Automotive Voice Recognition System Market Size, Share & Industry Analysis, By Deployment Type (Embedded / On-board, Cloud-based, and Hybrid), By Application (Navigation & Location-Based Services, Infotainment & Media Control, Communication Functions, Cabin Comfort & Climate Control, and Vehicle Control & Connected Services), By Vehicle Type (Hatchback/Sedan, SUVs, LCVs, and HCVs), By Technology (Command-based, NLU-based, and Conversational AI), and Regional Forecast, 2026–2034

Automotive Voice Recognition System Market Size and Future Outlook

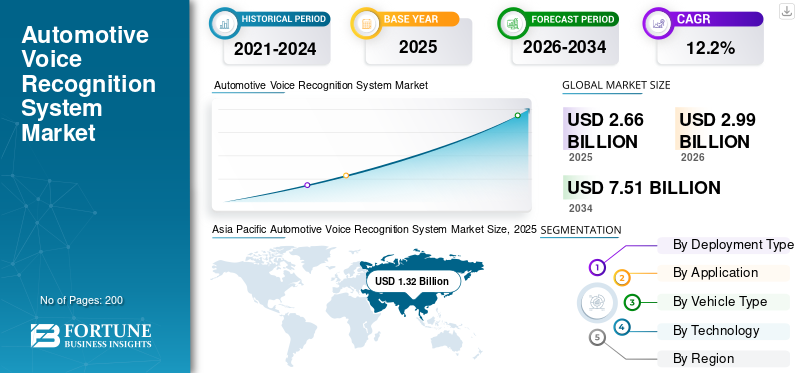

The global automotive voice recognition system market size was valued at USD 2.66 billion in 2025. The market is projected to grow from USD 2.99 billion in 2026 to USD 7.51 billion by 2034, exhibiting a CAGR of 12.2% during the forecast period. Asia Pacific dominated the automotive voice recognition system market with a market share of 49.62% in 2025.

An automotive voice recognition system is an in-vehicle technology that enables drivers and passengers to operate functions via spoken commands. It uses speech recognition, artificial intelligence and natural language processing to control navigation, infotainment, calling, messaging, climate settings, and selected vehicle functions. It improves convenience, reduces manual interaction, and enables safer, hands-free driving while supporting smarter connected-car experiences. The main drivers for the global market growth are rising demand for hands-free driving, growth in connected cars and software-defined vehicles, wider use of smart infotainment systems, and the shift from basic command systems to NLU and conversational AI. Better in-car connectivity and hybrid voice architectures are also raising adoption by improving response quality, personalization, and always-available functionality. Major players include Cerence, Bosch, HARMAN, and SoundHound AI, along with other cockpit and software providers. The key trend is a move from basic embedded cloud based and hybrid, conversational, AI-powered assistants integrated with broader digital cockpit platforms. Cerence highlights large-scale automotive deployment, while Bosch emphasizes on-board reliability, HARMAN focuses on emotionally intelligent cabin AI, and SoundHound is expanding multilingual conversational automotive solutions.

Download Free sample to learn more about this report.

AUTOMOTIVE VOICE RECOGNITION SYSTEM MARKET TRENDS

Rising Integration of Generative AI and Conversational Assistants Transforms In-Car Interaction

Automotive voice recognition is rapidly evolving from basic command-based interfaces to conversational, AI-driven assistants capable of contextual understanding and multi-turn dialogue. This shift is closely linked to the rise of software-defined vehicles, where digital cockpit capabilities are continuously upgraded via over-the-air updates. Voice is increasingly becoming the primary human-machine interface, integrated with touchscreens, augmented displays, and connected services. Automakers are focusing on delivering personalized, predictive experiences where the system learns driver preferences and proactively suggests actions. This transition enhances user engagement and positions voice as a central pillar of in-car digital ecosystems, strengthening brand differentiation and customer loyalty in a highly competitive automotive market.

