Anti-Aircraft Warfare (AAW) Market Size, Share & Industry Analysis, By Range/Engagement Tier (VSHORAD, SHORAD, MRAD, LRAD, and IAMD), By Platform (Land-based, Naval AAW, and Fixed-site/point-defense), By Component (Sensors, C2/Battle management, Fire-control & Support Equipment, Effectors (Missile-based Air Defense, Gun-based/CIWS, Directed Energy for C-UAS, and Hybrid Missile & Gun Systems)), By Target Set (Manned Aircraft, Rotary-wing, Cruise Missiles, UAS/drones, & Others), By Guidance (Command guidance, Semi-active radar homing, & Others), By End User, and Regional Forecast, 2026-2034

Anti-Aircraft Warfare Market Size and Future Outlook

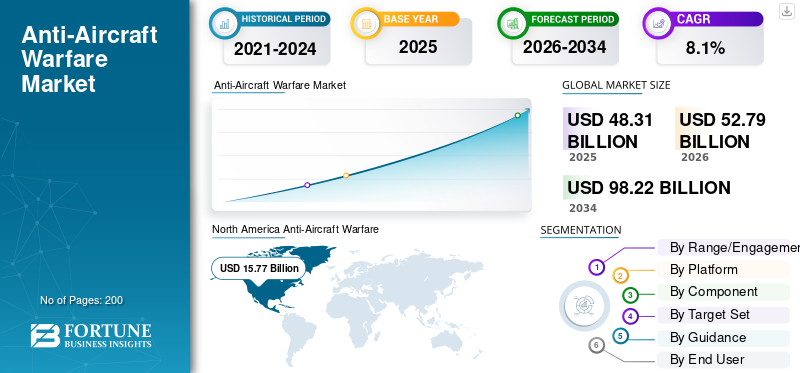

The global anti-aircraft warfare (AAW) market size was valued at USD 48.31 billion in 2025. The market is projected to grow from USD 52.79 billion in 2026 to USD 98.22 billion by 2034, exhibiting a CAGR of 8.1% during the forecast period. North America dominated the global anti-aircraft warfare (AAW) market with a market share of 32.64% in 2025.

The global AAW market consists of the technologies and services used to detect, track, command, and threats from unmanned aerial vehicles. These threats include aircraft, helicopters, cruise missiles, drones, and some types of ballistic missiles. The market uses a variety of sensors, including radars and electro-optics. It also includes command and control systems, battle management, fire control, and effectors such as missiles, guns, close-in weapon systems, and new directed-energy solutions. In simple terms, it acts as a shield that connects sensing, decision-making, and engagement across different defense systems. These include land-based, naval, and fixed-site/point-defense structures, typically within integrated air and missile defense networks.

Key players operating in the anti-aircraft warfare industry are RTX (Raytheon) (Patriot/NASAMS), Lockheed Martin (Aegis), and Europe’s MBDA/Thales (SAMP/T NG) and Rheinmetall (Skynex). They shape the market by upgrading old air defense systems into networked, layered systems. This involves better C2 integration, enhanced sensors, and stronger interceptors for point defense to handle drones and cruise missiles effectively.

Download Free sample to learn more about this report.

Anti-Aircraft Warfare Market Key Takeaways

- 2025 Market Size: USD 48.31 Billion

- 2026 Market Size: USD 52.79 Billion

- 2034 Forecast Market Size: USD 98.22 Billion

- CAGR: 8.1% from 2026–2034

- North America dominated the anti-aircraft warfare market with a 32.64% share in 2025.

- The SHORAD segment held the largest share by range/engagement tier in 2025.

- The land-based platform segment accounted for the largest market share in 2025.

North America

North America generated USD 15.77 billion in revenue and held a 32.64% market share in 2025.

Europe

Europe was the largest regional market in 2025 and is projected to grow at a CAGR of 6.3% through 2034.

Asia Pacific

Asia Pacific was the third-largest regional market in 2025 and is expected to expand at the fastest CAGR of 10.9%.

