Autonomous Maritime Drones Market Size, Share & Industry Analysis, By Platform Type (Unmanned Surface Vehicles (USVs) and Unmanned Underwater Vehicles (UUVs/AUVs)), By Autonomy Level (Remotely Operated, Semi-Autonomous, and Fully Autonomous), By Size Class (Small, Medium, Large, and Extra-Large), By Payload Type (Sonar Systems, EO/IR Cameras, Radars, SIGINT/EW Systems, Oceanographic Sensors, and Others), By End User (Defense & Naval Forces, Coast Guard & Homeland Security, Commercial Offshore, Marine Research & Academia, Environmental & Government Agencies), & Regional Forecast, 2026-2034

Autonomous Maritime Drones Market Size and Future Outlook

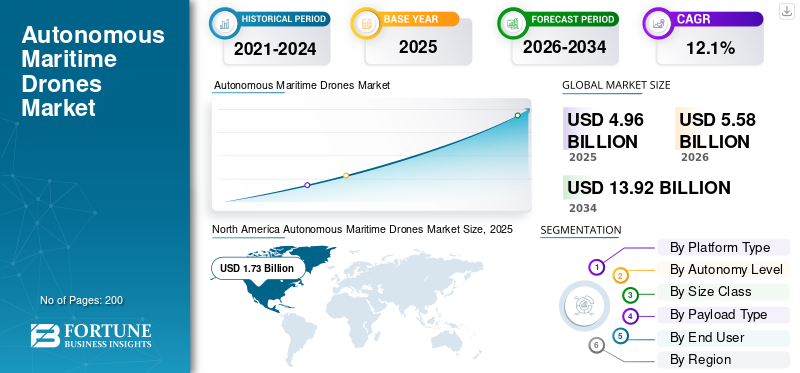

The global autonomous maritime drones market size was valued at USD 4.96 billion in 2025. The market is projected to grow from USD 5.58 billion in 2026 to USD 13.92 billion by 2034, exhibiting a CAGR of 12.1% during the forecast period. North America dominated the autonomous maritime drones market with a market share of 34.88% in 2025.

The global market encompasses advanced uncrewed systems designed for diverse operations across surface and underwater environments. These platforms are increasingly leveraging sophisticated technologies, including artificial intelligence for autonomous navigation, real-time data processing, and multi-sensor fusion. Industry participants are prioritizing the integration of satellite communications and swarm capabilities to enhance operational endurance and situational awareness beyond visual ranges. As the sector matures, the focus remains on deploying scalable, intelligent solutions capable of executing complex missions with high precision, representing a significant shift toward modernized, automated maritime infrastructure and resilient, remote-operated marine asset management systems.

Key players in the autonomous maritime drones market include Saildrone, Inc., Ocean Infinity, Saronic Technologies, Anduril Industries, Inc., Huntington Ingalls Industries, Inc., Kongsberg Discovery AS, Teledyne Marine, The Boeing Company, L3Harris Technologies, Inc., and Exail Technologies. These companies compete by advancing autonomous surface and underwater vessel capabilities, integrating sophisticated AI-driven navigation, and providing scalable, long-endurance platforms for complex missions.

Download Free sample to learn more about this report.

Autonomous Maritime Drones Market Key Takeways

- 2025 Market Size: USD 4.96 billion

- 2026 Market Size: USD 5.58 billion

- 2034 Forecast Market Size: USD 13.92 billion

- CAGR: 12.1% from 2026–2034

- North America dominated the autonomous maritime drones market with a 34.88% share in 2025.

- The unmanned underwater vehicles (UUVs/AUVs) segment is expected to witness strong growth during the forecast period.

- The fully autonomous segment is projected to register the fastest growth over the forecast period.

North America

North America remained the leading regional market, reaching USD 1.73 billion in 2025 after being valued at USD 1.55 billion in 2024.

Europe

Europe is expected to remain the second-largest regional market, reaching USD 1.59 billion in 2026.

Asia Pacific

Asia Pacific is projected to record the highest regional growth rate of 13.0% during the forecast period, reaching USD 1.44 billion in 2026.

U.S.

U.S. The market is estimated to reach approximately USD 1.67 billion in 2026, supported by strong investments in maritime defense and autonomous technologies.

Japan

Japan The market is projected to reach around USD 0.26 billion in 2026, driven by advancements in marine robotics and ocean monitoring initiatives.

