Artillery Fire Control Systems Market Size, Share, & Industry Analysis, By Offering (Hardware, Software, & Services), By System (Computer and Display & Interface Units, Target Acquisition & Guidance Systems, Navigation Systems, Power Systems, Auxiliary Systems, & Stabilization Systems), By Technology (Digital, Networked, Auto-laying, Digital, Networked, Manual-laying Assist, Partial Digital, & AI-Assisted), By Platform (Tracked SPH, 8×8 / 6×6 Wheeled SPH, Truck-Mounted Rocket Systems, Truck-Mounted Mortars, & Other), By Solution, By Sales Channel, By End User, and Regional Forecast 2026-2034

KEY MARKET INSIGHTS

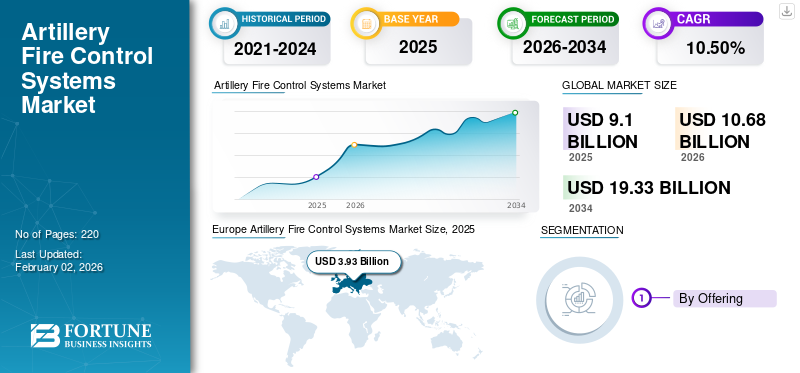

The global artillery fire control systems market size was valued at USD 9.10 billion in 2025 and is projected to grow from USD 10.68 billion in 2026 to USD 19.33 billion by 2034, exhibiting a CAGR of 10.50% during the forecast period. Europe dominated the global market with a share of 36.81% in 2025.

Artillery fire control systems (AFCS) are integrated technologies employed by armed forces to increase the accuracy, efficiency, and efficacy of their artillery units. These systems incorporate various sensors, data processing, software, and occasionally communications equipment to determine ballistic trajectories, conduct real-time targeting, and automate the aiming and firing of artillery weapons. Essentially, AFCS provides for quick computation of firing solutions by feeding information about target position, weather, type of ammunition, and weapon configuration, significantly lessening reaction time and battlefield accuracy.

The main rationale for using artillery fire control systems is to deliver maximum firepower at a minimal risk and amount of wasted ammunition. In contemporary warfare, the importance of fast responsiveness, integrated attacks, and minimizing collateral damage has increased exponentially.

AFCS enables rapid response to moving targets, environmental condition changes, and compatibility in higher-level networked battlefield technologies. This facilitates artillery units to provide effective fire support, defensive or offensive, with increased efficiency and a greater likelihood of first-round hits. In addition, the automation of ballistic calculations lightens the load on human operators, enabling them to concentrate on command decisions while suppressing errors associated with hand computation.

In the defense industry, there is a rising need for AFCS due to several factors. To begin with, the growing sophistication of threats, such as the emergence of highly maneuvering enemy forces and the spread of precision-guided munitions, calls for sophisticated targeting and response capabilities. Second, the military forces around the globe are undertaking continuous digital transformation efforts that call for interoperable systems that enable joint operations and unencumbered sharing of data.

The worldwide artillery fire control systems market consists of various key players with a reputation for innovation, scale of deployment, and top-of-the-line technology. The market's top 6-7 players are BAE Systems, Lockheed Martin Corporation, Rheinmetall AG, Leonardo S.p.A., Saab AB, Elbit Systems Ltd, General Dynamics Corporation, and so on, among others.

These organizations serve a wide variety of military customers worldwide, addressing the tide of growing battlefield digitization, more intelligent ammunition, and the need for greater survivability and operational responsiveness in artillery units. With military organizations putting greater emphasis on precision, velocity, and coordination, the position and complexity of the artillery fire control systems are likely to be anticipated in the forecast period.

Download Free sample to learn more about this report.

Artillery Fire Control Systems Market Key Takeaways

- 2025 Market Size: USD 9.10 billion

- 2026 Market Size: USD 10.68 billion

- 2034 Forecast Market Size: USD 19.33 billion

- CAGR: 10.50% (2026–2034)

- Europe dominated the market with a 36.81% share in 2025.

