Bio-Based Polyethylene Furanoate Market Size, Share & Industry Analysis, By Application (Packaging, Films, Fibers, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

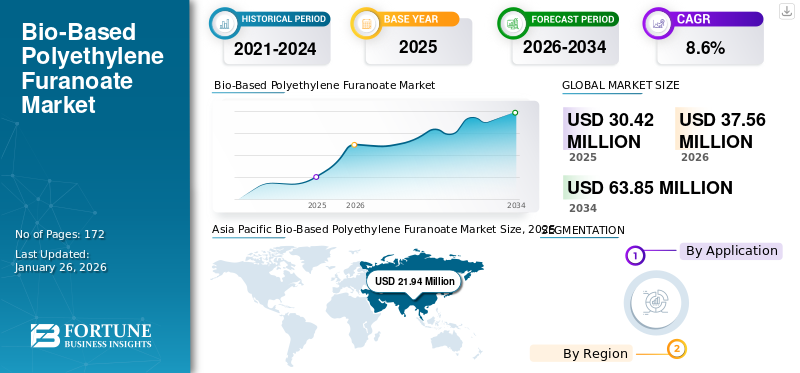

The global bio-based polyethylene furanoate market size was valued at USD 30.42 million in 2025 and is projected to grow from USD 37.56 million in 2026 to USD 63.85 million by 2034, exhibiting a CAGR of 8.6% during the forecast period. Asia Pacific dominated the bio-based polyethylene furanoate market with a market share of 72% in 2025.

Bio-Based Polyethylene Furanoate (PEF) is a fully renewable and biodegradable polymer derived from biological resources. PEF is considered as a sustainable alternative to conventional Polyethylene Terephthalate (PET), offering similar properties but with a lower environmental impact due to its renewable origins and biodegradability. PEF demonstrates advantages such as improved barrier properties, higher thermal stability, and a smaller carbon footprint, making it an attractive material for packaging and various applications in the plastics industry.

Demand for bio-based polyethylene furanoate is increasing as consumers and industries seek more sustainable alternatives to traditional plastics. This bio-based material, derived from renewable resources, offers properties similar to conventional polyethylene's properties while significantly reducing environmental impact. As awareness of ecological issues grows, the market for bio-based materials is expected to expand further, driven by innovation and regulatory policies promoting sustainability.

The major companies operating in the market include Swicofil AG, Sulzer Ltd, Avantium, and AVA Biochem AG.

Download Free sample to learn more about this report.

Bio-Based Polyethylene Furanoate Market Key Takeaways

- 2025 Market Size: USD 30.42 million

- 2026 Market Size: USD 37.56 million

- 2034 Forecast Market Size: USD 63.85 million

- CAGR: 8.6% from 2026–2034

- Asia Pacific dominated the bio-based polyethylene furanoate market with a market share of 72% in 2025.

- Packaging is the largest application segment, contributing the largest bio-based polyethylene furanoate market share in 2024.

- The fibers segment also contributes to positive growth.

Asia Pacific

Asia Pacific contributed 72.00% to the global market in 2025, with a valuation of USD 21.94 million, and is projected to reach USD 27.08 million in 2026. Asia Pacific leads the global market in terms of share and projected growth rate.

North America

The market was valued at USD 3.50 million in 2025 and is expected to reach USD 4.32 million in 2026, driven by strong environmental regulations and growing adoption of bio-based plastics.

Europe

The regional market stood at USD 3.08 million in 2025 and is forecast to reach USD 3.80 million in 2026, supported by stringent sustainability policies and advancements in biopolymer technologies.

U.S.

The U.S. market is experiencing strong growth due to increasing sustainability initiatives and rising preference for high-performance bio-based alternatives to conventional plastics.

Japan

Japan is expected to witness steady market growth, supported by increasing focus on sustainable packaging, advanced materials innovation, and circular economy initiatives.

