Atomic Clock Market Size, Share, Industry and Russia-Ukraine War Analysis, By Platform (Satellite Systems, Ground Control & Reference Stations, Aircraft & UAVs, Missile & Weapon Guidance Systems, Naval Systems, and Defense Data Centers & Command Networks), By Technology (Rubidium Atomic Clocks (Rb), Hydrogen Masers, Cesium Beam Standards, Pulsed Optically Pumped (POP) Atomic Clocks, Chip-Scale Atomic Clocks, & Optical Atomic Clocks), By Frequency Stability (Ultra-High Stability, High Stability, Medium Stability/Ruggedized & Others), By Application, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

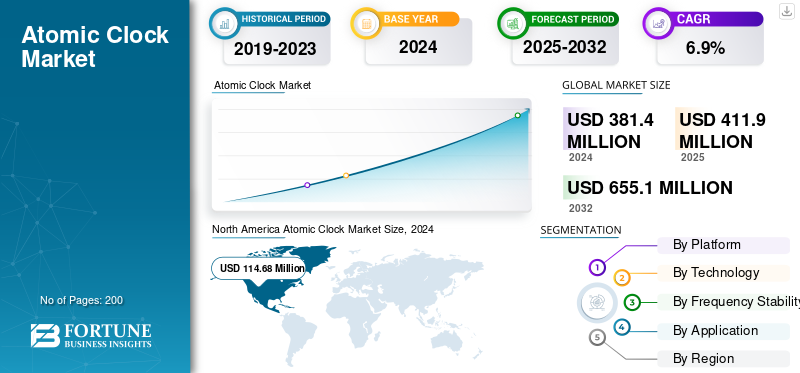

The global atomic clock market size was valued at USD 411.9 million in 2025. The market is projected to grow from USD 444.9 million in 2026 to USD 721.2 million by 2034, exhibiting a CAGR of 6.20% during the forecast period. North America dominated the atomic clock market with a market share of 29.90% in 2025.

The market is evolving rapidly due to the rising need for precision timing in GNSS-denied and data-synchronized combat environments. Military modernization programs emphasize secure PNT capabilities across autonomous systems, missile platforms, and space-based communication constellations. Miniaturized atomic clocks, particularly CSACs and advanced rubidium variants, are enabling field-level synchronization with low power consumption. Meanwhile, quantum and optical atomic clock R&D is gaining traction for future space-grade and long-endurance missions. The market’s trajectory is defined by the convergence of resilience, miniaturization, and autonomy, turning atomic timing from a background component into a frontline defense enabler.

Key participants include Microchip Technology Inc., Orolia (Safran), Oscilloquartz (ADVA Optical Networking), Frequency Electronics Inc., Excelitas Technologies, Spectratime, Stanford Research Systems, and AccuBeat Ltd. These players focus on ruggedized and miniaturized atomic clock solutions for satellite payloads, tactical radios, and navigation systems. Several companies collaborate with national defense agencies and quantum research centers to enhance optical clock stability and radiation tolerance. Emerging entrants in Asia, particularly in Japan, India, and China, are developing indigenous atomic timing modules to reduce import reliance and strengthen sovereign defense infrastructure.

Download Free sample to learn more about this report.

ATOMIC CLOCK MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 411.9 Million

- 2026 Market Size: USD 444.9 Million

- 2034 Forecast Market Size: USD 721.2 Million

- CAGR: 6.20% from 2026–2034

- North America dominated the atomic clock market with a 29.90% share in 2025.

- The satellite systems segment is projected to lead with a 31.07% market share in 2026.

- The rubidium atomic clocks (Rb) segment is expected to hold a 36.42% market share in 2026.

North America

North America generated USD 122.99 million in 2025, driven by defense modernization, GNSS resilience initiatives, and advanced timing infrastructure investments.

Europe

Europe held a 21.30% market share in 2025, benefiting from satellite navigation projects and indigenous atomic clock development efforts.

Asia Pacific

Asia Pacific accounted for 27.40% of global revenue in 2025, supported by expanding satellite navigation programs and rising defense-space investments.

U.S.

