Ballistic Protection Market Size, Share & Industry Analysis by Product Category (Personal Armor, Vehicle Armor, Aircraft Armor, Naval/Marine Armor, and Infrastructure & Fixed-Site Protection), By Material (Aramid Fibers, Ultra-High-Molecular-Weight Polyethylene, Ceramics, Composites, Metal Alloys, & Others), By Product Type (Soft Armor, Hard Armor, Helmets, Vehicle Armor Modules, Glass & Transparent Armor, & Others), By Threat Level (Low-Velocity/Handgun Protection, Intermediate Rifle Threat, & High-Caliber Rifle/AP Threat), By Procurement Mode, By End User, and Regional Forecast, 2025-2032

Ballistic Protection Market Size

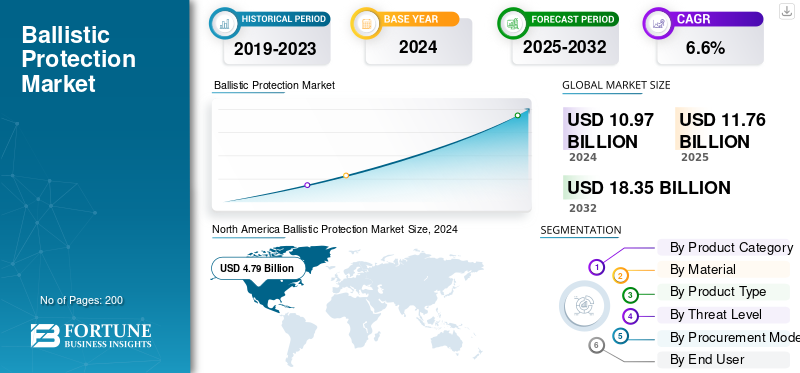

The global ballistic protection market size was valued at USD 10.97 billion in 2024. The market is projected to grow from USD 11.76 billion in 2025 to USD 18.35 billion by 2032, exhibiting a CAGR of 6.6% during the forecast period. North America dominated the ballistic protection market with a market share of 44.39% in 2024.

Ballistic protection refers to items designed to keep people and platforms safe from bullets and shrapnel. This includes vests and plates, helmets, shields, armored vehicles panels, bullet-resistant glass, and fortified rooms or facilities. These items are tested to specific standards, such as NIJ or STANAG, and can be purchased as new gear or as upgrades and replacements over time. Armed forces and police are continually updating their gear. Rising security threats are pushing buyers toward rifle and armor-piercing protection, driving the market growth.

Major players in the market include Point Blank Enterprises, Safariland, Armor Express, Galvion, Avon Protection, NP Aerospace, Rheinmetall, BAE Systems, Thales, KNDS (KMW/Nexter), Plasan Sasa, Elbit Systems, Rafael, Hanwha Defense, Hyundai Rotem, Isoclima, AGP, and upstream materials leaders DuPont (Kevlar), Teijin (Twaron), Avient/Dyneema, Honeywell (Spectra), CeramTec, CoorsTek, and Morgan Advanced Materials. They are increasing capacity, partnering for local production, bundling upgrades and support, and delivering lighter, stronger protection to the field more quickly to enhance their market share.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Tougher Ballistic Standards and Lighter Materials to Drive the Market Growth

A major factor driving industry expansion is the combination of stricter certification standards and new lightweight materials. This change forces replacement cycles and allows buyers to upgrade to better protection without increasing weight. The NIJ 0101.07 update strengthens test methods, including those for women’s armor. It drives new certifications and encourages agencies to phase out older 0101.06 models. At the same time, next-generation ultra-high molecular weight polyethylene (UHMWPE) and aramid materials, such as Dyneema’s new hard-ballistic UDs and DuPont’s Kevlar EXO, reduce weight while enhancing multi-hit performance. This leads to new purchases and higher average selling prices across soft armor, plates, helmets, and even vehicle and transparent armor integration.

- For instance, in November 2023, the U.S. NIJ published Standard 0101.07 and 0123.00, along with a transition plan away from 0101.06. Testing and certification under 0101.07 began in 2024. Agencies were told to expect 0101.07-certified armor from late 2024 to early 2025.

