Autonomous Mining Equipment Market Size, Share & Industry Analysis, By Equipment Type (Autonomous Haul Trucks, Autonomous Drilling Rigs, Autonomous Loaders (LHDs), Autonomous Dozers, Autonomous Graders, and Others), By Mining Type (Surface Mining, Underground Mining, and Others) , By Autonomy (Semi-Autonomous and Full Autonomous) By Propulsion Type (Diesel-Powered, Electric / Battery-Powered, Hybrid, and Others), By Application (Material Handling, Drilling & Blasting, Site Preparation & Development, Inspection & Monitoring, and Others), and Regional Forecast, 2026-2034

Autonomous Mining Equipment Market Size and Future Outlook

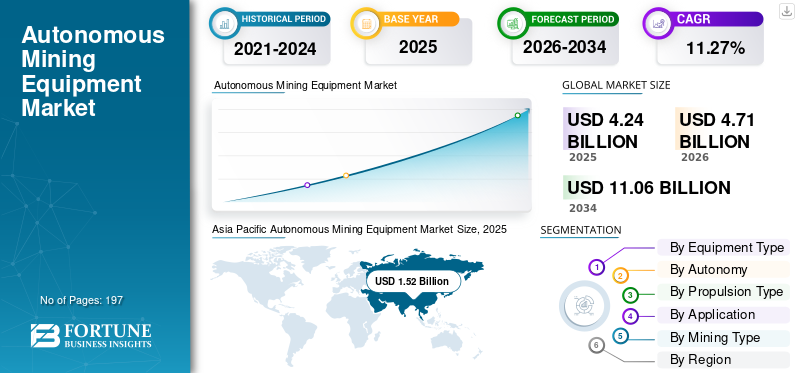

The global autonomous mining equipment market size was valued at USD 4.24 billion in 2025. The market is projected to grow from USD 4.71 billion in 2026 to USD 11.06 billion by 2034, exhibiting a CAGR of 11.27% during the forecast period. Asia Pacific dominated the autonomous mining equipment market with a market share of 35.84% in 2025.

Autonomous mining equipment represents a transformative advancement in the mining industry, enabling the automation of critical operations such as drilling, hauling, loading, and material handling with minimal human intervention. These systems integrate advanced technologies including artificial intelligence, machine learning, GPS, LiDAR, and real-time data analytics to enhance operational precision, safety, and productivity. Unlike conventional mining equipment, autonomous solutions operate through centralized control systems and sensor-driven navigation, allowing continuous and optimized performance even in complex and hazardous mining environments. Widely adopted across surface and underground mining applications, these technologies play a vital role in improving operational efficiency, reducing labor dependency, and ensuring consistent output, making them an essential component of modern digital mining ecosystems.

The demand for autonomous mining equipment is experiencing robust growth, driven by increasing pressure on mining companies to improve productivity, reduce operational costs, and enhance worker safety. The rising complexity of ore extraction, declining ore grades, and the need for efficient resource utilization are accelerating the adoption of automation technologies across mining operations. Additionally, advancements in connectivity, edge computing, and predictive analytics are enabling real-time decision-making and seamless equipment coordination. Industry trends such as smart mining, digital transformation, and the integration of IoT-enabled systems are further supporting market expansion.

The global market is moderately consolidated, characterized by the strong presence of leading mining equipment manufacturers alongside specialized technology providers. Key players such as Caterpillar Inc., Komatsu Ltd., Sandvik AB, Epiroc AB, and Hitachi Construction Machinery dominate the market through advanced autonomous haulage systems, drilling solutions, and integrated digital platforms. Moreover, emerging technology firms and regional players are contributing to market competitiveness by offering innovative, cost-effective, and application-specific solutions. Market participants are increasingly focusing on technological advancements in AI-driven automation, fleet management systems, and interoperability with existing mining infrastructure. Strategic initiatives including partnerships with mining companies, expansion into emerging mining regions, and continuous investment in R&D are shaping the competitive landscape and supporting the long-term growth of the market.

Download Free sample to learn more about this report.

