Automotive Airbag Fabric Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback & Sedans, SUVs, LCVs, HCVs), By Vehicle Propulsion (ICE and Electric), By Material Type (Nylon 6,6 (PA66), Nylon 6 (PA6), Polyester (PET), and Others), By Coating Type (Uncoated, Silicone-coated, Neoprene-coated, and Other Coatings), By Airbag Type (Front Airbag, Side Airbag, Curtain Airbag, Knee Airbag, and Far-side Airbag), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

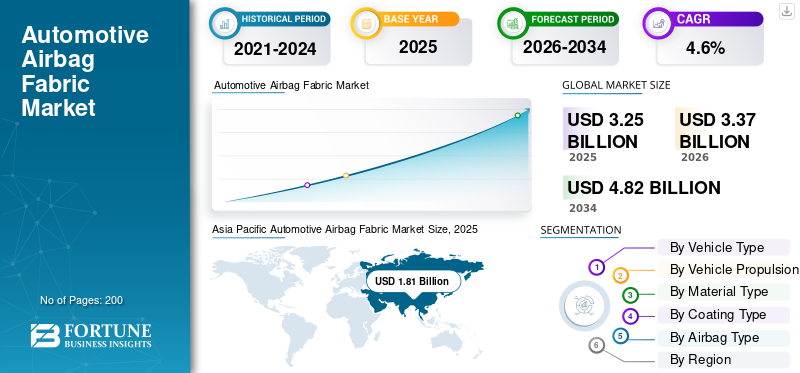

The global automotive airbag fabric market size was valued at USD 3.25 billion in 2025. The market is projected to grow from USD 3.37 billion in 2026 to USD 4.82 billion by 2034, exhibiting a CAGR of 4.6% during the forecast period. Asia Pacific dominated the global automotive airbag fabric market with a market share of 55.69% in 2025.

Automotive airbag fabric is a high-strength, tightly woven textile used in vehicle airbags, designed to withstand rapid inflation, control gas flow, and ensure reliable occupant protection during collisions. The market is driven by rising vehicle production, stricter safety regulations, increasing airbag installation across vehicle types, growing consumer safety awareness, electric vehicle adoption, and technological advancements in high-strength, lightweight, and durable textile materials.

- In July 2025, Hyosung Advanced Materials restructured its North American airbag unit to expand manufacturing and sales of airbag cushions and fabrics, aiming to strengthen local supply and customer responsiveness.

Furthermore, major players such as Toyoda Gosei, Autoliv, Hyosung, Toray Industries, and Kolon Industries are focusing on capacity expansion, lightweight fabric development, and sustainability initiatives using recycled yarns and advanced coating technologies to meet evolving automotive safety regulations and OEM performance requirements.

Download Free sample to learn more about this report.

Automotive Airbag Fabric Market Key Takeaways

- 2025 Market Size: USD 3.25 billion

- 2026 Market Size: USD 3.37 billion

- 2034 Forecast Market Size: USD 4.82 billion

- CAGR: 4.6% from 2026-2034

- Asia Pacific dominated the automotive airbag fabric market with a 55.69% share in 2025.

- The SUVs segment is projected to register the fastest growth at a CAGR of 5.3% during the forecast period.

- The electric vehicle segment is expected to grow at the highest CAGR of 7.4% during the forecast period.

Asia Pacific

Asia Pacific accounted for USD 1.81 billion in 2025 and is projected to reach USD 1.90 billion in 2026.

Europe

Europe is expected to reach USD 0.67 billion in 2026, supported by strong vehicle safety standards.

North America

North America is projected to reach USD 0.67 billion in 2026, maintaining its position as the third-largest regional market.

U.S.

The market is estimated to reach USD 0.44 billion in 2026, accounting for around 13.1% of global sales.

Germany

The automotive airbag fabric market is projected to reach USD 0.16 billion in 2026, representing around 4.8% of global sales.

Read More

AUTOMOTIVE AIRBAG FABRIC MARKET TRENDS

Shift Toward Lightweight and Sustainable Airbag Fabric Materials

One of the key market trends is the increasing focus on lightweight and sustainable, and eco-friendly materials. Automakers and suppliers are exploring recycled nylon yarns, bio-based fibers, and optimized fabric constructions to reduce vehicle weight and environmental impact. At the same time, advanced silicone coating techniques are being adopted to replace traditional coatings, improving flexibility, heat resistance, and recyclability. This trend aligns with broader automotive sustainability goals and regulatory pressure to lower vehicle emissions and lifecycle environmental footprints.

