Automotive Belts Market Size, Share & Industry Analysis, By Belt Type (Timing Belts, Serpentine Belts, V-Belts, and Others), By Material (Rubber Belts, Polyurethane Belts, and Reinforced Belts), By Vehicle Type (Hatchback/Sedan, SUVs, LCVs and HCVs), By Propulsion (ICE and Electric), By Sales Channel (OEM and Aftermarket), By Application (Engine Timing Systems, Alternator Drive, Power Steering, Air Conditioning Compressor, and others) and Regional Forecasts, 2026-2034

Automotive Belts Market Size and Future Outlook

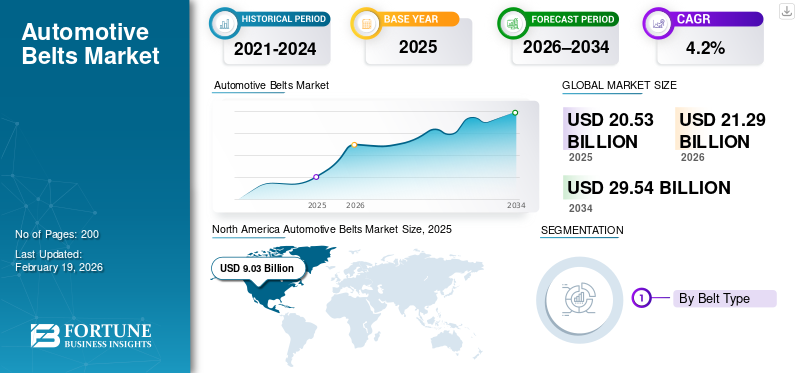

The global automotive belts market size was valued at USD 20.53 billion in 2025. The market is projected to grow from USD 21.29 billion in 2026 to USD 29.54 billion by 2034, exhibiting a CAGR of 4.2% during the forecast period. North America dominated the automotive belts market with a market share of 43.98% in 2025.

The global automotive belts market covers engineered belt systems used for power transmission across multiple vehicle functions, including engine timing, accessory drives, and auxiliary systems such as alternators, air-conditioning compressors, and water pumps. Belts are sold both into OEM production and, more importantly, into the service ecosystem as replacement parts. Demand is closely tied to the size and age of the global vehicle parc, maintenance habits, and repair-shop practices across the automotive sector.

Over the forecast period, market expansion is expected to be shaped by three forces. First, the continued scale of ICE and hybrid vehicles keeps belt demand resilient, even as electric vehicles increase their share of new sales and gradually reduce belt content in fully electric drivetrains. The IEA expects EV sales to keep growing strongly, but the global installed base transitions more slowly, sustaining belt demand for years. Second, a rising share of SUVs and commercial vehicles increases belt value intensity, as these vehicles typically operate under higher loads and longer duty cycles, encouraging the adoption of more durable designs and high performance belt specifications. Third, aftermarket premiumization supports value growth as workshops increasingly favor OE-quality kits and complete system replacements, improving reliability and protecting fuel efficiency by reducing accessory-drive losses and maintenance issues.

Applications span Engine Timing Systems, Alternator Drive, Power Steering, and Air Conditioning Compressor systems, with “Others” covering secondary auxiliaries and niche configurations. On the supply side, OEM vehicle production remains a steady contributor, supported by global automotive manufacturing scale. At the same time, aftermarket demand rises as fleets age and utilization in commercial duty cycles increases.

Across regions, Asia Pacific remains the key market due to its large vehicle parc and production footprint, while North America continues to be important for high vehicle miles traveled, pickup/SUV intensity, and robust service networks. Key suppliers such as Gates Corporation, Bosch, and Continental AG are expanding OE-quality aftermarket portfolios and launching sustainability-focused belt innovations to defend share and grow value.

Download Free sample to learn more about this report.

AUTOMOTIVE BELTS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 20.53 billion

- 2026 Market Size: USD 21.29 billion

- 2034 Forecast Market Size: USD 29.54 billion

- CAGR: 4.20% from 2026–2034

- North America dominated the automotive belts market with a market share of 43.98% in 2025.

