Antibody Drug Conjugates Market Size, Share & Industry Analysis, By Product/Target Family (HER2-directed ADCs, Nectin-4-directed ADCs, TROP2-directed ADCs, CD30-directed ADCs, and Others), By Payload Class (Topoisomerase I Inhibitor ADCs, Microtubule Inhibitor ADCs, and Others), By Disease Indication (Breast Cancer, Urothelial Cancer, Lymphoma, Lung Cancer, Ovarian Cancer, and Others), By Route of Administration (Intravenous and Others), By End User (Hospitals, Cancer Specialty Centers, Academic & Research Hospitals, Ambulatory Infusion Centers, and Others), and Regional Forecast, 2026-2034

Antibody Drug Conjugates Market Size and Future Outlook

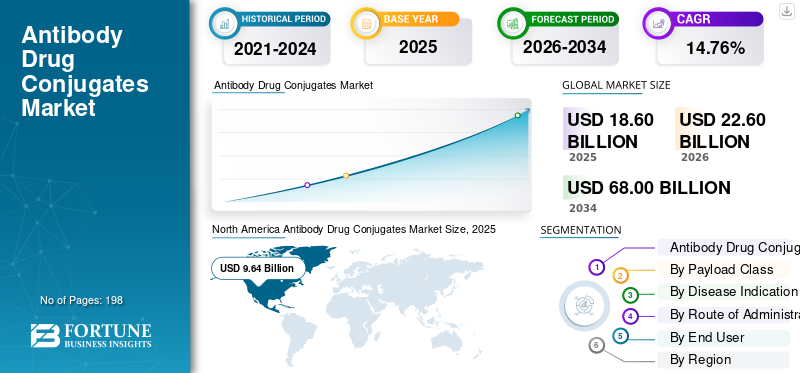

The global antibody drug conjugates market size was valued at USD 18.60 billion in 2025. The market is projected to grow from USD 22.60 billion in 2026 to USD 68.00 billion by 2034, exhibiting a CAGR of 14.76% during the forecast period. North America dominated the global market with a market share of 51.83% in 2025.

Antibody Drug Conjugates (ADCs) represent targeted cancer treatments that merge the specificity of monoclonal antibodies with the lethal efficacy of highly potent cytotoxic agents. The market is expanding as cancer treatments increasingly shift toward more precise, individualized therapies that enhance treatment efficacy while minimizing unnecessary harm to healthy tissues. Growing approvals in solid tumors and blood cancers, broader application of ADCs in earlier treatment lines, and robust clinical advancement efforts by leading pharmaceutical firms are facilitating greater adoption. The global product demand is also increasing as ADC platforms advance, with enhanced linker stability, more efficient payload types such as topoisomerase I inhibitors and microtubule inhibitors, and a wider range of tumor targets.

Key players operating in the global market include Daiichi Sankyo Company, Limited, AstraZeneca, Pfizer Inc., Astellas Pharma Inc., Gilead Sciences, Inc., and F. Hoffmann-La Roche Ltd. Their strategies include new product launches, regulatory approvals, co-development partnerships, acquisitions, and investment in next-generation ADC platforms to strengthen their presence in high-growth cancer treatment areas.

Download Free sample to learn more about this report.

Antibody Drug Conjugates Market Key Takeaways

- 2025 Market Size: USD 18.60 Billion

- 2026 Market Size: USD 22.60 Billion

- 2034 Forecast Market Size: USD 68.00 Billion

- CAGR: 14.76% from 2026–2034

- North America dominated the antibody drug conjugates market with a 51.83% share in 2025.

- HER2-directed ADCs accounted for the largest product/target family segment in 2025.

- Microtubule inhibitor ADCs are projected to hold 36.3% of the market in 2026.

North America

North America led the market with a value of USD 9.64 billion in 2025.

Asia Pacific

Asia Pacific is expected to reach USD 4.74 billion by 2026, driven by expanding oncology care access.

Europe

Europe is projected to grow at a CAGR of 13.95% during the forecast period.

U.S.

The market is projected to reach USD 10.66 billion in 2026, accounting for 47.2% of global revenue.

Japan

The market is estimated at USD 1.54 billion in 2026, representing 6.8% of global revenue.