- In January 2024, Mercedes-Benz announced at CES the integration of generative AI through Microsoft Azure OpenAI into its MBUX system, enabling more natural, conversational in-car interactions.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Demand for Hands-Free and Safer Driving Experiences Drives Adoption

The growing emphasis on road safety and reducing driver distraction is a major factor driving the adoption of automotive voice recognition systems. As vehicles incorporate more digital features, manual interaction becomes increasingly complex and unsafe. Voice control provides a natural, hands-free method to operate navigation, communication, and infotainment systems without diverting attention from driving. Regulatory bodies and safety organizations are also encouraging reduced manual interaction, indirectly supporting voice adoption. Additionally, consumers are becoming more accustomed to voice assistants on smartphones and in smart homes, accelerating their acceptance in vehicles. This convergence of safety needs and user familiarity is pushing OEMs to make voice functionality a standard or key feature across multiple vehicle segments.

- In June 2023, BMW introduced enhanced voice control in its iDrive system, allowing drivers to adjust vehicle settings and infotainment functions hands-free, reinforcing safety-focused interaction.

MARKET RESTRAINTS

Data Privacy and Connectivity Dependence Limit Full-Scale Adoption

Concerns about data privacy and reliance on internet connectivity continue to restrain the full-scale adoption of advanced automotive voice recognition systems. Cloud-based and hybrid voice platforms require continuous data exchange, raising questions about how voice data is stored, processed, and protected. Regulatory frameworks such as GDPR in Europe and similar policies in other regions require strict compliance, increasing development complexity and costs for OEMs and voice recognition technology providers. Additionally, inconsistent network infrastructure in certain regions affects the reliability of cloud-based voice systems, leading to delays or incomplete responses. While embedded systems provide better privacy and offline functionality, they lack the sophistication of cloud-driven AI, creating a trade-off that slows uniform adoption across global markets.

- In April 2021, the European Data Protection Board reinforced strict guidelines on in-vehicle data processing, highlighting the need for automakers to ensure user consent and secure handling of voice data.

MARKET OPPORTUNITIES

Expansion of Connected Ecosystems and Smart Mobility Creates New Growth Opportunities

The rapid expansion of connected vehicle ecosystems is unlocking new opportunities for automotive voice recognition system market growth. Vehicles are increasingly integrated with external digital environments such as smart homes, e-commerce platforms, and mobility services, enabling users to interact seamlessly across multiple domains through voice. This convergence allows automakers to offer value-added services such as remote vehicle control, voice-enabled payments, and personalized travel assistance. The growth of electric vehicles and shared mobility platforms further amplifies this opportunity, as these models rely heavily on digital interfaces and user-centric experiences. Voice recognition is emerging as a unifying interface that connects vehicles with broader digital lifestyles, opening new revenue streams and enhancing overall user engagement.

- In September 2022, Amazon expanded Alexa Auto integrations with multiple automakers, enabling drivers to control smart home devices and access services directly from their vehicles via voice.

MARKET CHALLENGES

Managing Multilingual Complexity and Accuracy Across Diverse Markets Remains a Key Challenge

Achieving consistent accuracy across multiple languages, accents, and real-world driving conditions remains a significant challenge for automotive voice recognition systems. Vehicles operate in noisy environments with varying acoustics, making speech recognition more complex than in controlled settings such as smartphones or homes. Additionally, global markets such as Asia Pacific, Europe, and the Middle East have diverse linguistic requirements, requiring systems to support multiple dialects and languages simultaneously. Inaccurate responses or misinterpretation of commands can reduce user trust and hinder adoption. Continuous updates and localization efforts increase development costs and technical complexity. Ensuring reliable, scalable, and context-aware voice performance across global markets remains a key hurdle for industry players.

- In May 2023, Hyundai Motor Group highlighted ongoing improvements to its AI voice assistant to understand regional accents and languages better, emphasizing the complexity of achieving global accuracy in real-world driving environments.

Segmentation Analysis

By Deployment Type

Reliable Offline Command Execution Sustains Embedded / On-board Segment Leadership

Based on deployment type, the market is segmented into embedded/onboard, cloud-based, and hybrid.

