Automotive Overhead Console Market Size, Share & Industry Analysis by Product Type (Basic Consoles, Advanced Consoles, and Smart/Connected Consoles), By Vehicle Type (Hatchback/Sedan, SUV, Light Duty Vehicle, and Heavy Duty Vehicle), By Propulsion Type (ICE and EV), By Sales Channel (OEM and Aftermarket), By Material (Plastic/Polymer, Fabric/Trim-integrated and Composite/Metal Reinforced), and Regional Forecast, 2026-2034

Automotive Overhead Console Market Size and Future Outlook

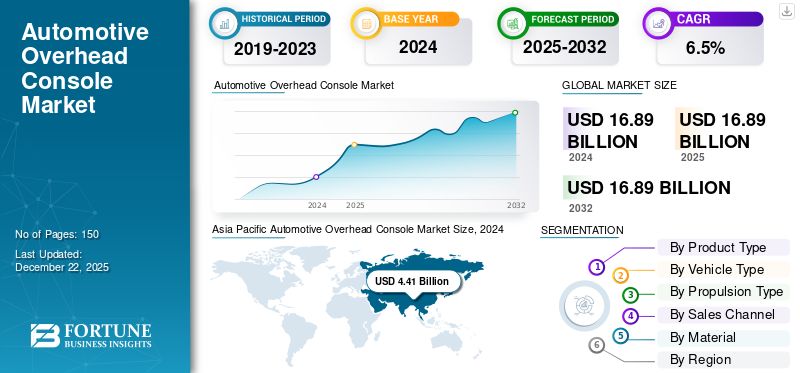

The global automotive overhead console market size was valued at USD 9.26 billion in 2025 and is projected to grow from USD 9.58 billion in 2026 to USD 18.00 billion by 2034, exhibiting a CAGR of 8.20% during the forecast period. Asia Pacific dominated the automotive overhead console market with a market share of 48.94% in 2025.

Automotive overhead console encompasses the global industry engaged in the design, manufacturing, supply, and integration of overhead console systems installed in vehicles. The console is a modular unit mounted on the vehicle’s headliner, typically above the driver and front seats (passenger car), that consolidates functional, safety, and comfort-related features into a compact assembly.

Automotive overhead consoles range from basic modules such as interior lights, sunglasses holders, and small storage compartments to advanced and smart consoles that integrate telematics, ambient lighting, HVAC controls, sunroof switches, infotainment interfaces, connectivity solutions (Bluetooth, microphones), emergency call (eCall) systems, sensors, and driver-assistance features. The expansion of the automotive industry and the rising demand for vehicle comfort are anticipated to boost product demand over the coming years.

Furthermore, the market encompasses several major players with Grupo Antolin, Gentex Corporation, Yanfeng Automotive Interiors, Magna International, and Daimay Automotive Interior at the forefront. A broad product portfolio that spans basic to smart overhead consoles, continuous innovation in lightweight materials, connectivity integration, and premium interior finishes, along with strong partnerships with leading OEMs, have supported the dominance of these companies in the global market.

In addition, other notable players such as IAC Group, Visteon Corporation, Toyota Boshoku, Hella GmbH & Co. KGaA, Motus Integrated Technologies, Continental AG, Ningbo Joyson Electronic Corp., Lear Corporation, Faurecia (FORVIA), and Flex Ltd. are actively contributing to market competition.

Download Free sample to learn more about this report.

Automotive Overhead Console Market KEY TAKEAWAYS

- 2025 Market Size: USD 9.26 billion

- 2026 Market Size: USD 9.58 billion

- 2034 Forecast Market Size: USD 18.00 billion

- CAGR: 8.20% from 2026–2034

- Asia Pacific dominated the market with a 48.94% share in 2025.

- The SUV segment is projected to hold a 44.26% share in 2026.

- The OEM segment is projected to hold a 82.91% share in 2026.

Asia Pacific

USD 4.53 billion in 2025. Strong automotive production hub with rising EV adoption and integration of advanced cabin technologies.

Europe

USD 2.36 billion in 2025. Supported by premium vehicle manufacturers and strict safety and connectivity regulations.

North America

USD 1.80 billion in 2025. Driven by high SUV/pickup penetration and adoption of advanced infotainment and lighting features.

U.S.