Read More

AUTONOMOUS MARITIME DRONES MARKET TRENDS

Technological Convergence and AI-Driven Autonomy Represent a Significant Market Trend

The market is currently defined by a rapid shift toward sophisticated AI-powered navigation and edge computing, allowing maritime drones to perform increasingly complex, long-duration missions without human intervention. Industry leaders are focusing on the integration of hybrid propulsion systems, which combine traditional power with renewable energy sources to significantly extend operational range. Furthermore, the development of swarm coordination technologies and multi-sensor fusion capabilities is enabling cooperative intelligence, where multiple drones act as a unified, resilient network. This trend is centralizing the move toward fully autonomous maritime ecosystems that prioritize real-time decision-making and operational resilience in harsh marine environments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Persistent Maritime Surveillance Continue to Support Market Expansion

The primary driver for autonomous maritime drones market growth is the urgent, global need for persistent, scalable, and cost-effective maritime security and border patrol capabilities. Rising geopolitical tensions, the necessity to combat illicit activities such as piracy and smuggling, and the requirement for round-the-clock monitoring of critical maritime infrastructure have made autonomous drones an essential asset. These systems offer significant operational advantages, including the ability to operate in hazardous, remote, or extreme weather conditions while drastically reducing risk to human personnel. As governments prioritize maritime domain awareness, the demand for autonomous surveillance solutions is expected to remain a powerful catalyst for long-term expansion.

MARKET RESTRAINTS

Complex Regulatory Landscape and Operational Standards to Limit the Pace of Adoption

A significant restraint for market expansion is the highly fragmented and stringent international regulatory environment governing maritime drone operations. The lack of unified certification standards, combined with restrictive beyond-visual-line-of-sight (BVLOS) flight rules in many jurisdictions, poses a substantial hurdle to the widespread deployment of autonomous fleets. Many operators face long delays in obtaining necessary approvals to integrate drones into congested shipping lanes and busy commercial aviation corridors. Until globally harmonized regulations and mature safety-of-flight standards are established, the scalability of autonomous maritime missions will remain limited, hindering the ability of firms to operate effectively across diverse international maritime zones.

MARKET OPPORTUNITIES

Expanding Roles in Offshore Energy and Defense to Create Strong Market Opportunities

A significant growth opportunity lies in the expansion of offshore wind infrastructure and global maritime defense requirements. These sectors necessitate continuous, high-fidelity seabed mapping, subsea asset inspection, and persistent surveillance capabilities that autonomous drones can provide more cost-effectively than manned vessels. Additionally, the emergence of drone-as-a-service and flexible leasing business models is lowering capital entry barriers, enabling a wider array of commercial and governmental operators to deploy autonomous fleets. By integrating these systems into broader smart maritime IoT networks, service providers can unlock new recurring revenue streams while improving the safety and efficiency of critical marine operations.

MARKET CHALLENGES

Technological Hurdles and Cybersecurity Vulnerabilities are Major Challenges in the Market

The industry faces significant technical and strategic challenges, particularly regarding the need for constant, high-energy R&D investment to overcome bottlenecks in propulsion and advanced AI navigation. Ensuring the cybersecurity of autonomous platforms is another critical challenge, as drones become increasingly interconnected and reliant on satellite data links, making them potential targets for signal jamming or data hijacking. Furthermore, successfully integrating these high-tech platforms into traditional, legacy maritime workflows remains a major hurdle. Operators must contend with the high initial capital expenditure of sophisticated sensors and hardware while managing the ongoing technical complexities of maintaining robust, reliable, and secure autonomous marine operations.

Segmentation Analysis

By Platform Type

Rising Need for Safer Surface Operations to Drive Unmanned Surface Vehicles (USVs) Segment Growth

Based on platform type, the market is segmented into unmanned surface vehicles (USVs) and unmanned underwater vehicles (UUVs/AUVs).

The unmanned surface vehicles (USVs) segment is anticipated to account for the largest autonomous maritime drones market share. The demand for unmanned surface vehicles is increasing as navies, coast guards, and offshore operators prioritize crew safety and persistent maritime presence. USVs enable surveillance, patrol, mine countermeasure support, and hydrographic missions without exposing personnel, while their modular payload capability supports a wide range of defense and commercial applications.

The unmanned underwater vehicles (UUVs/AUVs) segment is anticipated to rise at a CAGR of 12.4% over the forecast period.

By Autonomy Level

Remotely Operated Segment Led the Market Owing to Continued Requirement for Human Oversight in Critical Operations

Based on autonomy level, the market is segmented into remotely operated, semi-autonomous, and fully autonomous.

In 2025, the remotely operated segment dominated the global market. The demand for remotely operated systems remains strong as many maritime missions still require direct human supervision, particularly in congested ports, offshore energy zones, and sensitive defense environments. Regulatory constraints, safety considerations, and mission accountability continue to make remote operation a preferred choice in early-stage autonomy adoption.

