Automotive Lightweight Materials Market Size, Share & Industry Analysis, By Material Type (Metals, Composites, Plastics & Polymers, and Others), By Application (Body-in-White, Powertrain Components, Interior Components, and Others), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Manufacturing Process (Stamping, Casting, Injection Molding, and Others), By Propulsion Type (ICE and Electric), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

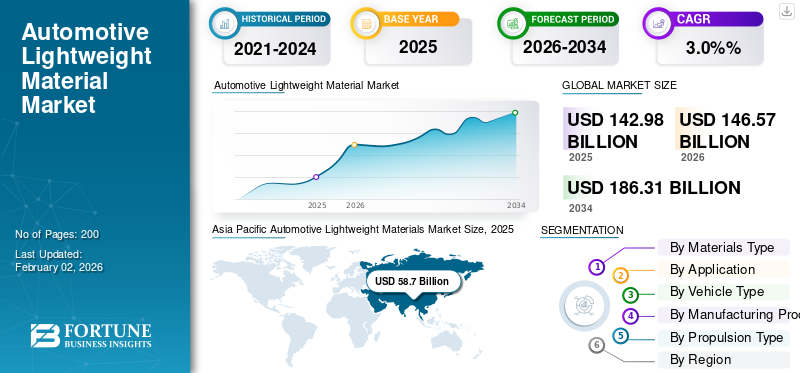

The global automotive lightweight materials market size was valued at USD 142.98 billion in 2025 and is projected to grow from USD 146.57 billion in 2026 to USD 186.31 billion by 2034, exhibiting a CAGR of 3.0% during the forecast period. Asia Pacific dominated the market with a 41.05% market share in 2025.

Automotive lightweight materials are specialized materials designed to reduce overall vehicle weight while maintaining strength, safety, and durability, addressing the rising demand for lightweight materials across the automotive industry. These materials include advanced high-strength steels (AHSS), aluminum, magnesium alloys, plastics, carbon fiber reinforced polymers, composites, and other non-ferrous metals. Their primary purpose is weight reduction without compromising structural integrity.

By integrating lightweight materials into key vehicle systems such as the body, chassis, suspension, and interiors, automakers can achieve improved fuel efficiency, enhanced performance, and better regulatory compliance. As consumers increasingly prefer fuel-efficient vehicles, lightweighting has become a fundamental part of modern automotive engineering.

Reducing vehicle weight directly enhances energy efficiency and lowers carbon emissions. In traditional internal combustion engine vehicles, lightweighting leads to better fuel economy and supports the growing demand for fuel-efficient mobility solutions. In electric vehicles (EVs), it extends driving range, reduces battery size requirements, and lowers overall system costs. The global sustainability mandates and stringent emission standards have made lightweighting one of the most effective strategies for automakers to meet environmental targets. Lighter vehicles also offer improved acceleration, handling, and braking performance, further increasing the demand for automotive lightweight materials in next-generation vehicle designs.

The market is evolving rapidly, driven by advances in materials science and manufacturing technologies. Automakers are increasingly adopting multi-material vehicle architectures that combine steel, aluminum, and composite materials to optimize strength and weight. Advanced manufacturing processes such as hot stamping, hydroforming, resin transfer molding (RTM), and additive manufacturing allow the creation of complex, lightweight structures at scale. At the same time, sustainability is becoming a key priority, with rising interest in recycled aluminum, bio-based polymers, and closed-loop material systems to reduce lifecycle emissions and industrial waste, further reinforcing the shift toward fuel-efficient, lighter vehicle platforms.

Industry leaders are propelling this transformation. Companies such as ArcelorMittal, POSCO, and Nippon Steel are developing ultra-light and high-strength steels tailored for EV architectures. Novelis, Hydro, and Constellium are expanding aluminum solutions for body-in-white and structural parts to address the global demand for automotive lightweight materials. BASF and Covestro are advancing engineering plastics and polymer composites for lightweight interiors and thermal-management components, helping automakers meet improved fuel efficiency targets. Meanwhile, Toray Industries and Teijin continue leading innovation in carbon fiber and thermoplastic composites, delivering high-performance materials for both luxury and mass-market fuel-efficient vehicles.

Download Free sample to learn more about this report.