- The Hardware sub-segment held the largest market share.

- Navigation Systems are projected to be the fastest-growing system segment.

Asia Pacific

Asia Pacific generated USD 2.62 billion in 2025 and is projected to reach USD 3.13 billion in 2026.

North America

North America recorded USD 2.08 billion in 2025 and is projected to reach USD 2.41 billion in 2026.

Europe

Europe accounted for USD 3.93 billion in 2025 and is expected to remain at USD 3.93 billion in 2026.

U.S.

U.S. remains a major market, driven by increasing investments in artillery modernization and advanced defense technologies.

Japan

Japan is expected to witness steady growth, supported by rising defense modernization initiatives and increasing focus on regional security.

Read More

Market Dynamics

Market Driver

Geopolitical Tensions, Defense Budget Expansion, and Precision Warfare Requirements Drive the Market Growth

The incorporation of sophisticated sensor technologies, ballistic compute algorithms, and real-time meteorology processing into fire control systems allows artillery forces to fire indirectly with unparalleled precision over extended ranges of engagement. Countries investing generously in artillery modernization are aware that digital fire control systems cut ammo expenditure substantially through enhanced hit probability, thus reducing operation expenses while increasing mission efficiency.

The U.S. Army's creation of the Artillery Execution Suite (AXS) is a paradigm shift in fires execution software, with end-to-end fires demonstrations successfully completed in May 2025 that engaged M142 HIMARS systems, signifying the evolution toward next-generation fire control capabilities that will phase out legacy AFATDS platforms.

Rising security concerns in multiple theaters, especially in Eastern Europe in the wake of Russia's continuous military campaigns in Ukraine and increased Indo-Pacific tensions over territorial conflicts, have pushed national governments to greatly augment defense appropriations with particular focus on building indirect fire capabilities through new artillery fire control systems.

The proven efficacy of precision artillery fires in recent wars has dramatically shifted military buying priorities, with defense planners realizing that better fire control technology gives asymmetric leverage in contested terrain where battlefield survivability is decided by rapid target engagement and shoot-and-scoot capability. Regional actors and partnering countries collectively are investing in fire control modernization initiatives that facilitate interoperability within multinational coalition structures, securing seamless data transfer and synchronized fires delivery across varied artillery systems operating under common command hierarchies.

Market Restraint

High System Acquisition Costs and Integration Complexity Can Hamper the Market Growth

The high capital outlay involved in the acquisition of sophisticated artillery fire control systems is an important market expansion constraint, especially for emerging economies and countries working within limited defense budgets that cannot put away enough funds to support total artillery modernization programs.

Developing countries with a limited defense industrial base experience compounded difficulties since complex fire control systems require elaborate support environments such as specialized maintenance facilities, periodic software downloads, secure data networks, and ongoing technical support from original equipment manufacturers over operational lifecycles.

The intricacy involved in bringing together fire control systems with current artillery platforms, command and control structures, and legacy communications networks requires great engineering skills and long implementation periods that test financial resources as well as organizational capacities. Apart from initial acquisition costs, artillery fire control systems involve steady operational expenses related to system upkeep, operator training initiatives, software license extensions, cybersecurity infrastructure, and periodic capability refreshals needed to ensure technology parity with changing threat postures.

Market Opportunity

Integration with Loitering Munitions and Extended Range Capabilities Creates Lucrative Opportunities

The fusion of artillery fire control systems and loitering munition capabilities is a revolutionary potential that will change the nature of indirect fires doctrine and tactical employment concepts on future battlefields forever. Artillery fire control systems are adapting to support a variety of munitions, including precision-guided projectiles, extended-range munitions, and loitering systems offering persistent surveillance and time-sensitive strike within company and battalion areas of operation.

The incorporation of loitering munitions into fire support planning allows commanders to engage targets with unprecedented flexibility, short-circuiting classical artillery coordination timelines while delivering precision effects against high-value mobile targets that would otherwise fall out of engagement windows.

Artillery troops that possess fire control systems with the capability to coordinate loitering munition use with conventional indirect fires can produce synergistic effects, harnessing mass fires to suppress areas while using precision loitering systems for surgical attacks against command nodes, tanks, and hidden positions. The U.S. Army's experimentation with loitering munitions as organic fire support resources in maneuver units, with Fire Support Teams at company and battalion levels being the controlling authorities, is a prime example of the doctrinal shift towards distributed precision fires capabilities that will enhance traditional artillery systems.