The market is projected to reach USD 121.66 million in 2026, supported by GNSS-independent PNT programs, defense projects, and satellite deployments.

Japan

The market is expected to reach USD 29.85 million in 2026, driven by investments in satellite navigation systems and advanced timing technologies.

Read More

RUSSIA-UKRAINE WAR IMPACT

Russia-Ukraine War Accelerates Demand for GNSS-Resilient and Locally Synchronized Timing Systems

The Russia-Ukraine conflict has redefined how nations perceive timing security in modern warfare. As both sides engage in extensive GNSS jamming and spoofing, global defense agencies are now prioritizing resilient, onboard atomic clock systems to sustain PNT (Positioning, Navigation, and Timing) accuracy under electronic warfare conditions. The war exposed that reliance on external satellite signals makes forces vulnerable to disruption. Consequently, NATO members and neighboring European countries have fast-tracked the adoption of chip-scale atomic clocks (CSACs), rubidium standards, and terrestrial timing infrastructures to maintain operational synchronization in contested zones. Demand has surged for deployable, GNSS-independent timing systems across missile guidance, ISR drones, and communications networks. The conflict also spurred diversification away from Russian suppliers, with production shifting toward the U.S., French, Japanese, and Israeli manufacturers, driving a structural rebalancing of the defense timing technology landscape.

ATOMIC CLOCK MARKET TRENDS

Transition Toward Miniaturized, Network-Synchronized Clocks to Accentuate Market Trend

The dominant trend shaping the atomic clock market is the shift toward miniaturization, SWaP-optimized CSACs, and network-synchronized timing ecosystems. Armed forces are embedding atomic clocks directly into field-deployable equipment radios, drones, missile seekers, and autonomous ground systems to maintain precision when GNSS signals are compromised. Parallel to this, space-based atomic clock deployment is increasing sharply, with LEO satellite constellations integrating rubidium and cesium variants for secure communications and resilient navigation. Another key trend is the convergence of atomic timing with quantum sensing and AI-based clock stabilization, allowing better frequency prediction and drift compensation. The broader ecosystem is moving toward distributed timing networks, where multiple portable atomic clocks synchronize through resilient mesh architectures. This reduces single-point timing failures and enhances coordinated strike or surveillance accuracy. Overall, the trend is a clear evolution from centralized, bulky time references to agile, secure, and edge-deployable precision timing nodes.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Secure, GNSS-Resilient PNT Capabilities to Boost Market Growth

A primary driver for the atomic clock market is the escalating requirement for secure and resilient PNT capabilities across all military domains: air, space, land, and sea. Modern warfare increasingly depends on synchronized data and sensor fusion, where a microsecond drift can compromise ISR, targeting, or encrypted communications. Atomic clocks deliver this stability and are indispensable to GNSS backup architectures and space-based navigation systems. As adversarial electronic warfare tactics grow in sophistication, countries are prioritizing GNSS independence by deploying localized atomic timing references. Defense modernization initiatives in the U.S., India, the U.K., and Japan are mandating integration of CSACs and rubidium clocks into field systems and LEO platforms. The emergence of hybrid clock systems combining quartz, rubidium, and CSAC synchronization further amplifies adoption. The convergence of space, quantum, and AI timing stabilization is amplifying demand, positioning atomic clocks as the cornerstone of next-gen defense infrastructure.

MARKET RESTRAINTS

High Production Complexity and Cost Barriers to Hamper Market Growth

Despite rising demand, the atomic clock market share faces notable restraints stemming from manufacturing complexity, cost, and supply-chain constraints. Manufacturing high-stability rubidium or cesium standards demands ultra-clean environments, precision optics, and vacuum systems, limiting scalability and vendor diversity. CSACs, though miniaturized, remain expensive due to microfabrication precision, limiting adoption in cost-sensitive programs or small defense contracts. Supply-chain dependencies on specialized materials (e.g., rubidium isotopes and vacuum-grade quartz) further expose vulnerabilities, particularly under geopolitical tensions. Moreover, export regulations and ITAR controls hinder international collaborations and cross-border sales, restricting global deployment. Another restraint is the long qualification cycle for space or defense-grade timing devices, often extending 3-5 years before field certification. Combined, these constraints slow down adoption, deter new entrants, and preserve the dominance of a few high-capability suppliers, creating structural bottlenecks in meeting fast-growing global demand.