Automotive Lightweight Material Market Key Takeaways

- 2025 Market Size: USD 142.98 billion

- 2026 Market Size: USD 146.57 billion

- 2034 Forecast Market Size: USD 186.31 billion

- CAGR: 3.0% from 2026–2034

- Asia Pacific dominated the automotive lightweight materials market with a 41.05% share in 2025.

- The composites segment is set to grow at the fastest pace, exhibiting a CAGR of 4.3% over the forecast period.

- The interior components segment is anticipated to witness the highest growth rate, with a CAGR of 4.2% over the analysis period.

Asia Pacific

The Asia Pacific region dominated the global market in 2025 and is expected to remain the industry’s growth engine throughout the forecast period.

North America

North America is projected to be the fastest-growing regional market, driven by rising EV manufacturing investments and greater adoption of aluminum and advanced high-strength steel platforms.

Europe

Europe continues to be a significant market, supported by stringent emission regulations, vehicle safety standards, and sustainability-focused automotive manufacturing initiatives.

U.S.

The market is benefiting from expanding domestic EV production, localized supply chains, and increasing investments in lightweight vehicle technologies.

Japan

The country continues to advance lightweight material adoption through automotive innovation, electrification strategies, and strong manufacturing capabilities.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Vehicle Electrification & Need for Weight Reduction Accelerate Lightweight Material Adoption

Automakers are under mounting pressure to increase EV range, hit stricter CO₂ and fuel-economy targets, and still offer larger, safer vehicles. Lightweight materials such as AHSS, aluminum, and advanced polymers are some of the few levers that improve efficiency without compromising safety. Hence, OEMs are systematically redesigning body-in-white, chassis, and battery structures around them, which is favoring the automotive lightweight materials market growth. Recent life-cycle studies also show that using advanced steels for lightweighting can deliver large, long-term greenhouse-gas savings compared with not lightweighting at all, further strengthening the regulatory and sustainability case.

- For instance, a 2025 fact sheet from the American Iron and Steel Institute reports that lightweighting a studied vehicle fleet with advanced high-strength steel (AHSS) can avoid about 260 million tonnes of CO₂-equivalent emissions by 2053 and as much as 400 million tonnes when compared directly with an aluminum-based lightweighting scenario. This highlights how strongly climate targets are pushing OEMs toward lighter, more efficient structures.

MARKET RESTRAINTS

Difficulty Recycling Mixed-Material Vehicles to Limit Large-Scale Adoption

Next-generation cars mix steel, aluminum, polymers, composites, and electronic systems in tightly integrated structures, which makes end-of-life dismantling and high-quality material recovery far more complex than for older, mostly-steel vehicles. Shredding and bulk separation struggle with bonded composites, coated plastics, and mixed aluminum alloys. Furthermore, upcoming regulations in key markets are starting to demand higher recycled content and better design for disassembly. This raises questions about the circularity and residual value of very aggressive multi-material designs and acts as a brake on how fast OEMs can scale them.

MARKET OPPORTUNITIES

Growing Use of Multi-Material Architectures in Next-Gen Platforms Creates High-Value Material Mix Opportunities

New platforms are increasingly engineered around “the right material in the right place,” combining AHSS, aluminum, magnesium, composites, and engineered plastics exactly where they add the most performance per kilogram. This multi-material approach lets OEMs tailor stiffness, crash performance, NVH, and thermal behavior while meeting stricter CO₂ limits and EV packaging needs, opening opportunities for suppliers who can co-develop grades, joining concepts, and low-carbon variants for specific zones of the vehicle. Partnerships between OEMs and material producers around low-carbon aluminum and advanced steels show how high-value material innovation is becoming a core part of future platform roadmaps.

- For instance, in 2025, Mercedes-Benz announced that its new electric CLA uses low-carbon aluminum from Norsk Hydro, cutting the model’s production-phase CO₂ footprint by around 40% compared with its non-electric predecessor. The metal is produced using hydropower and contains a significant share of recycled scrap, illustrating how OEMs are combining advanced lightweight materials with cleaner production routes in next-generation architectures.