The General's Ukrainian estimate that advancing columns will be discovered within three to five minutes and strike within a further three minutes emphasizes the tactical imperative for coupling loitering munitions with fire control architectures that support rapid engagement cycles. Trend Machine learning and artificial intelligence technologies are revolutionizing artillery fire control systems at their core by facilitating autonomous target recognition, predictive ballistic computation, and adaptive decision-making capabilities that significantly increase engagement effectiveness while minimizing human operator workload in time-constrained combat environments.

Artillery Fire Control Systems Market Trend

Growing Adoption of Artificial Intelligence and Autonomous Targeting Integration Fuels the Industry Trends

AI-driven fire control programs analyze real-time information from various sensors such as drones, satellites, acoustic sensors, and ground surveillance systems to produce advanced targeting solutions incorporating environmental factors, adversary movement behaviors, and terrain influences without any computational inputs by the artillery crew.

Sophisticated machine learning algorithms repeatedly improve firing solutions with iterative examination of engagement results, self-compensating for systematic inaccuracies, barrel wear profiles, and atmospheric changes to enhance first-round hit probabilities from one consecutive fire mission to the next. Computer vision algorithms included allow fire control systems to automatically detect and classify targets in complex battlefield environments, separate friend from foe from civilian infrastructure from valid military targets, and determine target priority as a function of threat and operational impact.

The development toward autonomous fire control goes beyond targeting improvement to include predictive maintenance features that examine sensor data from components of artillery systems to predict mechanical failures ahead of time, allowing preventive repair to optimize system availability while minimizing operational expenditure.

Autonomous AI-powered navigation systems enable autonomous artillery platforms to move through challenging terrain, select the best possible firing positions based on required ranges and survivability factors, and move to new locations automatically to evade counter-battery fire without being manually directed.

Download Free sample to learn more about this report.

Market Challenges

Interoperability Standards and Multinational Integration Complexity Hinder the Market Growth

Seamless interoperability of various national artillery fire control systems that exist in multinational coalition environments poses ongoing technical and procedural issues that make joint fires planning, coordination, and execution across coalition allies more difficult. Widespread use of proprietary fire control architectures utilizing incompatible communication protocols, data formats, and software interfaces establishes integration barriers that hinder real-time information exchange among artillery units of different countries, diluting the efficiency of coalition fires support operations.

NATO's Artillery Systems Cooperation Activities (ASCA) program provides standardized interfaces for multinational fire control systems to exchange data over common tactical internet networks, yet implementation challenges such as differences in software versions, hardware configurations, and national operating interface procedures generate friction points that slow fire mission processing and diminish operational tempo.

The Dynamic Front 22 exercise demonstrated that mission flow visualization through ASCA messaging structures continues to be difficult, and extensive documentation, such as Commanders Operating Guidance and National Interface Operating Procedures, is needed to establish a shared understanding of capability among national fire control systems.

Segmentation Analysis

By Offering

Artificial Intelligence and Automated Ballistic Computation are Accelerating the Software Segment

The global market, by offering, is further categorized into hardware, software, and services.

The software sub-segment is estimated to be the fastest growing segment in the artillery fire control systems market, propelled by swift technological progressions in artificial intelligence, machine learning algorithms, automated targeting solutions, real-time data processing, networked battlefield coordination, and digital fire control architectures that revolutionize conventional artillery operations from manual calculation processes to automated, intelligent systems capable of autonomous decision support and adaptive engagement strategies.

- For instance, in May 2024, Palantir Technologies won a contract worth USD 480 million from the U.S. Army for its Maven Smart System prototype equipped with artificial intelligence technology that employs algorithms and memory learning abilities generated by AI to scan and detect enemy systems.

Hardware sub-segment holds the leading position in the artillery fire control systems market, generating the highest revenue share in light of the inherent need for physical devices such as sensors, radar systems, ballistic computers, gun directors, navigation systems, laser rangefinders, stabilization systems, displays, power management units, and auxiliary equipment constituting the operational framework supporting precision artillery targeting and engagement capabilities.

