Automotive Middleware Market Size, Share & Industry Analysis, By Deployment Type (Embedded Middleware, Adaptive Middleware & Cloud-based Middleware), By Vehicle Type (Hatchback & Sedans, SUVs, LCVs & HCVs), By Application (Infotainment Systems, ADAS, Powertrain & Body Control, Telematics & Connectivity, and Autonomous Driving Systems), By Vehicle Architecture Type (Domain-based Architecture, Zonal Architecture & Centralized Computing Architecture), By Software Type (Operating System-based Middleware, Communication Middleware & Data Management Middleware), and Regional Forecast, 2026–2034

Automotive Middleware Market Size and Future Outlook

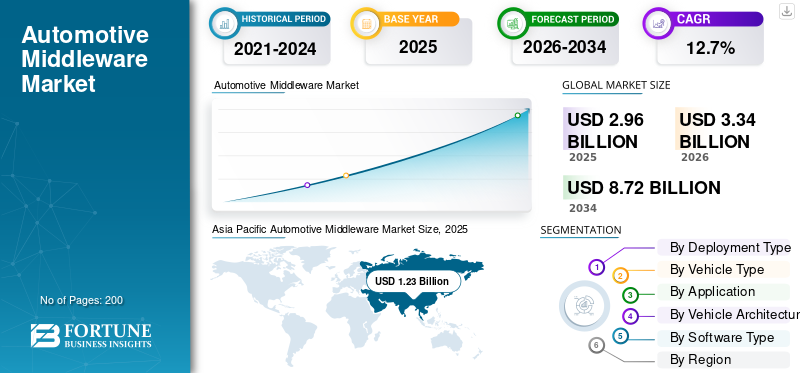

The global automotive middleware market size was valued at USD 2.96 billion in 2025. The market is projected to grow from USD 3.34 billion in 2026 to USD 8.72 billion by 2034, exhibiting a CAGR of 12.7% during the forecast period. Asia Pacific dominated the automotive middleware market with a market share of 41.55% in 2025.

Automotive middleware refers to software that acts as an intermediary layer between vehicle hardware and applications, enabling seamless communication, data exchange, connectivity, and integration of advanced systems. It plays a critical role in supporting functionalities such as ADAS, infotainment, and autonomous driving features. Market growth is driven by rising demand for connected vehicles, increasing adoption of autonomous vehicles, integration of ADAS and safety features, and growing need for high-performance vehicle software systems.

Major players in the global market include Bosch, Continental AG, Elektrobit, BlackBerry QNX, Vector Informatik, Aptiv PLC, NXP Semiconductors, and Renesas Electronics. These players compete through high-performance platforms, real-time processing, connectivity solutions, and innovations in software-defined vehicle architectures.

Download Free sample to learn more about this report.

AUTOMOTIVE MIDDLEWARE MARKET TRENDS

Rising Adoption of Software-Defined Vehicles Accelerates Product Demand

The transition toward software-defined vehicles is a major trend shaping the global automotive middleware industry. Automakers are increasingly adopting centralized and zonal architectures, where middleware serves as the backbone enabling communication between hardware and software layers. This architectural shift supports over-the-air updates, feature upgrades, and lifecycle management of passenger cars and commercial vehicles. As a result, demand for the product is expanding, as OEMs seek scalable and flexible software platforms to enhance vehicle performance, reduce complexity, and support continuous innovation in connected and autonomous mobility ecosystems.

- For instance, in January 2026, GlobalLogic expanded its partnership with Elektrobit to advance SDV platforms. The collaboration leverages AUTOSAR-based middleware, HPC, and cybersecurity frameworks aligned with ASPICE 4.0 and ISO 21434 standards, accelerating scalable and production-grade vehicle software development.

Integration of AI and Edge Computing Within Middleware Platforms Boost Industry Development

One of the key market trends is the integration of artificial intelligence and edge computing capabilities within middleware platforms. These technologies enable real-time data processing, predictive decision-making, and faster response times in advanced driver assistance systems (ADAS) and autonomous vehicles. Middleware solutions are evolving to support high-speed data exchange and low-latency communication, improving vehicle safety and operational efficiency. This trend is expected to witness strong momentum during the forecast period as demand for intelligent, self-learning automotive systems continues to grow globally.

