Assault Rifles Market Size, Share & Russia-Ukraine War Analysis, By Caliber (5.45 x 39 mm Soviet, 5.56 x 45 mm NATO, 7.62 x 39 mm Soviet, 7.62 x 51 mm NATO / .308 Winchester, 5.7 x 28 mm, and Others), By Rifle Configuration (Traditional Gas-Operated Rifles, Bullpup Rifles, Modular Weapon Systems, Designated Marksman Rifles (DMRs), Squad Automatic Weapon (SAW), and Others), By Firing Mode (Automatic, Semi-Automatic, and Burst Mode), By Range (Short Range (up to 300 m), Medium Range (300 to 600 m), and Others), End User (Law Enforcement and Military), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

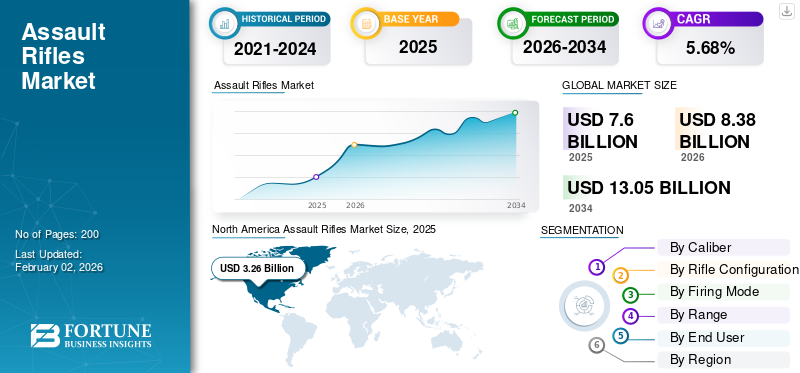

The global assault rifles market size was valued at USD 7.60 billion in 2025 and is projected to grow from USD 8.38 billion in 2026 to USD 13.05 billion by 2034, growing at a CAGR of 5.68% during the forecast period. North America dominated the global market with a share of 42.91% in 2025.

Assault rifle is a type of a long gun with selective fire capability that uses an intermediate cartridge and detachable magazine. The rifle can switch between semi-automatic and fully automatic or burst modes. These rifles possess a modular design which allows the users with various types of accessories such as optics, lights, and fore grips. The capacity of the number of standard magazines can vary, but mostly the assault weapons have a magazine capacity of 20 to 30 rounds. They have rapid rate, greater muzzle velocity, and are increasingly used in close combat situations, insurgency and other military operations.

Few prominent key players in the market including FN Herstal, Lithgow Arms, Heckler & Koch, Israel Weapon Industries (IWI), Norinco, Kalashnikov Concern JSC, and others constantly focus on the development of robust and effective assault guns with lightweight, maneuverable, and with shorter barrels. Companies are designing models including features such as folding or telescoping stocks, pistol grips, bayonet lugs, and threaded barrels for attaching accessories such as flash suppressors or grenade launchers.

Download Free sample to learn more about this report.

Russia-Ukraine War Impact

The Russia-Ukraine war has significantly impacted the market globally, influencing various aspects such as demand, manufacturing, supply chains, and geopolitical dynamics. There is an increase in demand and procurement to enhance the military capabilities of the countries involved in the conflict. Both Ukrainian forces and their allies have increased the procurement of automatic and semi-automatic rifles to equip frontline troops. Ukraine has received significant military aid from Western countries, including modern rifles. For instance, in April 2025, Germany showed its support for Ukraine by supplying equipment and weapons.

The country supplied protective equipment, vehicles, and weapons including assault weapons. For instance, in July 2025, Russian intelligence officers received A-545 KORD rifles with balanced automatic weapons that minimize recoil. In the Russian-Ukrainian war, this assault rifle was only occasionally used by Russian Special Forces. The conflict has affected global arms trade dynamics, influencing the availability and pricing of rifles worldwide. Countries are reassessing their military inventories and procurement strategies in response to the conflict which is expected to drive the demand for assault weapons.

Assault Rifles Market Trends

Development of Modular and Multi-Caliber Assault Rifles

Manufacturers have shifted to the development of advanced assault weapons with multi-caliber properties. These changes are made to enable quick alterations to components such as barrels, stocks, and calibers. This helps the users as the rifle can adapt according to the military and law enforcement needs and mission requirements for close quarters, combat or long range engagement. Assault weapon models such as SIG Sauer XM7 are used by the Army’s Next Generations Squad Weapon Program. These rifles often support calibers such as 5.56 mm, 6.8mm or .300 Blackout.