By deployment type, embedded/on-board remains the dominant segment as automakers still prioritize low-latency response, dependable performance in weak-network areas, reduced data dependence, and stronger control over core in-vehicle functions such as calling, navigation prompts, and basic settings. These systems are especially important in high-volume vehicle programs where reliability and cost discipline matter more than full cloud dependence.

- In April 2025, Opel stated that the new Mokka offers natural voice recognition in combination with navigation, showing how embedded capability remains central even as more advanced layers are added.

The hybrid segment is projected to grow at a 17.7% CAGR over the forecast period.

By Application

Daily Entertainment Control Keeps Infotainment & Media Applications in the Lead

Based on application, the market is segmented into navigation & location-based services, infotainment & media control, communication functions, cabin comfort & climate control, and vehicle control & connected services.

The infotainment & media control segment dominates the automotive voice recognition system market share as voice is most frequently used for music selection, radio control, streaming, media browsing, and quick interaction with digital cockpit screens. These functions are used daily, across price points, and are often the first voice features consumers actively adopt. That gives infotainment the widest installed base and the strongest usage intensity.

- In January 2023, Citroen stated that the new e-Berlingo offers a natural, fluid, and easy voice recognition system that helps users manage media functions through an on-board assistant.

The vehicle control & connected services segment is projected to grow at a 16.0% CAGR over the forecast period.

By Vehicle Type

Premium Features and Digital Cockpit Content Strengthen SUV Segment Momentum

Based on vehicle type, the market is segmented into hatchback/sedan, SUV, LCV, and HCV.

SUVs are the dominant segment as they increasingly offer premium infotainment, larger displays, connected services, and richer human-machine interface content, all of which raise automotive voice-recognition value per vehicle. Automakers also use SUVs to launch new cockpit technologies first, helping voice features diffuse faster through this category than in more price-sensitive vehicle classes. That combination supports both scale and higher software content. The SUV segment is projected to grow at a CAGR of 14.4% over the forecast period.

- In July 2024, Amazon stated that BMW’s next-generation voice assistant, built on Alexa technology, hit the road with the new X3, underscoring how SUVs are becoming leading platforms for advanced voice experiences.

The HCV segment is projected to grow at a CAGR of 12.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Broad Installed Base of Fixed Voice Commands Preserves Command-based Market Leadership

Based on technology, the market is segmented into command-based, NLU-based, and conversational AI.

Command-based remains the dominant segment as a very large installed base of vehicles still relies on predefined commands for calling, audio control, navigation input, and basic system operation. These systems are cheaper to deploy, easier to validate, and more practical for mass-market programs than higher-end conversational stacks. Their global installed base keeps revenue leadership intact even as smarter interfaces expand.

- In June 2020, Lincoln explained that SYNC’s voice-control architecture is built around a language model that pairs words or commands with specific tasks, underscoring why command-based systems continue to anchor the market.

The conversational AI segment is projected to grow at a CAGR of 16.3% over the forecast period.

AUTOMOTIVE VOICE RECOGNITION SYSTEM MARKET REGIONAL OUTLOOK

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Automotive Voice Recognition System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the dominant region due to massive vehicle production, rising middle-class demand, and rapid digitalization of vehicles. China dominates with strong local technology ecosystems and high smart cockpit penetration, while India is emerging as a high-growth market driven by increasing connected-car adoption. Japan and South Korea contribute through advanced automotive technologies. The region benefits from scale, increasing affordability of voice systems, and a strong push toward AI-driven in-vehicle experiences.

China Automotive Voice Recognition System Market

China dominates the Asia Pacific market with a 58.3% share, supported by massive vehicle production and strong domestic technology ecosystems. The high penetration of smart cockpits, rapid adoption of AI-powered voice assistants, and integration of connected services across both mass-market and premium vehicles drive substantial growth and reinforce China’s leadership in automotive voice recognition.

Japan Automotive Voice Recognition System Market

Japan’s market is projected to be valued at USD 0.23 billion in 2026, supported by advanced automotive technologies and a strong OEM presence. The growth is driven by the integration of intelligent voice assistants, a focus on user-friendly HMI systems, and the increasing deployment of hybrid voice solutions in passenger vehicles, particularly in technologically advanced and premium segments.