Read More

ANTIBODY DRUG CONJUGATES MARKET TRENDS

Focus on Development of Next-Generation Antibody Drug Conjugates is a Significant Trend Observed in Market

The advancement of next-generation antibody-drug conjugates is a significant trend in the global ADC market, as firms aim to enhance the safety, efficacy, and tumor targeting of current ADCs. Previous ADCs demonstrated significant clinical benefits, but issues such as off-target toxicity, unstable linkers, limited payload delivery, and resistance in certain patients underscored the need for improved ADC designs. Consequently, organizations are developing ADCs with more robust linkers, site-specific conjugation, higher drug-to-antibody ratios, innovative payloads, dual-payload structures, and enhanced tumor-targeting mechanisms. This movement is aiding the expansion of ADC applications beyond conventional targets such as HER2 and CD30 to emerging solid tumor targets, including TROP2, CLDN6/9, CDH17, VEGF, and various tumor-associated antigens. It is also enabling companies to place ADCs earlier in the treatment line and in challenging cancers where standard chemotherapy offers little advantage. Consequently, the advancement of next-generation ADCs is anticipated to bolster the market's long-term growth by improving treatment outcomes, expanding cancer coverage, and creating new business opportunities for both major pharmaceutical and biotech firms. These factors are supporting the overall global antibody drug conjugates market growth.

- For instance, in March 2025, MediLink Therapeutics announced that it would present preclinical data for two innovative ADC programs, YL217 and YL242, along with its next-generation dual-payload ADC platform at the AACR Annual Meeting 2025.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Adoption of Targeted Cancer Therapies is Driving Market Growth

The increasing adoption of targeted cancer therapies is a major driver of the global market, as cancer treatment is moving away from broad chemotherapy toward medicines that target specific tumor markers. ADCs fit this shift well, as they combine an antibody that recognizes a cancer target with a potent payload that kills cancer cells more selectively. This helps oncologists use a more personalized treatment approach based on biomarkers such as HER2, TROP2, Nectin-4, CD30, and folate receptor alpha. As biomarker testing becomes more common in oncology, more patients can be matched with ADC therapies that are suitable for their tumor profile. This is increasing ADC use across breast cancer, urothelial cancer, lung cancer, lymphoma, ovarian cancer, and gastric cancer. The rising number of approvals and label expansions also shows that ADCs are moving into broader patient groups and earlier treatment settings. Therefore, growing demand for targeted cancer care is directly supporting higher adoption of ADC drugs and strengthening market growth.

- For instance, in June 2025, Daiichi Sankyo and AstraZeneca’s DATROWAY was approved in the U.S. as the first TROP2-directed therapy for adults with locally advanced or metastatic EGFR-mutated non-small cell lung cancer who had received prior EGFR-directed therapy and platinum-based chemotherapy.

MARKET RESTRAINTS

High Research and Development Costs to Limit Market Growth

Elevated research and development expenses pose a limitation for the global market, as ADC development is more complex than that of many standard cancer medications. Businesses must enhance the antibody, linker, payload, drug-to-antibody ratio, stability, toxicity profile, and production process before an ADC advances effectively through clinical trials. This boosts expenditures in discovery, preclinical research, clinical development, analytical testing, and specialized production. The risk remains considerable as numerous ADC candidates might fail due to safety concerns, limited effectiveness, or challenges in demonstrating distinct advantages over current treatments. Consequently, smaller ADC developers might have to cut back on research efforts, postpone programs, find partners, or focus solely on the most promising assets. This may hinder pipeline growth and slow the pace at which new ADCs enter the market. Consequently, while ADCs present significant commercial opportunities, substantial R&D expenses and developmental risks may limit market expansion.

- For instance, in May 2025, Mersana Therapeutics announced a strategic restructuring and reprioritization plan to extend its cash runway and focus resources on its B7-H4-directed ADC emiltatug ledadotin (Emi-Le/XMT-1660). The company said it would reduce its workforce by about 55%, reduce research activities, and eliminate internal pipeline development efforts, showing how high development cost pressure can force ADC-focused companies to narrow their R&D programs.

MARKET OPPORTUNITIES

Rising Investments in Oncology Drug Development to Offer Market Growth Opportunities

Increasing funding in oncology drug development is generating a significant opportunity for the global market, with ADCs now regarded as one of the most appealing sectors in targeted cancer therapy. Major pharmaceutical corporations and biotechnology companies are boosting investments in ADC development due to the potential of these treatments to target high-priority cancers such as breast cancer, lung cancer, ovarian cancer, gastric cancer, and urothelial cancer. This funding is assisting firms in creating new targets, enhanced payloads, advanced linker technologies, and superior manufacturing capabilities. It is additionally fostering increased licensing agreements, acquisitions, and strategic alliances between global pharmaceutical companies and biotech firms centered on ADCs. With increased investment in ADC research, companies can expedite the progression of candidates into clinical trials and examine them across a broader range of tumor types and treatment lines. This presents a significant business prospect as effective ADCs can achieve high pricing, extensive oncology application, and extended lifecycle growth via additional indications.