Furthermore, rifle makers improve the weapon design based on the received feedback and suggestions from the defense forces. For instance, in May 2025, Ceská Zbrojovka (CZ) announced the launch of the CZ BREN 3 assault rifle modular, multi-caliber assault rifle available in 5.56×45mm NATO and .300 AAC Blackout calibers. This development was influenced by the mission requirements feedback from various military users including Czech Army and Ukrainian forces. In addition, military forces are shifting toward multi caliber assault weapons to reduce logistical burdens and replacement of weapon systems to adapt to evolving threats and technologies.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increase in Defense Budget & Military Modernization Programs to Propel Market Growth

Various countries across the globe are increasing their defense budgets with the aim of modernizing armed forces and enhancing defense capabilities. The defense expenditure has witnessed a significant increase in recent years. For instance, according to SIPRI (Stockholm International Peace Research Institute), the global defense budget reached USD 2.7 trillion in 2024, an increase of 9.4 per cent in real terms from 2023. Countries in Asia, the Middle East & Africa, and Europe, witnessed major budget increases in response to the rise in geopolitical tensions and security threats. For instance, in March 2025, China announced that it will increase the country’s defense budget 7.2% this year as it plans to modernize the military assets. The surge in conflicts, territorial disputes, and cross-border tensions occurring across the world has encouraged governments to start making huge investments in weapons such as assault rifles to strengthen national security.

In addition, the military sectors of different countries is initiating modernization plans to respond to new and emerging security challenges. There is also a rise in modernization efforts driven by a need to improve combat effectiveness, enhance soldier safety, and adapt to evolving threats and technologies. For instance, in April 2025, Netherlands defense forces announced its plans for acquisition of new military equipment such as assault weaponry including Colt C7 rifle and C8 carbine and the MAG 7.62mm across air, land, and sea to strengthen its armed forces and bolster supply security. Such defense budget increase and ongoing modernization programs are expected to drive the assault rifles market growth over the forecast period.

Market Restraints

Strict Government Regulations and Export Control Hinder Market Growth

There are stringent regulations on the manufacturing, design, supply and export of assault weapons. Governments across the world are making laws stricter as a response to the rising concerns over civilian gun violence, armed conflicts and terrorism. For instance, Australia and some parts of the European Union have rigorously banned civilian ownership of assault-style weapons. In addition, the international treaties such as Arms Trade Treaty and others impose strict export controls on small arms and light weapons to avoid any type of misuse.

Such policies enacted by the governments of various countries are expected to limit the market expansion opportunities. Furthermore, the manufacturing and sales of these rifles require lengthy licensing procedures, compliance costs and potential legal liabilities which hampers the assault rifles market share.

Market Challenges

State level Bans & Arms Trafficking Pose a Significant Challenge for the Market

The use of assault weapons continues to develop uncertainty in the overall global market as there are potential bans & restrictions which impacts the sales & production of assault weapons. Numerous countries and sub national entities impose strict regulations or outright bans on the sale, possession and manufacturing of assault weapons. Such restrictions create entry barriers to the market and limit opportunities for market expansion.

Market Opportunities

Technological Advancement to Drive Market Growth Opportunities

Technological advancements and evolution is expected to play a major role in the growth and expansion of the market. Due to the changing nature of conflicts and evolution of modern warfare, there is an increase in the need for lethal weapons that possess characteristics such as light weight, modular, and adaptability among others. This in turn fuels the advancement in material, design and optics as well as integration capabilities. Modern rifles are increasingly being designed with modular components allowing military personnel to customize barrels, stocks, grips & rails. Moreover, integration of smart optics, thermal scopes, holographic sight and fire control systems will enhance the targeting precision.

Segmentation Analysis

By Caliber

5.56 x 45 mm Segment Held the Largest Share Due to Widespread Adoption and Operational Versatility

On the basis of caliber, the market is classified into 5.45 x 39 mm Soviet, 5.56 x 45 mm NATO, 7.62 x 39 mm Soviet, 7.62 x 51 mm NATO / .308 Winchester, 5.7 x 28 mm, 5.8 x 42 mm, 6.5 mm Grendel, 6.8 mm Remington SPC, and others.

