Anti-block Additives Market Size, Share & Industry Analysis, By Type (Inorganic, Organic, and Hybrid), By Polymer Type (Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), and Others), By Application (Packaging Films, Industrial Films, Agricultural Films, Medical Films, and Others), and Regional Forecast, 2026-2034

Anti-block Additives Market Size and Future Outlook

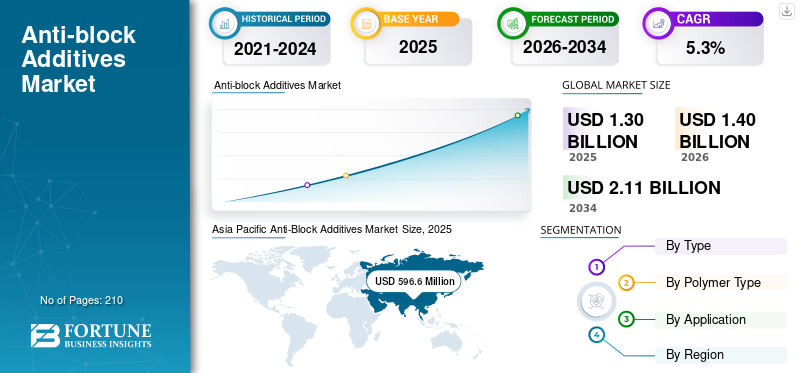

The anti-block additives market size was valued at USD 1,303.7 million in 2025. The market is projected to grow from USD 1,400.1 million in 2026 to USD 2,110.9 million by 2034, exhibiting a CAGR of 5.3% during the forecast period. Asia Pacific dominated the anti-block additives market with a market share of 45.76% in 2025.

Anti-block additives are specialty additives used in plastic films to prevent film surfaces from sticking together and to improve handling during processing, storage, and packaging. They are widely used in packaging, agricultural, industrial, and medical films, where smooth film opening, improved machinability, and good surface quality are essential. Market growth is closely linked to the growth of flexible packaging and polymer film production across industries. Globally, the market is driven by the need for improved film performance, cost-effective manufacturing, and efficient processing, while maintaining transparency, durability, and compatibility with different polymer materials.

A group of established additive manufacturers with strong polymer additive portfolios and long-term relationships with film and packaging producers dominates the market. Major players such as Ampacet Corporation, Avient Corporation, Tosaf, Sukano, and W. R. Grace & Co., as well as regional manufacturers, focus on product performance, polymer compatibility, and customized formulations, resulting in a moderately consolidated market characterized by steady demand, technical expertise, high customer retention, and continuous product development.

Download Free sample to learn more about this report.

ANTI-BLOCK ADDITIVES MARKET TRENDS

Shift Toward High-Clarity Anti-Block Additives is Reshaping Market

A key trend in the market is the growing use of high-clarity and low-haze additive solutions. Film manufacturers are focusing on additives that prevent film layers from sticking together without affecting transparency, gloss, sealing, or printing performance. This is especially important in thin, clear, and multilayer packaging films, where surface quality is a major requirement. As a result, additive producers are developing improved anti-block masterbatches with better particle control and polymer compatibility. This trend is helping film manufacturers improve product quality, reduce processing issues, and meet higher performance expectations in packaging applications.

- According to the U.S. Census Bureau, the U.S. plastics packaging film and sheet manufacturing industry had 426 employer establishments in 2023, supporting demand for advanced anti-block additives in film applications.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Flexible Packaging Films Supports Anti-Block Additives Consumption

The growing use of flexible packaging films across food packaging, consumer goods, agriculture, and industrial applications primarily drives anti-block additives market growth. Packaging manufacturers increasingly use anti-block additives to prevent film layers from sticking together and to improve film handling during processing, storage, and transportation. In addition, the rapid growth of multilayer and high-performance plastic films has increased demand for additives that enhance surface properties without compromising transparency or strength. This expanding use of flexible and specialty films continues to create strong demand for anti-block additives across the global packaging and polymer processing industries.

- According to the Flexible Packaging Association (FPA), the U.S. flexible packaging industry generated around USD 42.6 billion in sales in 2024, supporting strong demand for plastic films and anti-block additives used in film processing and packaging applications.

MARKET RESTRAINTS

Environmental Concerns Related to Plastic Waste Limits Market Expansion

The market faces challenges due to rising environmental concerns about plastic waste and growing pressure to reduce single-use plastics. Governments across several countries are introducing stricter regulations on plastic packaging, recycling requirements, and the use of sustainable materials, which can affect demand for conventional plastic films that rely on anti-block additives. In addition, the shift toward biodegradable materials, paper-based packaging, and reusable alternatives may reduce long-term consumption of traditional polymer additives. These changing sustainability trends create uncertainty for manufacturers operating in the conventional plastic film value chain.

