Autonomous Defense Platforms Market Size, Share & Industry Analysis, By Platform Type (Uncrewed Aerial Systems, Uncrewed Ground Vehicles, Uncrewed Surface Vessels, Uncrewed Underwater Vehicles and Autonomous Fixed Defense Systems), By Level of Autonomy (Human-in-the-loop, Human-on-the-loop, Supervised autonomy / bounded autonomy and Mission-level autonomy), By Domain (Air, Land, Surface Maritime, Subsea and Multi-Domain), By Application (ISR & persistent surveillance, Mine countermeasures, Logistics & resupply, Combat support, & Others), By End User, and Regional Forecast, 2026-2034

Autonomous Defense Platforms Market Size and Future Outlook

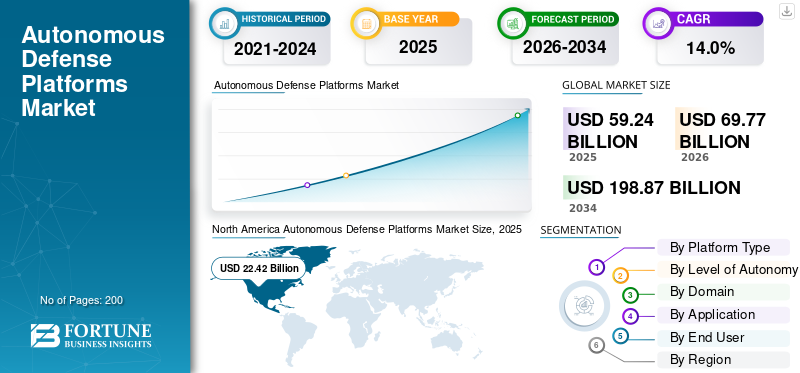

The autonomous defense platforms market size was valued at USD 59.24 billion in 2025. The market is projected to grow from USD 69.77 billion in 2026 to USD 198.87 billion by 2034, exhibiting a CAGR of 14.0% during the forecast period. North America dominated the autonomous defense platforms market with a market share of 37.54% in 2025.

The market includes defense technology focused on autonomous systems that can sense, decide and act during military operations. This includes Unmanned Aerial Vehicles (UAVs) and related systems. The demand for these platforms is increasing in North America, particularly in the U.S., due to tougher and faster command and control needs. Moreover, integration of artificial intelligence is the key driver for the market. AI-powered platforms provide real time awareness, threat detection and quicker decision-making for mission critical tasks, while also helping to protect vital infrastructure. Additionally, buyers are pushing suppliers for stronger supply chain resilience. However, autonomy is ineffective if parts, software updates, and maintenance cannot keep up.

Key players including BAE Systems plc and Northrop Grumman Corporation illustrate the influence of large companies on the market through integration and large-scale autonomy. BAE Systems plc. is enhancing defense capabilities by integrating autonomous defense technologies into modern command and control for military operations, with a strong focus on mission critical infrastructure. Northrop Grumman Corporation is deepening the role of AI in autonomy, enhancing AI powered sensing and real time threat detection, which supports UAVs and broader autonomous weapon systems. Both the companies continue to invest in supply chain resilience to ensure that these defense technology systems are available during truly mission critical operations.

Download Free sample to learn more about this report.

Autonomous Defense Platforms Market Key Takeaways

- 2025 Market Size: USD 59.24 billion

- 2026 Market Size: USD 69.77 billion

- 2034 Forecast Market Size: USD 198.87 billion

- CAGR: 14.0% from 2026–2034

- North America dominated the market with a 37.54% share in 2025.

- Uncrewed Aerial Systems (UAS) segment dominated the market in 2025.

- Air segment dominated the market in 2025.

North America

Led the market with USD 22.42 billion in 2025, driven by strong defense investments.

Asia Pacific

Fastest-growing region, projected to expand at a 15.5% CAGR.

Europe

Second-largest market, projected to grow at a 14.3% CAGR during the forecast period.

U.S.

The U.S. market was valued at USD 21.34 billion in 2025.

Japan

The Japan market is witnessing growth, supported by its multi-domain defense modernization program.

Read More

AUTONOMOUS DEFENSE PLATFORMS MARKET TRENDS

Shift toward Mass, Attritable Autonomy is an Emerging Market Trend

A significant market trend is the shift from a few high-end unmanned systems to a large number of cost-effective, attritable autonomous systems across air, land and sea. Militaries are also addressing the challenge of speed plus volume as they need to deploy autonomous platforms, update software and use it in groups or packs for gathering intelligence, providing strike support, and sensing in contested areas. This also encourages buyers to standardize interfaces as new payloads and AI can be swapped easily. Furthermore, it increases the need to strengthen supply chains, as scale only works if production and maintenance can ramp up.

