Light Duty Truck Market Size, Share & Industry Analysis, By Class (Class 1 and Class 2), By Drive Configuration (2WD and AWD), By Powertrain (ICE, Hybrid, and Electric), By Vehicle Type (Pickup Trucks, Vans, and Mini Trucks), By Component (Engine and Powertrain, Chassis & Suspension, Body and Bed, Braking and Steering, Electrical & Cooling System, Safety Features, Wheels & Tires, and Other Components), By Application (Delivery Services, Construction & Landscaping, Utility and Maintenance, Small Business Operations, Emergency Services, and Waste Management), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

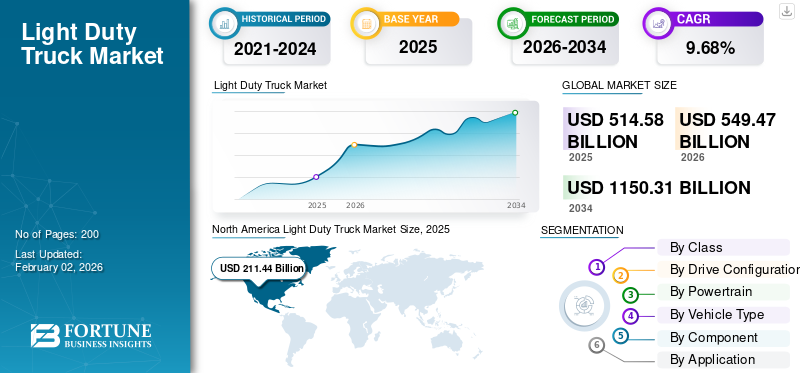

The global light duty truck market size was valued at USD 514.58 billion in 2025. The market is projected to grow from USD 549.47 billion in 2026 to USD 1,150.31 billion by 2034, exhibiting a CAGR of 9.68% during the forecast period. North America dominated the global market with a share of 41.09% in 2025.

A light duty truck is a motor vehicle primarily designed for transporting goods with a gross vehicle weight rating (GVWR) typically under 8,500 pounds (3,860 Kg). Common types include pickup trucks, cargo vans, and mini trucks. These vehicles offer a balance between payload capacity, fuel efficiency, and maneuverability, making them suitable for urban and suburban use, small businesses, and personal utility. They are also widely used in logistics, construction, and service industries.

The market is driven by rising e-commerce, urban delivery demand, and expanding infrastructure projects. Increasing preference for personal utility vehicles, fuel-efficient models, and electric variants boosts growth. Government incentives, evolving emission norms, and growing small business operations also support market expansion. Additionally, advancements in vehicle technology improve payload capacities, and fleet modernization efforts by logistics companies are key factors accelerating the global demand for light duty trucks.

Key players in the market include global OEMs driving innovation across segments. Ford, General Motors, Toyota, among others, lead the market with strong portfolios and innovation in fuel efficiency and electrification. Other industry players are expanding their market presence, competing through technology, global reach, and evolving emission-compliant models.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

E-Commerce Expansion and Urban Logistics Drive Market Growth

With growing online shopping, there is an increasing demand for efficient last-mile delivery solutions. Light duty trucks, especially cargo vans and mini trucks, are ideal for navigating congested urban environments, offering flexibility and cost-effectiveness. E-commerce giants and logistics providers are rapidly expanding their fleets to meet delivery timelines and customer expectations. Additionally, the need for frequent, small-scale deliveries in cities boosts demand for these vehicles, accelerating light duty truck market growth. Electrification trends further support adoption in emission-regulated urban zones, enhancing their long-term viability.

In October 2024, Chevrolet BrightDrop 400 electric vans began rolling out in major U.S. cities such as Austin, Dallas, Denver, Detroit, and others as a part of Walmart’s expanded InHome delivery service. The vans are equipped with 360-degree HD surround vision, blind-zone steering assists, auto-closing doors, ergonomic design, and enhanced city maneuverability, supporting Walmart’s goal to decarbonize its last-mile logistics.

