AI in Genomics Market Size, Share & Industry Analysis, By Component (Software and Services), By Technology (Machine Learning, Natural Language Processing, and Others), By Application (Clinical Diagnostics, Drug Discovery & Development, Population Genomics, Precision Medicine, and Others), By Deployment (Cloud-based, On-Premise, and Hybrid), By End User (Pharmaceutical & Biotechnology Companies, Academic & Research Institutes, Clinical Labs & Diagnostic Centers, and Others), and Regional Forecast, 2026-2034

Artificial Intelligence in Genomics Market Size and Future Outlook

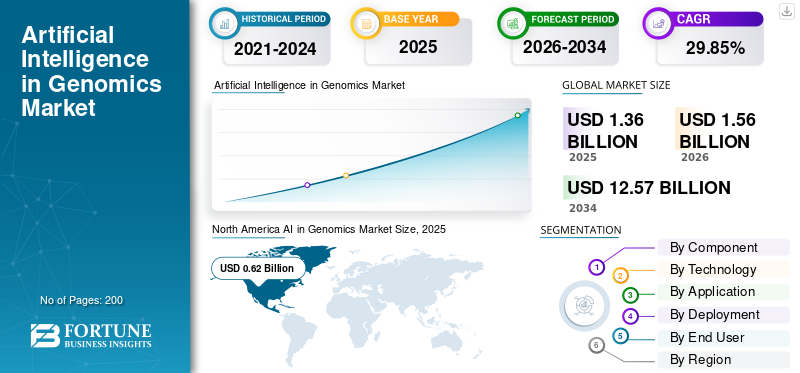

The global AI in genomics market size was valued at USD 1.36 billion in 2025. The market is projected to grow from USD 1.56 billion in 2026 to USD 12.57 billion by 2034, exhibiting a CAGR of 29.85% during the forecast period. North America dominated the AI in genomics market with a market share of 45.59% in 2025.

AI in genomics involves applying machine learning techniques along with other AI approaches to interpret DNA/RNA data and generate useful insights such as detecting disease-related variants, forecasting treatment outcomes, or discovering new drug targets. This market is experiencing rapid growth, driven by factors such as swift expansion of sequencing and multi-omics data volumes, increasing adoption of digital infrastructure, greater integration of AI, among others.

The market includes major players such as QIAGEN, NVIDIA Corporation, Illumina, Inc., and SOPHiA GENETICS. A strong focus on technological advancements in their product portfolios remains the key strategy for these companies.

Download Free sample to learn more about this report.

AI in Genomics Market Key Takeaways

- 2025 Market Size: USD 1.36 Billion

- 2026 Market Size: USD 1.56 Billion

- 2034 Forecast Market Size: USD 12.57 Billion

- CAGR: 29.85% from 2026–2034

- North America dominated the AI in genomics market with a 45.59% share in 2025.

- The cloud-based segment is projected to hold a 46.1% share in 2026.

- The drug discovery & development segment is expected to register strong growth during the forecast period.

Asia Pacific

Asia Pacific is projected to reach USD 0.31 billion in 2026.

North America

North America generated USD 0.62 billion in 2025.

Europe

Europe is projected to witness robust growth at a 29.58% CAGR during the forecast period.

U.S.

The AI in genomics market is projected to reach USD 0.64 billion in 2026.

Japan

The AI in genomics market is projected to reach USD 0.07 billion in 2026.

Read More

AI in GENOMICS MARKET TRENDS

Shift toward Cloud and Hybrid Deployment Emerged as a Prominent Market Trend

Cloud and hybrid implementations are emerging as a distinct trend in AI within Genomics, as laboratories and pharmaceutical teams face increasing pressure to quickly analyze expanding multi-omics datasets without perpetually enlarging local infrastructure. Cloud platforms enable users to adjust compute and storage resources as needed for intensive tasks, enhancing turnaround speed and reducing initial capital expenditures. Concurrently, numerous healthcare and regulated sectors demand strict data governance, leading to an increase in hybrid configurations, maintaining sensitive data or specific processes on-premises while utilizing the cloud for burst compute, collaboration, and updates. This deployment change also boosts vendor adoption since SaaS delivery streamlines upgrades, unifies pipelines across locations, and facilitates faster onboarding of new users. Gradually, purchasers are placing greater emphasis on flexible deployment (cloud-first or hybrid) as a purchasing criterion, which further boosts recurring platform revenues and implementation services. Such factors noted above are witnessed to support the overall global AI in genomics market growth.