In August 2023, the U.S. Department of Defense announced the Replicator initiative to deploy thousands of all-domain, attritable autonomous systems on an accelerated timeline and was delivered by August 2025. This clearly shows a shift toward scaled autonomy rather than small quantities.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing demand for AI-Powered Autonomy Fuels Market Growth

Global military forces are driving due to growing focus on investing in Artificial Intelligence (AI) and autonomous systems, especially Unmanned Aerial Vehicles (UAVs) and advanced robotic systems, to maintain their strategic advantage. As operational environments become faster, these technologies provide important benefits by assisting human decision-making and enhancing situational awareness in real time. These factors are driving autonomous defense platforms market growth.

In August 2025, Northrop Grumman Corporation partnered with Merlin on the Beacon project. They are integrating autonomous flight technology for U.S. defense testbeds to improve national security innovation.

MARKET RESTRAINTS

Safety, Legal and Policy Limitations on Autonomy Hinder Market Growth

A key challenge hampering the market is higher autonomy in systems that can choose and engage targets. These must undergo strict safety checks, legal requirements and policy reviews from top management. This process delays timelines, adds testing and verification needs, and makes procurement more cautious. Buyers usually prefer bounded autonomy with clear limits and human oversight. Even when funds are available, programs can get stuck in certification, negotiating rules of engagement and demonstrating reliable behavior in unusual scenarios.

MARKET OPPORTUNITIES

Increasing Navy Drone Focused Contracts Fuels Adoption of Collaborative Autonomy

Navies are trailing AI-driven platforms to work alongside manned jets. This change reduces risks in military operations while improving threat detection and real-time command and control. North America, particularly the U.S., stands to benefit significantly from these shifts in defense capabilities, driven by companies such as Northrop Grumman Corporation and RTX.

In September 2025, the U.S. Navy awarded contracts for Collaborative Combat Aircraft (CCA) drones to Northrop Grumman, Boeing, Lockheed, General Atomics, and Anduril. These contracts aim to strengthen carrier-based autonomous strikes.

MARKET CHALLENGES

Scaling Trust, Verification and Safe Autonomy for Combat-Ready Systems is a Major Challenge

While proof-of-concept demos are possible, the main challenge in autonomous defense is ensuring predictable and safe behavior in hostile, degraded, or contested environments (A2/AD). Making sure that systems comply in situations where civilians are nearby needs careful validation. This often leads to longer deployment timelines and higher costs, especially when autonomous systems dictate the use of force instead of just supporting it.

In January 2023, the U.S. Department of Defense updated DoD Directive 3000.09 (Autonomy in Weapon Systems). This update emphasizes the need for detailed hardware and software verification and validation, along with realistic developmental and operational testing before fielding.

Impact of Russia Ukraine War

Russia Ukraine War Has Increased Focus on Battlefield Tools Resulting in Higher Defense Spending

The rise of drones and loitering munitions has pushed militaries around the world to speed up production and deployment processes. In many cases, they have moved to a "mass production" approach. High-intensity operations and Electronic Warfare (EW) environments are also driving a shift toward affordable and easy-to-replace systems. These changes are supported by better counter-UAS technologies. As a result, there is greater demand for autonomous air and maritime platforms. This has led to shorter procurement cycles and an increased focus on supply chain security and manufacturing capacity.

SIPRI Yearbook 2025 discuss developments from 2024. It points out that 2024 reaffirmed the significant role of armed UAVs, with their development shaped by ongoing and extensive use, especially in the Russia-Ukraine war.

Segmentation Analysis

By Platform Type

Uncrewed Aerial Systems (UAS) Leads Due to Quick Deployed and Effective Performance

In terms of platform type, the market is categorized into Uncrewed Aerial Systems (UAS), Uncrewed Ground Vehicles (UGV), Uncrewed Surface Vessels (USV), Uncrewed Underwater Vehicles (UUV), and autonomous fixed defense systems.

In 2025, Uncrewed Aerial Systems (UAS) held the largest autonomous defense platform market share. Growth of this segment is attributed to their ability to deliver the quickest sensor-to-effect capability for modern militaries. UAS provide ongoing intelligence, surveillance, and reconnaissance (ISR), targeting support, and electronic warfare payload capacity. Also, they offer scalable mass at a lower, more accessible annual cost than traditional manned fleets, resulting in segment dominance.

