Refrigerated Trailer Market Size, Share & Industry Analysis, By Trailer Type (Single-temperature refrigerated trailers and Multi-temperature refrigerated trailers), By Refrigeration Technology (Diesel-powered refrigeration, Hybrid refrigeration and Electric refrigeration), By End-User Industry (Food & Beverages, Pharmaceutical & Healthcare, Chemicals and others) and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

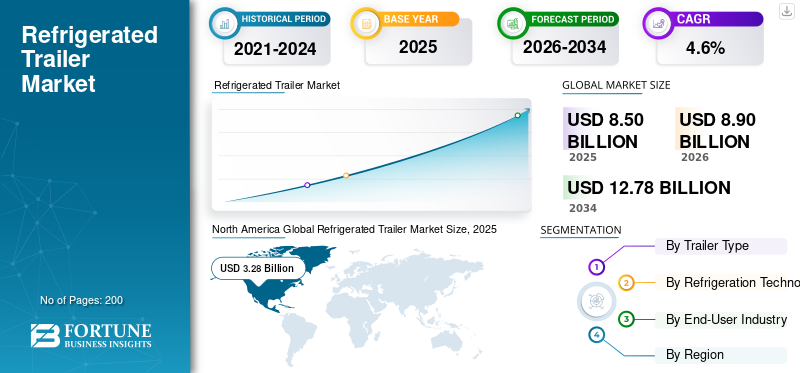

The global refrigerated trailer market size was valued at USD 8.50 billion in 2025. The market is projected to grow from USD 8.90 billion in 2026 to USD 12.78 billion by 2034, exhibiting a CAGR of 4.6% during the forecast period. North America dominated the global market with a market share of 38.59% in 2025.

The global refrigerated trailer market refers to the industry that designs and manufactures temperature-controlled trailers used to move goods that must stay within strict temperature ranges during transport. These trailers are essential for everyday logistics, supporting the movement of food and beverage products, pharmaceuticals, chemicals, and agricultural goods across domestic and international supply chains. As global trade becomes more time-sensitive and quality-driven, the role of the refrigerated trailer industry has become increasingly critical.

Market growth is strongly tied to the expansion of cold chain infrastructure, particularly in regions where food loss and temperature inconsistency were previously major challenges. Changing consumer habits, including higher consumption of frozen and chilled products, have increased the need for dependable refrigerated transport. At the same time, the growth of organized retail, cross-border food trade, and pharmaceutical distribution has led to a rising demand for trailers that can reliably maintain temperature throughout long-distance journeys. In many markets, stricter food safety and drug-handling regulations have turned refrigerated transport into a basic requirement rather than an optional upgrade.

Over the forecast period, the market is expected to grow steadily, driven by ongoing technological advancements. Trailer manufacturers such as Schmitz Cargobull, Kögel Trailer, and Great Dane are increasingly adopting real-time temperature monitoring, more fuel-efficient refrigeration systems, and structurally optimized trailer designs. These innovations allow fleet operators to monitor performance in real time, reduce cargo loss, and meet compliance requirements more easily.

Refrigerated trailers are widely used for transporting frozen food, dairy products, fresh fruits and vegetables, vaccines, biologics, and specialty chemicals. The market also benefits from fleet replacement and modernization programs, as logistics companies invest in newer equipment to improve efficiency and comply with tightening regulations. Together, these factors continue to push the refrigerated trailer market size upward, particularly in Europe and the Asia Pacific, where cold-chain investments remain a priority.

Download Free sample to learn more about this report.

REFRIGERATED TRAILER MARKET Key Takeaways

- 2025 Market Size: USD 8.50 billion

- 2026 Market Size: USD 8.90 billion

- 2034 Forecast Market Size: USD 12.78 billion

- CAGR: 4.6% from 2026–2034

- North America dominated the refrigerated trailer market with a 38.59% share in 2025.

- The multi-temperature segment is expected to witness strong growth at a CAGR of 5.8% during the forecast period.

- The electric refrigeration technology segment is projected to expand at a CAGR of 11.1% over the forecast period.

North America

North America held the leading position in the market, supported by a mature cold chain network, strong replacement demand, and widespread adoption of temperature-controlled transportation.

