Automotive DevOps Services Market Size, Share & Industry Analysis, By Service Type (Continuous Integration & Continuous Delivery (CI/CD) Services, Testing & Validation Automation Services, OTA Update Management Services, and Cloud & Infrastructure Management Services), By Application (ADAS & Autonomous Driving, Powertrain & Battery Management, Telematics & Fleet Management, and Others), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By End User (Automotive OEMs, Tier-1 Suppliers, Automotive Software Companies, and Mobility Service Providers), and Regional Forecast, 2026–2034

Automotive DevOps Services Market Size and Future Outlook

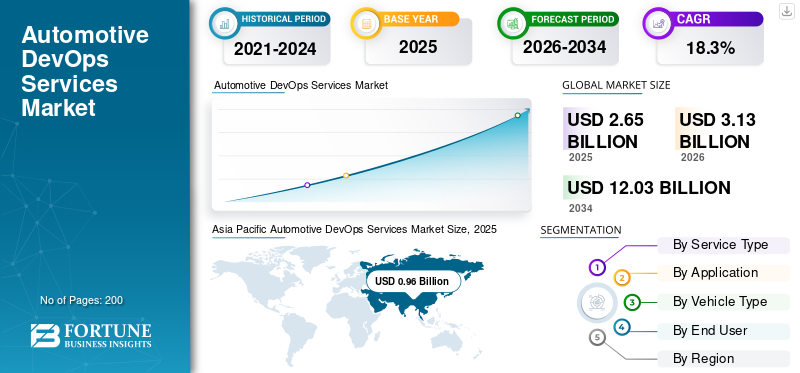

The global automotive DevOps services market size was valued at USD 2.65 billion in 2025. The market is projected to grow from USD 3.13 billion in 2026 to USD 12.03 billion by 2034, with a CAGR of 18.3% over the forecast period. Asia Pacific dominated the automotive devops services market with a market share of 36.22% in 2025.

Automotive DevOps services refer to software development, testing, deployment, cybersecurity, and cloud service management practices used to accelerate automotive software delivery. These services enable continuous integration, OTA updates, automated validation, and secure software lifecycle management for connected, electric, autonomous, and software-defined vehicles across OEM and supplier ecosystems. The rapid adoption of software-defined vehicles, connected cars, electric vehicles, and ADAS technologies primarily drives the market. Increasing OTA software updates, evolving automotive cybersecurity requirements, and the adoption of cloud-native vehicle architectures are accelerating DevOps adoption. OEMs and Tier-1 suppliers are investing heavily in automated testing, CI/CD pipelines, and faster software release cycles to reduce development complexity, improve vehicle performance, and ensure regulatory compliance.

Major players include Accenture, Capgemini, IBM, TCS, Infosys, HCLTech, Cognizant, Wipro, KPIT, Bosch, and Continental. The market trend is shifting toward AI-driven DevSecOps, cloud-based automotive software platforms, and OTA lifecycle management. Companies are expanding partnerships with automotive companies and OEMs to support software-defined vehicle development, autonomous-driving software integration, and connected-mobility ecosystems.

Download Free sample to learn more about this report.

AUTOMOTIVE DevOps SERVICES MARKET TRENDS

Rising Adoption of Software-Defined Vehicles to Accelerate Market Expansion

Automotive manufacturers are increasingly shifting toward software-defined vehicle (SDV) architectures, in which vehicle functions are continuously upgraded via software rather than hardware modifications. This transition is significantly increasing the demand for automotive DevOps services, especially CI/CD pipelines, automated testing, OTA deployment, and cloud-native software orchestration. OEMs are focusing on shortening software release cycles and enabling feature upgrades throughout the vehicle lifecycle. SDV development also requires seamless integration across infotainment, ADAS, telematics, and battery-management platforms, making DevOps frameworks critical for automotive engineering operations. The growing adoption of centralized computing architectures and AI-enabled vehicle platforms further supports long-term market expansion across passenger and commercial vehicles.

- In November 2024, Bosch Engineering joined SDVerse’s software marketplace ecosystem to accelerate software-defined vehicle engineering and vehicle software deployment capabilities.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Automotive Cybersecurity Regulations to Drive DevSecOps Adoption

Connected vehicles, OTA-enabled systems, and cloud-integrated automotive platforms are increasing cybersecurity risks across the automotive ecosystem. Automotive OEMs and Tier-1 suppliers are therefore investing heavily in DevSecOps, continuous monitoring, vulnerability validation, and secure software lifecycle management. Global cybersecurity regulations are compelling manufacturers to implement secure software update systems and cybersecurity management processes throughout the vehicle lifecycle.