- In September 2024, Autoliv introduced airbag cushions using 100% recycled polyester, validating recycled yarn-and-fabric pathways that lower emissions while keeping deployment performance, enabling greener sourcing strategies worldwide at scale today.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Stricter Vehicle Safety Regulations Accelerate Adoption of Advanced Airbag Fabrics

Stringent vehicle safety regulations across the globe are a key driver for the market. Governments and safety agencies are mandating higher crash-test performance standards, requiring wider installation of front, side, curtain, and knee airbags across vehicle categories. Regulations such as Euro NCAP, FMVSS, and China NCAP are continuously tightening occupant protection requirements, compelling automakers to use high-performance airbag fabrics with superior strength, tear resistance, and deployment reliability. This regulatory push ensures consistent demand for advanced woven and coated airbag textiles across both mature and emerging automotive markets.

- In November 2025, India’s government unveiled tougher Bharat NCAP 2.0 crash-test protocols, adding full-frontal and rear-impact tests, raising five-star requirements, and pushing OEMs toward more airbags and higher-grade fabrics.

MARKET RESTRAINTS

High Capital and Certification Costs Limit Rapid Market Expansion

A major restraint in the market is the high capital investment required for advanced weaving equipment, coating technologies, and rigorous safety testing. Airbag fabrics must meet strict quality, durability, and deployment standards, necessitating expensive certification processes and continuous compliance audits. Smaller textile manufacturers often struggle to enter the market due to high entry barriers and long qualification cycles with OEMs and airbag module suppliers. These factors limit supplier diversification and slow capacity expansion, particularly in cost-sensitive and emerging markets.

MARKET OPPORTUNITIES

Rising Electric Vehicle Production Creates New Design Opportunities

The rapid growth of electric vehicle production presents a strong opportunity for automotive airbag fabric manufacturers. EV-specific vehicle architectures, flat-floor designs, and altered crash structures require redesigned restraint systems and customized airbag fabrics. This creates demand for lightweight, high-tenacity fabrics that enhance energy absorption while supporting overall vehicle weight reduction. Additionally, EV safety concerns related to battery protection and cabin layout are driving innovation in curtain and side airbag applications. Suppliers that invest in EV-oriented fabric solutions can secure long-term partnerships with automakers.

- For instance, according to IEA, Global electric car production reached 17.3 million units in 2024, rising about 25% year-on-year, driven mainly by China, where output increased to 12.4 million electric vehicles.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Price Fluctuations Pose Risks

The market faces challenges from supply chain disruptions and volatile raw material prices, particularly for high-tenacity nylon yarns and specialty coatings. Geopolitical tensions, trade restrictions, and energy price fluctuations can impact material availability and production costs. Since airbag fabrics are safety-critical components, manufacturers must maintain consistent quality while managing cost pressures. Any disruption can delay OEM production schedules, increasing operational risks and margin pressure for airbag fabric suppliers operating in global markets.

Segmentation Analysis

By Vehicle Type

SUVs Lead Market Due to Their Higher Global Production Volumes

Based on vehicle type, the market is segmented into hatchback & sedans, SUVs, LCVs, and HCVs.

SUVs dominate and represent the fastest-growing segment due to their higher global production volumes and elevated safety content per vehicle. SUVs typically incorporate multiple airbags, including side and curtain airbags, increasing demand for airbag fabric per unit compared to other vehicle types. Rising consumer preference for SUVs across developed and emerging markets, coupled with stricter crash safety norms, is further boosting adoption. Additionally, electric SUV launches are accelerating the automotive airbag fabric market growth, as enhanced occupant protection requirements drive advanced airbag system integration.

- In November 2025, Kia launched the 2026 Seltos with upgraded ADAS, six airbags standard, larger infotainment displays, connected car software, OTA updates, improved powertrain calibration, and enhanced safety electronics architecture.

The SUVs segment is anticipated to be the fastest growing, registering a CAGR of 5.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Propulsion

Large Installed Base and High Production Volumes Sustain ICE Segment Dominance

Based on vehicle propulsion, the market is segmented into ICE and electric.

ICE vehicles dominate the market due to their significantly larger global vehicle parc and sustained production volumes, especially across emerging economies. Most ICE passenger and commercial vehicles are equipped with multiple airbags to meet long-established safety regulations, ensuring stable, high-volume demand for airbag fabrics. Additionally, ongoing model refresh cycles and incremental safety upgrades in ICE platforms continue to drive fabric consumption. While electrification is rising, ICE vehicles will remain the primary demand contributor in the medium term.