- For instance, in October 2025, Tubulis announced that it raised USD 360 million in Series C financing to accelerate the clinical development of its lead ADC candidate, TUB-040, and expand its ADC pipeline.

MARKET CHALLENGES

Limited Availability of Specialized Production Facilities Poses a Prominent Challenge to Market Growth

The limited availability of specialized production facilities poses a significant challenge for the global market, as ADC manufacturing requires highly specialized skills that are absent in conventional biologics or chemotherapy plants. Producing ADCs necessitates specialized knowledge in monoclonal antibody production, managing highly potent payloads, linker chemistry, bioconjugation, aseptic filling, containment, and analytical testing. Due to the high potency of cytotoxic payloads, facilities must adhere to stringent safety and containment regulations, leading to increased capital investment and limiting the number of qualified manufacturers. This may cause bottlenecks as additional ADC candidates transition from clinical trials to commercial production. Smaller biotech firms may face extended timelines or higher outsourcing costs due to their reliance on a limited number of ADC-centric CDMOs. With increasing demand, businesses are enhancing capacity, yet constructing and qualifying new facilities requires years. Consequently, the lack of dedicated ADC manufacturing facilities may hinder commercialization and pose a market obstacle.

Segmentation Analysis

By Product/Target Family

Strong Commercial Adoption of HER2-directed ADCs Boosted Segment Dominance

In terms of product/target family, the market is divided into HER2-directed ADCs, Nectin-4-directed ADCs, TROP2-directed ADCs, CD30-directed ADCs, CD79b-directed ADCs, Folate Receptor Alpha-directed ADCs, and others.

The HER2-directed ADCs segment led the global antibody drug conjugates market share in 2025. This is attributed to the significant commercial success and broader clinical application of products such as Enhertu and Kadcyla in HER2-positive and HER2-low cancers. The segment's dominance is due to the significant disease burden of breast cancer, gastric cancer, and other solid tumors that express HER2, resulting in a sizable pool of patients eligible for HER2-targeted therapy. Moreover, HER2-targeted ADCs have seen wider acceptance due to their demonstrated effectiveness in patients with few prior targeted therapies, particularly in metastatic disease scenarios. The ongoing growth of HER2 testing, rising label approvals, and the shift of these medications to earlier treatment stages are expected to drive the segment’s growth over the projected timeframe.

- For instance, in January 2025, Daiichi Sankyo and AstraZeneca’s Enhertu was approved in the U.S. for adults with unresectable or metastatic HR-positive, HER2-low or HER2-ultralow breast cancer after progression on one or more endocrine therapies.

The folate receptor alpha-directed ADCs segment is anticipated to rise with a CAGR of 27.09% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Payload Class

Established Clinical Use of Microtubule Inhibitor ADCs Supported Segment Dominance

Based on payload class, the market is classified into topoisomerase I inhibitor ADCs, microtubule inhibitor ADCs, maytansinoid ADCs, DNA-damaging ADCs, and others.

The microtubule inhibitor ADCs segment captured the leading position in the global market in 2025. This is owing to the early approval and strong commercial use of ADCs carrying auristatin- and maytansinoid-based payloads. The segment's dominance stems from the widespread use of products such as Adcetris, Padcev, Kadcyla, Polivy, and Tivdak in lymphoma, urothelial cancer, breast cancer, cervical cancer, and other oncology indications. These payloads are commonly used because they inhibit cancer cell division once introduced into tumor cells, making them effective against rapidly growing cancers. Additionally, the sector has gained from recognized physician knowledge, broader practical application, and several approved products for both solid tumors and hematologic cancers. The ongoing application of microtubule inhibitor ADCs in combination therapies is anticipated to promote consistent uptake of these medications in the marketplace. Furthermore, the segment is set to hold 36.3% share in 2026.

- For instance, in December 2023, the U.S. FDA approved Astellas and Pfizer’s Padcev in combination with Keytruda for adults with locally advanced or metastatic urothelial cancer. Padcev is a Nectin-4-directed ADC that uses the microtubule-disrupting payload monomethyl auristatin E (MMAE), supporting the strong clinical position of microtubule inhibitor ADCs in major cancer indications.