MARKET OPPORTUNITIES

GNSS-Independent PNT Systems and Quantum Timing Initiatives to Accentuate Market Growth

The strongest opportunity lies in the global transition toward GNSS-independent PNT architectures, driven by defense resilience mandates and commercial satellite modernization. Countries are actively investing in terrestrial timing networks, sovereign navigation satellites, and quantum clock R&D to achieve strategic autonomy. Optical lattice and cold-atom clock technologies, once confined to labs, are now entering military-grade prototypes with stability magnitudes higher than rubidium or cesium systems. The U.S., U.K., and Japan are allocating billions into quantum-timing R&D through DARPA and national space programs. India and France are funding indigenous atomic clock facilities for missile and satellite programs. Private aerospace entrants, including those in NewSpace sectors, also represent new buyers—embedding precision clocks in cubesats for time-tagging Earth observation and ISR data. With GNSS denial becoming a defining element of modern warfare, the opportunity extends beyond defense to telecom, power grid, and financial networks, all seeking ultra-stable, local atomic references to sustain operations in isolation.

MARKET CHALLENGES

Balancing SWaP Optimization with Ultra-Stability are Major Challenges in the Market

The key challenge for the atomic clock market growth is balancing miniaturization (SWaP-C) with long-term frequency stability and radiation tolerance. As defense systems migrate to smaller platforms, UAVs, nanosatellites, and portable C2 modules, designers face trade-offs between size, power consumption, and precision. Current CSACs, while compact, cannot match the stability of laboratory-grade optical or cesium clocks. Achieving quantum-level performance within field-deployable units demands breakthroughs in photonics integration, vacuum-free atomic cells, and AI-based drift correction. Additionally, the radiation-hardening of optical components for space remains a technological hurdle. There is no universally accepted defense-grade certification for CSACs, leading to interoperability gaps across systems. Finally, talent shortages in atomic and quantum timing physics constrain innovation speed. Overcoming these challenges requires multi-national collaboration between defense primes, quantum research labs, and semiconductor manufacturers to produce next-generation, robust, and scalable atomic clock solutions.

SEGMENTATION ANALYSIS

By Platform

Rising LEO and MEO Constellations Drive Satellite Systems Segment Growth

By platform, the market is segmented into satellite systems, ground control & reference stations, aircraft & UAVs, missile & weapon guidance systems, naval systems, and defense data centers & command networks.

The satellite systems segment captured the largest share of the market in 2024 and is anticipated to dominate with a 31.07% market share in 2026. Demand for satellite systems is increasing as countries expand LEO and MEO constellations for communications, ISR, and navigation. Each satellite requires high-stability onboard atomic clocks for synchronization and signal integrity. Defense and commercial missions now prioritize radiation-hardened, low-drift timing modules to ensure reliability in orbit and autonomous space operations.

The aircraft & UAVs segment is expected to grow at a CAGR of 8.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Rising Adoption of Rubidium Clocks for Defense-Grade Precision and Reliability Drives Segment Growth

The technology segment is classified into rubidium atomic clocks (Rb), hydrogen masers, cesium beam standards, Pulsed Optically Pumped (POP) atomic clocks, Chip-Scale Atomic Clocks (CSACs), and optical atomic clocks (Emerging).

In 2024, the rubidium atomic clocks (Rb) segment dominated by capturing the largest market share and is anticipated to dominate with a 36.42% share in 2026. These atomic clocks are in strong demand for missile guidance, radar, and military satellite payloads, offering a superior balance between stability, size, and cost. Their proven reliability and compact footprint make them ideal for rugged aerospace environments where long-term frequency accuracy and low maintenance are critical.

The Pulsed Optically Pumped (POP) atomic clocks segment is expected to grow at a CAGR of 7.8% over the forecast period.