U.S.

The market was valued at approximately USD 12.59 billion in 2025 and is projected to grow at a CAGR of 6.0%.

Japan

Rising defense spending and investments in air defense systems are supporting market growth.

Read More

ANTI-AIRCRAFT WARFARE MARKET TRENDS

Shift from Demonstration to Procurement Driven by Demand for Cheaper and Faster Point-defense Solutions

A noticeable trend in air and missile defense is the increased use of laser-based and other directed-energy systems alongside missiles and guns. This change is crucial for combating drones and low-cost saturation attacks. The reasoning is simple: missiles are effective but expensive and limited in number, while lasers have a very low cost per shot and can maintain a large supply of ammunition, depending on power capacity. Consequently, militaries are witnessing directed energy as a valid component of their defenses, especially for fixed-site and naval point-defense, where managing power and cooling is easier.

- In November 2025, the U.K. government announced a USD 404.48 million contract for MBDA to provide DragonFire laser systems to the Royal Navy starting in 2027. This follows trials where the system successfully shot down high-speed drones. This clearly shows that high-energy lasers are becoming a practical option for air and missile defense.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Drone and Missile Attacks are Accelerating Demand for Layered Air Defense Systems

Modern air threats from unmanned aerial vehicles no longer arrive one at a time; they come in mixed groups of drones, cruise missiles, and aircraft, sometimes including ballistic elements. This situation forces militaries to invest in more interceptors, better radars, and smarter battle management. They need to detect threats early, prioritize targets, and engage at various ranges instead of counting on one silver bullet system. This demand explains why the need for VSHORAD and SHORAD remains strong, while MRAD, LRAD, IAMD, and C2 integration continue to take up a larger share of budgets.

- In July 2024, in the Washington Summit Declaration, NATO confirmed its commitment to deter and defend against all air and missile threats by improving Integrated Air and Missile Defense (IAMD). This shows that investing in layered air defense remains a priority for the alliance.

MARKET RESTRAINTS

Interceptor Magazine Depth and Long Lead Times are Biggest Challenges to Market Growth

Air defense is very effective, but it depends on consumables. In real operations, interceptors are used up quickly. Replacing them isn’t as simple as buying trucks. Seekers, propulsion, warheads, and guidance electronics have limited supply chains and take years to deliver. This puts buyers in a tough position. Even when budgets allow for it, you can’t always get the missiles or spare parts fast enough. The cost per intercept can be high when shooting down low-cost drones with expensive interceptors. As a result, there are delays in fielding, longer upgrade schedules, and a stronger push toward guns, airbursts, and directed energy. However, those aren't quick solutions either.

- In September 2025, the U.S. Army signed a record deal worth about USD 9.8 billion to buy nearly 2,000 PAC-3 Patriot interceptors. This shows how urgently governments are working to rebuild and expand interceptor stocks due to high global demand and limited supply.

MARKET OPPORTUNITIES

Open-architecture IAMD Battle Management Enhance Radar and Interceptor Effectiveness

AAW budgets focus not just on buying more missiles but on integration. The opportunity lies in C2 and battle-management networks that connect different sensors and effectors into a unified fighting picture, combining land, naval, and fixed-site capabilities. This enables commanders to engage more quickly, prevent conflicts during engagements, and extend the life of interceptor stocks. In practical terms, purchasing can grow in this area. Once a country invests in an integrated C2 backbone, it typically continues to acquire connectors, software upgrades, network nodes, and new sensors and effectors that work within the system. This creates a high development of the anti-aircraft warfare industry.

- In June 2024, Northrop Grumman announced the delivery of the first production IBCS Engagement Operations Center and network relay equipment to the U.S. Army. This marks a significant step in rolling out a system designed to integrate multiple sensors and weapons for air and missile defense.