MARKET RESTRAINTS

Certification Burden (NIJ/STANAG/VPAM) Increases Cost and Time-to-Market Hindering Market Growth

Keeping up with changing ballistic standards forces manufacturers to redesign, re-tool, and re-certify products for different sizes and threat levels, especially for rifle and armor-piercing protection. Each new version requires lot testing for ballistic performance, fragmentation, and backface deformation, along with time from third-party labs and audits of documentation. Even small design changes, such as a new fabric lot, adhesive, or geometry, can lead to re-tests. This often stretches lead times by months and ties up cash in inventory that cannot be shipped. For agencies, this increases unit prices and delays deployment. For vendors, it reduces profit margins and takes away engineering resources that could be used for new products or expanding capacity.

MARKET OPPORTUNITIES:

Infrastructure and Critical-Site Hardening is a Lasting Growth Area Creating New Revenue Streams

Beyond frontline gear, governments and operators are upgrading embassies, bases, power and water plants, data centers, airports, and border posts with materials that better resist bullets and fragments. This includes doors, walls, guard booths, and clear armor. These programs involve significant funding, often coming from sources outside the main defense budgets. They follow predictable refresh cycles of about 7 to 12 years. This process includes using opaque panels, spall liners, glazing, and combined blast and ballistic packages, which leads to ongoing, reliable revenue.

- For instance, in February 2023, CISA and the Department of Energy published a Sector Spotlight on Electricity Substation Physical Security. It encourages layered ballistic barrier solutions and other physical upgrades, driving spend on opaque panels, spall liners, and protective enclosures at utilities.

MARKET CHALLENGES:

Compliance Upgrades to NIJ 0101.07 / 0123.00 to Lengthening Timelines and Raise Costs

Moving from legacy NIJ 0101.06 to 0101.07 with 0123.00 test security threats forces redesigns, re-tooling, and full requalification across sizes and variants. This is especially true for rifle/AP plates and multi-hit configurations. Each change in materials loT, adhesive, or geometry can trigger new lab runs, documentation, and audit cycles. This process ties up capital in inventory that cannot ship. Certifications by model and size multiply the test matrix for soft armor, while changes in transparent armor often require repeat optical or spall validation. Suppliers need to reserve limited ballistic-lab time and follow updated ASTM-referenced methods, which can add months to the timeline. The outcome is higher non-recurring engineering costs, longer lead times, and slower SKU availability for agencies, even when budgets are set.

BALLISTIC PROTECTION MARKET TRENDS:

Shift to Rifle/AP Protection Fueled by Lighter Materials and Stricter Standards

Agencies and militaries are transitioning from handgun-rated gear to rifle and armor-piercing protection in plates, helmets, vehicles, and transparent armor. Lightweight ceramic and ultra-high molecular weight polyethylene (UHMWPE) hybrids now provide higher stop levels without the previous weight penalty. This improvement increases actual wear time and allows more people to carry rifle-rated protection. Updates to standards, such as NIJ 0101.07, are tightening test protocols and speeding up re-certifications. This trend is leading to the retirement of older models and the introduction of next-generation kits, impelling ballistic protection market growth over the coming years.

- For example, in January 2025, Dyneema (Avient) launched the HB330 and HB332 hard-ballistic UDs, claiming about a 45% weight reduction in armor systems. This change allows for higher protection with less burden.

Russia Ukraine War Impact

Russia-Ukraine War Increased Demand, Changed Procurement Processes, and Put Pressure on Supply Chains for Global Ballistic Protective

The conflict created a steady increasing demand for plates, helmets, spall liners, and transparent armor as European and NATO budgets increased. Programs moved from pilot phases to large-scale purchases. Ukraine adopted centralized logistics and sourced more locally for vests and helmets. Meanwhile, allies replenished stocks and raised readiness levels, which boosted orders and the need for aftermarket supplies such as glass and liners. On the industry front, sanctions and export controls changed supplier lists and increased compliance tasks, even as Europe worked to boost defense production capacity. The war also accelerated the use of higher threat ratings and lighter ceramic-UHMWPE stacks, while emphasizing the need for hardening against drones and fragments. Overall, this led to faster procurement processes in Europe and nearby areas, along with tighter management of material risks and certification.