AUTOMOTIVE LIGHTWEIGHT MATERIALS MARKET TRENDS

Increasing Adoption of Aluminum, AHSS, and Engineering Polymers in Vehicle Structures and Components

Across global markets, the material mix of cars and light trucks is shifting away from conventional steels and cast irons toward aluminum, advanced steels, and plastics. Industry and association data show aluminum kilograms per vehicle increasing as EVs and larger body styles grow, while the World Steel Association (worldsteel) reports that many modern body structures already contain more than 50% AHSS. At the same time, plastics and engineering polymers are taking over more of the front-end modules, interior structures, and under-the-hood components, both for light weighting and for integrating complex functions.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Complex Manufacturing, Joining, and Repair Techniques for Lightweight Structures May Hinder Mainstream Scale-Up

Producing and repairing multi-material bodies requires a toolbox of advanced joining methods and very strict process control. Dissimilar joints between aluminum and steel, or between metals and composites, cannot simply be spot-welded, similar to conventional steel. They often need tailored combinations of adhesive bonding, self-piercing rivets, MIG-brazing, or specialized fasteners. Collision repair is also more demanding. OEM procedures frequently restrict heating, straightening, or sectioning of high-strength and ultra-high-strength steels, and shops must follow detailed repair matrices to avoid weakening critical structures. This complexity increases capex, training needs, and uncertainty for both automotive manufacturers and the aftermarket.

Segmentation Analysis

By Material Type

Metals Dominate Owing to Their Structural Strength, Cost Efficiency, and High Automotive Penetration

Based on material type, the market is divided into metals, composites, plastics & polymers, and others.

The metals segment, including advanced high-strength steel (AHSS) and automotive-grade aluminum, dominates the global automotive lightweight materials market share due to their superior crash performance, formability, and cost-effectiveness in large-scale production. They remain essential for body-in-white, chassis, closures, and especially for EV battery enclosures. Their established supply chains and maturing low-carbon production methods further reinforce adoption across mass-market vehicle programs.

- For instance, Novelis supplies aluminum sheet for high-volume vehicles such as the Ford F-150, while ArcelorMittal’s AHSS grades continue to be used extensively in body structures across major OEMs. Such developments are likely to strengthen metals’ leadership in automotive lightweighting.

The composites segment is set to grow at the fastest pace, exhibiting a CAGR of 4.3% over the forecast period.

By Application

Body-in-White Segment Leads Due to High Demand to Meet Weight-Reduction Targets

Based on application, the market is divided into body-in-white, powertrain components, interior components, and others.

The body-in-white (BIW) segment dominates application-based demand, as automakers increasingly deploy aluminum, AHSS, and mixed-material structures to meet crashworthiness and weight-reduction targets. BIW accounts for the largest share of lightweight material integration as mass savings in the structural shell have the greatest impact on overall vehicle efficiency, especially in EVs, where compensating for battery weight is critical.

- For instance, Tesla’s use of large aluminum castings (Giga Castings) in the Model Y rear underbody and Toyota’s multi-material BIW strategies highlight the continuous shift toward lighter, stronger structural assemblies.

The interior components segment is anticipated to expand at a CAGR of 4.2%, showcasing the fastest growth over the analysis period.

By Vehicle Type

Light Commercial Vehicles (LCVs) Segment Dominates Due to High Aluminum and AHSS Usage in Pickups and Vans

Based on vehicle type, the market is divided into passenger vehicles, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs).

The LCVs segment, including pickups, utility vans, and body-on-frame SUVs, dominates lightweight material consumption due to their larger size, higher structural requirements, and widespread aluminum and AHSS adoption. The electrification of LCV fleets further accelerates the need for lightweight architectures to offset battery mass while preserving payload capacity.

- For instance, Ford’s F-Series, built with an aluminum-intensive body structure, remains North America’s best-selling vehicle line, underscoring LCVs’ disproportionately high share in lightweight material usage.

To know how our report can help streamline your business, Speak to Analyst

The HCV segment is poised to exhibit the fastest growth with a CAGR of 3.8% during the analysis period.

By Manufacturing Process

Stamping Segment Dominated in 2025 Owing to Efficient Processing of AHSS and Aluminum Sheets

Based on the manufacturing process, the market is divided into stamping, casting, injection molding, and others.

