Automotive Interior Market Size, Share & Industry Analysis, By Material Type (Fabric, Genuine Leather, Synthetic Leather, Plastics & Polymers, Metal Materials, Wood Trims, & Composite Materials), By Vehicle Type (Hatchback & Sedans, SUVs, LCVs, & HCVs), By Interior Feature Level (Standard Interiors, Comfort-Enhanced Interiors, & Others), By Sales Channel (OEM & Aftermarket), By Component Type (Seating Components, Instrument Panel & Dashboard Components, Center Console Components, Door Interior Components, Headliner Components, Flooring Components, & Others), and Regional Forecast, 2026-2034

Automotive Interior Market Size and Future Outlook

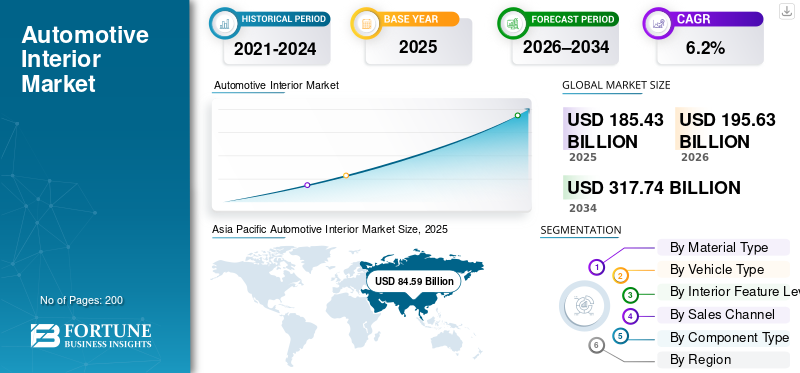

The global automotive interior market size was valued at USD 185.43 billion in 2025. The market is projected to grow from USD 195.63 billion in 2026 to USD 317.74 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. Asia Pacific dominated the automotive interior market with a market share of 45.62% in 2025.

Automotive interior refers to all components inside a vehicle, including seating, dashboard, trims, infotainment, controls, and materials, designed to enhance comfort, safety, functionality, and overall driving experience for occupants worldwide. Key market drivers include rising vehicle production, growing consumer preference for comfort and premium features, advancements in interior technologies, increasing focus on safety, and demand for lightweight, sustainable materials across global automotive markets.

The market includes major players such as Faurecia, Adient, Lear Corporation, and Magna International, which compete through innovative materials, smart interiors, lightweight designs, sustainability, and enhanced comfort and safety solutions.

Download Free sample to learn more about this report.

Automotive Interior Market KEY TAKEAWAYS

- 2025 Market Size: USD 185.43 billion

- 2026 Market Size: USD 195.63 billion

- 2034 Forecast Market Size: USD 317.74 billion

- CAGR: 6.2% from 2026–2034

- Asia Pacific dominated the market with a 45.62% share in 2025.

- Synthetic Leather segment is projected to grow at a CAGR of 8.1%.

- Hatchbacks & Sedans segment is projected to grow at a CAGR of 5.4%.

Asia Pacific

Strongest and fastest-growing region. Driven by high vehicle production in China, Japan, India, and South Korea along with rising demand for premium and EV interior features.

Europe

Strong growth driven by premium interiors, EV adoption, and demand for sustainable and lightweight materials.

North America

USD 33.09 billion in 2026. Growth supported by SUVs, pickup trucks, infotainment systems, and connected vehicle technologies.

U.S.

USD 33.09 billion in 2026. Demand led by SUV dominance, advanced infotainment systems, and aftermarket customization.

Japan

USD 13.13 billion in 2026. Supported by OEM strength, technological innovation, and premium interior materials adoption.

Read More

AUTOMOTIVE INTERIOR MARKET TRENDS

Integration of Smart, Connected, and Sustainable Materials as a Key Market Trend

One of the major market trends is the convergence of smart technologies with sustainable materials. Manufacturers are integrating digital dashboards, connected infotainment, and voice-controlled systems while increasing the use of recycled fabrics, bio-based plastics, and lightweight composites. This trend reflects shifting consumer preferences and regulatory pressure to reduce environmental impact and increases product demand, driving long-term market expansion and shaping innovation strategies across global automotive platforms.