MARKET OPPORTUNITIES

Growing Demand for Recyclable Packaging Films Creates New Growth Opportunities

The market is expected to benefit from the rising use of recyclable and sustainable packaging films across food, consumer goods, and industrial applications. Packaging companies focusing using recyclable polyethylene and polypropylene films that require effective anti-block additives for smooth processing and easy film separation. In addition, the shift toward mono-material packaging structures is increasing the need for additive solutions that maintain film quality, clarity, and performance without affecting recyclability. This trend is creating new opportunities for manufacturers developing advanced and environmentally compatible anti-block additive products.

- According to the U.S. EPA, plastic containers and packaging accounted for more than 14.5 million tons of plastic waste generation in the U.S., highlighting the growing focus on recyclable packaging materials and sustainable film solutions that support demand for advanced anti-block additives.

MARKET CHALLENGES

Raw Material Cost Volatility Pressures Producer Margins and Challenges Market Expansion

Anti-block additive producers face a key challenge from changing raw material and carrier resin costs, which can affect pricing stability and profit margins. Important inputs such as silica, talc, calcium carbonate, waxes, and polymer carriers are influenced by energy prices, mining costs, logistics, and resin market conditions. When film and packaging producers are under cost pressure, additive suppliers may find it difficult to pass on higher input costs. This creates margin pressure and increases the need for reliable sourcing, efficient production, and cost-effective formulations.

Segmentation Analysis

By Type

Inorganic Additives Dominate Due to Cost Efficiency and Strong Film Performance

Based on type, the market is segmented into inorganic, organic, and hybrid.

To know how our report can help streamline your business, Speak to Analyst

The inorganic segment accounted for largest anti-block additives market share in 2025. Inorganic anti-block additives such as silica, talc, and calcium carbonate are widely used in plastic films as they provide effective film separation, good processing performance, and cost efficiency. These additives are especially preferred in polyethylene and polypropylene films used for packaging, agricultural films, and industrial applications. Their strong availability, stable performance, and suitability for large-scale film production make them the leading choice for manufacturers. As demand for flexible and multilayer films continues to grow, inorganic additives remain the most widely adopted type in the market.

The organic segment is expected to grow at a 6.0% CAGR over the forecast period.

By Polymer Type

Increasing Demand for Polyethylene Films Drive Dominance of PE in the Market

Based on polymer type, the market is segmented into Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), and others.

To know how our report can help streamline your business, Speak to Analyst

The Polyethylene (PE) segment accounted for a largest share of the market in 2025. PE leads consumption as it is widely used in flexible packaging films, agricultural films, industrial films, and consumer packaging applications where smooth film opening and easy handling are important. Anti-block additives are commonly used in PE films to prevent layers from sticking during processing, winding, storage, and end-use handling. As PE remains one of the most preferred materials for film production due to its flexibility, cost efficiency, and processability, it continues to be the most structurally important polymer type for anti-block additive demand.

The Polyethylene Terephthalate (PET) segment is expected to grow at a 6.4% CAGR over the forecast period.

By Application

Flexible Packaging Demand Positions Packaging Films as Dominant Segment

Based on application, the market is segmented into packaging films, industrial films, agricultural films, medical films, and others.

The packaging films segment accounted for the largest share in 2025. Packaging films leads as these additives are essential for smooth film separation, easy handling, and efficient processing during film production, winding, storage, and packaging. Food packaging, consumer goods packaging, and flexible retail packaging require films with good surface quality, clarity, printability, and sealing performance. As flexible packaging continues to be widely used across daily-use products, packaging films remain the strongest and most consistent application base for anti-block additive demand.

The medical films segment is expected to grow at a 6.6% CAGR over the forecast period.

Anti-block Additives Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Anti-Block Additives Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in 2025, valued at USD 596.6 million, and is expected to retain its leading role in 2026, reaching USD 647.2 million. The region’s leadership is driven by its large-scale plastic film manufacturing base, strong packaging production, and high demand from food, consumer goods, agriculture, and industrial applications. Robust consumption of polyethylene and polypropylene films across China, India, Japan, South Korea, and Southeast Asia supports sustained demand for anti-block additives, particularly in cost-sensitive and high-volume flexible packaging applications.