Read More

BIO-BASED POLYETHYLENE FURANOATE MARKET TRENDS

Regulatory Support and Consumer Awareness Drives Market Growth

Governments are implementing policies and regulations to promote bio-based materials, including restrictions on single-use plastics and Extended Producer Responsibility (EPR) programs. Increasing consumer awareness about environmental issues and sustainable practices drives demand for PEF and other bio-based alternatives. In addition, efforts to educate consumers about the benefits of PEF are also contributing to its growing adoption.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Sustainable Packaging Solutions Drives Global Market

The increasing demand for sustainable packaging solutions drives the bio-based polyethylene furanoate market growth. As businesses and consumers alike seek environmentally friendly alternatives to traditional plastics, the bio-based nature of PEF positions it as an attractive option. Manufacturers of PEF capitalize on this driver by offering products that reduce carbon footprints and maintain high performance and versatility in packaging applications. The shift toward sustainability is reshaping the landscape of the material industry, with PEF emerging as a key player in meeting eco-conscious consumer preferences.

MARKET RESTRAINTS

High Production Costs May Restrain Market Growth

PEF is primarily derived from renewable sources such as fructose, which are generally more expensive than the petroleum-based feedstocks used in traditional plastics. The agricultural sector's variability, influenced by weather conditions and land use factors, can also lead to supply chain vulnerabilities and further increase costs.

Similarly, the availability of bio-based raw materials is more limited compared to conventional plastic feedstocks. This scarcity can create supply chain issues and contribute to higher production costs.

MARKET OPPORTUNITIES

Rising Investments in Bio-Based Polymers and Green Technologies Drive Market Growth

There is a significant increase in investor interest in bio-based polymers, particularly in developing alternatives to single-use plastics. This investment supports the large-scale production of PEF and helps lower its cost.

Similarly, ongoing R&D efforts focus on optimizing PEF production processes, reducing costs, and enhancing performance characteristics. This includes advancements in fermentation processes and catalytic methods. Such new technology creates an opportunity in the bio-based polyethylene furanoate market.

MARKET CHALLENGES

Competition from Other Bio-plastics Challenging Market Growth

Competition from other bio-plastics such as PLA, PHA, and bio-PET can pose challenges to the bio-based polyethylene furanoate market due to limited availability and high production costs.

PEF is still in its early stages of adoption and requires more manufacturing investments to increase its commercial availability. Also, the range of bioplastics available for large-scale manufacturing is narrower than that of conventional plastics.

TRADE PROTECTIONISM

The imposition of tariffs on bio-based chemical imports, including key PEF feedstock such as furandicarboxylic acid (FDCA), has raised production costs. This is particularly challenging for manufacturers that rely on European or Asian suppliers for bio-based intermediates.

The U.S. has accelerated its focus on domestic PEF production to reduce import dependency. However, challenges remain in scaling up fermentation capacity and achieving competitive pricing without subsidies or long-term offtake agreements.

Segmentation Analysis

By Application

Packaging is the Leading Application

Owing to Suitable Product Properties

Based on application, the market is classified into packaging, films, fibers, and others.

Packaging is the largest application segment, contributing the largest bio-based polyethylene furanoate market share in 2024. PEF offers excellent barrier properties, making it suitable for food and beverage packaging. Its high performance and recyclability make it an attractive alternative to traditional plastics such as PET. The demand for bio-based polyethylene furanoate in packaging is expected to grow significantly, driven by consumer preference for eco-friendly alternatives and regulatory requirements to reduce plastic waste.

The fibers segment also contributes to positive growth. PEF fibers offer sustainability and performance advantages in clothing, textiles, and industrial applications. The textile industry is increasingly exploring PEF to create biodegradable fibers, reflecting a growing trend toward eco-conscious fashion.

The films segment registered a notable growth. The superior barrier properties of PEF make it ideal for applications where oxygen and moisture resistance are critical.