- For instance, in March 2025, DNAnexus and Alida Biosciences (AlidaBio) announced that EpiPlex customers gain cloud access to the EpiScout analysis software on DNAnexus’ secure, scalable precision health data cloud platform.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Growth in Sequencing and Multi-Omics Data Volumes is Propelling Market Growth

The swift increase in the volume of sequencing and multi-omics data significantly propels the use of AI in Genomics, as laboratories and researchers now produce considerably more DNA/RNA/epigenetic datasets per project than in the past, making manual analysis insufficient. With increasing volumes, purchasers require AI to streamline secondary analysis (QC, alignment, variant calling), amalgamate multi-omics layers, and expedite finding prioritization with reliable accuracy. This directly boosts the demand for scalable analytics software, cloud/hybrid workflows, and services capable of operationalizing pipelines across various locations. Increased data throughput is driving pharmaceutical and population genomics initiatives to embrace AI-driven cohort analytics, enabling them to gain actionable insights without the need for extensive internal bioinformatics teams. In summary, higher data volume per study enhances both the demand and the readiness to invest in AI-driven interpretation and automation to safeguard turnaround time and efficiency. All these factors cumulatively drive the overall market growth.

- For instance, in October 2025, Illumina Inc. announced BioInsight, explicitly positioning it to meet the industry need to access and interpret ever larger-scale multiomic data by combining sequencing, data analysis, software and AI.

MARKET RESTRAINTS

Data Privacy, Security, And Data-Residency Constraints to Hamper Market Growth

Data privacy, security, and data-residency regulations serve as a market constraint in AI within Genomics due to the sensitive nature of complex genomic data, preventing many buyers from easily transferring it across borders or sharing it between institutions. This compels vendors to create hosting, consent management, and governance controls tailored to specific regions, leading to higher deployment time and expenses. Healthcare providers and public programs require robust auditability and stringent access controls, resulting in extended procurement cycles and a reduced rate of pilots rapidly transitioning to large-scale implementations. When organizations are concerned about breach risks or ambiguous downstream applications of genetic data, they may halt data-sharing agreements, restrict cloud usage, or limit secondary purposes, resulting in a direct decrease in platform utilization and postponing revenue growth. This results in limiting the market growth to a certain extent.

MARKET OPPORTUNITIES

Increasing Government and Public Health Investments to Boost Market Growth Opportunities

Investment by government and public health in genomic surveillance and population genomics initiatives presents a distinct market opportunity for AI in Genomics, as it generates sustained, budgeted demand for scalable analysis rather than merely isolated research projects. As nations transition from COVID-era trials to ongoing surveillance systems, they require AI-powered software to streamline variant identification, quality assurance, and outbreak signal analysis through extensive, continuous data streams. These initiatives also need secure data platforms to exchange insights across laboratories and countries while upholding governance, driving demand for cloud/hybrid genomics analytics solutions and managed services. Significantly, public programs produce extensive longitudinal datasets that can be repurposed for readiness, monitoring antimicrobial resistance, and understanding population risks, thereby enhancing the application of downstream AI analytics. This ongoing government support aids in stabilizing revenues and diminishes cyclicality in comparison to solely research-driven demand. All the above factors are anticipated to drive the market growth in the coming years.

- For example, in December 2025, Asia Pathogen Genomics Initiative announced the public preview of PathGen, an AI-powered outbreak intelligence tool designed to combine pathogen genomics with contextual data and support faster, cross-border outbreak decision-making.

MARKET CHALLENGES

Integration Complexity Pose as a Significant Challenge to Market Growth

Integration complexity with LIMS/EMR, lab workflows, and existing bioinformatics stacks is a key market challenge in AI in Genomics as most buyers cannot “rip and replace” their operational systems. Each lab typically has its own sample tracking, accessioning, QC rules, reporting formats, and data governance, so deploying an AI platform often requires custom interfaces, data mapping, and validation. This increases implementation time, elevates services dependency, and can delay go-live, especially in regulated clinical settings where workflow changes must be documented and audited. Integration issues also create adoption risk: even strong AI performance will not scale if results cannot flow cleanly into the clinician’s or laboratorian’s everyday tools. All the factors mentioned above collectively affect the growth of the market.

Segmentation Analysis

By Component

Increasing Number of Software Deployments to Propel Segmental Growth

Based on the component, the market is divided into software and services.

The software segment captured the largest global AI in genomics market share. This is the most repeatable revenue path in this market. As sequencing volumes rise, labs and pharma teams prioritize tools that automate manual review, standardize results, and shorten turnaround times, which drives larger and more recurring software contracts. Software also scales across sites and studies with low marginal cost, so enterprises can expand usage faster than they can grow specialized bioinformatics headcount. In addition, vendors continuously upgrade algorithms and pipelines, making subscription and license renewals more frequent.