USD 1.56 billion by 2026. Growth driven by high-end vehicle demand and advanced in-cabin technology integration.

Japan

USD 0.53 billion by 2026. Supported by strong OEM base and adoption of advanced automotive interior technologies.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Vehicle Comfort and Convenience to Propel the Market Growth

The rising consumer demand for in-cabin comfort, convenience, and personalization drives the market. Manufacturers are enhancing interiors with multifunctional components, as vehicles are increasingly viewed as modes of transportation and as extensions of lifestyle and workspaces. Earlier, overhead consoles were limited to basic utilities such as a dome light or small storage. The consumers expect integrated features such as sunglass holders, ambient lighting, sunroof controls, wireless charging, microphones for voice commands, and infotainment switches. This shift is especially prominent in SUVs and crossovers, where cabin space and comfort are key selling points. This development is poised to drive the automotive overhead console market growth during the forecast period.

- For instance, manufacturers such as Tesla (Model Y, Model X) and BYD (Han, Tang) integrate minimalist yet smart overhead modules, which combine lighting, microphones for voice assistants, and driver monitoring sensors.

MARKET RESTRAINTS

Aftermarket Limitation May Hamper the Marker Growth

The aftermarket for automotive overhead consoles is highly limited, acting as a key restraint on market growth. Compared to the easily replaceable or upgradeable components such as infotainment units or lighting kits, overhead consoles are factory-fitted, integrated into the roof liner, wiring, and electronics, making retrofits complex, costly, and unattractive for consumers. Thus, the aftermarket limitation may hamper the market growth.

MARKET OPPORTUNITIES

Growth of Electric Vehicles (EVs) and Smart Cabins to Create Lucrative Growth Opportunities

The rapid growth of electric vehicles (EVs) is augmenting the demand for automotive interior design, creating a strong opportunity for the adoption of advanced and smart overhead consoles. This shift drives OEMs to integrate voice-control microphones, ambient lighting, driver monitoring cameras, and telematics features directly into overhead console. Thus, the increasing demand for electric vehicles directly drive the market growth.

- For instance, in March 2024, BYD launched the Seal EV, which features a panoramic sunroof. The BYD Seal is available in three variants (Dynamic, Premium, and Performance) and comes with features such as a rotating 15.6-inch infotainment display, heads-up display, and advanced driver assistance systems (ADAS) suite.

AUTOMOTIVE OVERHEAD CONSOLE MARKET TRENDS

Shift toward Smart & Connected Overhead Consoles is a Significant Market Trend

The automotive industry is witnessing a clear shift from traditional overhead consoles which primarily offered storage and basic lighting to smart and connected modules that serve as digital control hubs inside the cabin. This transformation is driven by the rising consumer demand for voice-enabled assistance, seamless infotainment, safety compliance, and personalized user experiences. Automakers are also partnering with networks to bundle charging subscriptions with EV purchases.

- For instance, in April 2024, BMW launched the updated 5 Series (i5 EV) featuring a smart overhead control panel that integrates ambient LED lighting controls, touch-enabled sunroof operation, and microphones for the BMW Intelligent Personal Assistant. Such developments are likely to drive the market growth.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Supply Chain and Material Volatility to Emerge as a Challenging Factor for the Market

Volatility in raw materials and electronic components is one of the challenging factors for the market, which directly affects production costs and supply timelines. Overhead consoles are manufactured using engineering plastics (ABS, PC, polypropylene), composites, LEDs, sensors, wiring harnesses, and semiconductors. Any fluctuation in the availability or price of these materials can disrupt the entire value chain. Thus, supply chain and material volatility is a vital factor challenging the expansion of the market.

Segmentation Analysis

By Product Type

Integration with ADAS to Drive the Advanced Console Segment Growth

On the basis of product type, the market is classified into basic consoles, advanced consoles, and smart/connected consoles.

The advanced console segment is expected to hold the maximum automotive overhead console market share of 41.68% in 2026. The segmental growth is attributed to integration with ADAS, infotainment, ambient lighting, voice assistants, and eCall/SOS modules. Rising EV adoption and premium SUVs drive the demand for connected and multifunctional consoles, fueling market growth. Additionally, the rising sales of hybrid, electric, and autonomous vehicles many of which feature intelligent cockpits—accelerate the demand for multifunctional consoles with sensor integration for driver monitoring, telematics microphones, and sunroof controls.