Bio-Based Polyethylene Furanoate Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Bio-Based Polyethylene Furanoate Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 72.00% to the global market in 2025, with a valuation of USD 21.94 million, and is projected to reach USD 27.08 million in 2026. Asia Pacific leads the global market in terms of share and projected growth rate. Asia Pacific dominated the market with a valuation of USD 21.94 billion in 2025 and USD 27.08 billion in 2026. This dominance is fueled by rapid industrialization, growing demand for sustainable alternatives, and increasing consumer awareness of environmental issues. The region also observes significant investment in research, development, and production capacity.

North America

In 2025, North America represented USD 3.5 million, accounting for 12.00% of the worldwide market, and is projected to grow to USD 4.32 million in 2026. North America is a mature market with steady demand. Enhanced environmental regulations and a high consumer consciousness drive the demand for bio-based polyethylene furanoate. The region benefits from a well-established bio-based sector and significant government initiatives. The U.S. market is experiencing dominant growth, driven by increasing sustainability concerns and the superior properties of PEF compared to traditional plastics.

Europe

The Europe market generated USD 3.08 million in 2025, representing 10.00% of the global market landscape, and is expected to reach USD 3.8 million in 2026. Europe registers significant growth due to strong environmental policies and high consumer awareness of sustainability issues. The region is also a leader in technological advancements in biopolymer production and processing.

Latin America

The region benefits from abundant agricultural resources, providing a strong bio-based production base. Increasing demand for sustainable packaging and consumer products is also driving market growth. The market in Latin America reached USD 1.06 million in 2025, representing 3.50% of total market revenue, and is projected to reach USD 1.31 million in 2026.

Middle East & Africa

The Middle East & Africa market was valued at USD 0.85 million in 2025, capturing 3.00% of global revenue, and is estimated to reach USD 1.05 million in 2026. Increasing environmental regulations and a growing focus on sustainable development drive market growth. The region is also witnessing increasing investment in bio-based technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Constant Expansion and Launch of Novel Products by Notable Companies Led to Their Leading Positions in Market

The bio-based polyethylene furanoate market is greatly competitive, with key players concentrating on mergers & acquisitions, sustainability, and capacity expansion to fortify their market presence. Key global companies include Swicofil AG, Sulzer Ltd, Avantium, AVA Biochem AG, among others. While global leaders lead in developed markets, regional players are growing aggressively in developing economies, strengthening competition in the industry.

LIST OF KEY BIO-BASED POLYETHYLENE FURANOATE COMPANIES PROFILED

- Swicofil AG (Switzerland)

- Sulzer Ltd (Switzerland)

- TOYOBO CO., LTD. (Japan)

- Avantium (Netherlands)

- ALPLA (Austria)

- Origin Materials (U.S.)

- AVA Biochem AG (Switzerland)

- Stora Enso (Finland)

- Terphane (U.S.)

- Tereos (France)

KEY INDUSTRY DEVELOPMENTS

- November 2024: Avantium N.V. partnered with Kirin Holdings to explore using the company's plant-derived and recyclable material, PEF, for Kirin’s packaging and bottles across its product range.

- November 2023: Avantium N.V. entered into a strategic partnership with PANGAIA, whereby PANGAIA will acquire Avantium’s PEF to incorporate into their clothing line, aiming to produce materials and products that are recyclable and free from fossil fuels.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.6% from 2026-2034 |

|

Unit |

Value (USD Million) and Volume (Kiloton) |

|

Segmentation |

By Application

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 30.42 million in 2025 and is projected to reach USD 63.85 million by 2034.

In 2025, the market value stood at USD 21.94 million.

The market is expected to exhibit a CAGR of 8.6% during the forecast period of 2026-2034.

The packaging segment led the market by application.

Increasing demand for sustainable packaging solutions to boost market expansion.

Avantium, AVA Biochem AG, Swicofil AG, Sulzer Ltd, and TOYOBO CO., LTD. are some of the leading players in the market.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 172

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us