Market Restraints

Stringent Emission Regulations and Compliance Costs Hamper Market Growth

Governments across regions such as North America, Europe, and Asia are enforcing tough standards to reduce greenhouse gas emissions and air pollution. To comply, manufacturers must invest heavily in advanced technologies such as electric drivetrains, hybrid systems, and exhaust after-treatment solutions. These technologies substantially increase production costs, which are often passed on to consumers, making vehicles less affordable, especially in cost-sensitive markets. Smaller manufacturers also struggle with compliance, limiting their competitiveness. Additionally, regulatory uncertainty and shifting standards increase investment risks, deterring innovation and slowing market expansion.

Market Opportunities

Rising Technological Innovations Provide Market Opportunity

Technological innovations are creating significant growth opportunities in the light duty trucks market. Integration of advanced driver assistance systems (ADAS), real-time telematics, and predictive maintenance tools enhances vehicle safety, efficiency, and uptime. Connectivity features such as GPS tracking, fuel management, and IoT-based diagnostics support better fleet management. Automation and smart routing solutions reduce operational costs and improve delivery speed. Additionally, advancements in electric drivetrains, battery technology, and lightweight materials enable the development of energy-efficient, high-performance trucks. These innovations appeal to commercial operators seeking long-term savings and regulatory compliance, driving greater adoption of modern light duty trucks across global logistics, utility, and urban transportation sectors.

In February 2022, Chinese startup WeRide began deploying its Level 4 Robovan self-driving cargo vans for urban deliveries in partnership with JMC and ZTO Express. The fully autonomous vans based on JMC battery-electric platforms delivered goods and gathered data after surpassing 2.5 million km of unmanned driving across 300 vehicles in China and the U.S.

Market Challenges

High Competition and Market Saturation Challenge the Adoption of Light Duty Trucks

High competition and market saturation in regions such as North America and Western Europe challenge the market growth by limiting the expansion of opportunities and compressing profit margins. Established players face intense rivalry, leading to price wars and aggressive discounting strategies. With limited room for new customer acquisition, growth becomes reliant on vehicle replacements rather than a new demand. Additionally, product differentiation becomes difficult, as most offerings converge in features and performance. Emerging players, especially EV startups, struggle to penetrate mature markets dominated by brand loyalty and well-established dealer networks. This competitive pressure slows innovation and increases marketing and operational costs for all players.

Light Duty Truck Market Trends

Rise in Electrification Process in Traditional Fuel Vehicles Drives Market Trend

Electrification is driving growth in the market by offering cleaner and cost-efficient alternatives to traditional fuel vehicles. Strict emission regulations and government incentives are prompting manufacturers to adopt electric drivetrains. Lower operating and maintenance costs make electric trucks attractive to fleet operators. Corporate sustainability goals are also accelerating fleet electrification, with companies such as Amazon and DHL leading adoption. Advances in battery technology have improved range and reduced charging time, enhancing practicality. Additionally, expanding charging infrastructure and innovations such as battery swapping in markets such as China, and others are making electric light duty trucks a more viable option, fueling demand and market expansion over the forecasted period.

In October 2023, Amazon deployed around 10,000 Rivian electric delivery vans across the U.S. and Europe, as part of its 100,000 vehicle commitment by 2030. These EVs contribute to reduced carbon emissions and are supported by thousands of charging stations at Amazon facilities.

Impact of Tariffs

Market Witnesses Rise in Vehicle and Raw Material Costs Due to Tariffs

U.S. tariffs on imported vehicles, parts, and raw materials significantly impact the light duty market by increasing production and procurement costs. Tariffs on steel, aluminum, and auto components raise manufacturing expenses for both domestic and foreign automakers, leading to higher vehicle prices for consumers. This can reduce demand, especially in price-sensitive segments. Additionally, tariffs on imported electric vehicles and batteries may slow the adoption of electric light duty trucks by limiting supply chains and innovation. Retaliatory tariffs from other countries can disrupt export opportunities for U.S. manufacturers, affecting global competitiveness and creating uncertainty in long-term planning and investment decisions.