Autonomous Mining Equipment Market Trends

Increasing Adoption of Automation and Smart Mining Technologies to be a Significant Market Trend

The rapid integration of automation and smart mining technologies is significantly accelerating the growth of the market. Mining companies are increasingly deploying advanced solutions such as Autonomous Haulage Systems (AHS), robotic drilling equipment, and AI-powered fleet management platforms to enhance operational efficiency and productivity. These technologies enable real-time monitoring of equipment performance, optimized route planning, and improved resource allocation, allowing operators to reduce downtime and maximize output. As mining operations become more complex and cost-sensitive, the shift toward intelligent, data-driven systems is becoming essential for maintaining competitiveness and operational consistency.

Furthermore, the transition toward digital mining ecosystems is reinforcing the adoption of autonomous equipment across both surface and underground operations. The integration of Internet of Things (IoT) sensors, machine learning algorithms, and predictive maintenance tools is enabling continuous performance optimization under dynamic mining conditions. These systems not only enhance equipment utilization but also minimize unexpected failures and maintenance costs. Additionally, increasing emphasis on worker safety and the need to operate in hazardous or remote environments are encouraging mining companies to adopt autonomous solutions that reduce human exposure to risk while ensuring uninterrupted operations.

For instance, during 2023–2025, leading mining companies such as Rio Tinto, BHP, and Fortescue Metals Group continued expanding the deployment of autonomous haul trucks and drilling systems across large-scale mining sites, particularly in Australia’s iron ore sector. At the same time, equipment manufacturers including Caterpillar, Komatsu, Sandvik, and Epiroc advanced their autonomous technology portfolios through AI-enabled control systems, remote operation centers, and integrated digital platforms. Strategic collaborations between mining operators and technology providers during this period further strengthened the adoption of autonomous solutions, supporting improved productivity, enhanced safety standards, and long-term operational efficiency across the global mining industry.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Focus on Worker Safety and Operational Efficiency is Driving Market Growth

The increasing emphasis on improving worker safety and enhancing operational efficiency is a major factor driving the adoption of autonomous mining equipment. Mining environments are inherently hazardous, involving risks such as equipment collisions, exposure to dust and toxic gases, and unstable geological conditions. Autonomous equipment minimizes human intervention in high-risk areas by enabling remote operations and fully automated workflows. Additionally, these systems operate with high precision and consistency, reducing operational errors and improving overall productivity. As mining companies aim to ensure safer working conditions while maintaining output efficiency, the demand for autonomous solutions continues to rise significantly.

For instance, in 2024, Rio Tinto expanded its autonomous haulage operations in the Pilbara region, increasing the deployment of driverless trucks to enhance safety and improve operational efficiency across its iron ore mines, reinforcing the growing reliance on automation in mining operations.

MARKET RESTRAINTS

High Initial Investment and Integration Complexity are Limiting Market Expansion

Despite the long-term benefits, the autonomous mining equipment market growth is constrained by high upfront costs and complex integration requirements. Implementing autonomous systems involves substantial capital investment in advanced machinery, sensors, communication infrastructure, and software platforms. Moreover, integrating these systems with existing mining operations and legacy equipment can be technically challenging and time-consuming. Small and mid-sized mining companies, in particular, may face financial and operational barriers in transitioning to automation. These factors can slow down adoption rates, especially in developing regions where budget constraints and infrastructure limitations persist.

For instance, in 2025, industry discussions led by organizations such as the International Council on Mining and Metals (ICMM) highlighted the challenges associated with integrating autonomous technologies into existing mining infrastructure, particularly in brownfield projects, emphasizing cost and interoperability concerns.

MARKET OPPORTUNITIES

Advancements in AI, IoT, and Predictive Analytics are Creating Growth Opportunities

Technological advancements in artificial intelligence, Internet of Things (IoT), and predictive analytics are creating significant growth opportunities in the market. These innovations enable real-time data processing, intelligent decision-making, and predictive maintenance, allowing mining operators to optimize performance and reduce downtime. The increasing adoption of connected mining ecosystems and digital twin technologies is further enhancing equipment efficiency and lifecycle management. Additionally, the expansion of mining activities in remote and resource-rich regions is driving the need for autonomous solutions that can operate with minimal human intervention. These trends are expected to unlock new revenue streams and accelerate market growth in the coming years.

For instance, in 2024, Caterpillar announced advancements in its autonomous haulage technology integrated with AI-driven fleet analytics platforms, enabling enhanced real-time decision-making and predictive maintenance capabilities for mining operators.