The topoisomerase I inhibitor ADCs segment is anticipated to rise with a CAGR of 21.70% over the forecast period.

By Disease Indication

Large Patient Pool and Wider ADC Use in Breast Cancer Led to Segment Dominance

Based on disease indication, the market is classified into breast cancer, urothelial cancer, lymphoma, lung cancer, ovarian cancer, gastric & gastroesophageal cancer, and others.

The breast cancer segment dominated the market share in 2025. This is due to the high number of patients eligible for ADC-based treatment and the strong use of approved ADCs in metastatic settings. Additionally, factors such as the broad adoption of ADCs, growing use of biomarker testing, rising preference for targeted therapies, and ongoing label expansions are supporting higher ADC adoption in breast cancer. Furthermore, the segment is set to hold 39.0% share in 2026.

- For instance, in January 2025, the U.S. FDA approved Datroway for adults with unresectable or metastatic HR-positive, HER2-negative breast cancer who had received prior endocrine-based therapy and chemotherapy.

The ovarian cancer segment is anticipated to rise with a CAGR of 28.76% over the forecast period.

By Route of Administration

Hospital-based Infusion Use Fostered Intravenous Segment Dominance

On the basis of route of administration, the market is divided into intravenous and others.

In 2025, the market share was primarily led by the intravenous segment. This is owing to the fact that almost all approved antibody drug conjugates are given through IV infusion under medical supervision. The segment's dominance is linked to the intricate characteristics of ADCs, which integrate monoclonal antibodies with potent payloads and require careful dosing, dilution, infusion monitoring, and management of potential infusion-related reactions. IV administration enables oncologists to closely observe patients for toxicities such as neutropenia, neuropathy, ocular events, and liver-related side effects. Furthermore, the segment is set to hold 99.7% share in 2026.

- For instance, in April 2024, the U.S. FDA granted full approval to Pfizer and Genmab’s Tivdak for the treatment of recurrent or metastatic cervical cancer, and the product is administered as an intravenous infusion.

The others segment is anticipated to rise with a CAGR of 26.19% over the forecast period.

By End User

Hospitals Led Market due to Availability of Advanced Oncology Care Infrastructure

Based on end user, the market is segmented into hospitals, cancer specialty centers, academic & research hospitals, ambulatory infusion centers, and others.

The hospitals segment dominated the market share in 2025. The segment's dominance stems from the fact that most ADCs are administered via intravenous infusion, which requires skilled oncology teams, infusion centers, dosage monitoring, and management of potential side effects. In addition, hospitals typically have resources for diagnostic testing, oncology experts, pharmacy preparation units, and emergency care, positioning them as the preferred locations for complex cancer treatments. Numerous patients undergoing ADCs additionally require routine imaging, blood analyses, and toxicity assessments, typically handled by hospital oncology departments. Furthermore, the segment is set to hold 51.9% share in 2026.

- For instance, in February 2023, NICE recommended AstraZeneca and Daiichi Sankyo’s Enhertu for use through a managed access agreement for adults with HER2-positive unresectable or metastatic breast cancer after one or more anti-HER2 treatments.

In addition, ambulatory infusion centers are projected to grow at a 19.07% CAGR during the forecast period.

Antibody Drug Conjugates Market Regional Outlook

By geography, the market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Antibody Drug Conjugates Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest share of the global market, attaining USD 7.65 billion in 2024. In 2025, the region continued its dominance, with USD 9.64 billion. North America is expanding due to strong adoption of advanced oncology therapies, high cancer treatment spending, and early availability of approved ADCs.

U.S. Antibody Drug Conjugates Market

The U.S. market led the North American region and is projected to be approximately USD 10.66 billion in 2026, representing about 47.2% of the global market.

Europe

The market in Europe is set to grow at a CAGR of 13.95% during the forecast period. Europe is growing steadily due to rising adoption of targeted cancer therapies, strong reimbursement systems in major countries, and increasing use of ADCs in breast cancer, lymphoma, and urothelial cancer.

U.K. Antibody Drug Conjugates Market

The U.K. market in 2026 is estimated at around USD 0.69 billion, representing roughly 3.0% of global revenues.

Germany Antibody Drug Conjugates Market

The German market size is projected to reach approximately USD 1.11 billion in 2026, equivalent to around 4.9% of global sales.

Asia Pacific

The Asia Pacific market size is expected to reach a valuation of USD 4.74 billion by 2026. Asia Pacific is expected to grow owing to the factors such as show strong growth due to a large cancer patient pool, improving access to oncology care, and rising healthcare spending in China, Japan, South Korea, Australia, and India.