The 5.56 x 45 mm NATO is expected to hold the largest share of 50.54% in 2026, due to its wide use in the NATO countries and allied forces. This caliber has become the standard for rifles, including the widely deployed M4, M16, HK416, and FN SCAR-L. Due to its balanced performance, and effective range, it is gaining more popularity in current times. In addition, military forces across the world have heavily invested in the development of 5.56 x 45 mm NATO rifles.

The 6.8 mm Remington SPC segment is expected to depict the fastest growth over the forecast period. The segment is anticipated to grow in future due to the enhanced range and accuracy provided by this caliber type rifles. Many countries are investing in programs aimed to modernize the capabilities of weapon systems including automatic rifles. There is a rise in upgrading assault weapons with powerful cartridges that can perform effectively across urban, open and mountainous terrain. For instance, in April 2025, India’s Defence Research and Development Organization (DRDO) revealed a new prototype of 6.8x43mm assault rifle. This shift from development of 5.56mm to 6.8mm rounds is inspired by U.S Next Generation Squad Weapon (NGSW) program.

By Rifle Configuration

Traditional Gas Operated Rifles Segment to Hold the Largest Share Due to its Cost-Effectiveness & Standardized Rifle

On the basis of rifle configuration, the market is classified into traditional gas-operated rifles, bullpup rifles, modular weapon systems, designated marksman rifles (DMRS), squad automatic weapon (SAW), personal defense weapons (PDW)/close quarters battle (CQB) carbines, and civilian-legal semi-automatic rifles.

The Traditional Gas Operated Rifles segment is projected to remain the dominant segment market share of 32.52% in 2026. The segment holds the highest share as it has a long-standing dominance in military service across the world. These rifles use proven gas impingement or piston systems to cycle ammunition consistently under various combat conditions. Various models such as the M16, AK-47, AK 103 and G36 fall under this category. The widespread use, standardized training and mature production infrastructure makes it a cost-effective and suitable option for national defense procurement.

The modular weapons systems segment is estimated to grow at the fastest CAGR in the forecast period. This segment is expanding rapidly due to increase in demand for highly customizable, fission and adaptable platforms. These rifles are designed with interchangeable components such as barrels, stocks, upper receivers and optics. These components allow the personnel to tailor the weapon for their various missions and combat scenarios. They are also highly preferred in urban warfare and special operations.

By Firing Mode

Automatic Segment Leads Due to its Military Preference & Tactical Advantage

On the basis of firing mode, the market is classified into automatic, semi-automatic, and burst mode.

The automatic segment is projected to holds the largest share of the market as 66.47% in 2026, as militaries prefer automatic assault rifles for their ability to deliver continuous, rapid-fire bursts, which are crucial during intense combat scenarios. Automatic rifles allow soldiers to switch between semi-automatic and fully automatic modes, providing tactical versatility in various combat environments. Most standard rifles such as M4A1, FN2000 feature full auto capabilities as default or selective option. Thus, increase in use of automatic rifles due to its firing mode in close quarters combat and urban warfare drives the segmental growth.

The semi-automatic segment is estimated to be the fastest-growing segment as there is an increase in demand from civilian market and law enforcement agencies. Moreover, many countries impose restrictions on fully automatic firearms, making semi-automatic rifles the preferred choice for civilians and law enforcement due to their legal permissibility. Semi-automatic rifles are easier to operate and require less training compared to fully automatic weapons, making them suitable for a broader user base.

To know how our report can help streamline your business, Speak to Analyst

By Range

Medium Range (300 to 600 m) Segment Holds the Largest Market Share Due to Operational Versatility and Tactical Standardization

On the basis of range, the market is classified into short range (up to 300 m), medium range (300 to 600 m), and long range (above 600 m).

The medium range (300 to 600 m) segment is estimated to holds the largest share of the market as 53.05% in 2026, this range is preferred over most standard issue rifles adopted by military and paramilitary forces. Rifles such as the M4, AK 103 HK416, AK 12, HK417, FN SCAR®-L CQC have semi-automatic firing capabilities. Modern armed forces emphasize versatility, often requiring rifles that can effectively engage targets at intermediate distances (300-600 meters), driving demand for medium-range rifles.

The long range (above 600 m) segment is estimated to be the fastest-growing segment due to the increase in emphasis on designated marksman roles within infantry units and the need for more accurate high power rifles capable of emerging threats is growing. As modern warfare evolves there is a growing need for rifles that offer higher precision and stopping power. Thus, the technological advancement in optics, ammunition, and barrel design are enabling the development of advanced high range rifles.