- In November 2025, ECARX deepened its partnership with Volkswagen Group to supply advanced digital cockpit solutions, integrating the ECARX Antora 1000 computing platform, including 7 nm SE1000 SoC and modular Cloudpeak software with Google Automotive Services, plus cost-optimized Antora 500 for offline variants, enhancing infotainment and HMI across multiple Volkswagen models in Latin America.

MARKET DYNAMICS

MARKET DRIVERS

Rising Consumer Demand for Enhanced Comfort and Premium Features to Drive Market Growth

The surging consumer expectations for comfort, aesthetics, and advanced in-cabin experiences are driving the demand for interior upgrades. Features such as ergonomic seating, premium upholstery, ambient lighting, and advanced infotainment systems are increasingly influencing purchase decisions. Automakers are prioritizing interior differentiation to enhance brand value and customer satisfaction. This shift is encouraging higher investment in interior components, supporting consistent automotive interior market growth across both mass-market and premium vehicle segments globally.

- In August 2025, General Motors outlined its award-winning interior design process, highlighting the use of VR/AR digital modelling, full-size physical prototypes, and ergonomics-driven UX/UI integration with large portrait-oriented infotainment screens in models such as GMC Yukon Denali Ultimate and Cadillac OPTIQ.

MARKET RESTRAINTS

High Cost of Advanced Interior Technologies to Restrain Product Adoption

The adoption of advanced automotive interior technologies is restrained by their high development and integration costs. Smart displays, digital cockpits, premium materials, and connected infotainment systems significantly increase vehicle prices. These cost pressures are particularly impactful in price-sensitive and emerging markets, limiting penetration in entry-level vehicles. Additionally, rising raw material costs and complex manufacturing processes further challenge manufacturers’ ability to offer advanced interiors at competitive price points.

MARKET OPPORTUNITIES

Electrification and Autonomous Vehicles to Create New Interior Design Opportunities

The increasing adoption of electric and autonomous vehicles is creating strong opportunities for innovative automotive interior solutions. Reduced powertrain complexity and changing driver roles allow greater flexibility in cabin layout and functionality. Interiors are evolving into multifunctional spaces focused on comfort, rear seat entertainment, and productivity. This transformation enables interior suppliers to introduce modular designs, advanced displays, and personalized digital environments, unlocking new revenue streams during the forecast period.

- In January 2024, Yanfeng unveiled its Electric Vehicle Interior (EVI) concept at CES, eliminating traditional dashboards and consolidating cockpit functions into a Smart Cabin seat with active headrest audio, integrated safety systems, steer-by-wire controls, HMI displays, HVAC microclimate, and storage/charging features, simplifying assembly and reducing weight for future EV architectures.

MARKET CHALLENGES

Balancing Design Innovation with Safety and Regulatory Compliance Present Key Market Challenges

One of the key challenges in the market is balancing advanced design innovation with strict safety and regulatory requirements. Features such as large touchscreens, ambient lighting, and new materials must comply with crash safety, durability, and driver distraction norms. Managing diverse regulations across regions while maintaining aesthetic appeal, functionality, and cost efficiency complicates product development and extends validation timelines for interior manufacturers.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material Type

Cost Efficiency, Design Flexibility, and Lightweight Benefits to Drive Plastics & Polymers Segmental Dominance

Based on material type, the market is segmented into fabric, genuine leather, synthetic leather, plastics & polymers, metal materials, wood trims, and composite materials.

The plastics & polymers segment dominates the market due to its extensive use across dashboards, door panels, consoles, trims, and seating components. These materials offer superior design flexibility, lightweight advantages, durability, and cost efficiency compared to alternatives. Automakers prefer plastics and polymers to meet fuel-efficiency targets, safety requirements, and large-scale production needs. High adoption across passenger and commercial vehicles ensures consistent market demand and a strong market share globally.

- In January 2025, LyondellBasell launched a new Schulamid PA6/66 nylon grade for automotive interiors, offering improved flow, stiffness, and impact resistance that enhances parts molding efficiency, supports thinner-wall designs, and meets evolving OEM requirements for durability and lightweight performance.

The synthetic leather segment is the fastest-growing material category, expanding at a CAGR of 8.1% over the forecast period. The rising demand for premium aesthetics, sustainability, cost-effective alternatives to genuine leather, and easy maintenance is driving adoption across mid-range and luxury vehicle interiors.