Japan Antibody Drug Conjugates Market

The market in Japan in 2026 is estimated at around USD 1.54 billion, accounting for roughly 6.8% of global revenues.

China Antibody Drug Conjugates Market

The market in China is projected to reach USD 1.54 billion in 2026, representing roughly 6.8% of global sales.

India Antibody Drug Conjugates Market

The Indian market in 2026 is estimated at around USD 0.25 billion, accounting for roughly 1.1% of global revenues.

Latin America and Middle East & Africa

The growth in the Latin America and Middle East & Africa regions is anticipated to be slower over the forecast period. The growth of the market is driven by rising cancer burden, growing private healthcare coverage, and increasing use of specialty cancer medicines are supporting ADC demand. The Latin America market in 2026 is estimated at around USD 0.87 billion.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.21 billion in 2026, representing about 0.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong ADC Product Portfolio and Strategic Collaborations to Contribute to Players’ Market Dominance

The global antibody drug conjugates market features a semi-consolidated competitive landscape, with leading pharmaceutical companies such as Daiichi Sankyo Company, Limited, AstraZeneca plc, Pfizer Inc., Gilead Sciences, Inc., and F. Hoffmann-La Roche Ltd dominating the market. These players are focusing on regulatory label expansions, co-development agreements, acquisitions, and the development of next-generation ADC pipelines to strengthen their market positions across breast cancer, urothelial cancer, lymphoma, ovarian cancer, and other solid tumors.

- For instance, in October 2025, GSK acquired exclusive global rights to an antibody-drug conjugate program from Syndivia, strengthening its oncology pipeline with next-generation ADC technology to improve treatment options for cancer patients.

Other significant participants include AbbVie Inc., GSK plc, RemeGen, Astellas Pharma Inc., and Jiangsu Hengrui Pharmaceuticals Co., Ltd., among others. These companies are focusing on ADC product launches, regional commercialization, clinical trial expansion, and strategic partnerships to capture growth opportunities in the global market.

LIST OF KEY ANTIBODY DRUG CONJUGATE COMPANIES PROFILED

- DAIICHI SANKYO COMPANY, LIMITED (Japan)

- AstraZeneca (U.K.)

- Pfizer Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- AbbVie Inc. (U.S.)

- GSK plc (U.K.)

- RemeGen (China)

- Astellas Pharma Inc. (Japan)

- Jiangsu Hengrui Pharmaceuticals Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Gilead announced an agreement to acquire Tubulis, adding its next-generation ADC platform and lead candidate TUB-040, a NaPi2b-targeting ADC for ovarian cancer and other solid tumors.

- April 2026: Eli Lilly agreed to acquire CrossBridge Bio, a preclinical ADC company focused on dual-payload antibody-drug conjugates, strengthening Lilly’s next-generation oncology pipeline.

- October 2025: Boehringer Ingelheim and AimedBio entered a global collaboration and licensing agreement to develop a novel ADC therapy targeting a tumor-selective marker across multiple cancers.

- April 2025: Pfizer announced that it would present new data at ASCO 2025, including studies evaluating vedotin ADCs in combination with immune checkpoint inhibitors across oncology settings.

- May 2024: AstraZeneca announced plans to build a USD 1.5 billion ADC manufacturing facility in Singapore, its first end-to-end commercial-scale ADC production site.

REPORT COVERAGE

The global antibody drug conjugates market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides an understanding of essential factors, including technological progress, product innovations, pipeline analysis, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.76% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product/Target Family, Payload Class, Disease Indication, Route of Administration, End User, and Region |

| By Product/Target Family |

|

| By Payload Class |

|

| By Disease Indication |

|

| By Route of Administration |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 18.60 billion in 2025 and is projected to reach USD 68.00 billion by 2034.

In 2025, the market value in North America stood at USD 9.64 billion.

The market is expected to exhibit a CAGR of 14.76% during the forecast period of 2026-2034.

By product/target family, the HER2-directed ADCs segment is expected to lead the market.

Increasing approvals across solid tumors and hematologic cancers, expanding use of ADCs in earlier lines of therapy, and strong clinical development activity by major pharmaceutical companies are primarily driving market expansion.

DAIICHI SANKYO COMPANY, LIMITED, AstraZeneca, Pfizer Inc., Gilead Sciences, Inc., and F. Hoffmann-La Roche Ltd are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us