- In December 2025, Maruti Suzuki made six airbags standard across all Fronx variants, strengthening passive safety, meeting upcoming regulations, and enhancing occupant protection through improved restraint systems and crash safety compliance.

The electric vehicle emerged as the fastest-growing segment, registering a CAGR of 7.4% over the forecast period.

By Material Type

Superior Strength and Thermal Stability Drive Nylon 6,6 (PA66) Segment Leadership

Based on material type, the market is segmented into Nylon 6,6 (PA66), Nylon 6 (PA6), Polyester (PET), and others.

The Nylon 6,6 (PA66) segment dominates due to its high tensile strength, excellent heat resistance, and superior air permeability control, which are critical for reliable airbag deployment. PA66 offers consistent performance under extreme inflation temperatures and pressures, making it the preferred choice for frontal, side, and curtain airbags. Its proven durability, regulatory acceptance, and compatibility with advanced coating technologies further reinforce widespread adoption across global automotive platforms.

- In April 2023, Toyota Tsusho planned to commence nylon airbag scrap recycling at a Vietnam airbag plant, using Refinverse technology to create recycled resin and cut CO₂ versus virgin nylon.

The polyester (PET) segment is anticipated to register a CAGR of 6.2% over the forecast period.

By Coating Type

Enhanced Heat Resistance and Deployment Reliability Boost Silicone-Coated Fabric Dominance

Based on coating type, the market is segmented into uncoated, silicone-coated, neoprene-coated, and other coatings.

Silicone-coated fabrics dominate due to their superior heat resistance, flexibility, and controlled gas permeability during rapid airbag deployment. Silicone coatings enhance fabric durability, reduce aging effects, and support consistent inflation performance across varying temperatures. Additionally, they are lighter and more environmentally friendly than traditional neoprene coatings, aligning with automakers’ sustainability goals. Their compatibility with advanced airbag designs, including side and curtain airbags, further drives widespread adoption.

The uncoated segment is anticipated to be the fastest-growing, registering a CAGR of 5.2% over the forecast period.

By Airbag Type

Expanding Side-Impact Protection and Regulatory Focus Drive Curtain Airbag Dominance

Based on airbag type, the market is segmented into front airbag, side airbag, curtain airbag, knee airbag, and far-side airbag.

Curtain airbags dominate due to their critical role in protecting occupants during side impact and rollover crashes. Increasing regulatory emphasis on side-impact safety, coupled with higher adoption of multi-airbag systems including various types of airbags in passenger vehicles and SUVs, is driving demand for curtain airbags. These airbags require larger fabric surface areas and high-strength materials, resulting in higher airbag fabric consumption per vehicle. Growing consumer awareness and stricter crash test standards further support segment leadership.

- In October 2024, Toyoda Gosei launched a compact curtain airbag for sports coupes, using optimized fabric folding and deployment technology to improve head protection while fitting low-roof vehicle designs.

The far-side airbag segment is anticipated to be the fastest growing, registering a CAGR of 7.2% over the forecast period.

Automotive Airbag Fabric Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Automotive Airbag Fabric Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant automotive airbag fabric market share in 2025 with USD 1.81 billion and is expected to reach a valuation of USD 1.90 billion in 2026. Rising vehicle production, expanding middle-class demand, tightening safety regulations, and growing adoption of airbags in entry-level vehicles across China, India, and Southeast Asia drive the market. The region is also anticipated to grow at the fastest-growing CAGR of 6.5% over the forecast period.

China Automotive Airbag Fabric Market

Based on Asia Pacific’s strong contribution and China's dominance within the region, the China market can be analytically approximated at around USD 1.11 billion in 2026, accounting for roughly 33.0% of global Automotive Airbag Fabric sales.

Europe

Europe is expected to witness moderate growth in this market space during the forecast period. The European market is set to reach a valuation of USD 0.67 billion in 2026. Strict Euro NCAP standards, high focus on occupant protection, strong premium vehicle manufacturing, and rapid adoption of advanced airbag systems support sustained market growth.

U.K Automotive Airbag Fabric Market

The U.K. market in 2026 is estimated at around USD 0.04 billion, representing roughly 1.1% of global automotive airbag fabric revenues.

Germany Automotive Airbag Fabric Market

Germany’s market is projected to reach approximately USD 0.16 billion in 2026, equivalent to around 4.8% of global automotive airbag fabric sales.

North America

North America is estimated to reach USD 0.67 billion in 2026 and secure the position of the third-largest region in the market. The market is driven by stringent vehicle safety regulations, high airbag penetration across vehicle segments, strong SUV sales, and continuous adoption of advanced restraint and safety technologies by leading automotive OEMs.