- V-belts segment is expected to grow at a CAGR of 5.7% over the forecast period.

- Reinforced belts segment is expected to grow at a CAGR of 5.5% over the forecast period.

North America

North America is projected to record a growth rate of 4.0% in the coming years, which is the third highest among all regions, and reach a valuation of USD 4.47 billion by 2026.

Europe

Europe is estimated to reach USD 4.93 billion in 2026 and secure the position of the second-largest region in the market.

Asia Pacific

Asia Pacific held the dominant share in 2025, valued at USD 9.03 billion, and also maintained the leading share in 2024, with USD 8.89 billion.

U.S.

In the U.S., demand is reinforced by a large installed base and high utilization in commercial and personal-use light trucks.

Japan

Japan remains a key market within Asia Pacific, benefiting from its large automotive production capacity, extensive vehicle ownership base, and sustained demand for maintenance and replacement components in conventional and hybrid vehicles.

Read More

AUTOMOTIVE BELTS MARKET TRENDS

Adoption of Recycled Materials and Sustainability-focused Belt Designs is a Key Market Trend

Suppliers are embedding recycled and renewable inputs into belt constructions while maintaining performance, aligning with OEM and aftermarket sustainability targets. This trend supports brand differentiation and helps suppliers meet procurement expectations without sacrificing durability. As regulation and customer audits expand, sustainability-labeled belts and packaged kits are becoming a practical route to defend pricing and strengthen installer loyalty.

For instance, Continental introduced CONTI NXT Multi V-belts with nearly two-thirds sustainable materials, positioning the belt as a lower-footprint option for workshops seeking greener parts without performance trade-offs.

MARKET DYNAMICS

MARKET DRIVERS

Growing Vehicle Parc and Service-Led Demand Sustain Belt Replacements

A large global installed base of ICE and hybrid vehicles keeps belt demand stable, while higher utilization in SUVs and commercial fleets increases wear and accelerates replacement cycles. As workshops prioritize reliability, they increasingly specify OE-quality kits, raising value per job. This dynamic supports the belt and hose market’s growth even as new-vehicle cycles fluctuate.

- For instance, Dayco stated it is expanding serpentine belt coverage and kit offerings for high vehicle-in-operation applications, reflecting demand from service channels and fleet-heavy use cases.

MARKET RESTRAINTS

Electrification Gradually Reduces Belt Content Per Vehicle Further Restraining Market Growth

As electric vehicles scale up, fully electric drivetrains remove several belt-driven accessories and reduce the addressable belt demand compared to an ICE architecture. While the installed base changes slowly, regions with faster EV adoption will witness a structural headwind, especially for accessory drives. This shifts supplier focus toward hybrids, thermal-management solutions, and higher-value aftermarket kits, driving automotive belts market growth.

- For instance, the IEA highlights rapid growth in global EV sales and projections through 2035, reinforcing the long-term shift in vehicle technology that can reduce belt content in BEVs.

MARKET OPPORTUNITIES

Premium Belt Kits and Advanced Engine Architectures Open New Value Opportunities

Newer engines and service practices favor complete repairs; belt drive kits, timing kits, and bundled components rather than single-part replacements. This expands value per service event and supports the adoption of advanced belt designs engineered for durability, noise reduction, and tighter packaging. Suppliers that standardize kit programs and expand fitment coverage can win incremental aftermarket share as workshops prioritize first-time-fix outcomes.

- For instance, Gates launched an EMEA Micro-V kit campaign to encourage full kit replacement and emphasize inspection, aiming to improve repair quality and increase kit adoption versus loose parts.

MARKET CHALLENGES

Counterfeit and Low-Quality Parts Threaten Safety and Pricing Power

Illicit supply of counterfeit automotive components can undermine brand trust, distort price competition, and create safety risks when inferior parts fail prematurely. This is especially problematic in fragmented aftermarket channels where traceability is weak. For belt suppliers, counterfeits can raise warranty disputes and reduce installer confidence, forcing investment in authentication, channel governance, and distributor education.