- For instance, in March 2026, Tata Elxsi launched DevStudio.ai, an ASPICE-aligned GenAI platform supporting multi-agent SDLC workflows. The solution enables AI-assisted development, traceability, and deployment across both cloud and on-premise environments, supporting SDV architectures.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Demand for Connected Vehicles Drives Middleware Adoption

The increasing demand for connected vehicles is a primary driver of the automotive middleware market growth. Consumers demand seamless connectivity, infotainment, navigation, and remote diagnostics, all of which rely on middleware for efficient data exchange. Automotive manufacturers are investing heavily in connected ecosystems to enhance user experience and differentiate their offerings. This surge in connectivity requirements is significantly boosting demand for middleware, as it enables integration across multiple electronic control units and external communication networks in modern vehicles.

- For instance, in January 2026, Technica Engineering GmbH and KPIT Technologies the open-sourced SOME/IP middleware protocol, enabling secure Ethernet-based ECU communication across 40+ million vehicles. This initiative is accelerating SDV development, interoperability, and service-oriented automotive architectures globally.

Rising Development of Autonomous Vehicles Fuels Market Development

The rapid development of autonomous vehicles is driving the need for advanced middleware solutions capable of handling complex data flows and decision-making processes. Middleware supports communication between sensors, cameras, and control systems, which are essential for autonomous driving. As autonomous vehicle deployment increases, demand for high-performance middleware is expected to grow substantially. This driver is particularly strong in regions such as North America and Asia Pacific, where technological advancements and investments in mobility innovation are accelerating the development of autonomous driving capabilities.

- For instance, in February 2026, P3 developed middleware integrating Android Automotive OS with ADAS using ADASIS standards. This enables real-time map-to-vehicle data translation for predictive driving, enhanced safety, and vendor-agnostic autonomous vehicle interoperability.

MARKET RESTRAINTS

High Development Complexity and Integration Costs to Limit Product Adoption

One of the key restraints in the market is the high complexity associated with development and integration. Middleware must seamlessly operate across diverse vehicle architectures, operating systems, and hardware components, requiring significant engineering expertise and investment. Additionally, ensuring compatibility with evolving automotive standards and safety regulations further increase development costs and timelines. These challenges can slow adoption, particularly among smaller manufacturers, thereby impacting overall market growth despite rising demand for advanced vehicle software systems.

MARKET OPPORTUNITIES

Expansion of Electric Vehicles Creates New Middleware Opportunities

The rapid growth of electric vehicles presents a significant opportunity for the market. EVs require advanced software platforms for battery management, energy optimization, and system integration. Middleware plays a critical role in enabling communication between various EV components and supporting real-time monitoring. As governments worldwide promote electrification, the automotive middleware market share is expected to increase, with manufacturers focusing on developing specialized middleware solutions tailored to electric and hybrid vehicle architectures.

- For instance, in April 2026, Leapmotor selected QNX SDP 8.0 and Hypervisor for Safety 8.0 for its D19 SUV. This enables a centralized HPC architecture integrating ADAS, cockpit, and OTA updates with deterministic scheduling and multimodal AI capabilities.

Emerging Markets Offer Growth Potential for Middleware Deployment

Emerging regions such as the Asia Pacific and the Middle East and Africa present strong opportunities for market expansion. Increasing vehicle production, rising adoption of connected technologies, and supportive government initiatives are driving demand in these regions. The global automotive middleware market forecast indicates that these regions are expected to witness accelerated growth during the forecast period. Market players are expanding their presence and forming strategic partnerships to capture untapped potential and strengthen their competitive landscape in developing automotive ecosystems.

- For instance, in February 2026, Hyundai Motor Group partnered with Vodafone IoT to deploy connected vehicles across MENA using Global SIM+, enabling secure, compliant in-car connectivity, remote control, real-time monitoring, and cross-border IoT integration.

MARKET CHALLENGES

Cybersecurity Risks and Data Privacy Concerns to Challenge Market Growth

As vehicles become more connected and software-driven, cybersecurity risks pose a significant challenge to the market. Middleware acts as a critical layer managing data exchange, making it a potential target for cyber threats. Ensuring secure communication, robust data encryption, and compliance with stringent automotive cybersecurity regulations is both complex and resource-intensive. These challenges can hinder adoption and increase development costs. Addressing cybersecurity concerns is essential for sustaining automotive middleware market growth and maintaining consumer trust in connected and autonomous vehicle technologies.

Segmentation Analysis

By Vehicle Type

Rising Consumer Preference and Advanced Feature Integration Boost SUVs Segment Demand

Based on vehicle type, the market segmentation is fragmented into hatchback & sedans, SUVs, LCVs, and HCVs.

The SUVs segment dominates the market due to increasing consumer preference for premium, high-performance, and feature-rich vehicles globally. These vehicles are increasingly equipped with advanced driver assistance systems (ADAS), connected technologies, and enhanced safety features, significantly driving the market demand. Higher electronic content per vehicle and growing adoption across urban and semi-urban regions further strengthen their market share, making SUVs central to overall market growth during the forecast period.