U.S. Automotive Airbag Fabric Market

The U.S dominated the region, and is estimated to reach USD 0.44 billion in 2026, representing around 13.1% of the global sales. Growth is supported by federal safety mandates, large passenger vehicle production, high consumer safety awareness, and increasing integration of curtain and side airbags in mass-market vehicles.

Rest of the World

Rest of the World, comprising South America and the Middle East & Africa, is projected to record a growth rate of 4.8% in the coming years, which is the second highest among all regions, and reach a valuation of USD 0.14 billion by 2026. Market growth is driven by gradual safety regulation enforcement, increasing vehicle assembly activities, rising consumer safety awareness, and improving automotive manufacturing infrastructure in developing regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Capacity Expansion, Material Innovation, and OEM Partnerships Define Automotive Airbag Fabric Competition

The automotive airbag fabric market is shaped by continuous material innovation, large-scale capacity expansion, and long-term partnerships with airbag module suppliers and OEMs. Key players such as Toyoda Gosei, Autoliv, Hyosung, Toray Industries, and Kolon Industries compete through high-tenacity yarn development, advanced weaving and silicone-coating technologies, and stringent quality control systems. Companies are strengthening competitiveness by localizing production near OEM hubs, improving cost efficiency through automation, and developing lightweight and sustainable fabric solutions.

- In April 2023, Autoliv announced it would build its first Vietnam airbag cushion and fabric plant using Manufacturing 4.0 concepts, responding to customer demand and expanding regional textile capacity.

LIST OF KEY AUTOMOTIVE AIRBAG FABRIC COMPANIES PROFILED

- Global Safety Textiles (Hyosung Advanced Materials) (South Korea)

- Autoliv, Inc. (Sweden)

- Joyson Safety Systems (U.S.)

- Toyoda Gosei Co., Ltd. (Japan)

- Toray Industries, Inc. (Japan)

- Kolon Industries, Inc. (South Korea)

- Teijin Limited (Japan)

- Asahi Kasei Corporation (Japan)

- Milliken & Company (U.S.)

- HMT (Xiamen) New Material Technology Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Kolon Industries announced a 70-billion-won investment to build an airbag fabric plant in Ho Chi Minh City, adding weaving, processing, and coating to supply Autoliv from 2028.

- September 2025: Toyota Kirloskar Motor made six airbags standard across all Toyota Rumion variants, adding curtain protection and boosting per-vehicle airbag fabric consumption in India’s MPV segment nationwide rapidly.

- September 2025: Volvo Trucks North America made integrated side-curtain airbags standard on new VNL and VNR models, expanding curtain-airbag applications and demand for coated, high-tenacity textile cushions for fleets.

- July 2025: Hyosung Advanced Materials restructured its North American airbag unit to expand manufacturing and sales of airbag cushions and fabrics, aiming to strengthen local supply and customer responsiveness.

- October 2024: Toyoda Gosei expanded its Neemrana, India, facility and began production in a new building to meet rising airbag demand under stricter safety regulations, supporting regional sourcing needs.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Vehicle Propulsion, Airbag Type, Material Type, Coating Type, and Region |

|

By Vehicle Type |

· Hatchback & Sedans · SUVs · LCVs · HCVs |

|

By Vehicle Propulsion |

· ICE · Electric |

|

By Material Type |

· Nylon 6,6 (PA66) · Nylon 6 (PA6) · Polyester (PET) · Others |

|

By Coating Type |

· Uncoated · Silicone-coated · Neoprene-coated · Other Coatings |

|

By Airbag Type |

· Front Airbag · Side Airbag · Curtain Airbag · Knee Airbag · Far-side Airbag |

|

By Region |

· North America (By Vehicle Type, Vehicle Propulsion, Airbag Type, Material Type, Coating Type, and Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, Vehicle Propulsion, Airbag Type, Material Type, Coating Type, and Country/Sub-region) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, Vehicle Propulsion, Airbag Type, Material Type, Coating Type, and Country/Sub-region) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, Vehicle Propulsion, Airbag Type, Material Type, Coating Type) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.25 billion in 2025 and is projected to reach USD 4.82 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 1.81 billion.

The market is expected to exhibit a CAGR of 4.6% during the forecast period of 2026-2034.

By vehicle type, the SUVs segment is expected to lead the market.

Stricter vehicle safety regulations accelerate the adoption of advanced airbag fabrics.

Toyoda Gosei, Autoliv, Hyosung, Toray Industries, and Kolon Industries are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us