By System

GPS-Denied Operations and Autonomous Artillery Boost Navigation Technology Growth

The global market by system is further divided into computer and display & interface units, target acquisition & guidance systems, navigation systems, power systems, auxiliary systems, stabilization systems, and others.

Navigation systems are the most rapidly expanding system segment in the artillery fire control market, propelled by seminal operational needs for accurate artillery location, weapon pointing accuracy, quick emplacement times, and persistent operations in GPS-denied or GPS-degraded conditions dominated by enemy electronic warfare attacks, signal jamming, and spoofing threats to satellite-based positioning dependability. The marriage of Global Navigation Satellite System capabilities with inertial sensors produces hybrid INS/GNSS architectures that combine complementary strengths from both technologies, using satellite signals in nominal operations and naturally switching over to inertial-only navigation during jamming episodes.

- For instance, in February 2025, Safran Electronics & Defense settled a long-term contract spanning from 2024 to 2031 with the Finnish Defence Forces to provide Geonyx Inertial Navigation Systems that include Safran HRG Crystal technology for accurate navigation, targeting, and artillery pointing even in GNSS-denied conditions with compact and robust shock-resistant design to be integrated on various vehicles, mobile radars, and artillery systems such as howitzers, multiple rocket launchers, mortars, and light guns.

Computer and display sets form the preponderant system sector in the artillery fire control market, acting as the focal nervous system that consolidates sensor information, performs intricate ballistic computations, controls targeting solutions, and displays vital operational data using user-friendly interfaces that allow artillery units to conduct precision fire missions with little computational delay and optimal situational awareness.

By Technology

Machine Learning Algorithms and Autonomous Target Recognition to Fuel AI-Assisted Segmental Growth

The global market by technology is further divided into Digital, Networked, Auto-laying, Digital, Networked, Manual-laying Assist, Partial Digital, and AI-Assisted.

Artificial intelligence-assisted fire control systems are the most rapidly expanding technology area in the artillery market, led by revolutionary capabilities that provide autonomous target recognition, predictive trajectory optimization, adaptive ballistic calculation, real-time environmental compensation, and machine-speed decision-making that inherently increase fire control response time, accuracy, and operating efficiency beyond the limits of human cognitive processes and decrease crew workload and engagement times in fast-paced combat environments.

- For instance, in September 2025, SMARTSHOOTER received the Innovation Award at the World Police & Security Exhibition for its SMASH Fire modular AI-enabled precision fire control system with target acquisition, tracking, and engagement features using sophisticated artificial intelligence and machine learning algorithms that allow instant target recognition and precision targeting while ensuring human control.

Digital, networked, and auto-laying technologies are the dominating segment in the artillery fire control systems market, reflecting the enabling architecture to support today's artillery operations by automated fire control calculations, networked battlefield management, and autonomous weapon location features that obviate gun-laying operations by hand and incorporate artillery units into inclusive command and control networks across tactical through strategic echelons.

By Platform

Expeditionary Deployment and Reduced Logistical Footprint Driving Wheeled SPH Growth

The global market by platform is further categorized into Tracked SPH, 8×8 / 6×6 Wheeled SPH, Truck-Mounted Rocket Systems, Truck-Mounted Mortars, Fixed/Emplaced (Ground & Naval), and Air-Based Systems.

8×8 and 6×6 wheeled self-propelled howitzers (SPHs) are projected to be the fastest growing platform segment within the artillery fire control market, driven by military requirements for systems that offer strategic mobility, reduced acquisition and maintenance expenses, and compatibility with current wheeled vehicle fleets. Wheeled SPHs such as Nexter's Caesar, KNDS's RCH 155, and Turkey's T-155 Firtina can support high-speed inter-theater redeployment, road march speeds greater than 90 km/h, and lower infrastructure needs than tracked platforms and are therefore best suited for expeditionary, peacekeeping, and rapid reaction forces.

- For instance, in October 2025, KNDS and Leonardo DRS inked a strategic teaming agreement to promote the Caesar self-propelled howitzer on U.S. Army-standard 8×8 vehicle chassis, targeting the U.S. Army's cannon modernization program by coalescing established wheeled artillery mobility with Leonardo-developed advanced fire control integration, which represents a landmark in wheeled SPH market growth into North American defense programs.