Segmentation Analysis

By Class

High Demand in Urban Last Mile Delivery Drives the Class 1 Segment Growth

Class 2 is expected to account for 80.96% of the total market share in 2026, due to its compact size, affordability, and high demand in urban last-mile delivery and personal utility applications. These trucks are ideal for congested cities and are widely adopted by small businesses and courier services. Fuel efficient, environmental friendly, ease of handling, and lower regulatory constraints further boost their adoption in developed and emerging regions.

The class 2 trucks are expected to witness the highest growth rate in adoption due to the growing demand for vehicles with higher payload capacity without moving into heavy-duty classifications. Used extensively in construction, landscaping, and utility services, these vehicles offer a balance of power, efficiency, and flexibility. Rising commercial applications, increased hybrid and electric variants in this class are driving global market growth.

In May 2024, Tata Motors launched the all-new Ace EV 1000 electric mini truck, offering a 1-tonne payload and a certified 161 km range. Built on the EVOGEN powertrain, it delivers 27 kW/130 Nm power, features fast charging, a 7-year battery warranty, Fleet Edge telematics, and support via 150+ EV centers, aimed at transforming India’s last-mile logistics.

By Drive Configuration

Suitability for Urban and Paved Road Operations Fuels the 2WD Segment Dominance

Based on the drive configuration, the market is categorized into 2WD and AWD.

The 2WD drive configuration segment is projected to hold 61.71% of the market share in 2026, fuel efficiency, and suitability for urban and paved road operations. These are widely used in city deliveries and small business operations where off-road capability is not required. 2WD configurations are popular among cost-sensitive consumers and fleet operators, especially in regions with well-developed infrastructure.

The AWD (all wheel drive) segment is growing fast, driven by increasing demand for versatility and off-road capability. These trucks are preferred for utility, construction, and rural applications where terrain may vary. Technological advancements and the integration of AWD in electric and hybrid models also contribute to the rising popularity of the segment over the forecasted period.

In October 2024, RIDDARA launched Thailand’s first 100% electric pickup, the RD6, built on its M.A.P. platform. It accelerates 0 to 100 km/h in 4.5 seconds with 595 Nm torque, offers automotive AWD with seven terrain modes, 815 mm wading depth, 3t towing, plus SUV-level comfort and advanced ADAS.

By Powertrain

Affordability, Established Infrastructure, and Widespread Availability Drives the ICE Segment Dominance

Based on powertrain, the market is divided into ICE, hybrid, and electric.

The ICE powertrain segment is anticipated to dominate with a 83.67% market share in 2026. These vehicles dominate due to their affordability, established infrastructure, and widespread availability. They remain the preferred choice in regions with limited EV charging networks. Diesel and gasoline variants continue to serve high-load and long-distance applications effectively, especially in developing markets.

Electric light duty trucks are the fastest-growing segment, fueled by government incentives, emission regulations, and advancements in battery technology. Their adoption is accelerating in urban logistics and corporate fleets. Growing environmental awareness and reduced operational costs also contribute to this segment, driving the growth of the market over the forecasted period.

In January 2025, Omega Seiki Mobility unveiled the M1KA 1.0 electric mini-truck at Bharat Mobility Global Expo. It offers 90-170 km range via 10.24/15/21 kWh battery options, fast charging, 850 kg payload, 67 Nm and torque.

By Vehicle Type

Utility, Durability, and Dual-Purpose Usage to Drive the Pickup Trucks Segment Growth

By vehicle type, the market is segmented into pickup trucks, vans, and mini trucks.

Vans are forecast to represent 42.73% of the total market share in 2026. Pickup trucks lead the market due to their utility, durability, and dual-purpose use for personal and commercial applications. High towing capacity, comfort features, and brand loyalty in North America strongly support the dominance of the segment in the regional and global market.

The adoption of vans witnesses a high growth rate during the forecasted period. This growth is attributed to the booming e-commerce and last-mile delivery services. Their enclosed cargo space and suitability for urban use make them ideal for logistics and fleet operations in cities. This propels the growth of the market during the considered timeframe.

