Automotive Retail Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCVs, and HCVs), By Propulsion (ICE, Electric, and Hybrid), By Retail Channel (Offline and Online), By Services (Automotive Sales, Insurance Sales, Finance Sales, Spare Parts Sales, and Maintenance & Other Services), By End user (Individual Buyers and Fleet Operators), By Vehicle Condition (New and Used), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

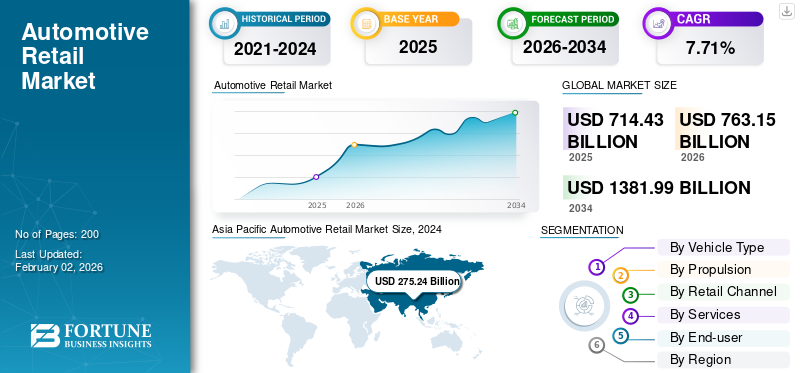

The global automotive retail market size was valued at USD 714.43 billion in 2025 and is projected to grow from USD 763.15 billion in 2026 to USD 1381.99 billion by 2034, exhibiting a CAGR of 7.71% during the forecast period. Asia Pacific dominated the global market with a share of 41.61% in 2025.

Automotive retail refers to the sale of vehicles and related services directly to consumers through dealerships, online platforms, showrooms, and spare parts shops. It encompasses both passenger cars and commercial vehicle sales. Automotive retailers act as intermediaries between manufacturers and end-users, providing product information, test drives, and after-sales services.

Rising adoption of EVs and hybrids, driven by government incentives and tighter emissions regulations, fuels retailer inventory and demand. Technological innovations such as connected vehicles, software-defined features, AR/VR virtual showrooms, and AI-enhanced customer services improve buying experiences and streamline the sales channel. An aging fleet also spurs demand for replacement parts, which fuels market growth simultaneously.

Major players in the market, including AutoNation, Lithia Motors, and Penske Automotive Group, lead the industry. These companies dominate through expansive dealership networks, digital retail platforms, and after-sales services.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Digital Transformation to Drive Market Growth

Digitalization is significantly transforming the automotive retail market outlook. Online platforms now allow customers to browse inventory, compare models, schedule test drives, and complete financing paperwork remotely. Virtual showrooms, AI-driven recommendations, and end-to-end e-commerce are enhancing the customer journey, improving convenience, and expanding dealer reach beyond physical boundaries. This shift is driven by growing internet penetration, changing consumer preferences, and OEM investment in omnichannel retailing. As a result, digital channels are becoming a critical growth enabler for the future of automotive retail. In March 2025, legacy automakers such as Volkswagen and Honda began offering direct-to-consumer online EV sales, making USD 60,000 purchases as seamless as buying a T-shirt.

Market Restraints

High Capital Requirement and Operating Costs to Restrain Market Progress

The market demands significant investment in infrastructure, skilled labor, inventory management, and technology. The cost of acquiring dealership licenses, maintaining service centers, meeting OEM standards, and managing unsold inventory burdens small and mid-sized players. Economic uncertainties, rising interest rates, and fluctuating vehicle prices further affect profitability. Additionally, compliance with evolving environmental and safety regulations increases operational expenses. These capital-intensive requirements limit new entrants and pose sustainability challenges for existing dealerships, thereby restraining market growth.

Market Opportunities

Vehicle Subscription and Leasing Models Provide Market Opportunity

Vehicle subscription and leasing models cater to consumers seeking flexibility, convenience, and lower upfront costs. These retail models appeal to urban dwellers, younger buyers, and businesses by providing access to vehicles without long-term ownership commitments. Retailers can generate recurring revenue through bundled services such as insurance, maintenance, and upgrades. As car ownership preferences evolve, especially in developed and urban markets, subscriptions and leases allow retailers to reach new customer segments, optimize inventory usage, and strengthen brand loyalty. This shift also enables retailers to differentiate their offerings in a competitive landscape and capitalize on changing mobility trends, fueling automotive retail market growth. In December 2024, Hyundai expanded its Mocean Subscription service beyond Spain and the U.K. into Germany, offering all-inclusive, flexible vehicle access (insurance, maintenance, taxes included) without a down payment, and allowing subscribers to swap cars every six months or cancel with one month’s notice.