The fully autonomous segment is projected to grow at a CAGR of 12.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Size Class

Medium Segment Dominated the Market due to Increasing Preference for Cost-Efficient and Multi-Payload Platforms

Based on size class, the market is segmented into small, medium, large, and extra-large.

The medium segment is anticipated to witness a dominating market share over the forecast period. The demand for medium-class autonomous maritime drones is rising as they provide an optimal balance between endurance, payload capacity, and cost. These platforms are versatile enough to support sonar, EO/IR, radar, and environmental sensors while remaining easier to deploy and maintain compared to larger systems.

The large segment is projected to grow at a high CAGR of 12.8% over the forecast period.

By Payload Type

Growing Focus on Underwater Threat Detection to Bolster Sonar Systems Segment Growth

Based on payload type, the market is segmented into sonar systems, EO/IR cameras, radars, SIGINT/EW systems, oceanographic sensors, and others.

The sonar systems segment dominated the global market share in 2025. Demand for sonar systems is increasing as maritime operators require reliable underwater detection for mine identification, anti-submarine warfare, and seabed mapping. Since underwater visibility is limited, sonar remains the primary sensing technology, making it a critical payload across UUVs, AUVs, and integrated maritime drone operations.

In addition, the SIGINT/EW systems segment is projected to grow at a CAGR of 14.3% during the analysis period.

By End User

Rising Naval Modernization to Drive the Defense & Naval Forces Segment Growth

Based on end user, the market is segmented into defense & naval forces, coast guard & homeland security, commercial offshore, marine research & academia, environmental & government agencies, and others.

The defense & naval forces segment dominated the global market share in 2025. The product demand across these forces is growing as militaries invest in autonomous maritime drones for intelligence, surveillance, and reconnaissance (ISR), mine countermeasures, port security, and anti-submarine operations. These systems enhance operational reach, reduce human risk, and support continuous surveillance in contested and strategically sensitive maritime regions.

In addition, the commercial offshore segment is projected to grow at a CAGR of 13.5% during the forecast period.

Autonomous Maritime Drones Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Autonomous Maritime Drones Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 1.55 billion, and also maintained the leading share in 2025, with USD 1.73 billion. The North America demand is driven by U.S. naval modernization, unmanned fleet experimentation, mine countermeasure programs, offshore security, and advanced autonomy development. Strong defense budgets and technology suppliers keep the region ahead in adoption.

U.S. Autonomous Maritime Drones Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.67 billion in 2026, accounting for a CAGR of roughly 11.5% during the forecast period. The product demand in the U.S. is led by navy investment in unmanned surface and undersea systems, distributed maritime operations, mine warfare replacement programs, and Indo-Pacific surveillance needs, supported by a strong domestic defense technology base.

Europe

The Europe market is estimated to reach USD 1.59 billion in 2026 and secure the position of the second largest region in the market. The product demand is rising due to NATO maritime security needs, North Sea infrastructure protection, Baltic surveillance, mine-countermeasure modernization, and growing investment in autonomous naval systems across the U.K., France, Germany, and Nordic countries.

U.K. Autonomous Maritime Drones Market

The U.K. market is estimated to touch around USD 0.33 billion in 2026, representing a CAGR of roughly 11.8% during the forecast period. The product demand in the U.K. is rising as the Royal Navy strengthens mine-countermeasure, seabed security, and autonomous vessel programs. Offshore infrastructure protection and NATO maritime commitments also support adoption across surface and underwater platforms.

Germany Autonomous Maritime Drones Market

The Germany market is projected to reach approximately USD 0.30 billion in 2026. The product demand in the country is supported by Baltic and North Sea security needs, mine-countermeasure modernization, port protection, and growing interest in autonomous systems for surveillance, seabed monitoring, and naval support missions.

Asia Pacific

The Asia Pacific market is projected to record a growth rate of 13.0% during the forecast period, which is the highest among all regions, and reach a valuation of USD 1.44 billion by 2026. The regional product demand is increasing due to contested sea lanes, island defense, maritime border monitoring, and rapid naval modernization. China, India, Japan, South Korea, and Australia are expanding unmanned maritime capabilities for surveillance and deterrence.

China Autonomous Maritime Drones Market

The China market is projected to be one of the largest markets in Asia Pacific, with 2026 revenues estimated to touch around USD 0.53 billion. The product demand in China is expanding due to naval modernization, South China Sea monitoring, undersea surveillance, and unmanned platform development. Domestic shipbuilding strength and defense technology investment support large-scale adoption.