By End User

Military Segment Holds the Largest Market Share Due to High Procurement & Long Term Modernization Programs

On the basis of end user, the market is classified into military and law enforcement.

The military segment acquires the largest share of the market due to high procurement of assault weapons to enhance national security and ongoing modernization programs. National defense forces across the globe constantly invest in upgrading the infantry weapons systems as a part of long term strategic options.

The law enforcement agency is estimated to be the fastest-growing segment. The segment growth is driven by increasing need for modern firearms in urban policing, counter terrorism, internal security operations. As threats such as organized crime, insurgencies and terrorism become more complex and urban centric the homeland security forces are required to upgrade their small arms with advanced assault weapons.

Assault Rifles Market Regional Outlook

On the basis of region, the market is studied across North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Assault Rifles Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 42.91% to the global market in 2025, with a valuation of USD 3.26 billion, and is projected to reach USD 3.6 billion in 2026. The U.S. has one of the highest civilian firearm ownership rates globally, with a strong cultural affinity for semi-automatic rifles such as AR-15s, fueling demand in the civilian market. Certain states, such as Texas, Florida, and Arizona, have relatively permissive gun laws, allowing easier access to rifles, which drives regional sales and market expansion. Urban and suburban areas, particularly in states including California and New York, have witnessed increased interest in tactical shooting and personal defense, leading to higher demand for rifles. In addition, the U.S is investing in replacing the current standard-issue weapons in the U.S. Army with a more innovative and effective weapon system. In 2025, the U.S. Army is in the process of procuring the new XM7 rifle (formerly known as NGSW) as its standard service rifle, gradually replacing the M4A1 carbine. The U.S. market is projected to reach USD 3.03 billion by 2026.

Europe

Europe accounted for USD 1.87 billion in 2025, representing 24.59% of the global market share, and is projected to reach USD 2.05 billion in 2026. Europe is witnessing rapid growth in the market, driven by increase in defense budget, and growing demand to improve defense capabilities for war and future conflicts. Germany, France, and the U.K. have been upgrading their military and police forces with assault weapons such as the HK416 and FN SCAR, creating regional demand for these firearms. For instance, in May 2025, Heckler & Koch completed the deliveries of the G95A1 and KA1 assault weapons to the German Armed Forces. This delivery was a part of the German Armed Forces’ small arms modernization program. European firearm manufacturers including Heckler & Koch and CZ have a significant export presence, which influences domestic markets, especially in countries where military-grade firearms are accessible for civilian use under strict regulations. The UK market is projected to reach USD 0.25 billion by 2026, and the Germany market is projected to reach USD 0.42 billion by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 1.64 billion in 2025, capturing 21.51% of global revenue, and is estimated to reach USD 1.82 billion in 2026. Asia Pacific is rapidly emerging as a significant player in the market. India, South Korea, and Australia have been investing heavily in upgrading their armed forces with rifles such as the INSAS, K2, and Steyr AUG, leading to increased domestic production and procurement. India, Pakistan, and China face insurgency and terrorism threats, prompting procurement of military-style firearms, including rifles, for their security forces to combat internal threats. For instance, in June 2025, Indo-Russian Rifles Private Limited (IRRPL) contracted with the Indian Army for supply of Indigenous AK-203 assault rifles which will be delivered by December 2025. Another batch of 70,000 rifles will be supplied in the next five months. The Japan market is projected to reach USD 0.2 billion by 2026, the China market is projected to reach USD 0.75 billion by 2026, and the India market is projected to reach USD 0.42 billion by 2026.

Middle East & Africa

The market in Middle East & Africa reached USD 0.34 billion in 2025, representing 4.51% of total market revenue, and is projected to reach USD 0.37 billion in 2026. In the Middle East & Africa countries such as countries such as Iraq, Syria, and Yemen have experienced prolonged conflicts, leading to high demand for rifles such as the AK-47, M16, and other military-grade firearms for the military. Moreover, countries across these regions are investing heavily in procurement due to an increase in defense budgets. For instance, in October 2024, the Turkish Ministry of Defense announced an increase in defense spending in 2025, the budget will amount to USD 47 billion. The Middle East is a major importer of assault rifles from global manufacturers (e.g., Russia, the U.S., and Eastern European countries), fueling regional availability and usage.