- For instance, models such as the Tesla Model Y, BMW X5, and BYD Han EV integrate advanced roof-mounted consoles to enhance safety, connectivity, and comfort.

By Vehicle Type

Rising Global SUV Sales to Drive the SUV Vehicle Type Segment Growth

In terms of vehicle type, the market is categorized into hatchback/sedan, SUV, light duty vehicles, and heavy duty vehicles.

The SUV segment is projected to capture the largest share of the market i.e, 44.26% in 2026. SUVs dominate due to their higher cabin space, which allows for larger, multifunctional overhead consoles. Consumers in this segment demand premium features such as ambient lighting, integrated microphones, sunroof controls, and storage compartments, resulting in nearly 100% console penetration in premium and mid-SUV models. The globally rising SUV sales further drive the market growth.

- For instance, in July 2024, Tata Motors announced the launch date of the new Curvv coupe SUV for the Indian market. The carmaker will introduce the first car in this segment, which will be offered with EV and ICE powertrains.

To know how our report can help streamline your business, Speak to Analyst

By Material

Plastic/Polymer Segment Led the Market in 2025 Due to Cost-Effectiveness and Lightweight

Based on material, the market is segmented into plastic/polymer, fabric/trim-integrated, and composite/metal reinforced.

The plastic/polymer segment captured the largest share of the market in 2024. The segmental growth is attributed to low cost, lightweight nature, and ease of molding into complex shapes. The material is used across mass-market, mid, and premium vehicles, which is a key aspect driving the market growth during forecast period.

By Sales Channel

Rising Consumer Demand for Factory-Fitted Features to Drive the OEM Segment

Based on sales channel, the market is segmented into OEM and aftermarket.

The OEM segment is projected to capture the largest share of the market i.e, 82.91% in 2026. Consumers increasingly prefer factory-fitted overhead consoles due to their seamless integration with vehicle interiors, higher reliability under warranty, and compliance with safety standards. These consoles also provide advanced functionalities such as lighting, sunroof controls, telematics, and driver monitoring systems, which drives segment growth.

By Propulsion Type

Wide Model Availability of ICE Vehicles and Increased Console Adoption to Push ICE Segment Growth

Based on propulsion type, the market is segmented into ICE and EV.

The ICE segment is willing to capture the largest market share of 73.29% in 2026. Compared to other vehicles, ICE vehicles are offered in a far wider range of models, covering everything from entry-level hatchbacks and sedans to SUVs, luxury cars, and commercial vehicles. This broad portfolio allows manufacturers to integrate overhead consoles at multiple cost points and trim levels. For instance, basic ICE variants may include simple lighting and storage units, while higher trims incorporate advanced functions such as ambient lighting, sunroof controls, and telematics.

Automotive Overhead Console Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Overhead Console Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific represented USD 4.53 billion, accounting for 48.94% of the worldwide market, and is projected to grow to USD 4.71 billion in 2026, supported by its position as the largest automobile manufacturing hub, with China, Japan, South Korea, and India accounting for a significant share of the global vehicle production. The rising production of SUVs and passenger cars, coupled with the rapid adoption of electric and hybrid vehicles, has accelerated the demand for advanced overhead consoles in the region. China alone contributes nearly 25-35% of the global vehicle production, with local OEMs such as BYD, SAIC, and NIO integrating multifunctional roof consoles featuring connectivity, ambient lighting, and driver monitoring modules. This increases the demand for automotive overhead consoles in the regional market. The Japan market is projected to reach USD 0.53 billion by 2026, the China market is projected to reach USD 2.86 billion by 2026, and the India market is projected to reach USD 0.43 billion by 2026.

North America, Europe, and the Rest of the World (RoW) held significant market share.

North America

The North America market accounted for USD 1.8 billion in 2025, representing 19.44% of the global industry, and is expected to reach USD 1.85 billion in 2026. North America’s growth is fueled by the high penetration of SUVs and pickup trucks, with OEMs such as Ford, GM, and Tesla equipping overhead consoles as standard in most mid to premium models. The U.S. dominates the regional market due to its large automotive production base and strong consumer preference for high-end vehicles. A high emphasis on the integration of advanced technologies such as ambient lighting, infotainment controls, and connectivity features within overhead consoles is another factor propelling industry expansion in the country. The U.S. market is projected to reach USD 1.56 billion by 2026.