- In June 2024, NATO data showed many allies reaching or exceeding the 2% of GDP goal, which supported larger equipment purchases and stock replenishments.

- In August 2024, Ukraine's Ministry of Defense reported that over 80% of materiel contracts were awarded to domestic producers after establishing a new State Logistics Operator. This indicated a shift toward local sourcing for vests, helmets, and related gear.

Since 2022, U.S. and EU sanctions and export controls have targeted Russia’s military-industrial base. These actions changed cross-border sourcing and compliance needs for dual-use materials.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Category

Personal Armor Dominated the Market in 2024 Due to Rising Demand for Lightweight and Modular Soldier Protection Systems

In terms of product category, the market is categorized into personal armor, vehicle armor, aircraft armor, naval / marine armor, and infrastructure & fixed-site protection.

The personal armor segment held the largest share in the global ballistic protective market in 2024. This is due to the ongoing increasing demand from military and law enforcement agencies for lightweight, ergonomic, and modular protection systems. The increase in asymmetric warfare, urban combat, and homeland security efforts has led to more investments in body armor, helmets and shields. Soldier modernization programs in countries such as the U.S., U.K., India, and Israel have further strengthened this segment's position. Improvements in aramid fibers, ultra-high molecular weight polyethylene (UHMWPE), and ceramic composites have increased protection while lowering weight. This makes personal armor essential in both defense and security applications.

- For instance, in March 2024, Point Blank Enterprises won a USD 215 million contract from the U.S. Army. They will supply next-generation modular body armor systems aimed at improving comfort and mobility for soldiers in the field.

The infrastructure & fixed-site protection segment is expected to grow at the fastest CAGR of 7.4% over the forecast period.

By Material

Aramid Fibers Lead the Market Due to their Proven Strength-to-Weight Ratio and Wide Use in Defense

On the basis of market segmentation by material, the market is classified into aramid fibers, ultra-high-molecular-weight polyethylene, ceramics, composites, metal alloys, and others.

The aramid fibers segment holds the largest share in the ballistic protection market. This is due to their high tensile strength, heat resistance, and lightweight properties, which make them perfect for helmets, bulletproof vests, and vehicle armor panels. Aramid fibers such as Kevlar and Twaron are widely used by defense forces around the world. Their reliability and consistent performance in real combat situations make them a trusted choice. Additionally, these fibers work well with composite layering techniques, allowing manufacturers to create flexible yet strong ballistic solutions. Ongoing innovations from top material science companies have led to new variants of aramid fibers that offer better durability and ballistic performance, further securing this segment’s leadership in the market.

- For example, in February 2024, DuPont de Nemours, Inc. announced the launch of its Kevlar EXO aramid series. This new series provides better flexibility and protection for advanced body armor, helmets and shields, representing a significant step forward in soldier survivability solutions.

To know how our report can help streamline your business, Speak to Analyst

By Product Type

Soft Armor Segment Leads the Market Due to High Use in Military and Law Enforcement Body Protection Programs

Based on product type, the market is segmented into soft armor, hard armor, helmets, vehicle armor modules, glass & transparent armor, and others.

The soft armor segment is at the forefront of the market due to its lightweight design, mobility, and extensive adoption by defense and law enforcement personnel. Soft armor is favored for its flexibility and comfort, making it ideal for long periods of wear during urban operations, riot control, and patrol duties. The growing number of modernization programs, especially in the U.S., Europe, and Asia Pacific, has increased the demand for modular soft armor systems made with aramid fibers and UHMWPE materials.

- For example, in April 2024, the U.S. Department of Defense awarded a USD 190 million contract to Safariland, LLC for next-generation soft body armor vests. These are made to offer better flexibility and protection for military and law enforcement forces.

The hard armor segment is expected to grow at a CAGR of 7.7% over the forecast period.

By Threat Level

Low-Velocity / Handgun Protection Leads the Market Due to High Adoption by Law Enforcement and Civilian Security Forces

Based on threat level, the market is segmented into low-velocity/handgun protection, intermediate rifle threat, and high-caliber rifle/AP threat.