By Frequency Stability

Defense Platforms Requiring Ruggedized Timing for Harsh Environments Boost Segment Growth

The frequency stability segment is categorized into ultra-high stability, high stability, medium stability/ruggedized, and prototype/experimental optical clocks.

The medium stability/ruggedized segment captured the largest market share in 2025 and will dominate in 2026 with a 36.91% market share. Medium stability and ruggedized atomic clocks are witnessing demand from battlefield, naval, and aerospace systems operating under temperature, shock, and vibration extremes. These clocks deliver operational consistency and secure synchronization across mobile command units, drones, and EW systems where durability and moderate precision outperform ultra-high-cost lab-grade models.

The high stability segment is expected to grow at a CAGR of 7.2% during the forecast period.

By Application

GNSS Segment Dominates Due to Rising Demand for Secure and Resilient Positioning Systems

By application, the market is classified into satellite navigation (GNSS), Electronic Warfare (EW) & Signals Intelligence (SIGINT), communication & command systems, radar systems, Inertial Navigation Systems (INS) augmentation, space exploration & scientific missions, and defense metrology & calibration.

The satellite navigation (GNSS) segment will lead the market with a 30.65% market share and attained the largest share of the market in 2026. Demand for the satellite navigation (GNSS) segment is surging as militaries and aerospace agencies confront jamming and spoofing threats. Atomic clocks are embedded in GNSS satellites and receivers ensure signal continuity and positional accuracy in degraded environments, forming the backbone of sovereign, GNSS-independent navigation and timing networks worldwide.

The Inertial Navigation Systems (INS) augmentation segment is expected to grow at a CAGR of 7.8% over the forecast period.

ATOMIC CLOCK MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the rest of the world.

North America Atomic Clock Market Size, 2026 (USD Million) To get more information on the regional analysis of this market, Download Free sample

North America

The North America market was valued at USD 122.99 Million in 2025, capturing 29.90% of global revenue, and is estimated to reach USD 131.89 Million in 2026. The region’s demand is driven by large-scale defense modernization programs, satellite navigation upgrades, and GNSS resilience initiatives. Government agencies and defense organizations continue investing in advanced atomic clock technologies to strengthen secure communications, intelligence systems, and precision timing infrastructure. The U.S. market is projected to reach USD 121.66 Million in 2026, supported by GNSS-independent positioning, navigation, and timing (PNT) programs, advanced defense projects, and expanding satellite deployments.

Europe

In 2025, Europe held 21.30% of the global market, reaching a valuation of USD 87.60 Million, and is projected to grow to USD 92.50 Million in 2026. Regional growth is supported by satellite navigation initiatives, timing infrastructure upgrades, and increasing investments in defense-space collaboration. Countries across Europe continue to focus on indigenous atomic clock development and next-generation timing technologies to reduce dependence on external navigation and synchronization systems. The U.K. market is projected to reach USD 21.53 Million in 2026, while Germany is expected to reach USD 19.28 Million.

Asia Pacific

The market in Asia Pacific reached USD 113.00 Million in 2025, representing 27.40% of total market revenue, and is projected to reach USD 125.30 Million in 2026. Growth is driven by expanding satellite navigation programs, indigenous atomic clock manufacturing initiatives, and rising investments in defense and space technologies. Governments across the region are prioritizing research and development for advanced timing systems used in satellite payloads, missile guidance, and secure communications. The China market is projected to reach USD 47.80 Million in 2026, while Japan and India are expected to reach USD 29.85 Million and USD 21.88 Million, respectively.

Rest of the World

The Rest of the World market generated USD 88.30 Million in 2025, contributing 21.43% to global market revenue, and is projected to grow to USD 95.20 Million in 2026. Demand is increasing across the Middle East, Africa, and Latin America due to growing investments in defense modernization, secure communication infrastructure, aerospace programs, and satellite-based technologies. Countries in these regions are increasingly adopting advanced atomic clock solutions to improve operational autonomy, navigation accuracy, and secure timing synchronization capabilities.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Established Defense and Space Timing Leaders Shaping the Future of Atomic Clock Technology

