Automotive Ball Joint and Steering Linkage Market Size, Share & Industry Analysis, By Product Type (Ball Joints and Steering Linkage), By Sales Channel (OEM and Aftermarket), By Steering Architecture (Rack & Pinion and Recirculating Ball), By Propulsion (ICE and Electric), By Material Type (Steel and Aluminum), By Manufacturing Process (Forging and Casting), By Vehicle Type (Passenger Cars, Light Commercial Vehicles and Heavy Commercial Vehicles) and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

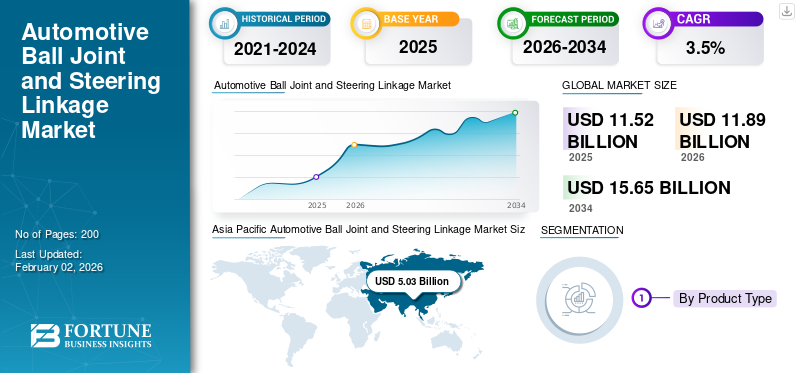

The global automotive ball joint and steering linkage market size was valued at USD 11.52 Billion in 2025. The market is projected to grow from USD 11.89 Billion in 2026 to USD 15.65 Billion by 2034, exhibiting a CAGR of 3.5% during the forecast period. Asia Pacific dominated the global market with a market share of 43.66% in 2025.

The market represents a critical segment of the vehicle chassis and steering system industry. Ball joints and steering linkages connect suspension and steering components, allowing smooth wheel movement while maintaining vehicle stability, alignment and directional control. These components play a vital role in comfort and safety, particularly during cornering, braking and uneven road conditions, making them essential across all passenger vehicles and commercial vehicle platforms.

Market expansion is closely linked to rising vehicle parc, increasing market growth in emerging economies, and the continued dominance of passenger cars and light commercial vehicles. This growth is further supported by replacement demand, as ball joints and steering linkages are wear-and-tear components requiring periodic replacement over a vehicle’s lifecycle. This factor significantly contributes to the global automotive ball joint demand beyond new vehicle production.

Over the forecast period, the market is expected to evolve through material innovation and design improvements aimed at enhanced durability and reduced maintenance. Manufacturers such as ZF Friedrichshafen, Bosch and Schaeffler are focusing on corrosion-resistant coatings, optimized load-bearing designs and lightweight materials to meet rising consumer preference for longer-lasting and cost effective components. The shift toward advanced suspension architectures and steering precision is also driving increased demand for high-quality linkage systems.

Additionally, stricter safety regulations and rising demand for advanced vehicle handling systems are strengthening the importance of reliable steering components. As a result, the market continues to expand steadily across the globe, supported by both OEM installations and strong aftermarket activity.

Download Free sample to learn more about this report.

Automotive Ball Joint and Steering Linkage Market KEY TAKEAWAYS

- 2025 Market Size: USD 11.52 billion

- 2026 Market Size: USD 11.89 billion

- 2034 Forecast Market Size: USD 15.65 billion

- CAGR: 3.5% from 2026–2034

- Asia Pacific dominated the global market with a market share of 43.66% in 2025.

- The Ball Joints segment is expected to grow at a CAGR of 4.0% over the forecast period.

- The OEM segment is expected to grow at a CAGR of 3.1% over the forecast period.

Asia Pacific

Asia Pacific led the global market owing to strong vehicle production volumes, expanding automotive manufacturing, and increasing demand for passenger vehicles.

North American

North America maintained a significant market position due to rising adoption of advanced steering systems and a strong automotive aftermarket.

Europe

Europe witnessed steady growth, supported by the presence of major automotive manufacturers and increasing investments in vehicle safety technologies

U.S.