Automotive DevOps services are becoming essential for ensuring regulatory compliance, software traceability, threat detection, and rapid patch deployment across connected vehicle fleets. As vehicle architectures become increasingly software-centric, the integration of cybersecurity into development and deployment environments is evolving automotive from an optional capability to a mandatory engineering requirement across global automotive markets.

- For instance, in August 2024, AWS highlighted UNECE WP.29 cybersecurity regulations requiring OEMs to maintain cybersecurity management systems and to secure OTA software update mechanisms for connected vehicles.

MARKET RESTRAINTS

High Integration Complexity to Restrain Large-Scale DevOps Deployment

Automotive software ecosystems involve multiple electronic control units, legacy vehicle architectures, safety-critical validation requirements, and highly fragmented supplier networks. Integrating DevOps practices across these environments remains technically complex and resource-intensive. Many OEMs still use legacy development frameworks originally designed for hardware-centric vehicle programs rather than for continuous software deployment. Differences in software stacks, cloud infrastructure, testing standards, and OTA deployment architectures often slow implementation timelines and increase operational costs. In addition, safety certification requirements for automotive systems require extensive validation before software deployment, reducing the speed advantages typically associated with DevOps models. These integration and compliance challenges continue to restrain rapid deployment, especially among smaller OEMs and regional suppliers with limited software engineering maturity.

MARKET OPPORTUNITIES

Increasing Use of OTA Platforms Creates Strong Future Growth Opportunities

The growing deployment of over-the-air software updates is creating significant long-term opportunities for automotive DevOps services providers. Automotive manufacturers increasingly use OTA platforms to remotely deploy performance upgrades, cybersecurity patches, battery-optimization features, infotainment improvements, and ADAS enhancements. This shift is enabling vehicles to receive continuous software improvements throughout their operational lifecycle, increasing the need for scalable CI/CD pipelines, automated software validation, cloud orchestration, and secure deployment management. Commercial vehicle fleets and electric vehicles are expected to become major contributors to OTA-driven DevOps demand, driven by their high software update frequency and connected fleet-management requirements. As OTA capabilities expand globally, service providers offering secure software delivery infrastructure and cloud-native automotive development platforms are expected to benefit substantially.

- For instance, in January 2025, Bosch announced the integration of NVIDIA DRIVE AGX Thor into next-generation centralized vehicle compute architectures to support AI-driven software-defined vehicle functionality and scalable software deployment.

MARKET CHALLENGES

Shortage of Specialized Professionals to Challenge Market Growth

The increasing complexity of software-defined vehicles is creating strong demand for engineers skilled in automotive software integration, cloud-native development, cybersecurity validation, AI-driven testing, and OTA lifecycle management. However, the availability of professionals with expertise in both automotive engineering and DevOps methodologies remains limited globally. Automotive software development requires knowledge of functional safety standards, embedded systems, cybersecurity compliance, and real-time validation environments, making workforce development more difficult than traditional enterprise DevOps implementation. This shortage of talent increases project costs, delays deployment timelines, reducess time-to-market efficiency, and creates operational pressure on OEMs and Tier-1 suppliers as they accelerate their SDV programs. Competition for skilled automotive software engineers is intensifying across North America, Europe, China, India, and Japan as automakers rapidly expand internal software capabilities.

- For instance, in September 2024, Cummins, Bosch Global Software, ETAS, and KPIT launched an open telematics software initiative to simplify SDV software development and address the growing complexity of automotive software engineering.

Segmentation Analysis

By Service Type

Rapid Rise of Software-Defined Vehicles Boosts Testing & Validation Automation Service Segment Growth

Based on service type, the market is segmented into continuous integration & continuous delivery (CI/CD) services, testing & validation automation services, DevSecOps & cybersecurity services, OTA update management services, and cloud & infrastructure management services.

Testing & validation automation services dominate the market as automotive software environments require continuous regression testing, functional safety validation, ADAS simulation, OTA verification, and real-time software reliability checks. The rapid rise of software-defined vehicles and connected automotive platforms has significantly increased testing workloads across OEMs and Tier-1 suppliers. Automated validation tools help reduce software deployment risks while improving release efficiency and compliance with automotive safety standards.

The DevSecOps & cybersecurity services segment is projected to grow at a CAGR of 21.4% over the forecast period.

- For instance, in June 2024, Siemens expanded its automotive software validation by enhancing AI-powered testing in its PAVE360 automotive digital twin platform.