Market Challenges

Economic Volatility and Financing Constraints to Challenge Market Development

Economic volatility and financing constraints reduce consumer purchasing power and vehicle affordability. High inflation, rising interest rates, and global uncertainties lead to tighter credit conditions, making loans more expensive and less accessible. As a result, potential buyers delay or cancel vehicle purchases, directly impacting sales volumes. Retailers face increased inventory holding costs and must offer deeper discounts or promotional financing, squeezing profit margins. Additionally, higher loan default risks deter lenders from approving vehicle loans. This combination of weak demand and limited financing availability slows market expansion and adds financial pressure on retailers worldwide.

Automotive Retail Market Trends

Shift Toward Electric Vehicles Is the Key Trend in the Market

Key trends such as the rapid adoption of electric vehicles are reshaping the evolving automotive retail. Consumers are increasingly opting for EVs due to environmental awareness, government incentives, and improved charging infrastructure. Retailers are adapting by showcasing EVs, training staff on EV features, and integrating EV servicing capabilities. This trend is compelling dealerships to update inventory, align with new OEM retail strategies, and offer education-focused customer engagement. As EVs gain mainstream acceptance, retailers must evolve to stay competitive in the changing landscape. According to the IEA, sales of electric light commercial vehicles (eLCVs) rose by around 40% in 2024, reaching 6 million units, owning a share of 7%, compared to 5% in 2023.

Impact of Tariffs

Tariffs Result in Higher Vehicle Prices, Reducing Affordability For Retailers

U.S. tariffs on imported vehicles and automotive components have a significant ripple effect on the global automotive retail market. These tariffs raise the cost of foreign-made vehicles and parts, leading to increased retail prices for consumers in the U.S., which affects demand and sales volumes. Global automakers may shift production or reroute supply chains to avoid tariffs, disrupting inventory flows and dealership operations. For retailers, higher vehicle prices can reduce affordability, lower showroom traffic, and squeeze profit margins. Export-dependent countries such as Germany, Japan, and South Korea face reduced competitiveness in the U.S. market. Additionally, trade tensions create uncertainty, discouraging investment in cross-border dealership expansion. Ultimately, tariffs distort global trade dynamics, making the retail market more volatile and regionally fragmented.

Segmentation Analysis

By Vehicle Type

Global Popularity Across Developed and Emerging Markets Drives SUVs Segment Growth

By vehicle type, the market is categorized into Hatchback/Sedan, SUVs, LCVs, and HCVs.

The SUVs segment led the market accounting for 44.74% market share in 2026 and is also expected to grow at the fastest CAGR over the forecast period. This is due to rising consumer demand for spacious, versatile vehicles with higher ground clearance and strong road presence. Their appeal spans family buyers, off-road enthusiasts, and premium segments alike. Advancements in fuel efficiency, hybrid and electric SUV offerings, and global popularity across developed and emerging markets drive rapid growth. Manufacturers are increasingly prioritizing SUV production, further boosting supply and innovation in this high-demand segment.

In June 2025, Mahindra teased its new “Nu” multi-powertrain platform, set to debut on 15 August 2025, supporting petrol, diesel, hybrid, and electric vehicles, including upcoming EV-SUVs based on this architecture.

The hatchback/sedan segment held the second-largest share of the market in 2024 due to their affordability, comfort, and fuel efficiency. Preferred by urban commuters and small families, these vehicles offer practicality and cost-effectiveness. Strong demand in emerging markets such as India and Southeast Asia, along with fleet and taxi usage, sustains their sales. The availability of hybrid and electric models in this segment further boosts appeal amid rising environmental regulations.

By Propulsion

Extensive Range and Fast Refueling Times Propelled ICE Segment Growth

By propulsion, the market is characterized into ICE, electric, and hybrid.

The ICE segment is expected to lead the market, contributing 69.11% globally in 2026 due to well-established fuel infrastructure and lower upfront costs compared to electric alternatives. Their extensive range and fast refueling times make them preferable for long-distance travel and commercial use. In developing nations, limited EV charging infrastructure and affordability issues further maintain ICE vehicle dominance in auto retailing across both passenger and commercial segments. In June 2025, Audi scrapped its ICE phase-out deadline, announcing new petrol and plug-in hybrid models to launch through 2026, with ICE production aimed to continue for another 7-10 years for added flexibility.