The low-velocity/handgun protection segment leads the market, mainly due to its wide use among police, homeland security, and private security personnel. Unlike heavy rifle-rated armor, handgun protection systems are lightweight, affordable, and comfortable for everyday wear, making them the preferred option for law enforcement and non-military users around the world. The ongoing rise in urban crime rates, the need for riot control, and the increasing demand for VIP protection have further increased the purchase of NIJ Level II and IIIA-rated vests. Additionally, the growth of civilian defense equipment markets in areas such as North America and Europe strengthens the dominance of this category, as these users typically face low-velocity ballistic security threats.

The high-caliber rifle / AP threat segment is set to flourish with a growth rate of 7.6% during the forecast period.

By Procurement Mode

Direct/OEM Procurement Segment Dominates the Market Due to Large-Scale Defense Modernization and Standardized Supply Contracts

Based on procurement mode, the market is segmented into direct/OEM, licensed local production, and retrofit & aftermarket.

The direct/OEM segment leads the market. Governments prefer direct contracts with original equipment manufacturers (OEMs) to ensure quality, timely delivery, and compliance with defense standards. Major militaries in North America, Europe, and Asia Pacific buy ballistic protection systems such as vests, helmets, and vehicle armor, directly from OEMs. This practice supports ongoing soldier modernization and vehicle upgrade programs. It also reduces logistical challenges and allows for quicker use of materials such as aramid fibers and UHMWPE composites. Additionally, OEM procurement offers customization and flexibility, which are crucial for large defense forces needing standard ballistic protection across various platforms.

The retrofit and aftermarket segment is set to flourish with a growth rate of 8.8% during the forecast period.

By End User

Military End User Dominates the Market Due to Rising Soldier Modernization and Cross-Border Security Programs

In terms of end user, the market is segmented into military, homeland & law enforcement, government & critical infrastructure, and civilian.

The military segment is the largest end user in the market. This is driven by increased global defense modernization efforts, increased defense spending, and the need for better survivability in modern warfare. Military forces in the U.S., Europe, China, India, and Russia are focusing on integrating advanced armor systems, including modular body armor, ballistic helmets, vehicle armor kits, and blast-resistant materials. These systems aim to protect troops from new battlefield threats. The use of lightweight composite and ceramic technologies has also improved mobility and comfort while maintaining protection. Rising geopolitical tensions, such as the Russia-Ukraine conflict and territorial disputes in the Indo-Pacific, have increased procurement activities and research and development investments in this area.

- For instance, in January 2024, the U.S. Department of Defense awarded Ceradyne, Inc., a subsidiary of 3M, a USD 168 million contract. This contract is aimed at supplying advanced ballistic helmets and armor plates for U.S. Army personnel under the Soldier Protection System program. The goal is to improve combat survivability and mission readiness.

The government & critical infrastructure segment is set to grow at a CAGR of 7.6% over the forecast period.

Ballistic Protection Market Regional Outlook

North America Dominates Due to Rapid Defense Modernization and Indigenous Development Initiatives

By geography, the market is categorized into Europe, North America, Asia Pacific, and rest of the world (Middle East & Africa and Latin America).

North America Ballistic Protection Market Size, 2024 ( USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The North America dominated the global ballistic protection market share in 2023, valuing at USD 4.36 billion, and also bagged the leading share in 2024 with USD 4.79 billion. This region's leadership comes from ongoing investments in soldier modernization programs, the use of lightweight materials, and a strong presence of major manufacturers such as BAE Systems, 3M Ceradyne, Point Blank Enterprises, and Avon Protection. Additionally, government programs such as the U.S. Army’s Integrated Visual Augmentation System (IVAS) and the Enhanced Small Arms Protective Insert (ESAPI) continue to boost the large-scale purchases of personal and vehicle armor.

Asia Pacific, Europe, and the Middle East

Other regions such as Asia Pacific, Europe, and Middle East are expected to see significant growth in the global market in the coming years. During the forecast period, the Asia Pacific region is projected to depict a growth rate of 6.8%, which is the second fastest among all regions. In the region, countries including China, India, South Korea, and Japan are expanding their domestic armor production to support military self-reliance. Based on these factors, countries such as China and India are expected to have reached a valuation of USD 0.96 billion and USD 0.48 billion respectively by 2025.

