Automotive Torque Converter Market Size, Share & Industry Analysis, By Vehicle Type (Hatchback/Sedan, SUVs, LCVs, and HCVs), By Transmission Type (Automatic Transmission, Continuously Variable Transmission, and Automated Manual Transmission), By Torque Converter Type (Single-Stage and Multi-Stage), By Drivetrain (Front-Wheel Drive, Rear-Wheel Drive, and All-Wheel Drive), By Component (Complete Torque Converter Assembly and Lock-Up Clutch/TC Module Assembly), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

Automotive Torque Converter Market Size and Future Outlook

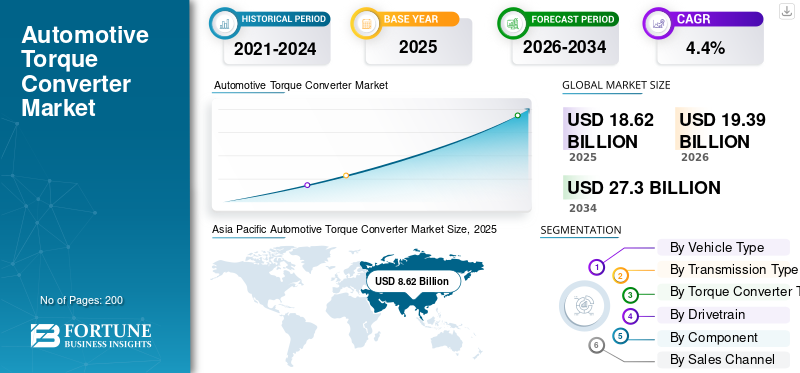

The automotive torque converter market size was valued at USD 18.62 billion in 2025. The market is projected to grow from USD 19.39 billion in 2026 to USD 27.30 billion by 2034, exhibiting a CAGR of 4.4% during the forecast period. Asia Pacific dominated the automotive torque converter market with a market share of 46.29% in 2025.

The global market represents a critical segment of modern transmission systems, enabling smooth power transfer between the engine and gearbox in automatic transmission vehicles. Torque converters play a vital role in enhancing driving comfort by allowing seamless gear shifting, reducing vibration and ensuring controlled torque multiplication at low speeds. This technology is widely adopted across passenger vehicles and commercial vehicles, particularly those powered by the internal combustion engine.

The market is primarily driven by the increasing demand for automatic transmissions, especially in urban and semi-urban regions where driving convenience and traffic congestion influence purchasing decisions. Automakers are increasingly integrating torque converters to improve fuel efficiency and reduce drivetrain stress, contributing to better vehicle longevity and performance. Growth in the passenger vehicle category continues to support the market growth, while steady demand from the commercial vehicle segment sustains long-term replacement demand.

In recent years, the market has evolved with advancements in lock-up clutch technology and lightweight materials, enabling higher efficiency and reduced power loss. These innovations support regulatory compliance related to emissions while maintaining performance standards. Additionally, expanding vehicle production across emerging economies has increased the demand for torque converters across multiple vehicle type categories.

Looking ahead, the market is expected to witness stable growth during the forecast period, supported by the growing installed base of automatic transmission vehicles and aftermarket replacement demand. While electrification poses long-term challenges, torque converters remain indispensable in conventional and hybrid transmission systems. Key players such as ZF Friedrichshafen AG, Aisin Corporation, Valeo SA, Schaeffler AG, and BorgWarner Inc. are focusing on product optimization, modular designs, and regional manufacturing expansion to strengthen competitiveness in the global automotive torque converter market.

Download Free sample to learn more about this report.

AUTOMOTIVE TORQUE CONVERTER MARKET TRENDS

Integration of Lock-Up Clutch Technology Gains Momentum

Manufacturers are increasingly focusing on enhanced filtration technology to meet stricter emission standard requirements and improve engine protection. Adoption of improved media and optimized filter designs supports longer service intervals and higher oil cleanliness, driving adoption of premium products. OEMs increasingly deploy lock-up clutch torque converters to meet fuel efficiency targets.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Automatic Transmissions Drives Market Expansion

The growing demand for automatic transmissions is a major driver of the automotive torque converter market growth. Consumers increasingly prefer automatic systems for driving comfort, smoother gear shifting and reduced fatigue. Automakers are responding by expanding automatic offerings across passenger vehicles and commercial vehicles, directly increasing the demand for torque converters and supporting consistent market growth. Global automatic transmission adoption continues to rise as automakers expand automatic variants across mass-market models.

MARKET RESTRAINTS

Growing Electrification Limits Long-Term Torque Converter Adoption

The rapid shift toward battery electric vehicles poses a restraint for the market. Electric drivetrains eliminate the need for conventional transmission systems, reducing torque converter applicability. As EV adoption increases, particularly in developed regions, the long-term growth during the forecast period may face structural limitations. EV adoption continues to rise globally, reducing dependence on traditional drivetrain components.

MARKET OPPORTUNITIES

Aftermarket Replacement Demand Creates Long-Term Growth Potential

The expanding installed base of automatic transmission vehicles presents a significant aftermarket opportunity. Torque converters are replaced during major transmission overhauls, particularly in high-mileage commercial vehicle applications. This replacement demand supports sustained revenue generation, strengthening long-term prospects for the automotive torque converter market. The growing vehicle parc in emerging economies supports transmission component aftermarket demand.