By Application

ADAS and Autonomous Driving Segment Leads due to Increasing Investment in Centralized Software Architectures

Based on application, the market is segmented into ADAS & autonomous driving, infotainment & connectivity, powertrain & battery management, telematics & fleet management, and OTA software updates.

The ADAS & autonomous driving segment dominates the market as autonomous systems require continuous software integration, sensor fusion validation, AI model testing, real-time updates, and cybersecurity monitoring. Automotive manufacturers are increasingly investing in centralized software architectures and AI-enabled driving systems, increasing DevOps deployment across automotive engineering operations. Growing penetration of Level 2 and Level 3 autonomous vehicles further supports long-term demand for software lifecycle management.

The powertrain & battery management segment is projected to grow at a CAGR of 21.1% over the forecast period.

- For instance, in March 2024, NVIDIA announced an expanded automotive partnership ecosystem supporting AI-driven autonomous vehicle development and centralized software-defined vehicle computing platforms.

By Vehicle Type

SUVs Segment to Lead due to its Ability to Support Larger Computing Architectures

Based on vehicle type, the market is segmented into Hatchback/Sedan, SUV, LCV, and HCV.

The SUV segment dominates the market and is projected to grow at a CAGR of 20.5% over the forecast period due to higher integration of connected infotainment systems, ADAS technologies, OTA software functionality, and premium digital cockpit platforms. Global OEMs increasingly prioritize SUVs for electric and software-defined vehicle launches as these vehicles support larger computing architectures and higher-value software ecosystems. The segment also benefits from strong consumer demand across North America, China, Europe, and the Middle East.

The HCV segment is projected to grow at a CAGR of 18.2% over the forecast period.

- For instance, in October 2024, Rivian introduced enhanced software and OTA functionality updates for its R1S SUV platform to improve driver assistance and connected vehicle performance.

To know how our report can help streamline your business, Speak to Analyst

By End User

Rising Investments in DevOps Pipelines Boost Automotive OEM Segment Growth

Based on end user, the market is segmented into automotive OEMs, Tier-1 suppliers, automotive software companies, and mobility service providers.

Automotive OEMs dominate the market as vehicle manufacturers are increasingly developing internally proprietary software stacks, centralized computing platforms, OTA ecosystems, and autonomous driving systems. OEMs are heavily investing in DevOps pipelines to accelerate software deployment cycles, reduce dependency on fragmented supplier architectures, and improve software lifecycle control. The transition toward software-defined vehicles is driving up internal software engineering budgets at global automotive manufacturers.

The automotive software companies segment is projected to grow at a CAGR of 20.9% over the forecast period.

- For instance, in April 2024, Volkswagen’s CARIAD expanded its collaboration with Bosch to accelerate the development of automated driving software and scalable vehicle software platforms.

AUTOMOTIVE DevOps SERVICES MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

NORTH AMERICA

Asia Pacific Automotive DevOps Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America continues to hold a significant position in the market due to the rapid adoption of software-defined vehicles, advanced cloud-native automotive development, and strong OTA deployment capabilities. The region benefits from high ADAS penetration, connected vehicle ecosystems, and autonomous mobility investments across the U.S. and Canada. Automotive OEMs are increasingly integrating DevSecOps, AI-driven validation, and centralized software architectures into vehicle development cycles. Rising cybersecurity compliance requirements and the expansion of EV software platforms further support market growth. The region also benefits from the strong presence of automotive software engineering providers and large-scale automotive cloud infrastructure deployment.

U.S. AUTOMOTIVE DevOps SERVICES MARKET

The U.S. dominates the North American market and is estimated to reach USD 0.72 billion by 2026. Strong SDV investments, OTA-enabled vehicle deployments, autonomous driving development, and cloud-based automotive software engineering continue to support market expansion. The country also benefits from high connected vehicle penetration, strong OEM digital transformation programs, and growing adoption of AI-enabled software validation and cybersecurity platforms across passenger and commercial vehicle ecosystems.

EUROPE

Europe remains a technologically advanced market, driven by premium automotive manufacturing, stringent cybersecurity regulations, and accelerated EV adoption. Automotive OEMs across the region are increasing investments in software-defined vehicle architectures, OTA lifecycle management, and AI-powered testing environments. The transition toward electrification and centralized vehicle computing platforms continues to increase demand for CI/CD, automated validation, and cybersecurity integration services. Strong engineering capabilities among OEMs and Tier-1 suppliers also support large-scale deployment of automotive cloud infrastructure and connected mobility software ecosystems across the region.