The electric segment is expected to grow at the fastest CAGR during the forecast period (2025-2032). Electric vehicles are the fastest-growing due to strong government incentives, emissions regulations, and rising environmental awareness. Automakers are expanding EV offerings across price segments, making them more accessible. Advancements in battery technology and increasing EV charging networks globally also enhance feasibility, attracting both individual buyers and fleets. This shift positions EVs as the most dynamic growth area in the retail market of automotive.

By Retail Channel

Preference for In-person Inspections and Human Interaction for High-Value Purchases Fuels Offline Segment Growth

By retail channel, the market is divided into offline and online.

The offline segment will account for 91.95% market share in 2026 due to the importance of physical touchpoints in vehicle buying. Customers expect in-person inspections, test drives, and human interaction for high-value purchases. Dealers provide personalized finance options, after-sales products and services, and negotiation flexibility, reinforcing trust. Additionally, established dealer networks and limited penetration in rural and semi-urban areas keep offline channels strong in global markets.

The online segment is expected to grow at the highest CAGR over the forecast period. This sales model is growing rapidly due to consumer preference for convenience, price transparency, and digital engagement. Platforms offer end-to-end services including vehicle selection, financing, insurance, and doorstep delivery. COVID-19 accelerated digital adoption, prompting OEMs and dealerships to invest in e-commerce. AI tools, virtual showrooms, and mobile-first strategies further enhance online automotive retail, attracting tech-savvy buyers across age groups and regions.

In March 2025, CARS24 expanded into the new-car market by launching an OEM and dealer aggregator platform called New Cars. It includes AI-powered video walkthroughs, on-road pricing, test-drives, financing, and car comparisons leveraging its existing user base, where 50% were evaluating new vehicles.

By Services

Growing Population Propelled the Automotive Segment Growth

By services, the market is divided into automotive sales, insurance sales, finance sales, spare parts sales, and maintenance & other services.

The automotive sales segment held the largest market share in 2024, dominating as the primary revenue stream for dealers and manufacturers. Demand is driven by population growth, urbanization, and rising incomes, especially in developing markets. New model launched, financing options, and trade-in programs continue to attract buyers. The emotional and functional value of car ownership remains high globally, sustaining automotive sales as the core offering in retail networks and fueling the growth of the segment.

The maintenance & other services segment is expected to grow at the fastest CAGR during the forecast period. The growth is due to extended vehicle lifespans and rising demand for convenience. Owners seek professional servicing, diagnostics, and quick repairs post-warranty. Additionally, connected car technologies enable predictive maintenance, enhancing service frequency. Subscription-based maintenance plans, mobile servicing, and digital appointment systems are boosting revenues, making after-sales services a vital growth driver for retailers in the automotive industry.

In February 2025, Stellantis initiated a pilot mobile service program in select U.S. Southeast cities. The program aims to scale nationwide by 2025, offering oil changes, tire rotations, software updates, and recall services at customers’ homes or workplaces, via dealership-partnered service vans.

To know how our report can help streamline your business, Speak to Analyst

By End-user

Increasing Affordability Through Loans, EMIs, and Trade-Ins Drives the Individual Buyer Segment Growth

By end-user, the market is divided into individual buyers and fleet operators.

The individual buyers segment is expected to account for 81.39% of the market in 2026, holding the largest share. This dominance stems from the continued aspiration for personal mobility and car ownership. For many consumers, vehicles symbolize independence, lifestyle, and status. Increasing affordability through loans, EMIs, and trade-ins further accelerates purchases. Government incentives, especially for personal EVs, and rising demand in urban and suburban areas, ensure that individual buyers remain the primary customer base in the automotive market.

The fleet operators segment is expected to record the fastest CAGR during the forecast period. Growth is driven by rising demand from e-commerce, logistics, and ride-hailing sectors. Businesses prioritize vehicle leasing, fleet optimization, and operational cost-efficiency. Increasing focus on last-mile delivery and sustainable transport solutions, especially with EV fleets, fuels growth. Fleet management platforms, data-driven maintenance, and commercial vehicle subscription models further support the segment’s expansion in the industry.

In May 2025, Tata Motors partnered with Egypt’s MTI to introduce a wide commercial vehicle lineup, including Tata Xenon pickups, Ultra T.7/T.9 trucks, Prima heavy-duty models, and LP 613 buses. The offering includes extended warranties and after-sales support through seven MTI service locations.

By Vehicle Condition

Rising Demand for Electric and Hybrid Models from Fleet Buyers Augments New Segment Growth

By vehicle condition, the market is divided into new and used.