- For instance, the OECD notes that counterfeit goods can create safety risks, including counterfeit automotive spare parts, reinforcing the need for belt makers and distributors to invest in traceability and enforcement.

Download Free sample to learn more about this report.

Segmentation Analysis

By Belt Type

Aftermarket Demand, Higher Accessory Loads, and SUV Usage Drives Serpentine Belts Segment Growth

On the basis of belt type, the market is divided into timing belts, serpentine belts, v-belts, and others.

Serpentine belts segment dominates the market as they run key auxiliaries and are common across most ICE vehicles, driving frequent replacement demand in the aftermarket. Their role in accessory loads and NVH performance supports continued specification upgrades and the use of higher-value materials. Growth is reinforced by SUV and light-truck duty cycles, where accessory loads and heat exposure are higher.

- For instance, Dayco launched a new ELA serpentine belt addition for pickups and SUVs, presenting ongoing product development and strong service demand in high-usage applications.

V-belts segment is expected to grow at a CAGR of 5.7% over the forecast period.

By Material

Rubber Belts Segment Leads the Market Due to Proven Durability and Cost Balance

On the basis of material, the market is segmented into rubber belts, polyurethane belts, and reinforced belts.

Rubber-based belt segment dominated the market. Its constructions remain the default for broad OE and aftermarket compatibility and stable performance across temperature ranges. Continued material engineering improves wear resistance and friction characteristics without pushing costs beyond mass-market acceptance. Inflation in elastomers supports value growth, while suppliers differentiate through compound design and reinforcement.

- For instance, ANRPC reported tight natural rubber supply-demand conditions in 2024, a factor that influences input costs and reinforces value growth and material optimization across rubber-based belt products.

Reinforced belts segment is expected to grow at a CAGR of 5.5% over the forecast period.

By Vehicle Type

Hatchback/Sedan Segment Dominate Due to Large Installed Base

On the basis of vehicle type, the market is segmented into hatchback/sedan, SUVs, LCVs and HCVs.

Hatchback/sedan segment dominated with the largest automotive belts market share. These vehicles form the backbone of the global passenger car parc, particularly in mass-market segments, leading to sustained demand for belts as replacement parts. Their continued reliance on the internal combustion engine and hybrids ensures consistent aftermarket servicing. At the same time, electrification in entry- and mid-level cars preserves belt-related demand over the forecast period.

- For instance, according to OICA vehicle production and parc statistics, passenger cars continue to represent the largest share of vehicles in operation globally, supporting the dominant aftermarket demand for automotive belt systems.

HCVs segment is expected to grow at a CAGR of 5.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

ICE Dominates as Belts Are Core to Ice Accessory and Timing Systems

On the basis of propulsion, the market is segmented into ICE and electric.

ICE segment dominates the market. Belts remain fundamental to ICE operation and accessory systems, and the global installed base turns over slowly. Even with EV acceleration, ICE and hybrids will continue to account for most belt-driven architectures for years, supporting aftermarket continuity. The market’s value is therefore anchored in ICE parc size and repair frequency.

- For instance, the IEA projects strong EV sales growth, but also shows a multi-year transition, supporting the view that ICE-installed-base demand remains the primary belt driver in the medium term.

Electric segment is expected to grow at a CAGR of 6.3% over the forecast period.

By Sales Channel

Aftermarket Dominates as Belts Are Recurring Replacement Items

On the basis of sales channel, the market is segmented into OEM and aftermarket.

Aftermarket segment led the market. Belts are replaced multiple times over vehicle life, making the aftermarket structurally larger than OEM fitment. Aging fleets, heavy-duty use, and service bundling (kits) further increase value per repair. Suppliers strengthen this channel via distribution partnerships, installer training, and broader SKU coverage in high-volume applications.

- For instance, Gates’ Micro-V kit conversion initiative promotes kit replacement over loose parts, directly supporting aftermarket value capture and improved repair outcomes for workshops.

Aftermarket segment is expected to grow at a CAGR of 4.8% over the forecast period.