MARKET CHALLENGES

Workforce Adaptation and Cybersecurity Risks are Emerging Challenges to Market Growth

The transition toward autonomous mining operations presents challenges related to workforce adaptation and cybersecurity. As automation reduces the need for manual labor, there is a growing need to reskill and upskill the workforce to manage and maintain advanced systems. Resistance to technological change and lack of skilled personnel can hinder smooth implementation. Furthermore, the increasing reliance on connected systems and digital platforms exposes mining operations to cybersecurity risks, including data breaches and system disruptions. Ensuring robust cybersecurity frameworks and effective workforce training programs is essential for the sustainable adoption of autonomous mining technologies.

For instance, in 2025, mining technology forums and industry stakeholders emphasized the increasing importance of cybersecurity frameworks and workforce upskilling initiatives to support the safe deployment of autonomous mining systems, highlighting evolving operational risks in digitally connected mines.

Segmentation Analysis

By Equipment Type

Ability of Autonomous Haul Trucks to Operate Continuously with Optimized Routes and Reduced Downtime Led to its Dominance

Based on equipment type, the market is segmented into autonomous haul trucks, autonomous drilling rigs, autonomous loaders (LHDs), autonomous dozers, autonomous graders, and others.

The autonomous haul trucks segment dominated the autonomous mining equipment market share, accounting for the 40.18% in 2025, driven by its widespread deployment in large-scale surface mining operations. Autonomous haulage systems (AHS) are extensively used in iron ore, coal, and copper mines, particularly in Australia, North America, and Latin America. These systems significantly reduce fuel consumption, improve cycle efficiency, and enhance operational safety by minimizing human intervention. The ability of haul trucks to operate continuously with optimized routes and reduced downtime further strengthens their dominance in the market.

The autonomous drilling rigs segment is emerging as the fastest-growing segment, growing at a CAGR of 15.03% during the forecast period. The growth is driven by increasing demand for precision drilling, improved fragmentation outcomes, and reduced operational risks. Mining companies are increasingly adopting automated drilling systems integrated with AI and real-time data analytics to enhance accuracy and productivity, especially in underground and hard-rock mining environments.

By Autonomy

Semi-Autonomous Segment Dominated as it Offers a Lower Initial Investment and Easier Integration with Existing Mining Infrastructure

Based on autonomy, the market is segmented into semi-autonomous and fully autonomous.

The semi-autonomous segment accounted for a substantial market share in 2025, as mining companies continue to adopt gradual automation strategies. These systems allow operators to retain partial control while benefiting from automation features such as assisted driving, collision avoidance, and automated drilling cycles. Semi-autonomous solutions offer a lower initial investment and easier integration with existing mining infrastructure, making them a preferred choice for many operators.

The fully autonomous segment is projected to witness the fastest growth, driven by increasing investments in digital mining and remote operation centers. Fully autonomous systems enable end-to-end automation of mining operations, reducing labor dependency and enhancing safety in hazardous environments. Continuous advancements in AI, machine learning, and sensor technologies are accelerating the transition toward fully autonomous mining ecosystems. The fully autonomous segment will grow at a CAGR of 13.76% during the forecast period.

By Propulsion Type

Established Presence and Reliability in Heavy-Duty Mining Operations Led to Dominance of Diesel-Powered Segment

Based on propulsion type, the market is segmented into diesel-powered, electric/battery-powered, hybrid, and others.

The diesel-powered segment held the largest market share accounting for 69.64% share in 2025, owing to its established presence and reliability in heavy-duty mining operations. Diesel-powered autonomous equipment is widely used due to its high power output, operational flexibility, and suitability for remote mining locations with limited charging infrastructure.

The electric/battery-powered segment is expected to grow at the fastest pace, driven by increasing emphasis on sustainability and emission reduction. Mining companies are actively investing in electrified autonomous fleets to comply with stringent environmental regulations and reduce carbon footprints. The integration of battery technologies with autonomous systems is further enhancing productivity and reducing total cost of ownership over the long term. The electric/battery-powered segment is growing at a CAGR of 15.71% during the forecast period.

By Application

Improved Operational Efficiency, Reduced Fuel Consumption, and Ensured Consistent Performance Led to Dominance of Material Handling Segment

Based on application, the market is segmented into material handling, drilling & blasting, site preparation & development, inspection & monitoring, and others.