The new segment dominates due to strong consumer interest in the latest models offering technological advancement, safety, and fuel efficiency. Automakers frequently update their product lineups to meet evolving regulations and customer preferences, encouraging regular vehicle replacements. Additionally, new car purchases are supported by attractive manufacturer financing, warranties, and promotional incentives. Fleet buyers, corporate leases, and rising demand for electric and hybrid models further sustain new vehicle sales as the dominant segment.

The used vehicles are the fastest-growing segment due to increased affordability and improved quality of pre-owned cars. Economic uncertainty and high prices of new vehicles drive consumers toward cost-effective alternatives. Certified Pre-Owned (CPO) programs with warranties and reconditioning boost buyer confidence. Digital platforms and online marketplaces enhance access, price transparency, and convenience, accelerating the shift toward used car purchases, especially in emerging markets and among first-time buyers, which fuels segment growth.

In June 2025, CarGurus unveiled an AI-powered car-shopping technology to enhance customer experience. Buyers can now use conversational prompts such as “three kids under 3 high safeties”, refine by budget or features, and revisit unique search URLs.

Automotive Retail Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America recorded a market size of USD 188.28 billion in 2025, capturing 26.35% of the global market share, and is expected to reach USD 199.21 billion in 2026. North America held a moderate share of the market in 2024, driven by high vehicle ownership rates and strong financial infrastructure enabling easy access to auto loans and leases. Additionally, a well-developed dealership network and a strong demand for trucks and SUVs contribute significantly to the region’s performance. The growing shift toward digital retail platforms and increasing interest in electric vehicles, especially in the U.S. and Canada, further sustains market strength in this mature region. The U.S. market is projected to reach USD 141.9 billion by 2026.

The automotive retail market in the U.S. is driven by a well-established dealership network and a strong culture of personal vehicle ownership, especially for pickup trucks and SUVs. Robust consumer financing options and high disposable incomes support consistent vehicle demand. The U.S. leads in digital innovation, with increasing adoption of online car sales, subscription models, and electric vehicles, making it a critical contributor to North America’s overall market size.

In February 2023, AutoNation USA opened its first store in Charleston, South Carolina, its 11th nationwide location at 2250 Savannah Highway. The 31,500 sq ft dealership created nearly 30 new jobs and offers pre-owned vehicles with haggle-free pricing, digital tools, and the “We’ll Buy Your Car” program.

Europe

In 2025, Europe represented USD 167.25 billion, accounting for 23.41% of the worldwide market, and is expected to reach USD 176.9 billion in 2026. Stringent emission regulations are accelerating electric vehicle sales, supported by government incentives and expanding charging infrastructure. Additionally, the region is home to a high concentration of premium vehicle manufacturers. The rise of digital retail agency models and subscription services also contributes to the market’s evolution and expansion across the region. The UK market is projected to reach USD 17.34 billion by 2026, while the Germany market is projected to reach USD 36.05 billion by 2026.

In December 2023, Penske Automotive Group agreed to acquire Rybrook Group Limited, 15 premium U.K. dealerships (BMW, MINI, Volvo, Land Rover, Porsche; plus BMW Motorrad), representing approximately USD 1 billion in annual revenue.

Asia Pacific

Asia Pacific Automotive Retail Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market generated USD 297.24 billion in 2025, representing 41.61% of the global market landscape, and is expected to reach USD 321.18 billion in 2026. Asia Pacific held the dominant automotive retail market share in 2024 and is poised to record the fastest CAGR over the forecast period (2025-2032). The region dominates due to a large population, rising middle-class incomes, and rapid urbanization, driving first-time vehicle ownership across countries such as China and India. Additionally, expanding road infrastructure, favorable government policies, and increasing digital adoption boost new car sales. The region also leads in electric vehicle adoption and manufacturing, supported by local OEMs and foreign investments, making it the fastest-growing and most dynamic automotive retail market globally. The Japan market is projected to reach USD 20.71 billion by 2026, the China market is projected to reach USD 153.47 billion by 2026, and the India market is projected to reach USD 19.96 billion by 2026.

In December 2024, Penske Automotive Group completed its acquisition of Porsche Centre Melbourne in Australia, its 25th Porsche dealership globally, adding an estimated USD 130 million in annualized revenue and boosting its Melbourne operations to USD 260 million in revenue across three locations.

Rest of the World

The market in Rest of the World reached USD 61.66 billion in 2025, representing 8.63% of total market revenue, and is projected to reach USD 65.87 billion in 2026. In the Rest of the World, including Latin America, the Middle East, and Africa, automotive retail industry growth is driven by improving economic conditions and increasing motorization rates. Rising urbanization and infrastructure development create demand for both personal and commercial vehicles. Additionally, the expansion of dealership networks and digital platforms, along with the availability of financing options, supports automotive retail penetrations in underdeveloped and emerging markets.