- For instance, in May 2025, Illumina launched DRAGEN v4.4 software, positioned as a comprehensive secondary analysis solution with out-of-the-box oncology apps, multi-omics pipeline support, and improved variant calling accuracy.

The services segment is anticipated to rise with a CAGR of 26.83% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

High Usage in Various Applications to Boost Segmental Growth

On the basis of technology, the market is divided into machine learning, natural language processing, and others.

The machine learning segment dominated the global market in 2025. This is due to the reason that most high-value genomic workflows are fundamentally pattern-recognition problems at massive scale, from separating true variants from sequencing noise to predicting variant impact and prioritizing clinically relevant findings. As sequencing volumes grow, buyers need algorithms that learn from data and generalize across assays, populations, and tumor types, which makes ML the core engine behind modern secondary analysis and interpretation. ML-based callers and recalibration models also improve accuracy while reducing manual review burden, directly supporting faster turnaround times in clinical genomics. In pharma and population genomics, ML is equally central for cohort modeling, biomarker discovery, and multi-omics integration where relationships are non-linear and high-dimensional. Furthermore, the segment is set to hold 66.8% share in 2026.

- For instance, in May 2025, in the DRAGEN v4.4 release, Illumina highlights “built-in AI” with machine learning-based variant recalibration for germline SNV calling, showing how ML is embedded in core genomics analysis software that drives the bulk of commercial demand.

The natural language processing segment is anticipated to rise with a CAGR of 32.79% over the forecast period.

By Application

High Usage in Disease Diagnosis to Boost Segmental Growth

On the basis of application, the market is divided into clinical diagnostics, drug discovery & development, population genomics, precision medicine, and others.

The clinical diagnostics segment captured the highest share of the global market in 2025. This can be linked to the rising prevalence of chronic illnesses, the escalating demand for swift disease detection, and the rising count of regulatory approvals for advanced products. Furthermore, the segment is set to hold 29.3% share in 2026.

- For instance, in February 2025, Aiforia announced it obtained IVDR certification and launched three CE-IVD marked AI solutions for breast and prostate cancer diagnostics.

The drug discovery & development segment is anticipated to rise with a CAGR of 28.44% over the forecast period.

By Deployment

Rising Shift toward Cloud-based Solutions Supported Segmental Dominance

Based on the deployment, the market is divided into cloud-based, on-premise, and hybrid.

The cloud-based segment is anticipated to capture the largest global market share in 2025. This is due to the reason that cloud deployment supports elastic acceleration (e.g., GPUs) for heavier ML models and multi-omics analysis, helping customers shorten turnaround times. In addition, cloud platforms also make it easier to standardize pipelines across sites, centralize governance, and collaborate across distributed research/lab teams without copying datasets repeatedly. Furthermore, the segment is set to hold 46.1% share in 2026.

- For instance, in April 2025, AWS announced workflow versioning support in AWS HealthOmics, a managed cloud service for biological data stores and workflows.

The hybrid segment is anticipated to rise with a CAGR of 31.08% over the forecast period.

By End User

Continuous Genomics Workloads Across Drug Lifecycle to Support Pharmaceutical & Biotechnology Companies Maintain Leading Position

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, clinical labs & diagnostic centers, and others.

In 2025, the pharmaceutical & biotechnology companies segment held the leading position in the global market. This is as they run the largest, most continuous genomics workloads across the drug lifecycle such as target discovery, biomarker identification, patient stratification, and companion diagnostic development. Their pipelines generate large multi-omics datasets, and AI tools help convert these datasets into actionable signals faster, improving R&D productivity and decision quality. Furthermore, the segment is set to hold 34.1% share in 2026.

- For instance, in August 2025, SOPHiA GENETICS announced an expanded multi-year collaboration where AstraZeneca will use SOPHiA’s multimodal AI Factories to analyze healthcare data (including genomics) and generate evidence on therapies.

In addition, clinical labs & diagnostic centers are projected to grow at a CAGR of 32.40% during the study period.

AI in Genomics Market Regional Outlook

By region, the market is segmented into Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa.

North America AI in Genomics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America market size was USD 0.55 billion in 2024 and dominated the global market. The region also maintained its dominance in 2025, with USD 0.62 billion. Key Factors such as strong pharmaceutical and diagnostic infrastructure, expanding usage of sequencing, and supportive government policies for AI adoption are driving the regional dominance.

U.S. AI in Genomics Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 0.64 billion in 2026, accounting for roughly 41.1% of the global market.

Europe

Europe market size is anticipated to grow at 29.58% CAGR during the forecast period. The region is anticipated to capture the second leading position among all regions. The European market is majorly driven by well-established presence of clinical genomics hubs and research centers, increasing investments in AI integration, and widespread adoption of AI technologies in healthcare.