In February 2025, Kia launched a PV5, its first modular electric van built on the E-GMP.S skateboard platform. The vehicle is available in Passenger, Cargo, Chassis Cab, WAV, and Light Camper variants. It offers up to 249 miles WLTP range, a 120 kW motor, 150 kW fast charging, V2L power, and versatile interior layouts.

To know how our report can help streamline your business, Speak to Analyst

By Component

Innovation in Fuel Efficiency, Emissions Control, and Electrification Drives the Engine and Powertrain Segment Growth

By component, the market is segmented into engine and powertrain, chassis & suspension, body and bed, braking and steering, electrical & cooling system, safety features, wheels & tires, and other components.

The engine and powertrain segment dominates the market due to its central role in vehicle performance, durability, and efficiency. Ongoing innovation in fuel efficiency, emissions control, and electrification is driving the investment in this area. Whether for ICE, hybrid, or electric models, the powertrain remains critical to the truck’s capability, cost efficiency, and long-term reliability. As emission regulations tighten, automakers continue to focus R&D on optimizing this core component to meet evolving global standards.

In August 2024, Hyundai revealed the development of an EREV (Extended Range Electric Vehicle) powertrain for its pickup trucks and SUVs. Featuring a small combustion engine that charges the battery while propulsion remains fully electric, it aims to deliver up to 1,000 km of range.

The electrical and cooling system segment is estimated to develop at the fastest-growing CAGR during the forecasted period due to the shift toward electric and hybrid trucks. Battery cooling, high voltage systems, and integrated control modules are becoming essential to ensure performance and safety. The demand for the segment is further fueled by advanced telematics, infotainment, and ADAS (Advanced Driver Assistance Systems) features requiring robust electrical support. As EV adoption grows, this segment will remain a key focus for innovation and investment.

By Application

Growth in E-commerce and Last-mile Logistics Propels Delivery Services Segment Growth

By application, the market is classified into delivery services, construction & landscaping, utility and maintenance, small business operations, emergency services, and waste management.

Delivery services held the largest market share in 2025. This is due to the explosive growth of e-commerce and last-mile logistics. Urbanization, digital retail, and increased consumer expectations for fast delivery drive continuous demand for efficient and compact trucks. Fleet operators prefer LDTs for their maneuverability, payload versatility, and cost efficiency. Electrification is also being rapidly adopted in this segment to comply with emission norms in urban centers. The reliability and adaptability of LDTs make them the preferred solutions for high-frequency deliveries.

In February 2025, Rivian opened up Commercial Van sales, formerly exclusive to Amazon, to U.S. fleets of all sizes. Two models launched, which include the Delivery 500 (161-mile range, USD 79,900) and Delivery 700 (160-mile range, USD 83,000), both with a 100 kWh LFP battery and standard driver and safety suite.

The construction and landscaping segment is witnessing the fastest growth as infrastructure development has accelerated globally. Light duty trucks serve as essential tools for transporting tools, raw materials, and workers across job sites. Demand is particularly strong in developing nations undergoing rapid urbanization and in developed regions investing in sustainable infrastructure upgrades. Trucks used in this segment are increasingly being equipped with reinforced beds, towing features, and off-road capabilities to suit rough conditions, which propels the growth of the market over the forecasted period.

Light Duty Truck Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Light Duty Truck Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America leads the market due to strong demand for pickup trucks and cargo vans across the commercial, industrial, and personal use segments. The presence of established OEMs such as Ford, GM, and Stellantis ensures constant innovation, competitive pricing, and widespread availability. The regions’ well-developed road infrastructure and high disposable income support vehicle ownership and fleet operations. Moreover, the booming e-commerce and logistics sectors are driving demand for light duty vehicles used in last-mile delivery, fueling market growth in the region. The U.S. market is projected to reach USD 186.94 billion by 2026. North America recorded a market size of USD 211.44 billion in 2025, capturing 41.09% of the global market share, and is projected to reach USD 222.7 billion in 2026.

The U.S. dominates this regional market, accounting for a significant share of sales and production. American consumers have a long-standing preference for pickup trucks due to their versatility, towing capacity, and suitability for personal and commercial use. Major automakers such as Ford, Chevrolet, and Ram lead the market with popular models, which fuels the light duty truck market growth in the country.