Truck-mounted rocket systems are the dominating in platform sector in the artillery fire control industry, with the greatest share of revenue thanks to their integration of high mobility, quick shoot–and–scoot performance, and multi–mission versatility. Fitted on standard military truck platforms (6×6 or 8×8), the systems provide modular rocket launchers with guided and unguided munitions deployed over extended distances, allowing forces to conduct precision strikes, area saturation, and counter–battery fires while staying open to strategic redeployment opportunities over varied road networks.

To know how our report can help streamline your business, Speak to Analyst

By Solution

Extending Legacy Systems’ Lifecycles with Cost-Effective Upgrades Accelerates Retrofit Demand

The global market by solution is further categorized into New-Build (OEM) and Retrofit.

The retrofit sub-segment is accounted for the largest artillery fire control systems market share in 2024 and is also estimated to be the fastest growing during the forecast period. The growth is attributed to the as defense organizations strive to upgrade existing artillery fleets by incorporating enhanced fire control capabilities without the cost and lead times of totally new platform purchases. Retrofit initiatives enable militaries to modernize older howitzers, rocket launchers, and mortar squadrons with computerized fire control computers, automated laying systems, inertial navigation kits, and networked communications suites, significantly improving precision, responsiveness, and survivability while leaving original capital investments and logistics support infrastructures intact.

- For instance, in July 2024, Leonardo DRS received USD 99 million U.S. Army order to upgrade current mortar platforms with advanced fire control systems, delivering Digital Fire Control Units, advanced ballistic computation software, integrated inertial navigation modules, and improved communication interfaces.

New-Build (OEM) solutions are a high-growth segment as defense buyers acquire finished, factory-integrated artillery platforms with advanced fire control systems, taking advantage of original equipment manufacturers' technical capability to harmonize hardware and software, reduce integration risks, and offer full warranties and support. OEM products incorporate self-propelled howitzers, truck-mounted rocket systems, armored gun carriers, and variants of specialized artillery purpose-designed with embedded digital fire control architectures that include sensors, ballistic computers, navigation systems, displays, and communications that guarantee smooth interoperability and performance validation through strict factory testing regimes.

By Sales Channel

National Sustainment Capabilities Enhancement Drives Local System Integrators Segmental Growth

The global market by sales channel is further categorized into OEMs, Tier-1 AFCS Specialist, Local System Integrator, and Depot/MRO.

Local system integrators are the fastest-growing channel of sales in the artillery fire control system market, propelled by defense ministries' need for specialized integration services, technology transfer contracts, and indigenous local participation satisfying offset obligations, lowering reliance on foreign OEMs, and enhancing national sustainment capabilities. Integrators team up with international OEMs and technology suppliers to domestically assemble, test, and configure fire control modules such as sensors, ballistic computers, displays, and communications suites into new or existing artillery systems, customizing solutions to individual operational doctrines, environmental profiles, and interoperability requirements required by national defense policies.

- For instance, in July 2025, India's Ministry of Defense awarded Bharat Electronics Limited around USD 200 million contract to locally integrate cutting-edge Air Defense Fire Control Radars featuring indigenous signal processors and display units under the Buy (Indian-IDDM) category for the Indian Army, representing a major augmentation of the role of local system integrators in providing customized fire control solutions while ensuring 70 percent indigenous content requirements.

Original Equipment Manufacturers (OEMs) are the dominant sales channel for artillery fire control systems, with the greatest share of procurement revenues because defense customers prefer factory-integrated solutions that integrate artillery platforms and embedded fire control architectures under single-source responsibility. OEMs provide turnkey packages including platform design, fire control hardware, ballistic computation software, navigation systems, communications suites, and lifecycle support through broad warranty and maintenance programs, minimizing integration risk and simplifying procurement processes.

By End User

Expeditionary Ground Combat Demands Drive Fire Control Modernization in Land Forces

The global market by end user is further classified into land force, naval force, and air force.

Land forces are the largest and fastest expanding end user segment in the artillery fire control systems market, with the highest revenue share due to armies globally focusing on precision indirect fires, quick shoot–and–scoot operations, and coordinated joint fires to address emerging land-based threats and asymmetric warfare environments. Contemporary ground combat theory focuses on networked, multi-domain operations necessitating sophisticated fire control capabilities that allow artillery to provide responsive, accurate, and synchronized fire support for maneuver forces, improving battlefield efficiency while minimal collateral damage and ammunition consumption.