The stamping segment held the largest market share in 2025 and will continue to dominate over the forecast period. Stamping is the most widely used manufacturing process for lightweight automotive components, given that it enables high-speed production, tight dimensional control, and efficient processing of AHSS and aluminum sheets. OEMs rely on advanced hot-stamping and press-hardening technologies to form complex structural parts used in BIW assemblies.

- For instance, Hyundai Motor Group and multiple Tier-1 suppliers operate large-scale hot-stamping lines to produce ultra-high-strength steel parts for safety-critical structures in models such as the Hyundai Ioniq 5 and Kia EV6.

The injection molding segment is estimated to depict the highest CAGR of 4% over the forecast period.

By Propulsion Type

ICE Segment to Lead with Large Global Installed Base despite Rapid Lightweighting demand in EVs

Based on propulsion type, the market is divided into internal combustion engine (ICE) and electric.

The ICE segment accounted for a leading market share in 2025 and is anticipated to continue its dominance over the analysis period. ICE platforms heavily rely on AHSS, aluminum, and engineering plastics to meet fuel economy and emission standards. While EVs require even more lightweight solutions, their adoption, though fast-growing, has not yet surpassed ICE volumes worldwide.

- For example, Toyota, Honda, and Hyundai continue to deploy lightweight steel and aluminum structures across high-volume ICE models such as the Corolla, Civic, and Elantra to meet tightening efficiency regulations.

The electric segment is anticipated to expand at a CAGR of 5.2%, depicting the fastest growth rate over the forecast period.

Automotive Lightweight Materials Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Lightweight Materials Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominated the global market in 2025 and is expected to remain the industry’s growth engine throughout the forecast period. The region’s leadership is supported by its massive vehicle production base, strong electrification push, and rapid adoption of multi-material architectures in passenger and commercial vehicles. China, Japan, India, and South Korea collectively account for some of the world’s highest automotive outputs, and each is advancing lightweighting through national EV strategies, safety regulations, and OEM-level material innovation. Continuous investment in aluminum smelting, AHSS production, and polymer processing capacity further strengthens the region’s competitive position. For instance, in January 2025, Hyundai Motor Group announced a USD 1.7 billion investment in its Ulsan EV plant, with a major focus on expanding aluminum-intensive EV platforms and advanced steel stamping lines. This development reinforced Asia Pacific’s central role in next-generation lightweight vehicle manufacturing.

North America

North America is projected to be the fastest-growing regional automotive lightweight materials market, supported by strong EV penetration, rapid adoption of aluminum- and AHSS-rich vehicle platforms, and significant OEM investments in domestic EV and battery production. The region benefits from integrated supply chains for steel, aluminum, and engineered plastics, while new policies focused on localizing EV manufacturing continue to accelerate lightweight-material demand.

Europe

Europe remains an important market, underpinned by strong regulatory pressure for CO₂ reduction, stringent vehicle safety standards, and ambitious low-carbon material policies under the EU Green Deal. While the region grows more slowly than Asia Pacific and North America, it remains at the forefront of material innovation, functional integration, and circular-economy practices in automotive manufacturing.

Rest of the World

The rest of the world is experiencing moderate but steady adoption of automotive lightweight materials. Growth is driven by increasing vehicle production, rising demand for fuel-efficient fleets, and surging imports of lightweight-intensive EVs and hybrid vehicles.

COMPETITIVE LANDSCAPE

Key Industry Players:

Material Innovation and Low-Carbon Technologies Reshape Competitive Positioning

The global automotive lightweight materials industry is moderately consolidated, with a mix of large metal producers, specialty polymer suppliers, and advanced composite specialists competing on material performance, sustainability, and deep technical integration with OEM platforms. Aluminum and advanced steel providers such as Alcoa Corporation, ArcelorMittal, Novelis Inc., Constellium SE, Thyssenkrupp AG, and POSCO Holdings Inc. anchor the market with body-in-white, chassis, and battery-enclosure solutions, increasingly focusing on low-carbon production routes and high-strength alloys tailored for EV architectures. Alcoa, for example, offers its Sustana line of low-carbon aluminum (EcoLum, EcoDura) with a carbon footprint well below the industry average, while ArcelorMittal’s S-in motion portfolio provides advanced high-strength steels (AHSS) for BEV body, chassis, and battery pack applications. POSCO’s GIGA STEEL and Thyssenkrupp’s lightweight steel portfolios similarly target strong yet formable grades for modern automotive lightweight construction.