Europe

Europe maintained a significant market presence, driven by stringent food safety regulations, cross-border trade activities, and established cold logistics infrastructure.

Asia Pacific

Asia Pacific is expected to record the fastest growth, fueled by expanding cold chain infrastructure, increasing consumption of frozen and processed foods, and rising logistics investments.

U.S.

The U.S. remains the largest contributor, driven by extensive long-haul refrigerated freight, a mature frozen and chilled food distribution network, and continuous investment by large logistics fleets in advanced refrigerated trailers.

Japan

Market growth is supported by increasing demand for high-quality cold chain logistics, food safety requirements, and the adoption of advanced refrigerated transportation solutions.

Read More

REFRIGERATED TRAILER MARKET TRENDS

Integration of Telematics for Smarter Trailer Monitoring Leads to Market Trends

A major trend in the refrigerated trailer industry is the widespread adoption of telematics and connectivity solutions. These systems allow fleet managers to track temperature, location, and performance in real time, enabling proactive decision-making and stronger compliance with food safety regulations. Telematics is becoming a standard rather than an optional feature in new refrigerated trailer configurations.

- For instance, the refrigerated transport industry is embracing telematics and data analytics to improve temperature control accuracy and supply chain visibility.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Cold Chain Infrastructure Boosts Refrigerated Trailer Demand

Investment in cold chain infrastructure worldwide continues to expand as food safety standards tighten and demand for refrigerated goods rises. Improved cold storage facilities, transportation hubs, and logistics networks make it easier for businesses to maintain product integrity from origin to destination. This expansion increases the need for dependable refrigerated transport capacity, propelling the refrigerated trailer industry forward as logistics providers upgrade and expand their fleets.

- For instance, India’s government has approved subsidies for cold chain projects, encouraging companies to strengthen their temperature-controlled logistics networks.

MARKET RESTRAINTS

High Upfront and Operating Costs Limit Fleet Expansion

The high purchase price of refrigerated trailers, coupled with ongoing fuel and maintenance costs, can deter smaller operators from expanding or modernizing their fleets. These financial barriers are especially impactful in developing regions, slowing adoption rates even as demand for cold logistics grows. Cost concerns thus act as a restraint on refrigerated trailer market growth during the early stages of industry expansion.

MARKET OPPORTUNITIES

Digital and Energy-Efficient Refrigeration Technologies Gain Traction

Advances in digital controls, telematics, and energy-efficient refrigeration systems present significant opportunities for the global refrigerated trailer market. These innovations help reduce fuel consumption, improve temperature control accuracy, and offer real-time performance visibility, benefits that appeal to logistics firms aiming to cut waste and enhance quality assurance.

- For example, Carrier Transicold’s Vector eCool fully electric refrigeration system demonstrates the industry’s shift toward sustainable, energy-efficient cold transport solutions.

MARKET CHALLENGES

Evolving Emissions and Refrigerant Regulations Increase Compliance Burden

The refrigerated trailer market is challenged by increasingly complex environmental and refrigerant-related regulations across regions. Manufacturers must redesign components, adopt new refrigerants, and meet diverse standards, which raises development costs and slows product rollout. These changing regulations create uncertainty and operational strain for both OEMs and fleet operators.

- For instance, the EU’s updated F-gas regulation requires refrigerant transitions, compelling manufacturers to redesign temperature-control equipment.

Segmentation Analysis

By Trailer Type

Single-Temperature Trailers Dominate the Segmental Growth Due to Operational Simplicity

On the basis of trailer type, the global refrigerated trailer market is segmented into single-temperature and multi-temperature refrigerated trailers.

Single-temperature refrigerated trailers lead the market as they are well-suited for bulk transport of uniform cargo such as frozen foods and dairy. Their simpler configuration, lower upfront cost, and ease of operation make them the preferred choice for long-distance food logistics. These trailers also align with replacement-driven demand, particularly among large fleets focused on reliability and cost efficiency.

- For instance, Fahrzeugwerk Bernard Krone GmbH emphasizes single-temperature refrigerated trailers as a core solution for transporting large volumes of food and frozen goods.