The atomic clock market is concentrated by a group of highly specialized players focused on advancing timing precision, miniaturization, and GNSS resilience. These include Microchip Technology Inc. (U.S.), Safran (France), Leonardo S.p.A. (Italy), AccuBeat Ltd. (Israel), Oscilloquartz (Switzerland), Stanford Research Systems (U.S.), Meinberg GmbH & Co. KG (Germany), IQD Frequency Products (U.K.), and CETC – China Electronics Technology Group (China). These companies are advancing rubidium, cesium, and chip-scale atomic clock technologies for applications in satellites, defense communications, and missile navigation systems, enabling countries to achieve GNSS-independent, secure, and synchronized operations in contested electronic environments.

LIST OF KEY ATOMIC CLOCK COMPANIES PROFILED

- Microchip Technology Inc. (U.S.)

- Safran (France)

- Leonardo S.p.A. (Italy)

- AccuBeat Ltd. (Israel)

- Oscilloquartz (Switzerland)

- Stanford Research Systems (U.S.)

- Meinberg GmbH & Co. KG (Germany)

- IQD Frequency Products (U.K.)

- CETC – China Electronics Technology Group (China)

- India Space Research Organization (India)

KEY INDUSTRY DEVELOPMENTS

- September 2025 - The Hong Kong Observatory (HKO) and the National Time Service Center (NTSC) of the Chinese Academy of Sciences formalized their initial cooperation agreement at the HKO Headquarters. It is aimed to improve collaboration in time measurement, timekeeping, and time services, along with the sharing of relevant experiences and technologies.

- September 2024 - The Australian Government is procuring quantum optical atomic clocks from QuantX Labs, located in Adelaide, to provide Position Navigation and Timing (PNT) capabilities for the Australian Defence Force (ADF). Two contracts totaling USD 2.7 million will allow AUKUS partners to advance PNT capabilities, thereby supporting improved decision-making advantages and heightened maritime domain awareness, which are essential goals outlined in AUKUS Pillar II.

- September 2024 - QuantX Labs, a mid-sized Australian firm, announced its first sales of cutting-edge optical atomic clocks, securing two Department of Defence contracts with the Commonwealth of Australia worth more than USD 2.7 million in total.

- April 2024 - ColdQuanta, a leader in the global quantum ecosystem, has announced a collaboration with LocatorX, the most innovative location tracking company in the world, to enhance the development of atomic clocks. This strategic alliance will allow both companies to collaboratively tackle a broader spectrum of atomic clock applications by integrating ColdQuanta's exceptional team and technology with LocatorX's cost-effective, compact, low-power atomic clocks.

- March 2024 - The European Space Agency (ESA), representing the European Commission, has entered into a contract worth USD 13 million with Leonardo S.p.A (Italy) and the Istituto Nazionale di Ricerca Metrologica to create and advance a new ultra-precise atomic clock technology intended for the Galileo system.

REPORT COVERAGE

The research report regarding the expansion of the atomic clock market provides an in-depth analysis by identifying key companies, product categories, and main applications within the industry. Additionally, the report highlights market trends and notable developments in this field. In conjunction with the aforementioned aspects, the report includes several factors that have contributed to the rapid market growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.20% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Platform

|

|

By Technology

|

|

|

By Frequency Stability

|

|

|

By Application

|

|

|

By Geography North America (By Platform, Technology, Frequency Stability, and Application)

Europe (By Platform, Technology, Frequency Stability, and Application)

Asia Pacific (By Platform, Technology, Frequency Stability, and Application)

Rest of the World (By Platform, Technology, Frequency Stability, and Application)

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 411.9 million in 2025 and is estimated to reach USD 721.2 million by 2034.

The market is growing at a CAGR of 6.20% during the projection period (2026-2034).

By technology, the rubidium atomic clocks (Rb) segment leads the global market.

Satellite systems is the leading sub-segment of the global market.

Microchip Technology Inc. (U.S.), Safran (France), Leonardo S.p.A. (Italy), AccuBeat Ltd. (Israel), Oscilloquartz (Switzerland), and Stanford Research Systems (U.S.) are some of the leading companies.

North America is projected to capture the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us