Latin America

In 2025, the Latin America market stood at USD 0.45 billion, representing 6.49% of global demand, and is projected to grow to USD 0.49 billion in 2026. Mexico, Brazil, and Venezuela face high levels of organized crime, drug trafficking, and gang violence, often involving the use of rifles such as AK-47s and AR-15s by criminal groups for protection and offensive operations. Moreover, cross-border smuggling of firearms from the U.S. and other sources supplies criminal organizations with assault rifles, increasing their prevalence in urban and rural conflict zones.

Competitive Landscape

Key Industry Players

Key Players Focus on Investment in R & D and Strategic Partnerships to Enhance Their Presence

The market is highly competitive, driven by rise in defense budget and investment in the production and procurement of rifles. It is primarily dominated by key market players such as Kalashnikov Concern from Russia, FN Herstal from Belgium, Heckler & Koch from Germany, and Colt from the U.S., although numerous regional and local manufacturers also focus on product portfolios tailored to meet specific national needs. Price and affordability are critical factors influencing procurement decisions, with cost-effective options such as the AK-47 and its variants remaining highly popular in markets with limited military budgets. Geopolitical relations also play a critical role, as countries often favor certain suppliers based on diplomatic ties and strategic alliances.

LIST OF KEY ASSAULT RIFLES COMPANIES PROFILED

- Kalashnikov Concern JSC (Russia)

- Heckler & Koch (Germany)

- Colt Manufacturing (U.S.)

- Israel Weapon Industries (IWI) (Israel)

- NORINCO (China)

- Lithgow Arms (Thales Group) (Australia)

- FN HERSTAL (Belgium)

- Beretta Defense Technologies (Hungary)

- SIG Sauer (Germany)

- Česká zbrojovka a.s. (Czech Republic)

- Kalyani Strategic Systems Ltd. (India)

- STEYR ARMS (Austria)

- Daniel Defense (U.S.)

- Zastava oružje AD Kragujevac (Serbia)

- Advanced Weapons and Equipment India Limited (AWIL) (India)

- ARSENAL (Bulgaria)

- FN America, LLC. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, Česká Zbrojovka (CZ) revealed CZ BREN 3 assault rifle IDET 2025 in Brno, Czech Republic. The CZ BREN 3 is designed to meet the diverse needs of armed forces, offering a versatile platform suitable for various operational requirements.

- In October 2024, Kalashnikov Concern JSC revealed its plans to commence mass production of the 5.45-mm AM-17 compact-sized rifle. The AM-17 is slated to supersede the AKS-74U rifle adopted for service in 1979.

- In June 2024, Israel Weapon Industries (IWI) received a contract from Israel Defense Forces (IDF) for the supply of thousands of Israeli-made Micro Tavor (X95) assault rifles. The current order is for the 5.56x45mm caliber Micro TAVOR with barrel lengths of 380mm and 419mm.

- In November 2024, Sig Sauer partnered with Nibe Group to manufacture assault rifles in India. The company aims to start producing a complete product in India by 2025. This will cater to the Indian Ministry of Defence and Ministry of Home Affairs.

- In August 2024, Sig Sauer secured a repeat contract from the India Army to provide 73,000 SIG716 rifles. The deliveries of these assault weapons are expected to be completed by end-2025.

REPORT COVERAGE

The report provides a detailed analysis of the sector and focuses on important aspects such as key players, technology, application, depending on various regions. Moreover, the research report offers deep insights into the market trends, competitive landscape, market competition, and market share and market status and highlights key industry developments. Additionally, it encompasses several direct and indirect factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 5.68% from 2026 to 2034 |

|

Segmentation

|

By Caliber

|

|

By Rifle Configuration

|

|

|

By Firing Mode

|

|

|

By Range

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 8.38 billion in 2026 and is projected to reach USD 13.05 billion by 2034.

Registering a CAGR of 5.68%, the market will exhibit significant growth during the forecast period.

By caliber, the 5.56 x 45 mm NATO segment leads the market.

Kalashnikov Concern JSC (Russia), Heckler & Koch (Germany), Colt Manufacturing (U.S.), and Israel Weapon Industries (IWI) (Israel) are some of the leading players in the market.

North America dominates the market in terms of share.

In 2025, the market value stood at USD 3.26 billion.

The key factors driving the market rise in increase in defense budget & military modernization programs.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us