By Application

Engine Timing Systems lead because failures are critical and costly

On the basis of application, the market is segmented into engine timing systems, alternator drive, power steering, air conditioning compressor, and others.

Engine timing systems segment dominates the market. Its maintenance-critical; missed intervals can cause severe engine damage, so customers and workshops prioritize quality and full-system replacement. This supports higher-value timing kits and associated components. While some engines use chains, belt-driven timing remains widespread, and premium “complete kit” servicing supports value growth.

- For instance, Continental highlighted expansion of belt drive kits and engine-related spare parts, reflecting strong timing and engine-service demand in the aftermarket and continued fitment coverage additions.

Air conditioning compressor segment is expected to grow at a CAGR of 5.2% over the forecast period.

Automotive Belts Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

North America Automotive Belts Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 9.03 billion, and also maintained the leading share in 2024, with USD 8.89 billion. Asia Pacific is expected to hold the largest market share due to its massive vehicle parc, high utilization in dense urban logistics, and a large base of ICE and hybrid vehicles requiring regular belt service. The region’s scale of automotive manufacturing supports steady OEM volumes, while fast-growing aftermarket networks drive recurring demand for replacement parts. Even as EVs rise, the installed base transition is gradual, keeping belt replacement resilient across the period.

- For instance, OICA production statistics consistently show Asia Pacific markets such as China, Japan, and India among the world’s largest vehicle producers, supporting a large vehicle parc and sustained belt service demand.

China Automotive Belts Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 3.54 billion, representing roughly 17.2% of global market.

India Automotive Belts Market

India market in 2025 was valued at USD 1.37 billion, accounting for roughly 6.7% of global revenues.

Europe

Europe is estimated to reach USD 4.93 billion in 2026 and secure the position of the second-largest region in the market. Europe’s market grows through premium aftermarket servicing, stronger sustainability requirements, and continued parc aging, while EV adoption creates a longer-term headwind for belt content. Suppliers respond by emphasizing OE-quality kits, advanced materials, and lower-footprint products, helping preserve value even as ICE share gradually declines.

Germany Automotive Belts Market

Germany market in 2025 was valued at USD 1.25 billion, accounting for roughly 6.1% of global revenues.

U.K. Automotive Belts Market

U.K. market in 2025 reached a valuation of USD 0.94 billion, accounting for roughly 4.6% of global revenues.

North America

North America is projected to record a growth rate of 4.0% in the coming years, which is the third highest among all regions, and reach a valuation of USD 4.47 billion by 2026. North America witnesses steady value growth driven by high vehicle miles traveled, a strong pickup/SUV mix, and mature service networks that favor complete kit replacements. Inflation in materials and labor supports higher average selling prices for OE-quality belts and kits. In the U.S., demand is reinforced by a large installed base and high utilization in commercial and personal-use light trucks.

U.S. Automotive Belts Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 3.56 billion, representing roughly 17.3% of global automotive belts market.

Rest of the World

Rest of the world growth is supported by parc expansion, rising motorization, and heavy use in commercial transport and last-mile delivery. As service infrastructure improves, customers shift toward branded belts and complete kits, lifting value per repair. Price inflation and higher-duty operating conditions also raise replacement frequency.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategies Shaping Competition Among Global Belt Suppliers

The competitive landscape in automotive belts is defined by scale, coverage depth, OE relationships, and aftermarket pull-through. Leading suppliers compete on material science, durability, and fitment breadth across fast-moving vehicle populations. Many key players treat belts as part of broader under-hood system offerings, bundling belt drive kits, tensioners, and related components to increase share-of-repair and reduce installation risk for workshops.

A core strategy is OE-grade aftermarket positioning; suppliers leverage original-equipment engineering and testing data to market belts and kits that mirror OE specifications and service intervals. Another major lever is fitment expansion, adding part numbers for high-volume applications (especially pickups and SUVs) to win shelf space with distributors and installers. Portfolio differentiation also matters; suppliers are adding belts designed for newer engine architectures (including wet/belt-in-oil applications) and improving belt constructions to handle higher loads, thermal cycling, and start-stop duty patterns.