- In May 2025, Olympian Motors and Foxconn launched Olympus OS, an AI-defined vehicle operating system with centralized gateway architecture, real-time data layer, and agentic AI, enabling scalable SUV and EV platforms with cloud, 5G, and predictive safety integration.

The hatchback & sedans segment holds the second-largest share and is expected to grow at a CAGR of 10.2% during the forecast period. Their large global vehicle base and steady integration of connectivity and safety technologies continue to support consistent middleware adoption across this segment.

To know how our report can help streamline your business, Speak to Analyst

By Deployment Type

Embedded Middleware Segment Leads due to its Key Role in Safety-Critical Applications

Based on deployment type, the market is segmented into embedded middleware, adaptive middleware, and cloud-based middleware.

The embedded middleware segment dominates the market due to its critical role in enabling real-time communication between vehicle hardware and software systems. It is widely adopted across electronic control units (ECUs) to ensure reliability, low latency, and efficient system performance. Its deep integration within vehicle architecture makes it essential for safety-critical applications such as ADAS and powertrain systems, thereby sustaining strong demand and reinforcing its leading position in the market.

- For instance, in April 2026, QNX expanded collaboration with NVIDIA by integrating QNX OS for Safety 8.0 with NVIDIA IGX Thor and Halos Safety Stack, enabling deterministic real-time control, AI processing, and functional safety for SDV and edge systems.

The adaptive middleware segment is expected to register a CAGR of 14.3% during the forecast period. Its flexibility, scalability, and compatibility with software-defined and autonomous vehicles are driving rapid adoption across next-generation automotive platforms.

By Vehicle Architecture Type

Domain-Based Architecture Segment Dominates, Driven by its Widespread Adoption in Modern Vehicles

Based on vehicle architecture type, the market is segmented into domain-based architecture, zonal architecture, and centralized computing architecture.

The domain-based architecture segment holds the largest market share due to its widespread adoption in modern vehicles for organizing electronic control units into functional domains such as powertrain, infotainment, and safety. This structure improves processing efficiency and reduces wiring complexity while supporting integration of advanced features such as ADAS and connectivity solutions. Its proven reliability and gradual transition path from traditional architectures continue to sustain strong demand in the market.

- For instance, in June 2025, NXP and Rimac co-developed a centralized SDV architecture using S32E2 processors, consolidating more than 20 ECUs into three units, enabling deterministic real-time control, ASIL D safety, and scalable domain and zonal applications.

The centralized computing architecture is the fastest-growing segment and is expected to register a CAGR of 14.7% during the forecast period. The increasing shift toward software-defined vehicles and the need for high performance computing platforms are accelerating the adoption of centralized systems.

By Software Type

Operating System-Based Middleware Segment Leads Owing to its Application

Based on software type, the market is segmented into operating system-based middleware, communication middleware, and data management middleware.

The operating system-based middleware segment dominates the market due to its fundamental role in managing hardware resources and enabling the stable execution of vehicle applications. It provides a standardized platform for integrating multiple software functions, ensuring reliability, security, and real-time performance. Its widespread use across critical vehicle systems such as ADAS, infotainment, and powertrain applications continues to drive strong demand and reinforces its dominance in the market.

- For instance, in March 2026, Google announced open-sourcing Android Automotive OS SDV platform, enabling standardized vehicle software architecture, OTA updates, cloud-based validation via Snapdragon VSoC, and integration across ADAS, telemetry, and control systems.

The data management middleware segment is the fastest-growing and is expected to register a CAGR of 14.6% during the forecast period. Increasing data generation from connected and autonomous vehicles is driving demand for efficient data processing, storage, and analytics solutions within vehicle systems.

By Application

Essential Role in Managing Core Vehicle Operations Drive Powertrain & Body Control Segment Growth

Based on application, the market is segmented into infotainment systems, advanced driver-assistance systems (ADAS), powertrain & body control, telematics & connectivity, and autonomous driving systems.

The powertrain & body control segment holds the largest market share due to its essential role in managing core vehicle operations such as engine performance, transmission, braking, and body electronics. Middleware enables seamless coordination between multiple control units, ensuring efficiency, reliability, and compliance with safety standards. Its critical importance in both conventional and electric vehicles continues to sustain market demand.

- For instance, in January 2026, Infineon and Flex launched a Zone Controller Development Kit featuring AURIX MCUs, modular ZCU architecture, cybersecurity, OTA A/B updates, and more than 30 building blocks, accelerating scalable SDV E/E development.