In April 2025, Kia officially confirmed its development of an electric mid-size pickup truck for the U.S. market. Riding on a new EV platform, the upcoming models aim to compete with the Ford Ranger and the Toyota Tacoma.

Europe

Europe holds the second-largest light duty truck market share, driven by strong environmental regulations and rapid transition to zero-emission transport solutions. Stringent CO2 emission targets and low-emission zones in urban areas have pushed demand for electric and hybrid light-duty trucks. The region’s mature automotive industry, led by companies such as Volkswagen, Renault, and Mercedes-Benz, is introducing innovative and efficient LDT models. Government subsidies, carbon credit programs, and green mobility strategies further support electrification, fueling market growth in this region. The UK market is projected to reach USD 24.13 billion by 2026, while the Germany market is projected to reach USD 45.34 billion by 2026. In 2025, Europe represented USD 146.5 billion, accounting for 28.47% of the worldwide market, and is projected to grow to USD 156.21 billion in 2026.

In May 2025, Mercedes-Benz began road testing its new modular electric van architecture, VAN.EA, with prototypes of upcoming public and luxury models. Built atop a modular “Lego-like” EV platform, the vans, ranging from compact to commercial units to upscale MPV, are set to launch in 2026. The VLE test vehicle recently completed a 1,100 km Stuttgart-Rom run with only two 15-minute charging steps.

Asia Pacific

Asia Pacific region holds a sustainable share in the market, and is attributed to develop at the fastest growing CAGR during the forecasted period. Rapid urbanization, industrial growth, and rising e-commerce fuel demand, particularly in countries such as China, India, and Japan. China leads global electric light duty truck adoption due to strong government support, battery innovation, and large-scale deployment of battery-swapping infrastructure. In India, increased infrastructure spending and rural connectivity programs create demand for affordable and durable LDTs. Local players such as Tata Motors, BYD, ISUZU, and others are expanding offerings, making trucks more accessible, further fueling the market growth within the region. The Japan market is projected to reach USD 23.01 billion by 2026, the China market is projected to reach USD 66.34 billion by 2026, and the India market is projected to reach USD 22.07 billion by 2026. The Asia Pacific market generated USD 134.48 billion in 2025, representing 26.13% of the global market landscape, and is expected to reach USD 146.68 billion in 2026.

In April 2025, Isuzu began mass production of its fully electric 1-ton pickup, the D-MAX EV, at its Thailand plant. Equipped with dual e-axles and full-time 4WD, it delivers 140 kW/325 Nm, over 1 tonne payload capacity, and 3.5 t towing, with a 66.9 kWh battery offering.

Rest of the World

The rest of the world comprises South America, the Middle East, and the African sub-regions, holding the smallest share in the market due to limited economic resources, infrastructure, and electrification. However, growth opportunities are emerging with increasing investments in logistics, agriculture, and small-scale industrial sectors. Demand is driven by the need for cost-effective, rugged, and fuel-efficient transport in developing regions. Although electric truck adoption is still nascent, CNG and hybrid models are gaining attention as viable alternatives, driving the market growth in these regions. The market in Rest of the World reached USD 22.16 billion in 2025, representing 4.31% of total market revenue, and is projected to reach USD 23.88 billion in 2026.

In May 2024, BYD launched its first-ever pickup truck, a plug-in hybrid BYD Shark, in Mexico. Built on the DMO Super hybrid platform, it delivers over 430 hp, accelerates 0-100 km/h in 5.7 seconds, and offers a combined range of 840 km with 100 km pure EV.

Competitive Landscape

Key Market Players

Strategic Partnerships, Fleet Orders, and Regional Expansions Provide Competitive Edge

The competitive landscape of the global light duty market is characterized by the presence of established automakers and emerging electric vehicle manufacturers. Key players include Ford, General Motors, and Toyota, among others, dominating with wide product portfolios and global reach. European firms such as Volkswagen and Renault focus on electric vans and low-emission models, while Chinese companies such as BYD are rapidly expanding in the EV segment. The market is intensely competitive, with players investing in electrification, connectivity, and advanced safety technologies. Strategic partnerships, fleet orders, and regional expansions provide a competitive edge in the market, as companies strive to capture the largest market share.