The market is driven by robust vehicle sales, growing demand for replacement components, and advancements in steering and suspension systems.

Japan

The market benefits from the country’s strong automotive manufacturing base, technological innovation, and focus on vehicle performance and safety.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Vehicle Parc and Replacement Demand Drive Sustained Market Expansion

The increasing number of vehicles on road directly supports automotive ball joint and steering linkage market growth due to frequent replacement of steering linkages and ball joints. These components experience continuous wear, particularly in passenger vehicles and light commercial vehicles, driving consistent aftermarket demand. Rising focus on comfort and safety further encourages timely replacement, supporting long-term market growth.

- For instance, in 2024, ACEA reported the average age of passenger cars in Europe exceeded 12 years, thus increasing replacement demand for wear-prone steering and suspension components.

MARKET RESTRAINTS

High Price Sensitivity Limits Adoption of Premium Steering Components

Price sensitivity in cost-driven markets restricts adoption of premium ball joints and steering linkages. Many consumers prioritize affordability over longevity, impacting demand for high-performance products. This restraint affects revenue potential despite rising ball joint market size, particularly in developing regions where cost effective solutions dominate.

- For instance, Automotive Service Association publications note that cost-conscious consumers often choose low-priced aftermarket steering parts, limiting adoption of premium ball joints despite durability benefits.

MARKET OPPORTUNITIES

Advancements in Materials Create Opportunities for Longer-Life Components

Innovation in metallurgy and coatings presents strong growth opportunities. Manufacturers developing corrosion-resistant and high-load components can meet rising demand for advanced vehicle performance. Improved materials enhance durability while aligning with consumer preference for reduced maintenance, supporting expansion across the global market.

- For instance, in 2023, Schaeffler highlighted advancements in surface coatings and steel processing to improve fatigue resistance and extend service life of chassis and steering components.

MARKET CHALLENGES

Counterfeit and Low-Quality Products Impact Brand Trust

The presence of counterfeit steering components challenges reputable manufacturers. Low-quality products compromise comfort and safety, affecting consumer confidence and price realization. This challenge limits premium product adoption and impacts organized players despite market growth.

- For instance, the Auto Care Association has warned that counterfeit steering and suspension parts pose safety risks and negatively impact legitimate manufacturers in the global aftermarket.

AUTOMOTIVE BALL JOINT AND STEERING LINKAGE MARKET TRENDS

Growing Shift Toward High-Durability Steering Components is Emerging Market Trend

A key trend reshaping the market is increasing adoption of steering components designed for enhanced durability. OEMs and aftermarket suppliers emphasize longer service intervals to improve ownership experience. This trend supports higher-quality ball joints and steering linkages, strengthening the market growth over the forecast period.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Steering Linkages Dominate Due to Structural Importance in Vehicle Control

On the basis of product type, the market is divided into ball joint and steering linkage.

Steering linkages dominate the market as they directly transmit driver input to wheel movement. Their role in handling, alignment and stability across passenger cars and light commercial vehicles sustains consistent demand.

- For instance, in October 2025, ZF Aftermarket launched TRW’s ‘True Control’ campaign, highlighting safety-critical steering linkage parts (tie rods, drag links, ball joints) and stressing OE-level validation for longevity.

The Ball Joints segment is expected to grow at a CAGR of 4.0% over the forecast period.

By Sales Channel

Aftermarket Segment Leads Market Due to Frequent Replacement Cycles

On the basis of sales channel, the market is segmented into OEM and Aftermarket.

The aftermarket dominates the market as ball joints and linkages require periodic replacement. Aging vehicles and rising vehicle parc support recurring demand across global service networks.

- For instance, in October 2025, DRiV (Tenneco) announced it would showcase an expanded aftermarket offering at AAPEX 2025, featuring MOOG and other service brands aimed at replacement demand.

The OEM segment is expected to grow at a CAGR of 3.1% over the forecast period.

By Steering Architecture

Rack & Pinion Dominates the Market Owing to Widespread Adoption

On the basis of steering architecture, the market is segmented into rack & pinion and recirculating ball.

Rack & pinion systems dominate the market due to compact design, steering precision and widespread use in modern passenger vehicles.