U.K. AUTOMOTIVE DevOps SERVICES MARKET

The U.K. market is likely to reach USD 0.10 billion by 2026, supported by rising connected vehicle deployments, autonomous mobility research, and the expansion of cloud-native software engineering. The country continues to strengthen automotive AI, simulation testing, and OTA software management capabilities by increasing investments in software-defined vehicles and fostering collaborations between automotive technology providers and OEM engineering centers.

GERMANY AUTOMOTIVE DevOps SERVICES MARKET

Germany accounts for approximately 28.2% share of the European market due to the strong presence of premium automotive OEMs, advanced vehicle software engineering, and high ADAS deployment intensity. The country remains a leading hub for automotive cybersecurity integration, SDV architecture development, and EV software platform engineering, supported by extensive investments in autonomous driving and centralized computing systems.

ASIA PACIFIC

Asia Pacific represents the largest automotive DevOps services market share globally due to large-scale vehicle production, rapid EV deployment, strong connected car adoption, and aggressive software-defined vehicle development. China, Japan, South Korea, and India are significantly expanding automotive software engineering capabilities, OTA deployment ecosystems, and cloud-native vehicle architectures. The region also benefits from high investments in battery management software, AI-powered ADAS systems, and automotive cybersecurity frameworks. Rising government support for EVs and smart mobility infrastructure further strengthens long-term demand for automotive DevOps services across both passenger and commercial vehicle segments.

CHINA AUTOMOTIVE DevOps SERVICES MARKET

China dominates the Asia Pacific market with approximately 60.3% regional share, driven by its leadership in EV production, software-defined vehicle deployment, and OTA-enabled automotive ecosystems. Strong domestic automotive software development capabilities, adoption of centralized computing architecture, and autonomous driving investments continue to accelerate demand for testing automation, DevSecOps, and cloud-based vehicle software lifecycle management services.

INDIA AUTOMOTIVE DevOps SERVICES MARKET

India is projected to record the highest CAGR of 22.2% during the forecast period. Rapid growth in automotive software engineering centers, rising EV production, the expansion of connected mobility, and increasing cloud adoption across automotive development environments are some of the key factors driving market growth. Expanding OEM digital transformation initiatives and rising ADAS integration are also strengthening demand for automated testing and CI/CD deployment services.

JAPAN AUTOMOTIVE DevOps SERVICES MARKET

Japan is estimated to reach USD 0.16 billion by 2026, driven by its advanced automotive engineering ecosystem and growing investments in autonomous-driving software, EV architectures, and vehicle cybersecurity systems. A strong focus on functional safety validation, OTA integration, and AI-powered automotive software development continues to support the increasing adoption of Automotive DevOps Services among Japanese OEMs and Tier-1 suppliers.

SOUTH AMERICA

South America is gradually strengthening its position in the market through increasing connected vehicle adoption, telematics deployment, and fleet digitalization initiatives. Automotive manufacturers are expanding investments in OTA functionality, cloud-based vehicle diagnostics, and software lifecycle management to improve operational efficiency and connected mobility capabilities. The growing integration of infotainment systems and rising commercial fleet connectivity are also supporting demand for testing automation and cloud infrastructure management services. Brazil remains the primary automotive software engineering and vehicle manufacturing hub across the region.

BRAZIL AUTOMOTIVE DevOps SERVICES MARKET

Brazil dominates the South American market, with approximately 61.1% regional share, driven by its large automotive manufacturing base and increasing connected vehicle adoption. Rising telematics integration, fleet management software deployment, and cloud-enabled automotive engineering activities continue to strengthen demand for DevOps services. Growing SUV penetration and automotive digital transformation programs further support long-term investments in software lifecycle management.

MIDDLE EAST & AFRICA

The market is growing steadily due to rising connected vehicle adoption, premium SUV demand, and the expansion of smart mobility infrastructure. GCC countries are increasingly investing in cloud-native mobility ecosystems, OTA software deployment, and cybersecurity-enabled automotive platforms. Commercial fleet modernization and telematics integration across the supply chain, logistics, and automotive sectors are also supporting the regional automotive DevOps services market growth. The adoption of centralized computing systems and connected infotainment technologies is expected to increase further as software-defined vehicle ecosystems expand across the region.