In August 2023, the U.S. Department of Defense announced the Replicator initiative to deliver all-domain, low-cost autonomous systems at high volumes by August 2025. This shows that high-volume uncrewed systems, where UAS are usually the most developed and scalable, are a top priority for procurement.

Autonomous fixed defense systems segment in market expected to show fastest grow at a CAGR of 17.3% over the forecast period.

By Level of Autonomy

Strict Legal Rules Associated With Lethal Force Leads To Human-In-The-Loop Systems Segment Growth

On the basis of level of autonomy, the market is classified into Human-in-the-loop, Human-on-the-loop, Supervised autonomy / bounded autonomy, and Mission-level autonomy.

In 2025, human-in-the-loop (HITL) systems hold the largest market share. Defense forces uses this model to maintain human accountability for lethal actions. This is important for identifying targets, timing engagements and deploying weapons. Moreover, HITL is favored as it presents lower political risk, fits with current rules of engagement and has simpler testing and validation processes, resulting in segment adoption and dominance.

Mission-level autonomy is expected to show fastest market growth at a CAGR of 21.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Domain

Air Domain Leads Market as it Provide Rapid, Long-Range and High-Precision Intelligence

Based on domain, the market is segmented into, air, land, surface maritime, subsea, and multi-domain.

Air segment dominated the market in 2025, as autonomous air platforms offers immediate results on the ground, by offering the continuous surveillance and rapid response capabilities. Moreover, the offers edge over many ground and maritime systems, as air based systems allows rapid deployment, cost-effective scalability, and new software based upgrades to adapt with evolving threats, making them important assets for military operation, cause of which government spend larges budget on air domain, resulting in segment dominance.

In February 2026, the U.S. Air Force announced it is accelerating its Collaborative Combat Aircraft (CCA) initiative by using the government-owned Autonomy Government Reference Architecture (A-GRA) across various vendor platforms. This confirms an open, modular approach to integrating autonomy and highlights that autonomous air platforms are a major priority in the near future.

Subsea is fastest growing segment in market at a CAGR of 18.6% across the forecast period.

By Application

Increasing Demand for Situational Awareness in Challenged Environments Leads to ISR And Persistent Segment Growth

Based on application, the market is segmented into, ISR & persistent surveillance, Mine Countermeasures (MCM), logistics & resupply, combat support, seabed warfare & infrastructure protection, and others. ISR and persistent surveillance segment dominated the market in 2025, the segment dominance is attributed to increasing geopolitical tensions and the need for operating in asymmetric, and harsh environments, resulting in market shifting toward continuous Intelligence, Surveillance, and Reconnaissance (ISR). Defense forces are upgrading from traditional, intermittent patrols to a 24/7 continuous monitoring technology, which offers instant threats detection, tracking and enabling faster, proactive response.

In July 2024, NATO announced a new strategy through its national armaments directors. This plan aims to improve the NATO Intelligence, Surveillance and Reconnaissance Force (NISRF) with additional capabilities focused on strengthening NATO’s ISR and early warning/control abilities.

Seabed warfare & infrastructure protection is fastest growing segment in market at a CAGR of 21.1% across the forecast period.

By End User

Ongoing Need for Force Protection and Logistics Automation Contributes to Army Segment Dominance

Based on end user, the market is segmented into army, navy, air force, special operations forces, joint/integrated commands, and defense R&D agencies.

Armies segment are at the forefront in 2025 due to high volume of deployment of UGVs as well as UAVs for dangerous and labor dependent task such as logistic, reconnaissance, mine clearance, and among others. This dominance is further fueled by the need to reduce soldier risk in dangerous urban environments and modernization efforts of traditional, labor-intensive ground combat platforms, resulting in segment dominance.

In October 2024, Team RIPSAW (Textron Systems, Howe & Howe, Teledyne FLIR Defense) delivered two RIPSAW M3 prototype vehicles to the U.S. Army for the Robotic Combat Vehicle (RCV) Phase I, Platform Prototype program.

Joint/Integrated commands segment is expected to show fastest market growth at a CAGR of 20.4% across the forecast period.

Autonomous Defense Platforms Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Middle East, and Rest of the World (Africa and Latin America).

North America

North America Autonomous Defense Platforms Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is leads mainly as the U.S. prioritizes autonomy in military force design. This strategy focuses on quick deployment, integration across all areas, and large procurement. The region also has strong command-and-control systems and a robust defense industry, this industry has capability to prototype, test, and ramp up production faster than most other region. As a result, North America region not just purchase autonomous platforms, they create system of policies, command and control, testing pathways, and suppliers that enables large-scale deployment of autonomy.