The autonomous driving systems is the fastest-growing segment and is expected to register a CAGR of 15.2% during the forecast period. Increasing investments in self-driving technologies and rising integration of AI-driven systems are accelerating middleware adoption in this segment.

Automotive Middleware Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America and the Middle East & Africa.

Asia Pacific

Asia Pacific Automotive Middleware Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the largest market share and is the fastest-growing region in the global automotive middleware market. The region’s dominance is driven by high vehicle production in countries such as China, Japan, and India, along with increasing adoption of connected vehicles and advanced driver assistance systems (ADAS). Strong presence of OEMs, rising demand for electric and autonomous vehicles, and government support for smart mobility further accelerate market growth. Expanding digital infrastructure and growing investments by key players continue to boost regional market expansion during the forecast period.

For instance, in February 2025, GAC and Huawei launched an AI middleware platform integrating data processing, large model training, and AI development toolchains. The platform supports intelligent R&D, smart manufacturing, and scalable automotive software-defined vehicle development, strengthening advanced automotive software capabilities.

China Automotive Middleware Market

The China market is estimated to reach around USD 0.78 billion in 2026, accounting for roughly 23.4% of global revenues. Strong EV production, rapid ADAS adoption, and government-backed smart mobility initiatives drive industry growth.

Japan Automotive Middleware Market

The Japanese market is estimated to touch around USD 0.20 billion by 2026, accounting for roughly 6.0% of global market revenues. Advanced automotive R&D, early autonomous technology adoption, and strong OEM ecosystem support steady market expansion.

India Automotive Middleware Market

The Indian market is estimated to touch around USD 0.14 billion by 2026, accounting for roughly 4.3% of global revenues. Rising vehicle production, increasing connected vehicle demand, and digital transformation initiatives drive rapid market growth.

North America

North America is the second-largest market and is expected to grow at a CAGR of 12.8% during the forecast period. The region benefits from early adoption of autonomous vehicles, connected technologies, and high-performance computing platforms. Strong presence of leading technology companies and automotive manufacturers drives innovation in middleware solutions. Increasing focus on vehicle safety features, cybersecurity, and software-defined vehicles further fuels demand. Continuous investments in R&D and favorable regulatory frameworks support automotive middleware market growth across the region.

- For instance, in January 2025, QNX, Vector, and TTTech Auto collaborated to develop a pre-integrated vehicle software platform with ASIL D and ISO 21434 compliance. This enables scalable SDV architectures, reduced integration complexity, and faster OEM development cycles.

U.S. Automotive Middleware Market

The U.S. market is estimated to touch around USD 0.67 billion by 2026, accounting for roughly 20.1% of the global market revenues. Strong technology ecosystem, autonomous vehicle testing, and high adoption of software-defined vehicles fuel market expansion.

Europe

Europe holds the third-largest market share in the global market, supported by stringent safety regulations and a strong emphasis on vehicle electrification. The region is a hub for premium automotive manufacturers integrating advanced software systems and ADAS technologies. Increasing focus on sustainability, along with rising adoption of electric and connected vehicles, drives middleware demand. Collaborative efforts between automakers and technology providers further enhance innovation, ensuring steady growth of the market across key European countries.

- For instance, in March 2025, BMW introduced its SDV architecture with four Superbrains and a shared middleware layer enabling OTA updates, AI-driven functions, zonal architecture, and 20x computing power for next-generation vehicles.

Germany Automotive Middleware Market

The Germany market is estimated to around USD 0.18 billion by 2026, accounting for roughly 5.3% of the global revenues. Strong premium OEM presence, electrification push, and stringent safety regulations drive consistent middleware adoption.

U.K. Automotive Middleware Market

The U.K. market in 2026 is estimated to reach around USD 0.11 billion, accounting for roughly 3.4% of global revenues. Increasing focus on autonomous mobility, innovation hubs, and connected vehicle development supports gradual market growth.

Middle East & Africa

The Middle East & Africa represent the fourth-largest market, witnessing gradual growth due to improving automotive infrastructure and rising demand for connected vehicle technologies. Increasing investments in smart mobility and transportation projects, particularly in countries such as the UAE and Saudi Arabia, are supporting middleware adoption. Growing awareness of vehicle safety features and digital solutions is also contributing to market expansion. Although still developing, the region is expected to witness steady growth during the forecast period with increasing participation from global market players.

- For instance, in November 2025, Abu Dhabi launched the world’s first modular smart vehicles, introducing a new transport category enabling reconfigurable, connected mobility platforms to support intelligent, autonomous, and flexible urban transportation systems.