MARKET CHALLENGES

Patchwork Air and Missile Defenses Leads to Interoperability Challenges

The main issue in air and missile defense isn’t just purchasing radars and missiles, it’s getting different national systems to communicate and work together. Effective air defense relies on quick coordination among sensors, command and control, and shooters. When countries have mixed fleets from various suppliers, issues with integration, doctrine, communication standards, and coordination can create delays. This slows down deployments, raises costs, and can create gaps even when the equipment is ready.

- In February 2025, NATO’s Integrated Air and Missile Defense Policy clearly stated that interoperability is essential for smooth integration and coordination among Allies’ air and missile defense systems and command and control structures. This means standardizing doctrines, procedures, communication, and coordination methods.

Impact of Russia Ukraine War

Russia-Ukraine War Drives Increased Funding for AAW and Accelerates Air Defense Procurement

Russia's invasion of Ukraine has tested air defense in real combat. It has changed the air and missile defense market in three clear ways. First, it has shifted air and missile defense from a secondary priority to a main budget focus. Ukraine's experience shows that cities, air bases, and logistics can be targeted repeatedly by mixed attacks with drones, cruise missiles, and aircraft. NATO has stressed the need to improve Integrated Air and Missile Defense. This means more funds for sensors, command and control, and layered interceptor systems, instead of just purchasing individual systems.

The war has speeded up procurement cycles and increased the demand for replenishment. Countries sending systems to Ukraine, while watching interceptor usage rates, have had to think about magazine depth and resupply. This leads to follow-up orders for interceptors and spare parts. The U.S. Congressional Research Service notes that Patriot systems and interceptors are expensive and in short supply. This situation turns demand into multi-year backlogs and raises interest in more affordable options such as guns and airburst systems, and eventually, directed energy.

Europe, including Russia in the discussion, has technologically advanced quickly toward layered air and missile defense systems. A clear example is Germany’s initiative to deploy Arrow 3 as a long-range ballistic missile defense layer. This is part of a broader European effort to improve air defense coverage after 2022. The market impact is clear, more countries are investing in higher-tier systems and the necessary connections to integrate them as Ukraine highlighted the serious costs of defense gaps.

Segmentation Analysis

By Range/Engagement Tier

Rise in Low-altitude Drones and Cruise-missile Threats Drives SHORAD Segment Growth

In terms of range/engagement tier, the market is categorized into VSHORAD, SHORAD, MRAD, LRAD, and IAMD.

SHORAD segment holds the largest share of the anti-aircraft warfare industry. SHORAD plays an essential role in air defense. It can be deployed in large numbers, moved alongside maneuver forces, and used to protect bases, logistics hubs, and front-line units from common threats from unmanned aerial vehicles, helicopters, and low-flying missiles. Medium-range air defense (MRAD) usually covers medium range 20 to 100 km. It serves as the primary layer that protects air bases, maneuver forces, and important infrastructure from aircraft, cruise missiles, and various UAV threats. It connects the SHORAD point defense and longer-range/IAMD systems.

In June 2024, a U.S. Congressional Research Service (CRS) brief stated that the U.S. Army planned to build about 312 Maneuver SHORAD (M-SHORAD) systems, with the option to increase that number. This shows how militaries are expanding SHORAD as a key air-defense layer for ground forces.

The LRAD segment in the market is expected to show fastest grow at a CAGR of 10.9% over the forecast period.

By Platform

Protect of Ground Forces and Critical Infrastructure Drives Dominance of Land-based Platform

On the basis of platform, the market is classified into land-based, naval AAW, and fixed-site/point-defense.

The land-based segment holds the largest share of the anti-aircraft warfare industry. Land-based air defense (AAW) is the preferred choice as it offers the most flexibility for covering cities, air bases, ports, and maneuver units. It can be layered from short-range air defense (SHORAD) to integrated air and missile defense (IAMD) using radars, command and control (C2), and interceptor batteries placed where the threat is highest. Naval AAW is essential but limited by the fleet. Fixed-site options are important but restricted by location. Land-based systems provide better coverage and are easier to deploy, which is crucial given the modern threats from unmanned aerial vehicles and missiles that countries must confront.