- For instance, In October 2025, the U.S. Army granted five Other Transaction Agreements worth USD 4 million to American Rheinmetall Vehicles, BAE BOFORS, Hanwha Defense USA, General Dynamics Land Systems, and Elbit Systems USA for Self-Propelled Howitzer Performance Demonstration contracts, kicking off competitive evaluation for the Next Generation Combat Vehicle program to provide land forces with state-of-the-art SPH platforms with digital fire control and autonomous gun laying on-board capabilities.

Naval platforms are a major growth end-user market for artillery fire control systems based on modernization of ship-mounted gun systems, amphibious assault support vehicles, and coastal defense batteries needing accurate naval fire support, shore bombardment capabilities, and coordinated air–sea engagement. Modern naval combat situations call for brisk target acquisition, range extension of gunfire support, and networked battlefield situational awareness to neutralize anti-ship missiles, swarm attacks, and littoral threats.

Artillery Fire Control Systems Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

Europe

Europe Artillery Fire Control Systems Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Europe region accounted for the largest share of the global artillery fire control systems market, fueled by unprecedented security needs resulting from the current Russia-Ukraine conflict and NATO's collective resolve to strengthen continental defense capacities through overall artillery modernization programs. Europe contributed approximately USD 3.93 billion to the global market in 2025, accounting for 36.81% share, and is expected to reach USD 3.93 billion in 2026.

European countries have radically shifted their defense procurement strategies towards filling vital capability shortfalls revealed by modern warfare, focusing on artillery systems with cutting-edge fire control capabilities that support precision targeting, networked operations, and the quick response capabilities needed to counter sophisticate adversary threats. The strategic focus on interoperability through the framework of NATO's Artillery Systems Cooperation Activities has driven investment in compatible fire control architectures that allow multinational forces to exchange targeting data across disparate platforms and conduct coordinated fires across the European theater from the Arctic Circle to the Black Sea.

For instance, in February 2025, Elbit Systems won a USD 57 million order to supply its PULS Rocket Launcher Artillery System to the German military, featuring C4I advanced hardware integration and multi-vendor munition capability, allowing the system to fire rocket munitions built by various original equipment manufacturers and offering interoperability across NATO operational environments.

Asia Pacific

The Asia Pacific region is projected to be the fastest growing market for artillery fire control systems, driven by surging defense budgets, border conflicts, competition dynamics, and overall military modernization programs aimed at precision fires capabilities of major military powers, including China, India, Japan, South Korea, and Australia. In 2025, the Asia Pacific market stood at USD 2.62 billion, representing 28.82% of global demand, and is projected to grow to USD 3.13 billion in 2026, with rising investment in advanced defense hardware fuelled by mounting desire to increase military capabilities amidst rising geopolitical tensions.

Border conflicts, territorial disputes in the South China Sea and Taiwan Strait, and regional security issues fuel continued demand for advanced artillery systems integrated with advanced fire control technologies to enhance armed forces' strike capabilities and operational effectiveness across varied terrain conditions from high-altitude mountain borders to sea-influenced theaters. In March 2025, India's Defence Ministry signed the USD 69.73 million acquisition deal for 307 Advanced Towed Artillery Gun Systems and 327 high mobility 6x6 gun-carriage vehicles, the first-ever contract for such heavy-duty indigenous howitzers developed and designed by DRDO, substantially improving the Army's battle readiness along borders with Pakistan and China through outstanding lethality and long-range precision strike capability.

China's military expenditure increased by 7% to an estimated USD 314 billion in 2024, accounting for 50% of all military spending in Asia and Oceania, as the nation continues three decades of consecutive growth, investing in continued military modernization, including artillery fire control systems integration with cyberwarfare capabilities and networked command structures.

North America

The market in North America reached USD 2.08 billion in 2025, representing 23.00% of total market revenue, and is projected to reach USD 2.41 billion in 2026. North America is the second-rapidly expanding regional market for artillery fire control systems, which is marked by high defense spending, extensive artillery modernization programs, and technological leadership in precision-guided ammunition and networked fire control architectures. The U.S. Department of Defense is heavily investing in modernizing artillery systems, developing long-range precision strike capabilities, and enhancing ground forces' mobility by embracing high-end advanced technologies such as automation, precision-guided munitions, and future fire control systems.