U.K. AI in Genomics Market

The U.K. market in 2026 is estimated at around USD 0.08 billion, representing roughly 5.3% of global revenues.

Germany AI in Genomics Market

Germany market size is projected to reach approximately USD 0.10 billion in 2026, equivalent to around 6.2% of global sales.

Asia Pacific

Asia Pacific market size is projected to be valued at USD 0.31 billion in 2026 and secure the position of the third largest region in the global industry. This is driven by rapid sequencing adoption and biotechnology investment in China, India, Japan, and other factors.

Japan AI in Genomics Market

The Japan market in 2026 is estimated at around USD 0.07 billion, accounting for roughly 4.4% of global revenues.

China AI in Genomics Market

China’s market is projected to reach revenues of around USD 0.08 billion in 2026, representing roughly 5.0% of global sales.

India AI in Genomics Market

The India market in 2026 is estimated at around USD 0.06 billion, accounting for roughly 3.8% of global revenues.

Latin America and Middle East & Africa

Latin America and the Middle East and Africa regions would grow at a relatively slower rate over the study period. The Latin America market size is set to reach a valuation of USD 0.09 billion in 2026. These regional growth is majorly driven through rising emphasis on digital healthcare infrastructure and expanding usage of AI in these regions.

Among the Middle East & Africa region, the GCC market in 2026 is estimated at around USD 0.02 billion, accounting for roughly 1.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Technological Advancements in AI-enabled Genomics Platforms by Prominent Companies to Strengthen Market Share

The global AI in genomics sector is moderately fragmented, with numerous technology and platform suppliers contending in areas such as secondary analysis, variant interpretation, and precision health data management. Major players such as Illumina, QIAGEN, SOPHiA GENETICS, DNAnexus, and NVIDIA, among others still represent a large portion due to their robust installed base, scalable software solutions, and expanding partner networks. These firms are mainly concentrating on ongoing software enhancements, preparedness for cloud/hybrid deployment, and collaborations with healthcare/pharma partners to increase adoption and broaden their market reach.

- For instance, in May 2025, QIAGEN announced it signed a definitive agreement to acquire Genoox, adding the Franklin AI-powered cloud platform for clinical genomics interpretation and strengthening QIAGEN Digital Insights for faster, scalable NGS data interpretation.

Other notable participants strengthening the competitive landscape include Fabric Genomics, Congenica, Genomenon, Velsera (Seven Bridges), and Tempus, among others. Further, these players are actively developing AI-driven interpretation and evidence automation capabilities for genomics-led clinical and R&D workflows.

LIST OF KEY AI in GENOMICS COMPANIES PROFILED

- Illumina, Inc. (U.S.)

- QIAGEN (Germany)

- SOPHiA GENETICS (Switzerland)

- Fabric Genomics, Inc. (U.S.)

- DNAnexus, Inc. (U.S.)

- TEMPUS (U.S.)

- NVIDIA Corporation (U.S.)

- Alphabet Inc. (U.S.)

- Velsera Inc. (U.S.)

- Genomenon, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: SOPHiA GENETICS and Complete Genomics announced a collaboration to integrate sequencing and SOPHiA’s AI analytics, launching/co-marketing oncology applications to accelerate adoption of personalized medicine

- September 2025: SeqOne announced that it entered an agreement to acquire Congenica, combining AI-driven NGS analysis with clinical decision support and interpretation services to create a larger genomics software pure player.

- July 2025: AWS HealthOmics introduced workflow creation from third-party Git repositories, supporting reproducible, collaborative bioinformatics pipeline deployment on a managed genomics workflow service.

- June 2025: Velsera announced expanded capabilities and impact of its Global Data Network (GDN), a federated ecosystem enabling life sciences teams to access real-world longitudinal clinico-genomic data at scale for drug development.

- March 2025: Genomenon launched an enhanced AI-powered integration for its Mastermind Genomic Intelligence Platform, aimed at improving genomic evidence search and interpretation workflows.

REPORT COVERAGE

The global AI in genomics market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements in products, the regulatory environment, and new product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments in the market. The global market forecast report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 29.85% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Technology, Application, Deployment, End User, and Region |

|

By Component

By Technology

By Application

By Deployment

By End User

|

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.36 billion in 2025 and is projected to reach USD 12.57 billion by 2034.

In 2025, the market value stood at USD 0.62 billion.

The market is expected to exhibit a CAGR of 29.85% during the forecast period.

By component, the software segment is expected to lead the market.

The rapid growth in sequencing and multi-omics data volumes, and growing adoption of digital infrastructure are primarily driving market expansion.

NVIDIA Corporation, Illumina Inc., and QIAGEN are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us