By Vehicle Type

Rising Consumer Preference for Spacious, Premium, and Versatile Vehicles to Drive SUV Demand

Based on vehicle type, the market is segmented into hatchbacks & sedans, SUVs, LCVs, and HCVs.

The SUVs segment dominates and remains the fastest-growing vehicle type in the market due to rising consumer preference for spacious cabins, elevated comfort, and premium interior features. SUVs increasingly incorporate advanced infotainment, larger displays, configurable seating, and high-quality materials. Strong demand across urban and semi-urban markets, coupled with expanding electric and hybrid SUV portfolios, supports sustained market demand and reinforces the segment’s leading market share globally.

- In October 2025, Hyundai Motor launched the ELEXIO SUV in China with a 27-inch 4K widescreen interior display driven by a Qualcomm 8295 chip, a Cyber Eye HUD (30,000:1 contrast ratio), Dolby Atmos audio, and health/fatigue monitoring systems, enhancing cockpit performance and safety through advanced digital and ergonomic features.

The hatchbacks & sedans segment represents the second-largest market share and is projected to grow at a CAGR of 5.4% over the forecast period. Stable demand from cost-conscious consumers, high production volumes, and continued interior feature upgrades support steady growth across the global passenger car market.

By Interior Feature Level

High Volume Production and Cost-Sensitive Consumer Base to Support Standard Interiors Segment

By interior feature level, the market is divided into standard interiors, comfort-enhanced interiors, premium interiors, and luxury interiors.

The standard interiors segment accounts for the largest share in the market due to their widespread adoption across entry-level and mid-range vehicles. Automakers prioritize functional, cost-effective interior configurations to cater to price-sensitive consumers and high-volume production models. Standard seating, basic infotainment, and durable materials ensure broad applicability across regions. The strong demand from mass-market passenger vehicles sustains consistent market demand and reinforces the segment’s dominant position globally.

The premium interiors segment is the fastest-growing segment, expanding at a CAGR of 7.0% over the forecast period. Increasing consumer willingness to pay for comfort, advanced infotainment, ambient lighting, and premium materials is driving adoption across luxury and upper mid-segment vehicles worldwide.

- In December 2025, Nissan unveiled next-generation interior technologies featuring a fully digital cockpit, advanced HMI displays, enhanced connectivity architecture, and ergonomic cabin layout, aimed at improving driver interaction, comfort, and safety across upcoming passenger vehicle and electric model lineups globally.

By Sales Channel

Integrated Vehicle Design and Large-Scale Production Contracts to Drive OEM Segment Growth

By sales channel, the market is categorized into OEM and aftermarket.

The OEM segment dominates the market due to the direct integration of interior components during vehicle manufacturing. Automakers collaborate closely with interior suppliers to ensure design consistency, quality compliance, and cost optimization at scale. High vehicle production volumes, especially in passenger cars and SUVs, support strong OEM demand. Additionally, the increasing incorporation of advanced interior features at the factory level reinforces OEMs’ leading market share globally.

- In April 2024, Lucid Motors introduced advanced interior enhancements featuring a Glass Cockpit with a curved 5K display, pilot panel touchscreen, over-the-air software updates, and Surreal Sound Pro audio system, improving HMI responsiveness, personalization, and immersive cabin experience across Lucid Air models.

The aftermarket segment is the fastest-growing sales channel, expanding at a CAGR of 6.6% over the forecast period. Rising vehicle parc, customization demand, interior refurbishment needs, and replacement of worn components are accelerating aftermarket sales across both developed and emerging automotive markets.

By Component Type

To know how our report can help streamline your business, Speak to Analyst

Essential Role in Comfort, Safety, and Ergonomics to Drive Seating Components Segmental Leadership

By component type, the market comprises various segments such as seating components, instrument panel & dashboard components, center console components, door interior components, headliner components, flooring components, interior lighting components, HVAC interior components, and infotainment & HMI components.

The seating components segment holds the largest automotive interior market share due to their critical role in occupant comfort, safety, and ergonomics across all vehicle types. High-volume requirements for seats, frames, foams, and upholstery in every vehicle ensure consistent demand. Continuous improvements in adjustability, lightweight structures, and safety integration further support widespread adoption, reinforcing the segment’s dominant position across global passenger and commercial vehicle platforms.