In August 2023, the U.S. Department of Defense, through the DIU, announced Replicator. This initiative aims to deploy multiple thousands of all-domain attritable autonomous systems by August 2025.

U.S. Autonomous Defense Platforms Market

Based on North America size the U.S. dominance within the region, the U.S. market was at USD 21.34 billion in 2025, increasing at a CAGR of 12.7%.

Europe

Europe market was second largest in 2025. The Europe region is projected to have a CAGR of 14.3% over the forecast period. Europe is making rapid progress in autonomous defense platforms, by not only buying advanced platforms but also establishing standards for compatible autonomy in joint operations. Driven by NATO’s effort to improve joint ISR increases the need for autonomous sensing and persistence. Additionally, EU-funded programs are conducting field trials to validate manned-unmanned ground teaming and cross-domain, multi-platform compatibility. Russia continues to be a significant regional influence, acting both as a threat with electronic warfare, mass drones, and layered air defense, and as a reason for European militaries to focus on attritable systems and protect undersea infrastructure.

U.K. Autonomous Defense Platforms Market

U.K. market reached USD 2.05 billion in 2025, equivalent to around 12.74% of market revenues.

Germany Autonomous Defense Platforms Market

The Germany market was at USD 2.42 billion in 2025, representing roughly 15.05% of Europe revenues.

Asia Pacific

Asia Pacific market is third largest globally and is anticipated to be the fastest growing segment during the forecast period, growing at a CAGR of 15.5%. The regional demand focuses on maritime security and multi-domain deterrence, this includes island defense, long-range surveillance, and reliable communications and command. For instance, Japan’s Defense Buildup Program highlights the country’s commitment to creating a multi-domain force posture by integrating space, cyber, and electromagnetic domains. This approach includes unmanned and autonomous platforms in roles such as intelligence, surveillance, and reconnaissance, force protection, and strike support.

China Autonomous Defense Platforms Market

China’s market is projected to be one of the largest, with 2025 revenues at 6.39 billion, representing roughly 44.86% of Asia Pacific market sales.

India Autonomous Defense Platforms Market

The India market in 2025 was at USD 1.84 billion, accounting for roughly 12.92% of Asia Pacific market revenues.

Middle East

Middle East market anticipated to be the third fastest growing segment during the forecast period, growing at a CAGR of 14.6%. The Middle East market is shaped by rapid acquisitions and local industrial growth. Countries such as the UAE and Saudi Arabia are purchasing with goals for domestic production. They are creating autonomy programs, founding joint ventures, and establishing local manufacturing to reduce reliance on outside sources and improve delivery times. There is also a strong focus on systems that support border security, maritime safety, and the protection of critical infrastructure.

Saudi Arabia Autonomous Defense Platforms Market

Saudi Arabia market is projected to be one of the largest Middle East, with 2025 revenues at USD 0.91 billion, representing roughly 23.38% of Middle East market sales.

United Arab Emirates Autonomous Defense Platforms Market

United Arab Emirates market in 2025 was at USD 0.75 billion, accounting for roughly 19.12% of Asia Pacific market revenues.

Rest of the World

Rest of World (Africa and Latin America), has comparatively smaller in share but is growing at a CAGR of 11.7%. Adoption of autonomous defense platforms is taking place, but it is limited by budgets, maintenance, and training pipelines. Demand centers on practical, lower-cost autonomy such as ISR drones, base and convoy protection tools, and specific maritime autonomy. Latin America has a clearer path for autonomous maritime systems related to coastal security and mine countermeasure missions. Africa market growth is driven by increasing security threats, the need for modern surveillance, and rising defense expenditures, with projected 10.8% CAGR through 2034.

Latin America Autonomous Defense Platforms Market

The Latin America market was at USD 1.18 billion, accounting for roughly 45.38% of rest of the world revenues, in 2025.

Africa Autonomous Defense Platforms Market

Africa market was USD 1.42 billion in 2025, and is expected to reach USD 3.71 billion in 2034, representing roughly 54.62% of rest of the world Autonomous Defense Platforms sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competition Between Major Defense Companies and Flexible AI-Focused Firms Contributes to Market Expansion

North America is the center of the market. Companies such as Northrop Grumman Corporation and BAE Systems PLC are leading with AI-powered unmanned aerial vehicles (UAVs) and autonomous weapon systems, moreover these U.S. based firms have good ties with the United States military. Resulting they secure significant contracts and outpace their competitors in integrating defense technology for real-time threat detection and command and control.