Europe

The market in Europe is estimated to be USD 3.22 billion in 2025, making it the second-largest region in the market. In this region, the U.K. and France are expected to reach USD 0.58 billion and USD 0.50 billion, respectively, in 2025. Countries such as Germany, the U.K., and France continue to focus on developing lightweight and sustainable ballistic materials.

Rest of the World

In the rest of world, the Middle East and Africa is witnessing a rising demand for vehicle and infrastructure armor due to geopolitical instability and regional conflicts. At the same time, Latin America is slowly adopting ballistic protection systems for law enforcement and anti-narcotics efforts, with Brazil and Mexico taking the lead. Overall, these regions are expected to experience steady growth owing to local production, modernization of security, and partnerships in defense.

COMPETITIVE LANDSCAPE

Key Industry Players:

Global Defense Giants Dominate the Market through Innovation, Large Contracts, and Advanced Material Integration

The ballistic protection market is dominated by major defense companies such as BAE Systems, 3M Ceradyne, Avon Protection, Point Blank Enterprises, and Safariland. These firms lead with significant defense contracts, strong investments in research and development, and innovations in materials. They focus on creating lightweight, high-strength armor systems made from aramid fibers, ceramics, and UHMWPE composites. Collaborating with agencies such as the U.S. Department of Defense and NATO helps strengthen their market position and ensures steady revenue.

Emerging companies such as MKU Limited (India), Hard Shell (UAE), TenCate Advanced Armor (Netherlands), and Rheinmetall AG (Germany) are gaining traction by offering localized production and affordable armor solutions. Supported by defense industrialization programs in Asia Pacific and the Middle East, these regional manufacturers are improving their competitiveness through technology transfer, partnerships, and adaptable product designs. This contributes to a more diverse global market.

LIST OF KEY BALLISTIC PROTECTION COMPANIES PROFILED:

- BAE Systems plc. (U.K.)

- Avon Protection plc. (U.K.)

- Point Blank Enterprises, Inc. (U.S.)

- Safariland, LLC (U.S.)

- 3M Ceradyne, Inc. (U.S.)

- Rheinmetall AG (Germany)

- TenCate Advanced Armor (Netherlands / Denmark)

- MKU Limited (India)

- Hard Shell FZE (UAE)

- ArmorSource LLC (U.S.)

- S. Armor Corporation (U.S.)

- Mehler Vario System GmbH (Germany)

- NP Aerospace Ltd (U.K.)

- Verseidag-Indutex GmbH (Germany)

- Survitec Group Limited (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- In July 2025, Safe Pro Group Inc. (U.S.) secured a contract from a U.S. government contractor to deliver ballistic protection and EOD equipment for operations in the Indo-Asia Pacific region, with deliveries expected in Q3 2025.

- In February 2024, the U.S. Army Contracting Command awarded Avon Protection plc a USD 204 million Direct OEM contract to deliver next-generation body armor and combat helmets for the Integrated Head Protection System (IHPS) program. This contract ensures efficient production and deployment.

- In July 2023, Avon Protection received its second delivery order worth USD 38 million from the U.S. Army under the NG-IHPS helmet contract (W91CRB-21-D-0022).

- In September 2020, Avon Protection was awarded a sole-source contract valued up to USD 93 million to develop and supply the U.S. Army with the Next-Generation Integrated Head Protection System (IHPS).

REPORT COVERAGE

The global market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on strategic partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ARRTIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 6.6% from 2025 to 2032 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product Category

|

|

By Material

|

|

|

By Product Type

|

|

|

By Threat Level

|

|

|

By Procurement Mode

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 10.97 billion in 2024 and is projected to reach USD 18.35 billion by 2032.

In 2024, the North America market value stood at USD 4.79 billion.

The market is expected to exhibit a CAGR of 6.6% during the forecast period of 2025-2032.

In 2024, the personal armor segment led the market by product category.

Tougher ballistic standards and lighter materials are triggering mandatory upgrade cycles and raising average selling prices across personal, vehicle, and transparent armor, driving the market growth.

BAE Systems, Avon Protection, Point Blank Enterprises, Safariland, 3M Ceradyne, Rheinmetall AG, TenCate Advanced Armor, and MKU Limited are the top companies in the market, driving global leadership through advanced material innovation, large-scale defense contracts, and continuous modernization of personal and vehicle armor systems.

North America dominated the market in 2024.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us