The U.S. Army Self-Propelled Howitzer Modernization program is a comprehensive effort to significantly increase firepower, range, and rate of fire through the incorporation of mature technologies, with five top defense contractors American Rheinmetall Vehicles, BAE BOFORS, Hanwha Defense USA, General Dynamics Land Systems, and Elbit Systems USA receiving contracts that are worth around USD 4 million in October 2024 for the conduct of performance demonstrations assessing operationally acceptable solutions.

Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 0.78 billion in 2025, accounting for 8.58% share, and is expected to reach USD 0.89 billion in 2026. The Middle East and Africa offer moderate but consistent artillery fire control systems market growth, led by high defense expenditures among Gulf Cooperation Council countries, consistent security threats such as counter-terror operations, and strategic initiatives aimed at modernizing and focusing on indigenous defense industrial development.

Lead spenders such as Saudi Arabia, UAE, Qatar, and Israel with significant procurement programs for advanced artillery and related fire control technologies. Regional authorities value political agility and technological autonomy, engaging highly competitive market forces where U.S., European, Russian, and increasingly Chinese defense contractors vie for profitable long-term contracts while transfer of technology agreements enable local production capacities in accordance with economic diversification policies.

Latin America

The Latin America market accounted for USD 0.28 billion in 2025, representing 0.00% of the global industry, and is expected to reach USD 0.31 billion in 2026. Latin America is a moderately growing market for artillery fire control systems, with limited defense budgets compared to other regions, but exhibiting strategic priorities for military modernization, improved border security, and regional cooperation efforts towards minimizing dependencies on conventional arms suppliers. Brazil, Chile, Colombia, and Peru are making selective upgrades to artillery capabilities for armored vehicles, howitzers, and integrating fire control system support while prioritizing cost-effectiveness and regional partners' interoperability.

COMPETITIVE LANDSCAPE

Key Market Players

Growing Modernization Programs and Increasing Defense Expenditure Lead to the Major Key Players' Innovations

The global artillery fire control systems market has a semi-consolidated to fragmented structure, with several established defense contractors vying for market share based on technological differentiation, strategic alliances, and long-term government contracts. The market space includes around fifteen to twenty large international competitors such as Rheinmetall AG, BAE Systems plc, Lockheed Martin Corporation, Elbit Systems Ltd., Leonardo S.p.A., Thales Group, General Dynamics Corporation, Northrop Grumman Corporation, Hanwha Aerospace, Saab AB, L3Harris Technologies, RTX Corporation, Kongsberg Gruppen, KNDS N.V., and Honeywell International, which are competing with unique technological strengths, local market positions, and established customer bases to win procurement orders. The market reflects intense competitiveness, especially in Europe and North America, where defense contemporaryization initiatives have hastened purchasing timetables, compelling producers to make quick headway in fire control capacities incorporating artificial intelligence, autonomous targeting, and networked warfare capabilities to make their offerings stand out.

Foreign defense contractors aggressively compete with local manufacturers in developing countries, forming joint ventures, technology transfer agreements, and local production facilities to overcome offset requirements, meet export control regulations, and gain market share in fast-growing defense markets in the Asia-Pacific and Middle East regions. The strict regulatory climate that dictates defense procurement creates significant entry barriers for new market entrants, with incumbent contractors having enjoyed decades of experience working through intricate International Traffic in Arms Regulations, Foreign Military Sales procedures, and national security clearance requirements that constrain technology transfers and limit access to the market by companies that do not have established defense credentials.

The competition dynamics are further complicated by offset clauses requiring local industrial involvement, technology transfer, and domestic content requirements affecting contract awards, with manufacturers setting up subsidiary facilities, partnering with local defense companies, and developing regional production capabilities to meet nationalization needs while preserving technological advantages.

List of Key Artillery Fire Control Systems Market Company Profile

- ASELSAN A.Ş. (Turkey)

- BAE Systems plc (U.K.)

- Bharat Electronics Limited (BEL) (India)

- Denel SOC Ltd. (South Africa)

- Elbit Systems Ltd. (Israel)

- Hanwha Aerospace Co., Ltd. (South Korea)

- Indra Sistemas, S.A. (Spain)

- Israel Aerospace Industry (IAI) (Israel)

- KNDS N.V. (Netherlands)

- Leonardo S.p.A. (Italy)

- Rafael Advanced Defense Systems Ltd. (France)

- Rheinmetall AG (Germany)

- Roketsan A.Ş. (Turkey)

- RTX Corporation (U.S.)