Key companies include BAE Systems, Northrop Grumman, Lockheed Martin, RTX, and L3Harris, along with autonomy-focused firms such as Anduril and General Atomics. European companies including Thales and Saab also play significant roles in naval autonomy. The market currently focuses on AI-driven by verified progress done on open autonomy architectures. These architectures enable quicker integration of autonomy software and specific maritime autonomy programs moving into deployment. Competition now focuses more on software maturity, edge AI, surviving in contested environments, and scalable autonomy that can be used in various defense areas.

LIST OF KEY AUTONOMOUS DEFENSE PLATFORMS COMPANIES PROFILED

- BAE Systems plc. (U.K.)

- Northrop Grumman Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- RTX (Raytheon Technologies) (U.S.)

- General Dynamics Corporation (U.S.)

- Boeing Defense, Space & Security (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- General Atomics Aeronautical Systems, Inc. (U.S.)

- Anduril Industries (U.S.)

- Kratos Defense & Security Solutions, Inc. (U.S.)

- AeroVironment, Inc. (U.S.)

- Teledyne FLIR Defense (U.S.)

- SAIC (Science Applications International Corp.) (U.S.)

- Leonardo S.p.A. (Italy)

- Thales Group (France)

- Safran (France)

- Airbus Defence and Space (Europe)

- Saab AB (Sweden)

- Rheinmetall AG (Germany)

- Kongsberg Gruppen (Norway)

- Hensoldt AG (Germany)

- Elbit Systems Ltd. (Israel)

KEY INDUSTRY DEVELOPMENTS

- February 2026: The U.S. Air Force validated the government-owned Autonomy Government Reference Architecture across multiple vendor CCA platforms. This process strengthens the open-architecture approach, speeding up upgrades and reducing vendor lock-in for autonomous systems.

- December 2025: The U.K. Royal Navy, through DE&S, awarded Thales an initial USD 13.39 million contract for portable autonomous command centers for minehunting. This contract may grow to around USD 133.87 million as next-gen autonomous mine countermeasure capabilities expand.

- October 2024: Textron Systems, part of Team RIPSAW, delivered two RIPSAW M3 prototypes to the U.S. Army for Robotic Combat Vehicle Phase I. This delivery shows ongoing progress in autonomous and robotic ground combat platforms.

- July 2024: NATO announced that national armaments directors agreed on a strategy to improve NATO’s ISR Force with added capabilities. This move emphasizes the growing need for autonomous ISR and ongoing surveillance tools across the Alliance.

- March 2024: The U.K. government announced the AUKUS RAAIT trials as part of Project Convergence. These trials show real-time AI and autonomous sensing interoperability among partners. This is an important step toward compatible autonomy in coalitions.

- February 2024: The U.K. MoD announced a USD 2.34 billion, 15-year contract with Thales UK. This contract focuses on maintaining and modernizing key Royal Navy sensors and availability. It will use AI and data-driven maintenance, supporting the idea of AI-enabled readiness across defense platforms.

- August 2023: The DoD, through DIU, launched Replicator. This project aims to deliver multiple thousands of all-domain attritable autonomous systems by Aug 2025. It signals a shift toward larger-scale purchases and faster adoption.

- January 2023: The U.S. DoD reissued DoD Directive 3000.09 for Autonomy in Weapon Systems. This reinforces governance and highlights the importance of human judgment in using force. It also sets stricter expectations for verification and validation. These changes will affect how quickly higher-autonomy systems can be deployed.

REPORT COVERAGE

The global autonomous defense platforms market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 14.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation

|

By Platform Type

|

|

By Level of Autonomy

|

|

|

By Domain

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 69.77 billion in 2026 and is projected to reach USD 198.87 billion by 2034.

In 2025, the North America market value stood at USD 22.42 billion.

The market is expected to exhibit a CAGR of 14.0% during the forecast period of 2026-2034.

The Uncrewed Aerial Systems (UAS) led the market by platform type.

Urgency to scale mass autonomy for contested battlespaces drives market growth.

Key players in the market include BAE Systems, Northrop Grumman, Lockheed Martin, RTX, General Dynamics, Boeing Defense, L3Harris, General Atomics, Anduril Industries, Kratos Defense & Security Solutions, AeroVironment, Teledyne FLIR Defense, Thales, Airbus Defence and Space, Saab, Rheinmetall, Leonardo, Safran, Kongsberg, Hensoldt, and Elbit Systems.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us