Polymer and composite specialists such as BASF SE, Covestro AG, Toray Industries, Inc., and SGL Carbon SE play a crucial role in high-value applications, including battery modules, e-motor components, structural composites, and lightweight interiors. BASF supplies engineering plastics (e.g., Ultramid, Ultradur) and e-mobility solutions for high-voltage connectors, battery housings, and thermal-management parts, while Covestro provides lightweight polycarbonate and polyurethane systems for exteriors, lighting, interiors, and EV battery packaging, increasingly incorporating recycled and circular grades to meet OEM sustainability targets. Toray and SGL Carbon focus on carbon-fiber-based composites for high-performance and increasingly higher-volume automotive programs, offering structural and semi-structural parts, carbon-ceramic brake components (through SGL’s JV with Brembo), and tailored composite systems, positioning themselves as key players for OEM multi-material architectures.

Within this landscape, Novelis and Constellium are at the forefront of automotive aluminum sheet and structural solutions, particularly for EVs. Novelis is expanding its recycling and rolling capabilities to supply high-recycled-content aluminum sheet for automotive body and closure applications, while Constellium is pushing the envelope on extruded and structural aluminum for crash-management systems and EV battery enclosures. For instance, in September 2024, Constellium announced that its ALIVE (Aluminum Intensive Vehicle Enclosures) research project achieved around 12–35% weight savings for electric vehicle battery enclosures through optimized aluminum designs and manufacturing processes, underlining how leading suppliers are using advanced alloys and engineering to secure long-term positions in the EV-focused lightweight materials value chain.

LIST OF KEY AUTOMOTIVE LIGHTWEIGHT MATERIALS COMPANIES PROFILED:

- Alcoa Corporation (U.S.)

- ArcelorMittal S.p.A. (Luxembourg)

- BASF SE (Germany)

- Covestro AG (Germany)

- Thyssenkrupp AG (Germany)

- Toray Industries, Inc. (Japan)

- Constellium SE (France)

- SGL Carbon SE (Germany)

- Novelis Inc. (U.S.)

- POSCO Holdings Inc. (South Korea)

KEY INDUSTRY DEVELOPMENTS:

- November 2025: ArcelorMittal S.A. launched its 3D Car Configurator, an interactive digital tool that enables OEM engineers to select advanced high-strength steel grades and coatings in real-time for weight-saving, multi-material vehicle architectures. This highlights steel’s evolving role in lightweight electrified vehicles.

- November 2025: Continental Structural Plastics (CSP) introduced 'TCA Ultra Lite Float', a composite material nearly 23% lighter than its predecessor and light enough to float. The new formulation significantly reduces the vehicle body-panel weight while maintaining structural performance and paintability.

- October 2025: BASF, in partnership with ETH Zurich and BEST GmbH, revealed two pilot recycling processes that convert automotive shredder plastic-waste + biomass into high-quality feedstock, showing progress toward circular lightweight-material systems for vehicles.

- June 2025: The UK’s TWI (The Welding Institute) announced its Aluminum & Innovation 2025 initiative, focusing on aluminum additive manufacturing, coatings, and composites for automotive and electrification applications, underlining how royalty-light metals are being re-engineered for high-volume vehicle manufacturing.

- June 2025: Constellium SE unveiled new aluminum alloy and recycling technologies intended to reduce structural component weight by 20% and energy use by 95% compared to virgin metal. This would position aluminum as a more sustainable alternative to composites for high-volume vehicles.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material Type, Application, Vehicle Type, Manufacturing Process, Propulsion Type, and Region |

|

By Material Type |

|

|

By Application |

|

|

By Vehicle Type |

|

|

By Manufacturing Process |

|

|

By Propulsion Type |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 142.98 billion in 2025 and is projected to reach USD 186.31 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 58.71 billion.

The market is expected to exhibit a CAGR of 3.0% during the forecast period of 2026-2034.

The metals segment leads the market by materials type.

Rising urbanization, government push for public transport electrification, and surging need for vehicle electrification is a key factor driving the growth for market.

BASF SE, Toray Industries, Inc., Constellium SE, and Novelis Inc. are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us