- In July 2025, Adient launched a mechanical massage seating solution featuring a 3D massage module that simulates professional kneading, smart controls with multiple modes, OTA update support, flexible comfort structures, and enhanced safety features for deep-recline seat applications.

The infotainment and HMI components segment is the fastest-growing segment, expanding at a CAGR of 8.8% over the forecast period. Rising consumer demand for connected dashboards, touchscreens, digital clusters, and intuitive human-machine interfaces is accelerating adoption across modern vehicle interiors worldwide.

Automotive Interior Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Interior Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market dominates and remains the fastest-growing region with the highest CAGR over the analysis period. The regional market is driven by high vehicle production volumes in China, Japan, India, and South Korea. Rapid urbanization, rising disposable incomes, and growing demand for comfort-oriented and premium interior features are accelerating market growth. The presence of large OEM manufacturing bases, expanding electric vehicle adoption, and increasing focus on localized interior innovation further support product demand.

- In March 2023, BASF and Toyota launched automotive interior trims made with ultra-thin high-strength materials using advanced polymer composites, achieving weight reduction, improved mechanical performance, and enhanced surface quality for cabin components while supporting fuel efficiency and sustainability goals.

China Automotive Interior Market

The China market is estimated to touch around USD 52.54 billion in 2026, accounting for roughly 26.9% of global revenues, driven by high vehicle production, SUV demand, and rapid premium feature adoption.

Japan Automotive Interior Market

The Japan market is estimated to reach around USD 13.13 billion in 2026, accounting for roughly 6.7% of global revenues, supported by technological innovation, premium materials, and strong OEM manufacturing capabilities.

India Automotive Interior Market

In 2026, the India market is estimated to touch around USD 12.50 billion, accounting for roughly 6.4% of global revenues, fueled by rising vehicle ownership, SUV penetration, and the fastest-growing domestic demand.

Europe

Europe represents the second-largest market share and is projected to grow at a CAGR of 4.9% over the forecast period. Strong demand for premium interiors, advanced infotainment, and sustainable materials drives market growth. Stringent emission regulations and high electric vehicle penetration encourage lightweight and eco-friendly interior solutions. Established automotive brands and continuous interior design innovation push the product demand across the region.

- In January 2024, Renault revealed the interior of the next-generation Twingo EV, featuring a minimalist dashboard, large central touchscreen, digital instrument cluster, sustainable materials, and modular storage solutions, emphasizing affordability, connectivity, and efficient cabin packaging for urban electric mobility.

Germany Automotive Interior Market

The Germany market is estimated to touch around USD 10.31 billion in 2026, accounting for roughly 5.3% of global revenues, driven by premium vehicle production, electric mobility focus, and advanced interior technologies.

U.K. Automotive Interior Market

The U.K. market is estimated at around USD 4.31 billion in 2026, accounting for roughly 2.2% of global revenues, supported by luxury vehicle demand, interior customization, and sustainable material adoption.

North America

The North America market stands as the third-largest market, supported by strong demand for SUVs, pickup trucks, and premium passenger vehicles. Consumers prioritize comfort, advanced infotainment, and digital HMI features, driving interior value enhancement. The high adoption of connected vehicle technologies and autonomous-ready interiors further supports market demand. Stable vehicle sales, strong aftermarket activity, and continuous interior upgrades contribute to steady market growth across the U.S. and Canada.

- In January 2025, Volvo Cars returned to the Interior Design Show in Toronto to debut the new XC90, showcasing its refined Scandinavian cabin with ambient lighting, recycled Nordico upholstery, and an 11.2-inch free-standing infotainment system with Google built in alongside advanced safety and comfort enhancements.

U.S. Automotive Interior Market

The U.S. market is estimated to reach around USD 33.09 billion in 2026, accounting for roughly 16.9% of global revenues. The market growth is driven by SUV dominance, advanced infotainment adoption, and strong aftermarket customization demand.

Rest of the World

The rest of the world, including South America, the Middle East and Africa, is witnessing gradual growth. Rising vehicle ownership, improving economic conditions, and expanding urban populations are increasing the demand for basic and mid-range interior components. The growing localization of vehicle assembly and aftermarket interior upgrades further support market demand, creating long-term growth opportunities despite relatively lower adoption of advanced interior technologies.