Japan Autonomous Maritime Drones Market

The Japan market share is estimated to reach around USD 0.26 billion in 2026, accounting for a CAGR of roughly 12.2% during the forecast period. The drone demand is driven by island defense, undersea surveillance, mine countermeasures, and maritime domain awareness. Rising security concerns in surrounding waters are encouraging the greater use of autonomous surface and underwater systems.

India Autonomous Maritime Drones Market

The India market is estimated to touch a value of around USD 0.24 billion in 2026. The product demand in the country is increasing as the navy strengthens maritime surveillance, coastal security, mine countermeasures, and Indian Ocean monitoring. Indigenous defense programs and unmanned systems procurement are making India one of the markets growing at a faster rate.

Rest of the World

The rest of the world includes the Middle East and Africa and Latin America. These regional markets are expected to witness moderate growth during the forecast period. The Middle East & Africa and Latin America markets are set to reach valuation of USD 0.36 billion and USD 0.25 billion in 2026. The product demand in the rest of the world is supported by offshore energy security, port protection, coastal surveillance, and naval modernization in the Middle East, Latin America, and Africa. The product adoption remains smaller but steadily expanding.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies to Launch New Unmanned Surface and Underwater Platforms to Consolidate their Market Positions

The autonomous maritime drones market is being reshaped by the rising need for continuous maritime domain awareness, distributed naval operations, and reduced human risk in contested and remote waters. End users are no longer seeking standalone platforms. They increasingly demand integrated, mission-ready systems that combine surface and underwater vehicles, advanced payloads such as sonar, EO/IR, and SIGINT, secure communications, AI-driven autonomy, and fleet-level command-and-control integration. Performance is defined by how effectively these systems can detect, classify, track, and respond across long-duration missions with minimal human intervention. The product demand is growing across both new procurement programs and fleet modernization efforts, while lifecycle spending is expanding as software upgrades, sensor integration, maintenance, and autonomy enhancements remain critical for sustained operational effectiveness.

Key players such as Saildrone, Ocean Infinity, Saronic Technologies, Anduril Industries, Huntington Ingalls Industries are strengthening their autonomous maritime portfolios through new unmanned surface and underwater platforms, advanced sensor payloads, AI-enabled autonomy, and naval mission integration. These companies are also expanding trials, defense partnerships, offshore survey programs, and fleet-scale deployment models. These aspects are helping move the market from limited experimentation toward operational adoption across surveillance, seabed mapping, mine countermeasures, and maritime security missions.

LIST OF KEY AUTONOMOUS MARITIME DRONES COMPANIES PROFILED

- Saildrone, Inc. (U.S.)

- Ocean Infinity (U.K.)

- Saronic Technologies (U.S.)

- Anduril Industries, Inc. (U.S.)

- Huntington Ingalls Industries, Inc. (U.S.)

- Kongsberg Discovery AS (Norway)

- Teledyne Marine (U.S.)

- The Boeing Company (U.S.)

- L3Harris Technologies, Inc. (U.S.)

- Exail Technologies (France)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Saronic raised a value of USD 1.75 billion in a Series D funding round to accelerate the production of autonomous surface vessels (USVs) for the U.S. Navy.

- February 2026: Elbit Systems secured USD 277 million in contracts from an undisclosed international customer for unmanned systems.

- January 2026: Ocean Aero secured Series D funding to continue the development of its Triton autonomous underwater/surface vehicles.

- April 2025: Boeing secured a contract from the U.S. Navy to deliver five additional Orca Extra-Large Unmanned Undersea Vehicles (XLUUVs).

- August 2024: Anduril Industries secured a USD 249.9 million contract to provide enhanced air defense capabilities, furthering its work on autonomous maritime systems.

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study also highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Platform Type, By Autonomy Level, By Size Class, By Payload Type, By End User, and Region |

| By Platform Type |

|

| By Autonomy Level |

|

| By Size Class |

|

| By Payload Type |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.96 billion in 2025 and is projected to reach USD 13.92 billion by 2034.

In 2025, the North America market value stood at USD 1.73 billion.

The market is expected to exhibit a CAGR of 12.1% during the forecast period of 2026-2034.

By end user, the defense & naval forces segment dominated the market in 2025.

The rising demand for persistent maritime surveillance continue is a key factor supporting market expansion.

Saildrone, Inc. (U.S.), Ocean Infinity (U.K.), Saronic Technologies (U.S.), Anduril Industries, Inc. (U.S.), Huntington Ingalls Industries, Inc. (U.S.), and Kongsberg Discovery AS (Norway) are major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us