- Safran Electronics & Defense SAS (France)

- ST Engineering Ltd. (Singapore)

- Thales Group (France)

- WB Electronics S.A. (Poland)

KEY INDUSTRY DEVELOPMENTS

- October 2025 - General Dynamics' information and technology division has obtained a task order valued at USD 1.25 billion to assist the U.S. Army in Europe and Africa. This contract, which was awarded in September, includes a five-month initial period for transition as well as seven additional option years. Under the Enterprise Mission Information Technology Services 2 (EMITS 2) task order, GDIT will provide enterprise IT, communications, and mission command support services to the U.S. Army's headquarters in Europe and Africa, its subordinate organizations, NATO, and other allies.

- February 2025 - Israel’s Elbit Systems has received a contract worth around USD 57 million to provide its Precise and Universal Launching System (PULS) rocket artillery system to the German military. The order is being carried out through agreements between the Dutch, Israeli, and German governments.

- February 2025 - Elbit Systems Ltd. has obtained a contract from a European country to provide a Joint National Digital Fire Command Center (JNDFC) and incorporate the nation’s strategic and tactical firepower into the system. The agreements, estimated at around USD 100 million, will allow Elbit to supply sophisticated multi-domain digital warfare capabilities at a joint level.

- February 2025 - Safran Electronics & Defense has completed a contract to supply its Geonyx Inertial Navigation Systems (INS) for the artillery systems of the Finnish Defence Forces. The value of the agreement has not been revealed and will be in effect from 2024 to 2031. Designed with Safran’s HRG Crystal technology, the Geonyx INS is built for precise navigation and artillery targeting, even in situations where global navigation satellite systems may be unreliable.

- July 2024 - Hanwha Aerospace has obtained a contract worth nearly USD 1 billion with Romania for the provision of 54 K91 self-propelled howitzers (SPH) and 36 K102 ammunition resupply vehicles (ARV), underscoring the company's ongoing growth in the international defense sector.

REPORT COVERAGE

The global artillery fire control systems market growth analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the artillery fire control systems market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.50% from 2026-2034 |

|

Unit |

USD Billion |

|

Segmentation |

By Offering · Hardware · Software · Services By System · Computer and Display & Interface Units · Target Acquisition & Guidance Systems · Navigation Systems · Power Systems · Auxiliary Systems · Stabilization Systems · Others By Technology · Digital, Networked, Auto-laying · Digital, Networked, Manual-laying Assist · Partial Digital · AI-Assisted By Platform · Tracked SPH · 8×8 / 6×6 Wheeled SPH · Truck-Mounted Rocket Systems · Truck-Mounted Mortars · Fixed/Emplaced (Ground & Naval) · Air-Based Systems By Solution · New-Build (OEM) · Retrofit By Sales Channel · OEMs · Tier-1 AFCS Specialist · Local System Integrator · Depot/MRO By End User · Land Force · Naval Force · Air Force By Regional North America (By Offering, By System, By Technology, By Platform, By Solution, By Sales Channel, By End User, By Country) · U.S. · Canada Europe (By Offering, By System, By Technology, By Platform, By Solution, By Sales Channel, By End User, By Country) · U.K. · Germany · France · Nordic Countries · Russia · Rest of Europe Asia Pacific (By Offering, By System, By Technology, By Platform, By Solution, By Sales Channel, By End User, By Country) · China · India · Japan · South Korea · Australia · Rest of Asia Pacific Middle East & Africa (By Offering, By System, By Technology, By Platform, By Solution, By Sales Channel, By End User, By Country) · Saudi Arabia · UAE · Israel · Iran · South Africa · Rest of Middle East & Africa Latin America (By Offering, By System, By Technology, By Platform, By Solution, By Sales Channel, By End User, By Country) · Brazil · Argentina · Rest of Latin America |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.10 billion in 2025 and is projected to reach USD 19.33 billion by 2034.

In 2025, the market value stood at USD 3.93 billion.

The market is expected to exhibit a CAGR of 10.50% during the forecast period of 2026-2034.

The land force segment is expected to hold the highest CAGR over the forecast period.

Geopolitical tensions, defense budget expansion, and precision warfare requirements drive the market growth.

Raytheon Technologies, Lockheed Martin, Thales Group, Bharat Electronics Limited (BEL), Israel Aerospace Industries (IAI), and others are top players in the market.

Europe dominated the global market with a share of 36.81% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us