MARKET CHALLENGES

Raw Material Price Volatility Impacts Manufacturing Costs

Managing cost efficiency amid raw material price fluctuations and supply chain disruptions remains a key challenge. Torque converter manufacturing requires precision engineering and specialized materials, making cost control difficult. These factors can impact profitability and slow adoption across price-sensitive vehicle type categories.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

Hatchback and Sedan Dominate Due to High Production Volumes

On the basis of vehicle type, the market is segmented into hatchback/sedan, SUVs, LCVs and HCVs.

Hatchback and sedan models dominate the market due to their large share in global passenger vehicle production. Rising automatic penetration in mass-market cars and affordability drive adoption. These vehicles account for a significant portion of automatic transmission vehicles, ensuring steady demand for torque converters.

- For instance, in March 2024, OICA reported that passenger cars continued to account for the majority of global vehicle production, reinforcing demand for automatic-equipped hatchback and sedan platforms.

LCV segment is expected to grow at a CAGR of 4.3% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Transmission Type

Automatic Transmission Leads with Superior Driving Comfort

On the basis of transmission type, the market is segmented into automatic transmission, continuously variable transmission and automated manual transmission.

Automatic transmission dominates due to strong consumer preference for convenience and smoother gear shifting. Growing adoption across both passenger vehicles and commercial vehicles sustains torque converter demand and strengthens market leadership.

- For instance, in July 2023, Toyota announced the expansion of automatic transmission availability across multiple compact and mid-size passenger vehicle models to improve driving comfort and efficiency.

Continuously variable transmission segment is expected to grow at a CAGR of 3.8% over the forecast period.

By Torque Converter Type

Single-Stage Torque Converters Lead Due to Simplicity

On the basis of torque converter type, the market is segmented into single-stage and multi-stage. Single-stage torque converters dominate owing to cost efficiency and widespread use in standard automatic transmission systems. Their reliability makes them ideal for high-volume passenger vehicle applications.

- For instance, in September 2023, ZF highlighted continued demand for single-stage torque converters in conventional automatic transmissions due to their efficiency and suitability for high-volume passenger vehicles.

Multi-stage segment is expected to grow at a CAGR of 4.5% over the forecast period.

By Drivetrain

Front-Wheel Drive Dominates with Mass-Market Adoption

On the basis of drivetrain, the market is segmented into front-wheel drive, rear-wheel drive and all-wheel drive.

Front-wheel-drive vehicles dominate due to their extensive use in compact and mid-size passenger vehicles, supporting consistent demand for torque converters.

- For instance, in February 2024, Hyundai Motor Group emphasized front-wheel-drive architectures for mass-market passenger vehicles, citing packaging efficiency and compatibility with automatic transmissions.

All-wheel drive segment is expected to grow at a CAGR of 4.0% over the forecast period.

By Component

Complete Torque Converter Assemblies Lead OEM Demand

On the basis of component, the market is segmented into complete torque converter assembly and lock-up clutch/TC module assembly.

Complete assemblies held largest automotive torque converter market share as OEMs prefer integrated solutions for manufacturing efficiency and reliability across vehicle segment platforms.

- For instance, in August 2023, Valeo stated that OEMs increasingly prefer fully assembled torque converter modules to simplify transmission integration and improve reliability.

Lock-Up Clutch/TC module assembly segment is expected to grow at a CAGR of 4.7% over the forecast period.

By Sales Channel

OEM Segment Leads Through Direct Vehicle Integration

On the basis of sales channel, the market is segmented into OEM and Aftermarket. OEM sales dominate as torque converters are installed during vehicle production, especially in automatic transmission vehicles, ensuring volume consistency.

- For instance, in November 2023, Hyundai Transys confirmed long-term supply of torque converters to global OEMs for factory-installed automatic transmission systems.

Aftermarket segment is expected to grow at a CAGR of 6.1% over the forecast period.

Automotive Torque Converter Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

Asia Pacific

Asia Pacific Automotive Torque Converter Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valuing at USD 8.62 billion, and also maintained the leading share in 2024, with USD 8.51 billion. This is due to high vehicle production and growing passenger vehicle demand. Rising urbanization and increasing automatic adoption in China, Japan and India support market expansion. The region benefits from cost-efficient manufacturing and a large installed vehicle base.

- For instance, in January 2024, OICA reported Asia Pacific vehicle production exceeded 55 million units in 2023, led by China, Japan, and India, sustaining strong demand for torque-converter-equipped automatic transmissions.

China Automotive Torque Converter Market

China’s market is projected to be one of the largest worldwide, and held USD 3.85 billion share in 2025, representing roughly 20.7% of market sales.

India Automotive Torque Converter Market

India Market in 2025 was at USD 1.15 billion, accounting for roughly 6.2% of global revenues.