China Anti-Block Additives Market

Based on Asia Pacific’s strong contribution, the China market reached USD 271.0 million in 2025, accounting for approximately 45.4% of regional revenues. Demand is supported by high-volume polyethylene and polypropylene film production for packaging, agricultural, industrial, and consumer goods applications, as well as by a well-established polymer processing and flexible packaging industry across major clusters.

India Anti-Block Additives Market

The Indian market in 2025 was at USD 96.9 million. Growth is supported by expanding flexible packaging production, rising demand for packaging food and consumer goods, wider use of agricultural films, and domestic polymer processing capacity serving packaging and industrial applications.

North America

North America remains a significant regional market and reached USD 278.2 million in 2025. Mature flexible packaging, food packaging, medical films, agricultural films, and industrial film applications support demand. The region benefits from established polymer processing infrastructure, strong packaging standards, and steady use of high-performance films. Growth remains moderate, reflecting market maturity, stable replacement demand, and ongoing preference for efficient film handling and processing solutions across applications.

U.S. Anti-Block Additives Market

The U.S. market in 2025 was at USD 238.9 million, representing approximately 85.9% of global revenues. Consumption is driven by flexible packaging films, food packaging, medical films, agricultural films, and industrial films that require smooth separation, easy processing, good surface quality, and reliable performance during production, storage, and end-use handling.

Europe

Europe is projected to record modest growth over the forecast period and reached a valuation of USD 243.5 million in 2025. Strict plastic packaging rules, sustainability targets, and rising demand for recyclable film structures shape the region. Despite these pressures, food packaging, medical films, industrial films, and high-performance flexible packaging continue to support steady consumption of anti-block additives across mature and specialized European application markets.

Germany Anti-Block Additives Market

Germany’s market reached USD 75.1 million in 2025, equivalent to around 30.8% of the regional market. Demand is supported by packaging production, advanced polymer processing, food and medical film applications, and industrial film use.

U.K. Anti-Block Additives Market

The U.K. market in 2025 was at USD 35.9 million, accounting for roughly 14.7% of regional revenues. Consumption is concentrated in flexible packaging films, food packaging, medical films, and selected industrial film applications requiring smooth processing, easy handling, and reliable surface performance.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth during the forecast period. The Latin America market was at USD 106.5 million in 2025, driven by rising demand for flexible packaging, expanding food packaging production, and the growing use of plastic films in agricultural and industrial applications. In the Middle East & Africa, demand is driven by packaging films, agricultural films, consumer goods packaging, and the gradual development of downstream polymer processing capacity. The region also benefits from urbanization and the growth of packaged food consumption across key economies. The market reached USD 78.8 million in 2025.

GCC Anti-Block Additives Market

The GCC market accounted for USD 44.0 million in 2025, representing approximately 55.8% of regional revenues. Demand is supported by flexible packaging, food and consumer goods films, agricultural film use, and the region’s petrochemical base supporting film production.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Strategic Asset Management Shape Competition in Market

The market is moderately consolidated and formulation-driven, as product performance requirements, polymer compatibility, customer qualification processes, and consistent supply standards create significant barriers to entry. These factors limit new participation and concentrate demand among established specialty additive producers and masterbatch suppliers with technical expertise and strong customer relationships.

Leading players such as Ampacet Corporation, Avient Corporation, Tosaf, Sukano, and W. R. Grace & Co., focus primarily on improving additive performance, film clarity, processing efficiency, and polymer compatibility rather than pursuing aggressive capacity expansion. Recent activities across these companies highlight a strategic emphasis on customized formulations, sustainable packaging support, cost competitiveness, and high-performance solutions for flexible film applications.

LIST OF KEY ANTI-BLOCK ADDITIVES COMPANIES PROFILED

- Ampacet Corporation (U.S.)

- Avient Corporation (U.S.)

- Evonik Industries AG (Germany)

- Imerys (France)

- Tosaf (Israel)

- Ingenia (Canada)

- PMC Group, Inc. (U.S.)

- Sukano (Switzerland)

- Kafrit Industries (Israel)

- R. Grace & Co. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2022: Sukano signed a conditional offtake agreement with Avantium to develop masterbatches for PEF resins, supporting specialty additive solutions for sustainable packaging

REPORT COVERAGE

The global anti-block additives market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.3% from 2026-2034 |

| Unit | Value (USD Million) Volume (Kiloton) |

| Segmentation | By Type, Polymer Type, Application, and Region |

| By Type |

|

| By Polymer Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1,303.7 million in 2025 and is projected to reach USD 2,110.9 million by 2034.

Recording a CAGR of 5.3%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The packaging films application segment led the market.

Asia Pacific held the highest market share.

Increasing use of plastic films in packaging, agriculture, medical, and industrial applications is driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us