India Automotive Voice Recognition System Market

India is the fastest-growing market, with a 16% CAGR during the forecast period, driven by increasing connected-car adoption and rising demand for feature-rich infotainment systems. The growth is supported by expanding SUV sales, improving digital infrastructure, and OEM focus on integrating voice-enabled controls in mid-range vehicles, enhancing accessibility and market penetration.

North America

North America shows strong and steady growth driven by high adoption of connected vehicles, advanced infotainment systems, and early integration of AI-based voice assistants. The U.S. leads due to strong OEM-tech partnerships and widespread deployment of hybrid voice systems. The growth is supported by premium vehicle demand and increasing use of voice for vehicle control and connected services. Canada follows similar trends, while Mexico contributes through manufacturing expansion. The region maintains a high value per vehicle due to the high penetration of advanced digital cockpits.

U.S. Automotive Voice Recognition System Market

The U.S. dominates the North American market share, with a value of USD 0.60 billion in 2026, driven by high connected vehicle penetration and strong OEM-tech collaborations. Advanced deployment of hybrid voice systems, integration with AI assistants, and widespread adoption in SUVs and premium vehicles significantly contribute to market leadership and sustained growth.

Europe

Europe demonstrates robust growth supported by premium vehicle production, stringent safety standards, and rapid adoption of software-defined vehicle architectures. Countries such as Germany, the U.K., and France lead in integrating advanced voice-enabled infotainment and AI assistants. The region is witnessing strong growth in hybrid and conversational AI systems, driven by OEMs' focus on digital differentiation. Increasing electrification and connected services further enhance adoption, while regulatory emphasis on driver safety supports the shift toward hands-free voice interfaces.

U.K. Automotive Voice Recognition System Market

The U.K. market is projected to be valued at USD 0.07 billion in 2026, supported by increasing adoption of connected infotainment systems and regulatory focus on driver safety. Growth is driven by rising deployment of hybrid voice solutions, strong EV penetration, and demand for hands-free interfaces, particularly in urban mobility and premium passenger vehicles.

Germany Automotive Voice Recognition System Market

Germany holds a significant 28.2% share of the European market, driven by its strong automotive manufacturing base and premium vehicle segment. High integration of digital cockpit technologies, early adoption of conversational AI, and OEM innovation in connected vehicles contribute to its dominance and continuous advancement in voice-enabled automotive systems.

South America

South America is experiencing moderate growth as connected vehicle adoption gradually expands across key markets such as Brazil and Argentina. The region is transitioning from basic embedded systems toward hybrid voice solutions, supported by improving telecom infrastructure and rising demand for infotainment features. The growth is influenced by increasing SUV penetration and the gradual digital transformation of vehicles. However, economic fluctuations and cost sensitivity limit rapid adoption, keeping overall market growth steady but slower compared to developed regions.

Brazil Automotive Voice Recognition System Market

Brazil dominates the South American market with a 58.9% share, supported by its large automotive production base and growing demand for connected vehicles. The increasing adoption of infotainment systems, the gradual shift toward hybrid voice solutions, and rising SUV penetration are driving steady market expansion despite economic and cost-related constraints.

Middle East & Africa

The Middle East & Africa region is witnessing faster growth, driven by increasing demand for premium and connected vehicles, particularly in GCC countries. Markets such as the UAE and Saudi Arabia show higher adoption of advanced infotainment and voice-enabled systems due to higher purchasing power. South Africa contributes through its automotive base. The growth is supported by expanding connected services and SUV demand, though limited infrastructure and lower penetration in several African markets moderate overall regional expansion.