South America

South America is experiencing moderate growth in the market, driven by increasing vehicle sales and the gradual adoption of connected technologies. Countries such as Brazil and Argentina are focusing on modernizing automotive systems and improving vehicle safety standards. Rising demand for infotainment and telematics solutions is supporting middleware integration. While economic fluctuations may impact growth, improving digital infrastructure and expanding automotive aftermarket services are expected to create steady opportunities for middleware providers in the region.

- For instance, in October 2025, Volkswagen partnered with Nuvei to deploy integrated payment middleware for connected vehicles, enabling subscription-based services, recurring billing, and multi-provider payment integration within VW Play Connect infotainment systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Are Investing in Scalable Architectures to Address Evolving OEM Requirements

The market is moderately consolidated, with a mix of global technology providers and specialized automotive software companies competing across regions. Key players such as Bosch, Continental AG, Elektrobit, BlackBerry QNX, Vector Informatik, Aptiv PLC, NXP Semiconductors, and Renesas Electronics focus on high-performance middleware platforms, real-time processing, and connectivity integration in vehicles. Companies are strengthening their competitive edge through software-defined vehicle solutions, AI-enabled platforms, and cybersecurity capabilities. Strategic partnerships, platform standardization, and investments in scalable architectures are key strategies to boost their market share and address evolving OEM requirements.

For instance, in February 2025, Qorix partnered with Qualcomm to integrate middleware with Snapdragon Digital Chassis platforms, including Ride and Cockpit platforms. This integration enables scalable, high-performance SDV solutions with deterministic processing, functional safety, and pre-integrated software stacks.

LIST OF KEY AUTOMOTIVE MIDDLEWARE COMPANIES PROFILED

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Elektrobit (Germany)

- BlackBerry Limited – QNX (Canada)

- Vector Informatik GmbH (Germany)

- Aptiv PLC (Ireland)

- NXP Semiconductors (Netherlands)

- Renesas Electronics Corporation (Japan)

- Harman International (U.S.)

- KPIT Technologies (India)

- Wind River Systems (U.S.)

- Green Hills Software (U.S.)

- TTTech Auto AG (Austria)

- Luxoft (Switzerland)

- Valeo SA (France)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Qorix partnered with RN Embedded Solutions in India to distribute AUTOSAR Classic/Adaptive TÜV-certified middleware, along with AI-enabled development tools and high-performance computing stacks. This collaboration aims to accelerate software-defined vehicle deployment among OEMs and Tier-1 suppliers.

- December 2025: TTTech Auto launched MotionWise Communication middleware, built on DDS and Zenoh protocols. The solution enables deterministic, safety-certified communication across HPCs, ECUs, and microcontrollers, supporting SDV architectures with TSN-based Ethernet and QoS management.

- November 2025: Eclipse released S-CORE 0.5-alpha, featuring deterministic orchestration, IPC, and data management modules. Qorix contributed middleware orchestration enabling scalable, safety-critical execution for ADAS, powertrain, and HPC-based software-defined vehicle architectures.

- September 2025: Infineon launched AURIX TC4x software with AUTOSAR MCAL drivers, SafeTlib, and CDSP libraries. The platform supports ASIL D compliance under ISO 26262, and ASPICE Level 3, enabling AI-based ADAS, virtualization, and high-performance ECU development.

- June 2025: Eclipse Foundation launched S-CORE, an open-source middleware stack for SDVs. The platform supports IPC, orchestration, and data persistence on QNX SDP 8.0, enabling scalable, ISO 26262-aligned development for high-performance ECUs.

- June 2025: QNX and Vector signed a MoU to develop a foundational SDV platform integrating QNX OS, Vector middleware, and TTTech MotionWise scheduling, supporting ASIL D, ISO 21434, and scalable ECU-based deployment.

- April 2024: ETAS and BlackBerry QNX partnered to deliver AUTOSAR Adaptive middleware integrated with QNX OS, featuring cybersecurity solutions compliant with UN-R155 and ISO/SAE 21434 for safe, high-performance SDV architectures.

REPORT COVERAGE

The global automotive middleware market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends that are expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.7% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Application, By Vehicle Type, By Deployment Type, By Vehicle Architecture Type, By Software Type, and By Region |

| By Application |

|

| By Vehicle Type |

|

| By Deployment Type |

|

| By Software Type |

|

| By Vehicle Architecture Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.96 billion in 2025 and is projected to reach USD 8.72 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.23 billion.

The market is expected to exhibit a CAGR of 12.7% during the forecast period.

The SUVs segment leads the market in terms of vehicle type.

Growing demand for connected vehicles is a key factor driving the market.

Major players in the market include Bosch, Continental AG, Elektrobit, BlackBerry QNX, Vector Informatik, Aptiv PLC, NXP Semiconductors, and Renesas Electronics.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us