Multi-temperature segment is expected to grow at a CAGR of 5.8% over the forecast period.

By Refrigeration Technology

Diesel-Powered Systems Remain the Primary Choice Due to Proven Reliability and Long-Haul Independence

On the basis of refrigeration technology, the market is segmented into diesel-powered, hybrid, and electric refrigeration.

Diesel-powered refrigeration systems continue to dominate the market due to their proven reliability, long operating range, and suitability for continuous long-haul operations. Fleet operators rely on dieselsystems to maintain consistent cooling even in areas with limited charging infrastructure. Despite emerging alternatives, diesel technology remains central to refrigerated transport, where uptime and flexibility are critical.

- For instance, Thermo King notes that diesel-powered refrigeration units remain widely used for long-distance refrigerated transport requiring uninterrupted cooling performance.

The electric refrigeration technology segment is expected to grow at a CAGR of 11.1% over the forecast period.

By End-User Industry

To know how our report can help streamline your business, Speak to Analyst

On the basis of end-user industry, the market is segmented into food & beverages, pharmaceutical & healthcare, chemicals, and others.

The food and beverage segment dominates the global refrigerated trailer market share because temperature-controlled transport is essential for preserving freshness, safety, and shelf life. The rising consumption of frozen food, dairy, meat, and fresh produce has increased the dependence on refrigerated trailers across long-haul and regional logistics. Growth is further supported by stricter food safety regulations and expanding cold-chain distribution networks linking producers, processors, and retailers.

- For example, the U.S. Department of Agriculture highlights refrigerated transportation as critical to maintaining quality and safety across the national food supply chain.

The pharmaceuticals & healthcare segment is growing at a CAGR of 5.9% over the forecast period.

Refrigerated Trailer Market Regional Outlook

By region, the global refrigerated trailer market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Global Refrigerated Trailer Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominates the global refrigerated trailer market due to its highly developed cold logistics ecosystem, strong replacement demand, and widespread use of temperature-controlled transport across food, pharmaceutical, and retail supply chains. Fleet modernization and compliance-driven upgrades continue to support steady growth.

The U.S. remains the largest contributor, driven by extensive long-haul refrigerated freight, a mature frozen and chilled food distribution network, and continuous investment by large logistics fleets in advanced refrigerated trailers.

- For instance, in 2024, Wabash National Corporation highlighted continued demand for refrigerated trailers from U.S. food and grocery supply chains, supported by fleet replacement and cold logistics expansion.

Europe

Europe follows North America, supported by stringent food safety regulations, dense cross-border trade, and a well-established cold chain network. Demand is largely replacement-driven, with growing emphasis on efficient trailer designs and compliance-focused refrigeration systems across food and pharmaceutical logistics.

Asia Pacific

Asia Pacific represents the fastest-growing regional market, driven by expanding cold chain infrastructure, rising consumption of frozen and processed food, and improving logistics standards. Growth is fueled by new fleet additions rather than replacements as temperature-controlled transport penetration continues to increase.

Rest of the World

The Rest of the World market is smaller but steadily expanding as the adoption of cold logistics improves. The growth is supported by increasing food imports, healthcare distribution needs, and gradual investments in refrigerated transport infrastructure, although cost sensitivity continues to influence adoption rates.

COMPETITIVE LANDSCAPE

Key Industry Players

Established Trailer Manufacturers Compete Through Scale, Technology, and Reach

The competitive landscape of the global refrigerated trailer market is shaped by a mix of long-established trailer manufacturers and regionally strong players that specialize in temperature-controlled transport solutions. Competition in the refrigerated trailer industry is driven less by price alone and more by product reliability, engineering quality, regulatory compliance, and long-term customer relationships with logistics operators and food distributors.

Leading manufacturers focus heavily on improving insulation performance, durability, and load efficiency, as refrigerated trailers are expected to operate continuously under demanding conditions. Companies such as Schmitz Cargobull AG, Kögel Trailer GmbH & Co KG, Fahrzeugwerk Bernard Krone GmbH, and Wabash National Corporation consistently invest in upgrading trailer designs to reduce tare weight, improve thermal efficiency, and extend service life. These improvements help fleet operators lower operating costs while meeting stricter temperature-control standards.