The material handling segment accounted for the highest share contributing to 46.24% of the market, supported by extensive use of autonomous haul trucks and loaders in transporting ore and overburden materials. Automation in material handling improves operational efficiency, reduces fuel consumption, and ensures consistent performance across mining cycles, making it a critical application area.

The drilling & blasting segment is anticipated to register the fastest growth, driven by the increasing adoption of automated drilling technologies for precision and safety. Autonomous drilling systems enable optimized blast patterns, reduced material wastage, and improved downstream processing efficiency.

By Mining Type

To know how our report can help streamline your business, Speak to Analyst

Surface Mining Segment Dominated Market Owing to their Large Scale Operations & Higher Adoption of Autonomous Equipment

Based on mining type, the market is segmented into surface mining, underground mining, and others.

The surface mining segment dominated the market in 2025, driven by its large-scale operations and higher adoption of autonomous equipment. Surface mines, including open-pit and strip mining operations, extensively utilize autonomous haul trucks, drills, and dozers to handle large volumes of material efficiently. The deployment of Autonomous Haulage Systems (AHS) is particularly high in surface mining due to well-defined haul routes, predictable environments, and the ability to operate equipment continuously with minimal human intervention. Major mining regions including Australia, North America, and Latin America have significantly invested in surface mining automation to enhance productivity, reduce fuel consumption, and improve safety outcomes.

The underground mining segment is expected to witness the fastest growth, driven by increasing demand for safety and operational efficiency in complex mining environments. Underground mines pose higher risks due to confined spaces, limited visibility, and hazardous working conditions, which is accelerating the adoption of Autonomous Loaders (LHDs), drilling rigs, and remote-controlled equipment.

Autonomous Mining Equipment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Autonomous Mining Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominated the global market, accounting for approximately USD 1.52 billion in 2025. The growth is driven by the region’s large-scale mining operations, particularly in iron ore, coal, and metals, along with increasing adoption of automation technologies across Australia, China, and India. The region benefits from high mining output, presence of mega mining sites, and strong investments in digital mining solutions, which are encouraging the deployment of autonomous haul trucks, drilling systems, and loaders. Additionally, increasing focus on improving operational efficiency, reducing labor dependency, and enhancing safety in hazardous mining environments is further supporting market growth.

Australia Autonomous Mining Equipment

In 2025, the Australian market reached a valuation of approximately USD 0.52 billion. The market is growing due to large-scale deployment of autonomous haulage systems by leading mining companies such as Rio Tinto, BHP, and Fortescue. High adoption of advanced automation technologies and strong presence of large iron ore mines are further accelerating demand.

China Autonomous Mining Equipment

The Chinese market was valued at around USD 0.40 billion in 2025. The growth is driven by extensive mining activities, increasing government support for smart mining initiatives, and rising adoption of autonomous and digitally integrated mining solutions across coal and metal mining sectors.

North America

North America was valued at approximately USD 0.94 billion in 2025. The region is growing due to the presence of large mining companies, increasing adoption of advanced automation technologies, and strong focus on improving productivity and safety standards. The region is witnessing rising investments in autonomous haulage systems, remote operation centers, and AI-driven mining solutions to optimize operational efficiency and reduce costs.

U.S. Autonomous Mining Equipment

The U.S. market was approximated at USD 0.69 billion in 2025. The growth is driven by increasing deployment of autonomous equipment in large mining operations, strong technological capabilities, and rising focus on digital transformation across the mining industry.

Europe

The Europe region accounted for approximately USD 0.69 billion in 2025. The market is growing in the region due to strong presence of leading OEMs, increasing adoption of underground mining automation, and rising focus on safety and efficiency. The region is at the forefront of mining technology innovation, particularly in autonomous drilling and loader systems.

Sweden Autonomous Mining Equipment

The Sweden market was valued at approximately USD 0.17 billion in 2025. The market is supported by the presence of major equipment manufacturers such as Sandvik and Epiroc, along with high adoption of advanced underground mining automation technologies.

Finland Autonomous Mining Equipment

The Finland market was valued at around USD 0.14 billion in 2025. The growth is driven by strong mining automation ecosystem, increasing investments in smart mining solutions, and focus on electrified and autonomous equipment deployment.

Latin America

Latin America accounted for approximately USD 0.67 billion in 2025. The market is primarily driven by extensive mining activities across the region, particularly in copper and iron ore, along with the increasing adoption of automation technologies to enhance productivity and optimize operational costs. Chile, Brazil, and Peru are experiencing strong demand, supported by expanding mining operations and rising investments in digital and autonomous mining solutions.