UAE Automotive Voice Recognition System Market

The UAE market is projected to grow at a CAGR of 16% over the forecast period, driven by strong demand for premium and connected vehicles. The high adoption of advanced infotainment systems, the increasing deployment of AI-based voice assistants, and the expansion of connected services in luxury SUVs support rapid growth, positioning the UAE as a key emerging market in the region.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Integration, Hybrid Architectures, and OEM Partnerships Define Competitive Intensity

The automotive voice recognition system market trends are moderately consolidated, with a mix of specialized voice technology providers and large automotive software and infotainment companies shaping competition. Key players such as Cerence, Bosch, HARMAN, SoundHound AI, Nuance (Microsoft), Amazon, and Google compete through advanced conversational AI platforms, multilingual capabilities, and deep integration with digital cockpit ecosystems. Companies are focusing on hybrid voice architectures combining on-board and cloud processing to enhance accuracy, latency, and reliability. Strategic collaborations with OEMs, cloud providers, and semiconductor firms are critical to expanding deployment across vehicle segments. Players are also investing in generative AI, personalization, and continuous OTA updates to improve user experience and differentiation.

- In January 2024, Mercedes-Benz integrated Microsoft Azure OpenAI into its MBUX system, enabling more natural, conversational in-car voice interactions and strengthening its competitive positioning in AI-driven automotive interfaces.

LIST OF KEY AUTOMOTIVE VOICE RECOGNITION SYSTEM COMPANIES PROFILED

- Cerence Inc. (U.S.)

- Nuance Communications, Inc. (U.S.)

- SoundHound AI, Inc. (U.S.)

- Microsoft Corporation (U.S.)

- Google LLC (U.S.)

- com, Inc. (U.S.)

- Apple Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- Huawei Technologies Co., Ltd. (China)

- HARMAN International Industries, Inc. (U.S.)

- Baidu, Inc. (China)

- Tencent Holdings Ltd. (China)

- Bosch Limited (Germany)

- Continental AG (Germany)

- Denso Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Automakers accelerated the deployment of AI-powered assistants in vehicles, with increasing integration of conversational AI to enhance in-car experiences. The report highlights how companies are moving beyond command-based systems toward intelligent assistants capable of contextual understanding, personalization, and seamless interaction across infotainment and connected services ecosystems.

- April 2026: Volkswagen intensified its focus on voice AI technology for Chinese vehicles, aiming to compete with domestic automakers offering advanced digital cockpits. The company is enhancing voice-enabled systems with localized AI capabilities, reflecting the growing importance of intelligent assistants in differentiating connected vehicles within the highly competitive Chinese automotive market.

- April 2026: BMW introduced Alexa-based conversational AI in its 2026 iX3, enabling more natural and interactive voice control within the vehicle. The system enhances user experience by supporting contextual conversations, infotainment control, and connected services, demonstrating the increasing integration of advanced voice assistants in next-generation electric vehicles.

- December 2025: Cerence launched new automotive AI agents that extend its conversational capabilities beyond the dashboard into ownership and servicing workflows. The company introduced an ownership companion agent that can answer vehicle questions, support diagnostics, and help schedule service, showing how voice-recognition vendors are expanding from in-car commands into broader automotive software ecosystems.

- April 2025: Kia launched its AI-powered voice assistant in Europe, expanding advanced conversational capabilities across its connected vehicle lineup. The system enables natural language interaction for navigation, infotainment, and vehicle functions, marking a shift toward generative AI-driven cockpit experiences.

REPORT COVERAGE

The global automotive voice recognition system market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on rapid technological advancements, new product launches, key industry developments, strategic partnerships, mergers & acquisitions. The market forecast provides a comprehensive competitive landscape, including the most significant global market shares, emerging opportunities, and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.2% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Deployment Type, By Application, By Vehicle Type, By Technology, and By Region |

| By Deployment Type |

|

| By Application |

|

| By Vehicle Type |

|

| By Technology |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.66 billion in 2025 and is projected to reach USD 7.51 billion by 2034.

In 2025, the market value stood at USD 1.32 billion.

The market demand is expected to grow at a CAGR of 12.2% from 2026 to 2034.

By deployment type, the embedded/on-board segment led the market share.

The rising demand for hands-free driving, the growth in connected and software-defined vehicles, and the wider use of smart infotainment systems are driving market momentum.

Key market players include Cerence, Bosch, HARMAN, and SoundHound AI.

The Asia Pacific region accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, South America, and the Middle East & Africa regions are considered in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us