List of Key Light Duty Truck Companies Profiled in the Report:

- Ford Motor Company (U.S.)

- General Motors (U.S.)

- Stellantis (Netherlands)

- Toyota Motor Corporation (Japan)

- Mercedes-Benz (Germany)

- Volkswagen Commercial Vehicles (Germany)

- ISUZU Motors Ltd. (Japan)

- Nissan Motors Co. (Japan)

- Hyundai Motor Company (South Korea)

- Tata Motors (India)

- Mahindra and Mahindra (India)

- Fuso Truck (Japan)

Key Industry Developments

- In July 2025, Slate Auto quietly dropped its “under USD 20,000” pricing for the upcoming EV pickup after the tax-cut bill eliminated the USD 7,500 federal EV credit due to end in September 2025.

- In May 2025, GAC unveiled its futuristic Pickup 01 concept at Auto Shanghai 2025. Boasting a “sci-tech” aesthetic reminiscent of Tesla’s Cybertruck and Hummer EV, it features digital mirrors, illuminated light bars, a GAIA adaptive platform, and a sliding steering wheel for LHD/RHD conversion.

- In April 2025, Nissan unveiled the all-new Frontier Pro plug-in hybrid pickup at Auto Shanghai 2025. Powered by a 1.5 L turbo engine and electric motor, it delivers over 300kW and up to 800 Nm torque, with around 135 km EV range.

- In October 2024, Scout Motors, a Volkswagen-owned U.S. startup, revealed two near-production electric vehicles: the Terra Pickup and Traveler SUV. Both feature body-on-frame architecture, solid rear axles, mechanical lockers, 800 V charging, and are projected to reach 350-mile EV range, with operational gas-powered generators boosting range to 500 miles, and towing exceeds 10,000 lbs.

- In March 2023, Ford revealed its next-generation electric pickup, codenamed Project T3, branded internally as the “Millennium Falcon” of trucks, with production set for 2025 at the new BlueOval City plant in Tennessee.

Investment Analysis and Opportunities

Electrification and Technological Innovation Drive Investment Opportunities

The light duty truck market presents strong investment opportunities driven by rising demand for urban logistics, electrification, and last mile delivery solutions. Investors are focusing on electric vehicle startups, battery manufacturers, and charging infrastructure developers. Established OEMs are allocating significant capital toward investing in research and development and EV production facilities to meet regulatory targets and consumer demand. Government incentives and emission mandates are encouraging green mobility investments. Additionally, emerging markets in Asia Pacific and Africa offer growth potential due to rising urbanization and infrastructure development. Strategic partnerships, fleet electrification projects, and technological innovation in telematics and autonomous driving are key areas attracting global investment interest in the market.

Report Coverage

The global light duty truck market report analyzes the market in depth. It highlights crucial aspects such as prominent companies, market scope, competitive landscape, class/payload capacity, drive configuration, powertrain, vehicle type, engine capacity, component, and application. Besides this, the market research reports provide insights into the light duty truck market trends and highlight significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

|

|

Unit |

Value (USD Billion) and Volume (Thousand Units) |

|

Segmentation |

By Class

By Drive Configuration

By Powertrain

By Vehicle Type

By Component

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says the global light duty truck market was valued at USD 514.58 billion in 2025 and is anticipated to reach USD 1,150.31 billion by 2034.

The market will exhibit a CAGR of 9.68% over the forecast period (2026-2034).

In 2025, the ICE segment by powertrain will dominate the market, and the pickup truck will hold the largest market share by vehicle type.

E-commerce expansion and urban logistics drive the market growth.

Stringent emission regulations and compliance costs hamper market growth.

Ford, General Motors, and Toyota, among others, lead the global light duty truck market.

In 2025, the North American region led the global market, with the U.S. dominating the region.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us