- In January 2025, Genesis unveiled the X Skorpio off-road concept for the Rub al Khali desert in the UAE, featuring a rugged interior with modular seating, high-contrast digital displays, advanced HMI controls, and durable materials, aligning cabin design with off-road functionality and Genesis’ evolving luxury electric vehicle concept strategy.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Emphasize Design Innovation and Investments in Sustainability to Outpace their Rivals

The automotive interior market is fragmented, with numerous global Tier-1 suppliers and regional manufacturers competing across materials, components, and feature levels. Competition is driven by continuous innovation in seating systems, infotainment, HMI, and sustainable materials. Key players, including Faurecia, Adient, Lear Corporation, and Magna International, focus on OEM partnerships, modular interior platforms, and localization strategies. Companies differentiate through premiumization, lightweight solutions, digital cockpit integration, and investments in eco-friendly materials to strengthen market positioning globally.

- In February 2025, FORVIA acquired 100% of Faurecia Aptoide Automotive, strengthening its leadership in in-vehicle app ecosystems, enabling OEMs to deploy secure Android-based infotainment platforms, scalable app stores, and software-defined cockpit solutions across global vehicle programs.

LIST OF KEY AUTOMOTIVE INTERIOR COMPANIES PROFILED

- FORVIA (Faurecia) (France)

- Adient plc (U.S.)

- Lear Corporation (U.S.)

- Yanfeng Automotive Interiors (China)

- Magna International (Canada)

- Grupo Antolin (Spain)

- Continental AG (Germany)

- Robert Bosch GmbH (Germany)

- DENSO Corporation (Japan)

- Panasonic Automotive Systems (Japan)

- JVCKENWOOD Corporation (Japan)

- Pioneer Corporation (Japan)

- Sage Automotive Interiors (U.S.)

- Benecke-Kaliko (Germany)

- Pinnacle Industries Ltd. (India)

- Toyota Boshoku Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Mercedes-Benz detailed a refreshed S-Class cabin centered on the MBUX Superscreen spanning driver, center and passenger displays, with generative-AI voice control. It features Dolby Atmos audio, digital vent controls, multistage air filtration, and MB.DRIVE driver-assistance suite standard.

- January 2026: Valeo won a premium OEM interior-lighting program, deploying TactoTek In-Mold Structural Electronics (IMSE) to embed LEDs and electronics into one thin smart surface. A new automated high-volume line targets flush, lightweight, energy-efficient, durable cabin panels globally.

- October 2025: Tobii and STMicroelectronics began the mass production of a single-camera interior-sensing system. Using ST’s VD1940 5.1MP hybrid RGB/IR image sensor, it delivers wide-FoV driver/passenger monitoring day or night with reduced overall system cost.

- October 2025: Bridge of Weir and Piston Interiors marked 20 years of collaboration by launching a complete leather-interior service for U.S. automakers, covering design, material selection, cutting, sewing, finishing, testing, and delivery, enabling single-seat through full-cabin programs with premium Scottish leather.

- October 2025: Toyota premiered the Land Cruiser FJ prototype, targeting a mid-2026 Japan launch. The cabin uses a horizontal instrument panel, a low cowl for forward visibility, a consolidated monitor/switch layout to minimize eye movement, and a natural-operation shift knob for off-road control.

- April 2025: Lectra introduced Valia, a cloud-based AI platform that works with Versalis (digital leather cutting) and Vector (fabric cutting) to optimize automotive interior production. It analyzes real-time data to improve pattern nesting, cut waste, and enable predictive maintenance.

- May 2023: MediaTek and NVIDIA partnered to boost smart-cabin computing by integrating an NVIDIA GPU chiplet into MediaTek’s Dimensity Auto platform. Dimensity Auto Cockpit supports multi-displays, HDR cameras, and audio processing, while Auto Connect adds high-speed telematics and Wi-Fi.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material Type, By Vehicle Type, By Interior Feature Level, By Sales Channel, By Component Type, and By Region |

| By Material Type |

|

| By Vehicle Type |

|

| By Interior Feature Level |

|

| By Sales Channel |

|

| By Component Type |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 185.43 billion in 2025 and is projected to reach USD 317.74 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 84.59 billion.

The market is expected to exhibit a CAGR of 6.2% during the forecast period of 2026-2034.

The SUVs segment leads the market in terms of vehicle type.

Rising consumer demand for enhanced comfort and premium features to drive market growth.

Key players in the market include Faurecia, Adient, Lear Corporation, and Magna International, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us