Fixed-site/point-defense is expected to show fastest anti-aircraft warfare market growth at a CAGR of 11.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Effectors lead Component Segment by Enabling Effective Neutralization of Incoming Threats, Not Just their Defection

Based on component, the market is segmented into sensors, C2/battle management, fire-control & support equipment, and effectors (missile-based air defense, gun-based/CIWS (AAA, airburst), directed energy (HEL/HPM) for C-UAS, and hybrid missile & gun systems).

The effectors segment holds the largest share of the anti-aircraft warfare industry. In AAW, sensors and C2 are ineffective without enough shoot capacity. Effectors, such as interceptors, guns, CIWS, and new directed energy systems, typically take the largest budget share. Real operations quickly show the reality, you need enough missiles, resupply, and various engagement options to handle repeated attacks and mixed salvos. This is why countries continue to place large, multi-year orders for interceptors and point-defense systems while they update radars and networks.

- In September 2025, the U.S. Army awarded Lockheed Martin a USD 9.8B contract to produce 1,970 PAC-3 MSE Patriot interceptors and related hardware. This is one of the clearest signs that spending on effector replenishment and scaling is where major money is going.

C2/battle management is the fastest growing segment in the market at a CAGR of 10.7% across the forecast period.

By Target Set

Manned Aircraft Dominate Segment Driven by Need to Defeat High-value, High-impact Air Raids

Based on target set, the market is segmented into manned aircraft, rotary-wing, cruise missiles, UAS/drones, and selected ballistic missile threats.

The manned aircraft segment holds the largest share of the anti-aircraft warfare industry. Even with drones gaining attention, manned aircraft remain a significant part of AAW spending. They can carry the heaviest payloads, work with electronic warfare support, and force defenders to invest in better radars, fire-control systems, and interceptors. In simple terms, effectively stopping manned aircraft often leads to investing in the same robust AAW setup that also protects against cruise missiles and many UAS situations. This target set continues to shape capability needs and budgets.

- In April 2023, Raytheon announced a USD 1.2 Billion contract to supply Patriot air defense systems to Switzerland. This includes GEM-T missiles, which are effective at defeating enemy aircraft, as well as cruise and tactical ballistic missiles. This contract clearly shows ongoing investment in air defense aimed at defeating manned aircraft.

The UAS/drones segment is expected to show fastest market growth at a CAGR of 12.8% across the forecast period.

By Guidance

Shift Toward Networked, Beyond-visual-range Engagements, Active Radar Homing, and Datalink Lead Segment Growth

Based on guidance, the market is segmented into command guidance, Semi-Active Radar Homing (SARH), Active Radar Homing (ARH) & datalink, IR/EO seekers (IIR, dual-mode), and others.

Active Radar Homing (ARH) & datalink segment holds the largest share of the anti-aircraft warfare industry. ARH and datalink are the best guidance methods for today’s air-defense situation. Threats are faster, lower, and often strike in groups. Defenders need missiles that can be updated in flight and then home in on targets during the final phase without relying on one illuminator the entire time. In simple terms, ARH and datalink give forces more shots per radar, better handling of multiple targets, and more flexibility for integrated air defense.

- In July 2025, the U.S. Department of Defense awarded Raytheon a contract worth up to USD 3.5 billion for AMRAAM Production Lots 39 and 40. This program's official product description highlights midcourse updates and an on-board active radar to finish the intercept, following the ARH and datalink strategy.

IR/EO seekers (IIR, dual-mode) segment is expected to show second fastest market growth at a CAGR of 8.8% across the forecast period.

By End User

Protection Needs Against Drones and Low-altitude Threats Drive Army Segment Dominance

Based on end user, the market is segmented into army, navy, air force, and joint forces.