Chile Autonomous Mining Equipment

The Chile market was valued at around USD 0.23 billion in 2025. The growth is supported by large-scale copper mining operations, rising deployment of autonomous haul trucks, and the strong presence of global mining companies focused on improving efficiency and safety.

Middle East & Africa

The Middle East & Africa accounted for approximately USD 0.42 billion in 2025. The market is witnessing steady growth due to expanding mining activities, increasing emphasis on automation to improve safety, and rising investments in mining infrastructure across both Africa and the Middle East. The gradual adoption of autonomous equipment is helping mining companies enhance productivity and minimize operational risks.

South Africa Autonomous Mining Equipment

The South African market was valued at around USD 0.17 billion in 2025. The growth is driven by extensive underground mining operations and the increasing adoption of autonomous loaders and drilling equipment aimed at improving safety and operational efficiency.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Companies are Advancing Autonomous Technologies and Digital Platforms to Enhance Mining Efficiency

The autonomous mining equipment market is moderately consolidated, characterized by the presence of established heavy equipment OEMs, mining automation specialists, and digital mine technology providers. Leading participants such as Caterpillar, Komatsu, Sandvik, Epiroc, Liebherr, Hitachi Construction Machinery, Volvo Construction Equipment, Hexagon, and ABB maintain strong positions through portfolios spanning autonomous haulage systems, automated drilling, autonomous loaders, remote operation platforms, fleet management software, collision avoidance, and electrified mining equipment.

In April 2025, the Epiroc secured its largest-ever contract to supply fully autonomous and electric surface mining equipment to Fortescue in Australia, highlighting the growing convergence of automation and zero-emission mining fleets. Komatsu reached a major milestone in 2026 by commissioning its 1,000th autonomous ultra-class haul truck equipped with FrontRunner AHS, reinforcing the commercial scale of autonomous haulage adoption. Caterpillar also continued expanding its MineStar Command ecosystem, with industry coverage noting its ambition to grow autonomous truck deployment significantly by 2030.

LIST OF AUTONOMOUS MINING EQUIPMENT COMPANIES PROFILED IN REPORT

- Caterpillar Inc. (U.S.)

- Komatsu Ltd. (Japan)

- Sandvik AB (Sweden)

- Epiroc AB (Sweden)

- Liebherr Group (Switzerland)

- Hitachi Construction Machinery Co. Ltd (Japan)

- Volvo Construction Equipment (Sweden)

- Hexagon AB (Sweden)

- ABB Ltd. (Switzerland)

- ASI Mining (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Komatsu commissioned its 1,000th autonomous ultra-class haul truck equipped with the FrontRunner Autonomous Haulage System, strengthening its position as one of the leading global providers of autonomous haulage solutions.

- May 2026: Hexagon expanded its autonomous mining solutions portfolio by enhancing its fleet management and collision avoidance systems, enabling real-time data integration and improved operational safety across large-scale mining sites.

- November 2025: Sandvik enhanced its AutoMine platform with new AI-driven features, enabling improved fleet coordination, real-time decision-making, and higher levels of autonomy in underground mining operations.

- September 2025: Liebherr advanced its autonomous and battery-electric mining truck development, emphasizing integration of automation with zero-emission technologies to support sustainable and efficient mining operations.

- April 2025: Epiroc won its largest-ever contract to deliver a major fleet of fully autonomous and electric surface mining equipment to Fortescue in Australia, reflecting rising demand for integrated automation and electrification in large-scale mining operations.

REPORT COVERAGE

The global autonomous mining equipment market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.27% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Equipment Type, By Mining Type, By Autonomy, By Propulsion Type, By Application, and By Region |

| By Equipment Type |

|

| By Mining Type |

|

| By Autonomy |

|

| By Propulsion Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.24 billion in 2025 and is projected to reach USD 11.06 billion by 2034.

The market is expected to exhibit a CAGR of 11.27% during the forecast period (2026-2034).

The surface mining segment led the market in terms of mining type.

Rising focus on worker safety and operational efficiency is driving market growth.

Caterpillar Inc., Epiroc AB, Sandvik AB, and Komatsu Ltd. are the top players in the market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 197

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us