North America

North America is projected to record a growth rate of 3.6% in the coming years, and reach a valuation of USD 4.75 billion by 2026. North America shows steady growth driven by high penetration of automatic transmission vehicles and strong aftermarket demand. The U.S. remains the largest contributor due to a mature vehicle parc and preference for automatic drivetrains.

U.S. Automotive Torque Converter Market

Based on North America’s strong contribution, the U.S. market can be analytically approximated at around USD 3.10 billion, representing roughly 16.6% of global market.

Europe

Europe is estimated to reach USD 4.11 billion in 2026 and secure the position of the third-largest region in the market. Europe experiences moderate growth supported by replacement demand and continued automatic adoption in premium vehicles. Regulatory pressure encourages efficiency-focused torque converter technologies.

Germany Automotive Torque Converter Market

Germany market in 2025 was at USD 0.95 billion, accounting for roughly 5.1% of global revenues.

U.K. Automotive Torque Converter Market

U.K. market in 2025 reached USD 0.78 billion, accounting for roughly 4.2% of global revenues.

Rest of the World

Rest of the World grows gradually due to expanding vehicle ownership and rising automatic adoption in emerging economies, supporting long-term market stability.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Technology Upgrades Shape Market Competitive Dynamics

The automotive torque converter market is moderately consolidated, with global and regional suppliers competing on technology, quality, and long-term OEM relationships. Leading manufacturers focus on innovation within automatic transmission systems, emphasizing durability, efficiency and compatibility with evolving engine architectures. The ability to serve both passenger vehicles and commercial vehicles gives established players a competitive advantage.

Key strategies include investment in advanced lock-up clutch designs to improve fuel efficiency and reduce power losses, particularly in high-volume passenger vehicle applications. Suppliers are also strengthening their global manufacturing footprint to mitigate supply chain risks and support localized production. Long-term supply agreements with OEMs ensure stable revenue streams and reinforce market positioning.

Another major competitive strategy is product standardization across multiple vehicle segment platforms. By developing scalable torque converter modules, manufacturers can address varying torque requirements while controlling costs. This approach supports rising demand for automatic transmissions across mid-range and premium vehicles. Aftermarket expansion is also gaining attention, driven by growing installed base of automatic transmission vehicles.

In addition, companies are forming partnerships to accelerate development timelines and enhance manufacturing efficiency. Digital simulation, material innovation and precision engineering are increasingly used to improve reliability in global automotive torque converter solutions.

- For instance, in March 2024, ZF announced advancements in its torque converter and automatic transmission portfolio to enhance efficiency and compatibility with next-generation powertrains.

LIST OF KEY AUTOMOTIVE TORQUE CONVERTER COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Aisin Corporation (Japan)

- Valeo SA (France)

- Schaeffler AG (Germany)

- BorgWarner Inc. (U.S.)

- Allison Transmission (U.S.)

- Hyundai Transys (South Korea)

- JATCO Ltd. (Japan)

- Exedy Corporation (Japan)

- Punch Powertrain (Belgium)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Hyundai Motor Group confirmed the continued use of torque-converter automatic transmissions across its global SUV portfolio, citing improved drivability, durability, and customer feedback compared to dual-clutch systems.

- July 2025: Hyundai confirmed the 2026 Santa Fe would adopt an 8-speed torque-converter automatic, replacing DCT, impacting annual volumes of over 300,000 units globally.

- February 2025: Volkswagen Group stated that automatic transmissions accounted for more than 65% of its global vehicle production, supporting continued deployment of torque converters across multiple platforms.

- November 2024: Volkswagen Group confirmed the wider rollout of eight-speed torque-converter automatic transmissions across select Volkswagen and Skoda passenger vehicle models, particularly in emerging markets. The move aims to enhance transmission reliability, reduce long-term maintenance risks, and deliver smoother gear shifting, underscoring the continued relevance of torque converters within modern automatic transmission architectures.

- September 2024: ZF highlighted sustained demand for torque-converter–based automatic transmissions in passenger and light commercial vehicles, particularly in regions prioritizing driving comfort and towing capability.

- March 2024: SIAM reported automatic transmission penetration in Indian passenger vehicles rose to around 25% in 2023, up from low double digits five years earlier, supporting torque converter adoption.

- March 2024: The U.S. EPA finalized emissions rules for model years 2027–2032, targeting up to 56% CO₂ reduction, indirectly increasing demand for efficiency-enhancing torque-converter lock-up strategies.

REPORT COVERAGE

The global automotive torque converter market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Type, Transmission Type, Torque Converter Type, Drivetrain, Component, Sales Channel and Region |

| By Vehicle Type |

|

| By Transmission Type |

|

| By Torque Converter Type |

|

| By Drivetrain |

|

| By Component |

|

| By Sales Channel |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 18.62 billion in 2025 and is projected to reach USD 27.30 billion by 2034.

In 2025, the market value stood at USD 8.62 billion.

The market is expected to exhibit a CAGR of 4.4% during the forecast period of 2026-2034.

Hatchback/sedan segment led the market by vehicle type.

Rising demand for automatic transmissions is driving the market.

ZF Friedrichshafen AG, Aisin Corporation, Valeo SA, Schaeffler AG, and BorgWarner Inc. are some of the top players in the market.

Asia Pacific dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us