The army segment holds the largest anti-aircraft warfare market share. In most countries, the Army usually owns most day-to-day air defense. It needs to guard brigades on the move, logistics routes, forward bases, and key locations close to the action. This need drives higher demand for deployable, layered ground-based air defense. It requires more launchers, radars, and, most importantly, many interceptors to keep a strong magazine depth during repeated attacks.

The joint forces segment is expected to show fastest market growth at a CAGR of 10.5% across the forecast period.

Anti-Aircraft Warfare Market Regional Outlook

Security Shock in 2022 and Rapid Rearmament Drive Europe Leadership in Regional Segment

By region, the market is categorized into North America, Europe, Asia Pacific, Middle East, and Rest of the World (Africa, and Latin America).

North America

North America Anti-Aircraft Warfare (AAW) Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is concentrating on air and missile defense. The region funds both advanced defenses and is technologically advanced that enables mixed fleets to work together. In 2024, the U.S. spent USD 997 billion, making it the world’s leading defense spender. This spending helps modernize and replenish integrated air and missile defense systems. A notable example is the U.S. Army's progress with IBCS, which plays a key role in modernizing air-defense command and control. This shows that the region is investing in both missiles and the supporting frameworks.

U.S. Anti-Aircraft Warfare Market

Based on North America market size, strong contribution and the U.S. dominance within the region, the U.S. market analytically approximated at around USD 12.59 billion in 2025, increasing at a CAGR of 6.0%.

Europe

Europe anti-aircraft warfare market size was estimated to be the largest in 2025, during the forecast period, the Europe region is projected to have a CAGR of 6.3%. The market value in Europe was USD 0.78 billion in 2025. Europe has had to speed up its air and missile defense upgrades more than any other area. After 2022, the defense gaps became clear. The goal is not just to buy more missiles; it's to create layered coverage from SHORAD to IAMD. This includes the radars and battle-management networks needed to handle mixed attacks. When several countries modernize at the same time and restock their supplies, Europe significantly impacts AAW budgets.

- In April 2025, SIPRI reported an unprecedented rise in global military spending for 2024. The report showed that European spending increased noticeably, reflecting the ongoing defense focus in response to the regional security situation. This environment encourages quicker AAW procurement and integration programs throughout Europe.

U.K. Anti-Aircraft Warfare Market

The U.K. AAW market value reached approximately USD 1.40 billion in 2025, equivalent to around 5.5% of Europe Anti-Aircraft Warfare (AAW) industry revenues.

Germany Anti-Aircraft Warfare Market

The Germany AAW market size valued at around USD 2.03 billion in 2025, representing roughly 9.8% of Europe AAW revenues.

Asia Pacific

Asia Pacific AAW market size is the third largest in the global market and is anticipated to be the fastest growing segment during the forecast period, growing at a CAGR of 10.9%. Demand in the Asia Pacific is rising due to growing regional tensions. There is a need to protect large areas, such as bases, ports, airfields, and maritime routes, from drones, cruise missiles, and other technologically advanced threats. SIPRI reports strong spending trends in this region, with East Asia experiencing a 7.8% increase in 2024. Japan had its largest spending increase since 1952, directly tied to a plan focusing on air defense systems, which includes significant investments for 2024.

China Anti-Aircraft Warfare Market

China’s AAW market was projected to be one of the largest in Asia Pacific, with 2025 revenues at around USD 5.07 billion, representing roughly 42.12% of Asia Pacific AAW sales.

India Anti-Aircraft Warfare Market

The India AAW market value in 2025 was around USD 1.99 million, accounting for roughly 16.52% of Asia Pacific Anti-Aircraft Warfare (AAW) revenues.

Middle East

In the Middle East, the market responds to frequent attacks and the need to protect critical infrastructure. This focus pushes procurement toward fixed-site and layered defenses, which include sensors, command and control, interceptors, and point defense systems. SIPRI notes that conflict dynamics heavily influence budgets. For example, Israel’s military spending rose 65% in 2024, driving the region toward rapid replenishment and faster upgrades of defense measures.