Another key area of competition is the integration of technology. Manufacturers increasingly differentiate themselves through technological advancements, including real-time temperature tracking, telematics systems, and data-driven maintenance tools. These features allow logistics providers to monitor cargo conditions in real time, reduce spoilage risks, and demonstrate compliance with food and pharmaceutical regulations. As a result, technology has become a deciding factor in purchasing decisions rather than an optional add-on.

Geographic expansion also plays a critical role in gaining a competitive advantage. Several companies operate as diversified or utility trailer manufacturing company groups, enabling them to leverage production scale and regional manufacturing footprints. Expanding sales and service networks in high-growth regions such as the Asia Pacific allows manufacturers to capture new customers as cold chain infrastructure improves.

Overall, competition in the market is expected to intensify during the forecast period, as players balance cost control with innovation to address rising demand, sustainability expectations, and evolving regulatory requirements.

- For instance, in September 2025, logistics provider Manfreight deployed 100 new Schmitz Cargobull S.KO COOL refrigerated trailers, underscoring strong OEM demand and customer confidence in the quality and telematics performance of these trailers.

LIST OF KEY REFRIGERATED TRAILER COMPANIES PROFILED

- Schmitz Cargobull AG (Germany)

- Fahrzeugwerk Bernard Krone GmbH (Germany)

- Kögel Trailer GmbH Co KG (Germany)

- Wabash National Corporation (U.S.)

- Great Dane (U.S.)

- Lamberet SAS (France)

- Utility Trailer Manufacturing Company (U.S.)

- Chereau SAS (France)

- CIMC Vehicles (China)

- Hyundai Translead (South Korea)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Schmitz Cargobull positioned its S.KO COOL reefer as a trendsetter by pushing telematics as standard (incl. digital temperature recording) and introducing the S.CU dc90 transport refrigeration unit plus service options.

- July 2025: Utility Trailer and Cargobull North America announced a redesigned TRU featuring a high-efficiency microchannel condenser and radiator, making the upgrade available on all new units. The change targets better heat exchange and higher overall performance for hybrid TRUs.

- June 2025: Great Dane marked production of the 25,000th trailer at its Pennsylvania plant (milestone reached in May 2025). The announcement underlines ongoing capacity utilization and manufacturing scale in North America.

- May 2025: Kögel ceremonially opened a modern production facility for refrigerated vehicle panels at its Burtenbach headquarters, signaling investment in core reefer-body components and supply reliability.

- March 2025: Utility Trailer announced advanced options aimed at improving versatility and efficiency across its 3000R refrigerated trailer lineup (and 4000D-X composite vans). The move reflects OEM strategy: incremental spec upgrades that improve TCO and operational fit.

REPORT COVERAGE

The global refrigerated trailer market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Trailer Type, Refrigeration Technology, End-User Industry, and Region |

|

By Trailer Type |

· Single-temperature refrigerated trailers · Multi-temperature refrigerated trailers |

|

By Refrigeration Technology |

· Diesel-powered refrigeration · Hybrid refrigeration · Electric refrigeration |

|

By End-User Industry |

· Food & beverages · Pharmaceuticals & healthcare · Chemicals · Others |

|

By Region |

· North America (By Trailer Type, Refrigeration Technology, End-User Industry, and Country) o U.S. o Canada o Mexico · Europe (By Trailer Type, Refrigeration Technology, End-User Industry, and Country) o Germany o U.K. o France o Italy o Rest of Europe · Asia Pacific (By Trailer Type, Refrigeration Technology, End-User Industry, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Trailer Type, Refrigeration Technology, End-User Industry, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.50 billion in 2025 and is projected to reach USD 12.78 billion by 2034.

In 2025, the market value stood at USD 3.28 billion.

The market is expected to exhibit a CAGR of 4.6% during the forecast period of 2026-2034.

The food & beverages segment led the market by end-user industry.

Expansion of cold chain infrastructure is driving the global refrigerated trailer market.

Schmitz Cargobull, Krone Gorup, Kögel Trailer, and Great Dane are some of the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us