- For instance, in March 2025, Nexteer’s 2024 year-end results noted its first Rack-Assist EPS launch with a Japanese OEM and additional REPS launches, reinforcing rack-based steering adoption.

The Rack & Pinion segment is expected to grow at a CAGR of 3.8% over the forecast period.

By Propulsion

ICE Vehicles Dominate the Market Due to Existing Fleet Size

On the basis of propulsion, the market is segmented into ICE and electric.

ICE vehicles continue to dominate due to their large installed base. Steering and suspension designs remain similar, sustaining steady demand.

- For instance, in 2024, Our World in Data (using IEA data) reported electric cars were 22% of global new-car sales, depicting most new vehicles still used ICE/hybrids, supporting steady steering hardware demand.

The electric segment is expected to grow at a CAGR of 10.6% over the forecast period.

By Material Type

Steel Segment Leads Market for Strength and Cost Efficiency

On the basis of material type, the market is segmented into steel and aluminum.

Steel segment dominates due to high load-bearing capacity, durability, and cost effective manufacturing, making it ideal for steering applications.

- For instance, ZF Aftermarket states its TRW linkage and suspension parts use low-alloy steel to deliver high-strength performance in commercial vehicles, showing why steel remains the default for steering components.

Aluminum segment is expected to grow at a CAGR of 6.9% over the forecast period.

By Manufacturing Process

Forging Segment Dominates Market Due to Structural Integrity

On the basis of manufacturing process, the market is segmented into forging and casting. Forging ensures superior strength and fatigue resistance, making it the preferred process for safety-critical steering components.

- For instance, ZF Aftermarket says its steering and chassis portfolio includes forged steel linkage products (tie-rod ends, control arms, ball joints), demonstrating why forging is preferred for strength and fatigue resistance.

Casting segment is expected to grow at a CAGR of 4.8% over the forecast period.

By Vehicle Type

To know how our report can help streamline your business, Speak to Analyst

On the basis of vehicle type, the market is segmented into passenger cars, light commercial vehicles and heavy commercial vehicles. LCVs dominate due to heavier loads and higher usage intensity, accelerating wear of ball joints and steering linkages.

- For instance, Nexteer explains Rack-Assist EPS is designed for heavier vehicles to handle higher front-axle loads, including trucks, supporting why LCV duty cycles push higher steering and linkage demand.

Passenger cars segment is expected to grow at a CAGR of 2.0% over the forecast period.

Automotive Ball Joint and Steering Linkage Market Regional Outlook

By geography, the Market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

Asia Pacific

Asia Pacific Automotive Ball Joint and Steering Linkage Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to large-scale vehicle production, high replacement demand and expanding automotive manufacturing ecosystems. Countries such as China, India, and Japan contribute significantly through strong sales of passenger vehicles and light commercial vehicles. Rising urbanization, increasing vehicle ownership and improving road infrastructure support consistent aftermarket demand. Additionally, growing focus on comfort and safety and the presence of cost-efficient manufacturing hubs drive sustained market growth across the regional market.

- For instance, China and India continue to lead global vehicle production, producing 19.16 million vehicles in quarter 1&2 in 2025, supporting strong demand for steering and suspension components.

North America

North America is expected to witness steady growth driven by a large and aging vehicle fleet. Frequent replacement of steering components supports aftermarket demand. In the U.S., high usage of pickup trucks and commercial vehicles accelerates wear, strengthening demand for durable ball joints and steering linkages. Strong service networks further support regional market expansion.

Europe

Europe’s market growth is supported by strict vehicle safety standards and emphasis on component reliability. Demand remains stable across passenger cars, with manufacturers focusing on durable and compliant steering systems. The region also benefits from a well-established aftermarket ecosystem.

Rest of the World

The Rest of the World, including middle east & Africa, shows gradual growth driven by rising vehicle imports and expanding service infrastructure. Increasing demand for replacement parts in commercial fleets supports steady aftermarket expansion, particularly in urbanizing economies.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic OEM Alignment and Aftermarket Expansion Drive Competition

The competitive landscape of Market is moderately consolidated, with a mix of global Tier-1 suppliers and regional manufacturers competing across OEM and aftermarket channels. Leading players focus on long-term supply agreements with original equipment manufacturers OEMs, while also strengthening their aftermarket presence to capture recurring replacement demand.