Competitive Landscape

Key Market Players

Key Players Focus on Partnership with Fintech and Insurtech to Gain Competitive Edge

The global automotive retail market is highly competitive, characterized by a mix of franchised dealerships, independent retailers, digital platforms, and OEM-owned stores. Traditional dealerships dominate physical retail, offering vehicles, financing, and after-sales services. Major players such as AutoNation, Penske Automotive Group, and Lithia Motors lead the market. Automakers such as Tesla and BYD are adopting direct-to-consumer models, bypassing dealerships entirely. Intense price competition, especially in the EV segments, is forcing retailers to differentiate through value-added services and personalized experiences, and gain competitive advantage. Additionally, technology integration, flexible ownership models, and partnerships with fintech and insurtech firms are becoming crucial for survival. The retail landscape in automotive is evolving rapidly, demanding innovation and agility from all players to retain market share.

List of Key Automotive Retail Companies Profiled:

- AutoNation (U.S.)

- Penske Automotive Group (U.S.)

- Lithia Motors (U.S.)

- Group 1 Automotive (U.S.)

- Sonic Automotive (U.S.)

- Asbury Automotive Group (U.S.)

- CarMax Inc. (U.S.)

- Carvana Co (U.S.)

- Lookers Plc (U.K.)

- Vertu Motors Plc (U.K.)

- Pendragon Plc (U.K.)

- Inchcape Plc (U.K.)

- Emil Frey Group (Switzerland)

- Daimler AG Retail (Germany)

- Toyota Tsusho Corporation (Japan)

- Volkswagen Group Retail (Germany)

- China Grand Automotive Services (China)

- China Yongda Automobiles Services (China)

- Cargiant Ltd. (U.K.)

- Bilia AB (Sweden)

Key Industry Developments

- In July 2025, Penske Automotive Group completed its acquisition of a Ferrari dealership in Modena, Italy, its 9th location globally. This move expanded its Italian luxury footprint to 29 locations and is expected to generate around USD 40 million in annual revenue.

- In June 2025, Lithia & Driveway acquired two Mercedes-Benz dealerships in Collierville. Tennessee and Jackson, Mississippi, are its first in the Southeast, adding approximately USD 220 million in annualized revenue.

- In April 2025, AutoNation completed the acquisition of Groove Ford and Groove Mazda in Englewood, Colorado. The dealership was rebranded as AutoNation Ford Arapahoe and AutoNation Mazda Arapahoe.

- In January 2025, AutoNation was named America’s Most Admired Automobile Retailer for the 5th consecutive year and made Fortune’s World's Most Admired Companies list for the 8th straight year.

- In October 2023, AutoNation launched AutoNationParts.com, an e-commerce platform offering genuine OEM and aftermarket automotive parts and accessories from over 25 brands, with fast nationwide shipping and a VIN-based fit guarantee.

Investment Analysis and Opportunities

The global automotive retail market offers attractive investment opportunities driven by rising vehicle demand, digital transformation, and the shift toward electric and connected vehicles. Investors can capitalize on trends such as online vehicle retail, EV-specific dealerships, and after-sales service networks. High-margin segments such as financing, insurance, and maintenance provide recurring revenue potential. Additionally, emerging markets with rising motorization present growth avenues. Strategic investments in digital infrastructure, AI-driven platforms, and mobility services can yield strong returns. AS the industry evolves, businesses that embrace innovation and sustainability are best positioned for long-term profitability and investor interest in the automotive retail space.

Report Coverage

The global automotive retail market report analyzes the market in depth. It highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, vehicle type, propulsion, retail channel, services, and end-user. Besides this, the market research reports provide insights into the market trends and highlight significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.71% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

By Propulsion

By Retail Channel

By Services

By End-user

By Vehicle Condition

By Region

|

Frequently Asked Questions

Fortune Business Insights says the global market was valued at USD 714.43 billion in 2025 and is anticipated to reach USD 1381.99 billion by 2034.

The market will exhibit a CAGR of 7.71% over the forecast period (2026-2034).

By vehicle type, the SUVs segment holds the leading share of the market.

Digital transformation in the automotive retail sector is a key factor driving market growth.

High capital requirements and operating costs are key factors restraining the market.

AutoNation, Penske Automotive Group, and Lithia Motors are the leading players in the market.

In 2026, the Asia Pacific region led the global market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us