Sustainability and compliance are emerging as competitive tools. Several suppliers are introducing belt materials with recycled/renewable content and promoting lower-footprint production, aligning with customer procurement requirements and broader decarbonization policies. Geographic strategy is also key; capacity additions or localization in growth markets reduce lead times and support price competitiveness in regions with volatile logistics costs.

Moreover, marketing and installer-education campaigns are used to shift demand toward complete kit replacement rather than single-belt swaps, increasing value per service event and improving repair outcomes, an advantage in an aftermarket where trust and repeat purchase drive share.

- For instance, Continental announced that it is expanding its engine-related aftermarket range, including water pumps and belt drive kits, and introduced the CONTI NXT Multi V-belt, which features a high share of sustainable materials.

LIST OF KEY AUTOMOTIVE BELTS COMPANIES PROFILED

- Gates Corporation (U.S.)

- Continental AG (Germany)

- Schaeffler (Germany)

- Bosch (Germany)

- SKF (Sweden)

- Dayco (U.S.)

- Mitsuboshi Belting Ltd. (Japan)

- Bando Chemical Industries, Ltd. (Japan)

- Arntz Optibelt Group (Germany)

- Nitta Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Dayco introduced timing belt-in-oil technology in the North America aftermarket, offering OE-equivalent solutions for selected Ford and Lincoln turbocharged engines. This launch reflects the increasing adoption of advanced belt architectures designed to improve durability, noise reduction, enhance emissions performance, and support modern engine designs.

- October 2025: Mitsubishi Belting Ltd. expanded production capacity for Electric Power Steering (EPS) drive belts to address rising demand from automotive OEMs. The expansion supports increased adoption of electronically assisted steering systems and reinforces the company’s focus on specialized belt solutions for evolving vehicle architectures.

- May 2025: Dayco expanded its North America aftermarket range with new part numbers across timing chain kits, tensioners, and hose lines, strengthening bundled-service coverage.

- October 2024: Dayco expanded its HT POWER synchronous belt line and improved ordering flexibility and processing speed, aiming to shorten lead times and improve service responsiveness.

- September 2024: Continental announced a major expansion initiative for its aftermarket portfolio, including progressive expansion of engine-related spare parts and belt drive kit coverage.

- July 2024: Gates launched a Micro-V kit conversion campaign in EMEA to promote full kit replacement and emphasize inspection, improving repair outcomes and increasing kit adoption.

- April 2024: Bando announced development of a cellulose nanofiber-compounded rubber double cog belt concept for high-load applications, reflecting ongoing material innovation in belt performance.

REPORT COVERAGE

The global automotive belts market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Belt Type, Material, Vehicle Type, Propulsion, Sales Channel, Application and Region |

|

By Belt Type |

· Timing Belts · Serpentine Belts · V-Belts · Others |

|

By Material |

· Rubber Belts · Polyurethane Belts · Reinforced Belts |

|

By Vehicle Type |

· Hatchback/Sedan · SUVs · Light Commercial Vehicles (LCVs) · Heavy Commercial Vehicles (HCVs) |

|

By Propulsion |

· ICE · Electric |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Application |

· Engine Timing Systems · Alternator Drive · Power Steering · Air Conditioning Compressor · Others |

|

By Geography |

· North America (By Belt Type, Material, Vehicle Type, Propulsion, Sales Channel, Application and Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Belt Type, Material, Vehicle Type, Propulsion, Sales Channel, Application and Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Belt Type, Material, Vehicle Type, Propulsion, Sales Channel, Application and Country) o China (By Vehicle Type) o India (By Vehicle Type) o Japan (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Belt Type, Material, Vehicle Type, Propulsion, Sales Channel, Application and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 20.53 billion in 2025 and is projected to reach USD 29.54 billion by 2034.

In 2025, the North America market value stood at USD 9.03 billion.

The market is expected to exhibit a CAGR of 4.2% during the forecast period of 2026-2034.

Hatchback/sedan segment led the market by vehicle type.

Growing vehicle parc and service-led demand are the key factors driving the market.

Gates Corporation, Continental AG, Bosch and Dayco are some of the top players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us