UAE AUTOMOTIVE DevOps SERVICES MARKET

The UAE market is projected to grow at a CAGR of 20.5% during the forecast period, driven by rising smart mobility investments, premium demand for connected vehicles, and the expansion of OTA-enabled automotive ecosystems. A strong focus on AI-driven transportation infrastructure, autonomous mobility initiatives, and cloud-based fleet management systems continues to support the rising adoption of automotive software engineering, validation automation, and cybersecurity deployment services.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Focus on Collaborations to Accelerate Software Development

The global automotive DevOps services market is moderately fragmented, with competition driven by automotive software engineering expertise, cloud-native development capabilities, OTA lifecycle management, and vehicle cybersecurity integration. Major players, including Accenture, Capgemini, IBM, TCS, Infosys, HCLTech, Cognizant, KPIT, Bosch, and Wipro, compete through SDV engineering platforms, automated testing frameworks, DevSecOps integration, and AI-enabled automotive software validation services. Companies are strengthening their competitive positioning by expanding partnerships with OEMs and Tier-1 suppliers, investing in centralized vehicle software architectures, and developing scalable cloud-based deployment ecosystems for connected, electric, and autonomous vehicles. Strategic collaborations with hyperscalers, cybersecurity providers, and automotive semiconductor firms are becoming increasingly common as organizations seek to accelerate software development.

For instance, in January 2025, ETAS and AWS expanded collaboration to accelerate software-defined vehicle development through cloud-based automotive DevOps, cybersecurity management, and OTA software deployment capabilities for OEMs globally.

LIST OF KEY AUTOMOTIVE DevOps SERVICES COMPANIES PROFILED

- Accenture plc (Ireland)

- Capgemini SE (France)

- Tata Consultancy Services (India)

- Infosys Limited (India)

- HCLTech (India)

- Wipro Limited (India)

- Cognizant Technology Solutions (U.S.)

- KPIT Technologies Ltd. (India)

- Luxoft, a DXC Technology Company (Switzerland)

- Bosch Global Software Technologies (Germany)

- Elektrobit Automotive GmbH (Germany)

- AVL List GmbH (Austria)

- IBM Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Google announced Android Automotive OS for Software-Defined Vehicles, extending AAOS beyond infotainment into non-safety vehicle software. The open platform supports modular architecture, granular updates, diagnostics, communication layers, Renault Trafic e-Tech validation, Qualcomm scaling, reduced development cost, and faster deployment for OEM software programs.

- January 2026: VDA highlighted growing automotive open-source collaboration around Eclipse Software Defined Vehicle and Eclipse S-CORE. The initiative brings OEMs, suppliers, cloud providers, and software companies together to build shared automotive-grade software stacks, backend blocks, digital twins, OTA campaign management, traceability, and reusable components for next-generation vehicle platforms.

- January 2026: GlobalLogic and Elektrobit expanded their long-standing partnership to accelerate the development of next-generation software-defined vehicles. The alliance focuses on high-performance computing, SDV platforms, global market enablement, AUTOSAR middleware, infotainment, connectivity, functional safety, cybersecurity, ASPICE 4.0, ISO 21434 compliance, and scalable software engineering for global automotive customers.

- January 2026: L&T Technology Services secured a multi-year Mobility engineering and R&D agreement from a leading global automotive OEM. The engagement covers advanced software, connectivity, secure development practices, and digital engineering across multiple vehicle technology domains, strengthening LTTS’s role in supporting next-generation premium mobility and automotive software programs.

- December 2025: ETAS announced a collaboration with Microsoft to launch ETAS calibration and analytics tools on Microsoft Marketplace for CES 2026. The Azure-based toolchain enables cloud calibration, shift-left validation, big-data analysis, faster iteration cycles, and AI-driven orchestration, helping OEMs and suppliers accelerate software-defined vehicle development.

REPORT COVERAGE

The global automotive DevOps services market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on rapid technological advancements, new product launches, key industry developments, strategic partnerships, mergers & acquisitions. The market forecast provides a comprehensive competitive landscape, including the most significant global market shares, emerging opportunities, and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 18.3%from 2026 to 2034 |

| Unit | Value (USD billion) |

| Segmentation | By Service Type, By Application, By Vehicle Type, By End User, and By Region. |

| By Service Type |

|

| By Application |

|

| By Vehicle Type |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.65 billion in 2025 and is projected to reach USD 12.03 billion by 2034.

In 2025, the market value stood at USD 0.96 billion.

The market demand is expected to grow at a CAGR of 18.3% from 2026 to 2034.

The SUV segment leads the market share by vehicle type.

Rapid adoption of software-defined vehicles, connected cars, electric vehicles, and ADAS technologies is the key factor driving the market.

Key market players include Accenture, Capgemini, IBM, TCS, Infosys, HCLTech, Cognizant, and Wipro.

The Asia Pacific region captures the largest share of the market.

North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us