Saudi Arabia Anti-Aircraft Warfare Market

Saudi Arabia AAW market 2025 revenues was estimated at around USD 1.56 billion, representing roughly 29.98% of Middle East AAW sales.

Israel Anti-Aircraft Warfare Market

Israel AAW market in 2025 was estimated at around USD 1.10 million, accounting for roughly 21.20% of Middle East AAW revenues.

Rest of the World

Rest of World (Africa and Latin America), has comparatively smaller in share but is growing at a CAGR of 7.2%. In these areas, air and missile defense purchases are often selective and limited by budgets. Demand mainly focuses on practical short-range air defense and point defense systems, along with radar updates and upgrades, instead of large-scale integrated air and missile defense systems. SIPRI’s 2024 data indicates that spending increases in Africa are usually found in a few countries, such as Algeria, which saw a 12% rise in 2024, and Morocco, which also increased its spending. This illustrates a trend where spending spikes relate to specific security concerns and procurement chances, rather than ongoing major modernization efforts.

Latin America Anti-Aircraft Warfare Market

The Latin America AAW market was projected to be one of the largest in rest of the world, with 2025 value at around USD 0.99 million, accounting for roughly 54.72% of rest of the world AAW revenues.

Africa Anti-Aircraft Warfare Market

Africa anti-aircraft warfare market size was valued at around USD 0.82 billion in 2025, and is expected to reach USD 1.68 billion in 2034, representing roughly 45.28% of rest of the world anti-aircraft warfare sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Surging UAV Threats Driving MRAD (20–100 km) and AI/ML-Enabled System Integration in AAW Competitive Landscape

The AAW market is mainly run by a small group of defense contractors that can offer complete air-defense systems, not just individual missiles or radars. Buyers now look at vendors based on how well the entire system works. This includes the full cycle of surveillance, tracking, command and control, and engagement. They also consider how easily the system fits into national networks and how quickly it can boost its magazine capacity. A key focus is medium-range air defense (MRAD), which typically covers about 20 to 100 km. This range provides the best balance between coverage and cost for protecting bases, maneuver forces, and vital infrastructure. This is especially true when it operates with short-range air defense (SHORAD/VSHORAD) below and long-range air defense (LRAD/IAMD) above. On the threat side, risks from unmanned aerial vehicles (UAVs) and mixed attacks that use drones with cruise missiles are changing the competition. This pushes leading companies to offer layered responses using multiple weapons, including missiles, guns, and new directed energy, rather than just standalone solutions.

Competition focuses on software as much as on hardware. Top players are using artificial intelligence and machine learning (AI/ML) for sensor fusion, track classification, and engagement decision aids. This aims to reduce operator workload and allow quicker responses to saturation attacks, while still keeping humans involved in rules of engagement. That is why companies with strong command and control and integration abilities, such as battle management, open architectures, and secure data links, tend to do better. They can connect different inventories and update older fleets with new technology. In summary, the leading contractors are those that can provide network-ready, MRAD-focused systems with proven abilities against UAS threats, credible upgrade paths, and the ability to produce interceptors and spare parts quickly.

LIST OF KEY ANTI-AIRCRAFT WARFARE COMPANIES PROFILED

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Boeing Company (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- General Dynamics Corporation (U.S.)

- BAE Systems plc (U.K.)

- MBDA (France)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Rheinmetall AG (Germany)

- Kongsberg Gruppen ASA (Norway)

- Diehl Defense GmbH & Co. KG (Germany)

- Israel Aerospace Industries Ltd. (Israel)

- Rafael Advanced Defense Systems Ltd. (Israel)

- Elbit Systems Ltd. (Israel)

- ASELSAN A.Ş. (Türkiye)

- Roketsan A.Ş. (Türkiye)

- Hanwha Aerospace (South Korea)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Israel’s Ministry of Defense reported that the German Bundestag approved an Arrow 3 contract expansion worth about USD 3.1 billion, adding to the original purchase. This reflects Europe’s shift from simply buying to scaling up, increasing capacity as the security landscape becomes more challenging.