Key companies invest heavily in product quality, testing standards and manufacturing precision to ensure enhanced durability and compliance with safety regulations. Product differentiation is achieved through improved sealing technologies, advanced forging processes and optimized materials that enhance fatigue resistance. These strategies help suppliers meet evolving consumer preference for reliability and reduced maintenance costs.

Another major competitive strategy involves expanding regional manufacturing and distribution networks. Companies are localizing production to reduce logistics costs and support faster delivery across high growth markets. Partnerships with distributors and service networks strengthen aftermarket reach, making the sales channel strategy a core competitive lever.

Digitalization and engineering collaboration also play an important role. Suppliers increasingly work closely with vehicle manufacturers to customize steering linkage systems for specific market segment needs, including passenger cars and light commercial vehicles. This alignment allows suppliers to maintain relevance as vehicle platforms evolve.

- For instance, in June 2024, ZF strengthened its steering components portfolio by expanding chassis system production to support OEM demand for durable ball joints and steering linkages.

LIST OF KEY AUTOMOTIVE BALL JOINT AND STEERING LINKAGE COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Robert Bosch GmbH (Germany)

- Schaeffler AG (Germany)

- NSK Ltd. (Japan)

- THK Co., Ltd. (Japan)

- MOOG / Federal-Mogul (U.S.)

- TRW Automotive (Germany)

- CTR Corporation (South Korea)

- Delphi Technologies (U.K.)

- MAS Industries (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: DRiV, a Tenneco company, presented its expanded aftermarket portfolio at AAPEX 2025, highlighting steering and suspension components aimed at improving parts availability and coverage for global service channels.

- October 2025: ZF Aftermarket introduced TRW’s ‘True Control’ campaign, emphasizing OE-validated steering linkage and suspension parts, including tie rods and ball joints, to support safe and reliable commercial vehicle servicing.

- September 2025: Delphi expanded its steering and suspension portfolio through new ‘first-to-market’ part number additions, targeting faster aftermarket availability for newer passenger vehicle platforms across Europe.

- August 2024: Nexteer Automotive launched its Modular Pinion-Assist Electric Power Steering system, enabling scalable rack-based steering solutions across ICE and electric vehicles while improving cost efficiency and development flexibility.

- October 2024: Mevotech released 239 new undercar aftermarket part numbers, including steering and suspension components designed to address durability and fitment needs for high-usage passenger and light commercial vehicles.

REPORT COVERAGE

The global automotive ball joint and steering linkage market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Sales Channel, By Steering Architecture, Propulsion, Material Type, Manufacturing Process, Vehicle Type, and Region |

|

By Product Type |

· Ball Joints · Steering Linkage |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Steering Architecture |

· Rack & Pinion · Recirculating Ball |

|

By Propulsion |

· ICE · Electric |

|

By Material Type |

· Steel · Aluminum |

|

By Manufacturing Process |

· Forging · Casting |

|

By Vehicle Type |

· Passenger Cars · Light Commercial Vehicles (LCVs) · Heavy Commercial Vehicles (HCVs) |

|

By Geography |

· North America (By Product Type, Sales Channel, By Steering Architecture, Propulsion, Material Type, Manufacturing Process, Vehicle Type, and Country) o U.S. o Canada o Mexico · Europe (By Product Type, Sales Channel, By Steering Architecture, Propulsion, Material Type, Manufacturing Process, Vehicle Type, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Product Type, Sales Channel, By Steering Architecture, Propulsion, Material Type, Manufacturing Process, Vehicle Type, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Product Type, Sales Channel, By Steering Architecture, Propulsion, Material Type, Manufacturing Process, Vehicle Type, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.52 Billion in 2025 and is projected to reach USD 15.65 Billion by 2034.

In 2025, the market value stood at USD 5.03 Billion.

The market is expected to exhibit a CAGR of 3.5% during the forecast period of 2026-2034.

Light Commercial Vehicles segment led the market by vehicle type.

Rising vehicle parc and replacement demand is driving the Market.

Bosch, ZF Friedrichshafen, Schaeffler and NSK are some of the top players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us