Europe

Europe recorded a market size of USD 2.36 billion in 2025, capturing 25.42% of the global market share, and is projected to reach USD 2.44 billion in 2026. The product demand in Europe is shaped by strict safety regulations, such as the mandatory eCall system, and the high share of premium manufacturers (BMW, Mercedes-Benz, Audi, Volkswagen) that integrate advanced technologies of overhead modules with connectivity and lighting features. Such developments are anticipated to propel market growth. The UK market is projected to reach USD 0.33 billion by 2026, and the Germany market is projected to reach USD 0.47 billion by 2026.

Rest of the World

In 2025, Rest of the World held 6.20% of the global market, reaching a valuation of USD 0.57 billion, and is projected to grow to USD 0.58 billion in 2026. The rest of the world, including Latin America, the Middle East, and Africa, contributes a relatively smaller share due to price-sensitive markets and lower premium vehicle adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Players Emphasize Innovation, OEM Partnerships, and Regional Production Capabilities to Sustain Growing Competition

The global automotive overhead console market is moderately consolidated, with a mix of global Tier-1 suppliers and specialized component manufacturers competing for OEM contracts. Players compete on the basis of technological innovation, OEM partnerships, cost efficiency, and regional production capabilities.

Companies such as Grupo Antolin, Yanfeng Automotive Interiors, Hella GmbH, Magna International, and Johnson Controls (Adient) dominate the market by supplying overhead consoles directly to major OEMs. These players leverage global manufacturing footprints, R&D investments in smart and connected consoles, and strong relationships with leading manufacturers (Toyota, Ford, Volkswagen, BMW, and Hyundai).

Companies such as DaikyoNishikawa (Japan), Kyowa Sangyo (Japan), Huayu Automotive (China), and Motus Integrated Technologies (U.S.) compete in specific regions by offering cost-competitive and customized solutions.

LIST OF KEY AUTOMOTIVE OVERHEAD CONSOLE COMPANIES PROFILED

- AGM Automotive (U.S.)

- Continental AG (Germany)

- Daimay Automotive Interior Co., Ltd. (China)

- Gentex Corporation (U.S.)

- Grupo Antolin (Spain)

- Hella GmbH & Co. KGaA (Germany)

- IAC Group (Luxembourg)

- Johnson Controls (Ireland)

- LS Automotive India Pvt Ltd. (India)

- Magna International Inc. (Canada)

- Methode Automotive Solutions (U.S.)

- Plastic Omnium (France)

- Valeo (France)

- Yanfeng Automotive Interiors (China)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, Preh unveiled a transparent, icon-based center-console concept that integrates onboard charger with full V2G, V2L, and V2H functionality, hinting at future console interactions.

- In April 2025, Continental unveiled its In2Visible Overhead Console, a sleek new module that seamlessly integrates roof-mounted electronics—including sunroof actuators, in-cabin sensors, and smart surface materials—into a refined user interface. This reflects the growing OEM demand for more elegant, yet highly functional, overhead designs.

- In September 2024, Magna International introduced its Advanced Overhead Consoles (part of the ClearView system), deployed in the RAM 2500/3500 heavy-duty trucks. These modules embed driver-monitoring sensors, displays, and electronics, enhancing both convenience and safety.

- In November 2023, Yanfeng Automotive Interiors announced a partnership with a tech startup to integrate gesture control technology into overhead consoles, enabling touchless control of lighting, climate, and infotainment.

- In November 2022, Grupo Antolin introduced the Innovative Upper Trim—an overhead console concept incorporating capacitive switches, customizable materials, closed headliner design, and ambient lighting controls. It served as early design inspiration, now moving toward production integration.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.20% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Vehicle Type

|

|

|

By Propulsion Type

|

|

|

By Sales Channel

|

|

|

By Material

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.58 billion in 2026 and is projected to reach USD 18.00 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 4.53 billion.

The market is expected to exhibit a CAGR of 8.20% during the forecast period of 2026-2034.

In 2025, the SUV segment led the market by vehicle type.

The rising demand for vehicle comfort & convenience is a key factor set to propel the market growth.

Grupo Antolin, Yanfeng Automotive Interiors, Hella GmbH, Magna International, and Johnson Controls (Adient) are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us