- December 2025: The U.S. State Department approved a potential FMS to Denmark for AMRAAM-ER missiles and related equipment, estimated at up to USD 951 million. This deal supports Denmark’s transition toward a layered, ground-based air-defense system that meets NATO interoperability needs.

- November 2025: The U.K. signed a USD 421.16 million contract with MBDA U.K. to deliver DragonFire laser systems to the Royal Navy from 2027, following successful tests against high-speed drones.

- September 2025: The U.S. State Department gave the green light for a potential FMS to Germany for AIM-120D-3 AMRAAM missiles and related equipment, estimated at USD 1.23 billion. This shows that Europe is spending actively on modern missiles to address gaps and boost readiness.

- September 2025: The U.S. Army awarded Lockheed Martin a USD 9.8 billion contract to produce 1,970 PAC-3 MSE interceptors and related hardware. This indicates that interceptor inventory has become a top procurement priority, rather than a secondary concern.

- May 2025: The U.S. State Department approved a potential Foreign Military Sale (FMS) to Saudi Arabia for AIM-120C-8 AMRAAM missiles and support, estimated at USD 3.5 billion. This package highlights how Gulf buyers are focusing on modern, network-ready interceptors to counter rapidly evolving air threats.

- July 2024: NATO’s Washington Summit Declaration stated that Allies are committed to deterring and defending against air and missile threats by improving Integrated Air and Missile Defense (IAMD). This policy direction creates a clear demand for layered systems that combine sensors, command and control, and effectors across Europe and allied partners.

- June 2024: Northrop Grumman delivered the first production set of IBCS equipment, including an Engagement Operations Center and network relay, to the U.S. Army. This is important as modern air defense success relies more on integration and battle management than just standalone launchers.

- September 2023: Germany and Israel signed the Arrow 3 agreement valued at about USD 3.5 billion, following U.S. approval due to the system’s joint development. This marked a significant step in Europe’s efforts for better air and missile defense after 2022.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.1% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By Range/Engagement Tier · VSHORAD · SHORAD · MRAD · LRAD · IAMD |

|

By Platform · Land-based · Naval AAW · Fixed-site / point-defense |

|

|

By Component · Sensors · C2/Battle management · Fire-control & support equipment · Effectors o Missile-based air defense o Gun-based / CIWS (AAA, airburst) o Directed energy (HEL/HPM) for C-UAS o Hybrid missile & gun systems |

|

|

By Target Set · Manned aircraft · Rotary-wing · Cruise missiles · UAS/drones · Selected ballistic missile threats |

|

|

By Guidance · Command guidance · Semi-active radar homing (SARH) · Active radar homing (ARH) & datalink · IR/EO seekers (IIR, dual-mode) · Others |

|

|

By End User · Army · Navy · Air force · Joint Forces |

|

By Region

o China (By Platform) o India (By Platform) o Japan (By Platform) o South Korea (By Platform) o Australia (By Platform)

o Saudi Arabia (By Platform) o Israel (By Platform) o UAE (By Platform) o Qatar (By Platform)

o Latin America (By Platform) · Africa (By Platform) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 52.79 billion in 2026 and is projected to reach USD 98.22 billion by 2034.

In 2025, the market value stood at USD 15.77 billion.

The market is expected to exhibit a CAGR of 8.1% during the forecast period.

The land-based led the market by platform.

Drone and missile attacks are pushing countries to buy layered air defense faster than they can set it up.

RTX (Raytheon), Lockheed Martin, and Northrop Grumman for integrated air and missile defense architectures and battle management, alongside European champions such as MBDA, Thales, Leonardo, and Rheinmetall for layered ground-based air defense and sensors, and Israel’s Rafael and Israel Aerospace Industries (IAI) for combat-proven interceptors and multi-layer air defense, with additional strength from Saab, Kongsberg, Diehl Defense, and ASELSAN, among others, are the top companies in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us