Biomass Logistics Service Market Size, Share & Industry Analysis, By Service Type (Transportation, Collection & Aggregation, Storage & Handling, Pre-processing / Conditioning, and Others), By Feedstock Type (Agricultural Residues, Forestry Residues, Energy Crops, Urban Biomass Waste, and Others), By End User (Bioenergy Producers, Biofuel Manufacturers, Power & Utility Plants, Pulp & Paper Industry, and Others) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

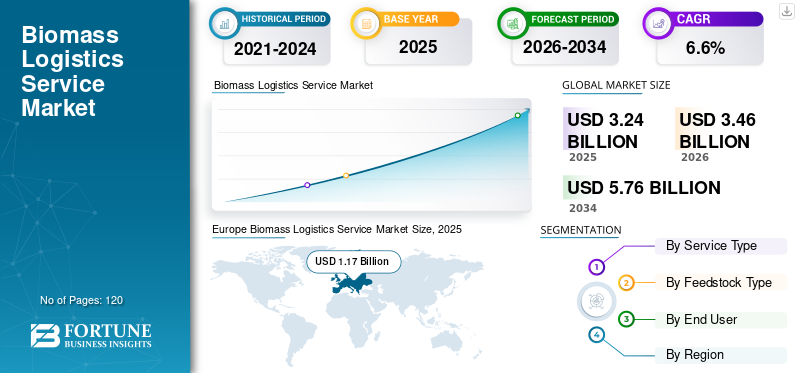

The global biomass logistics service market size was valued at USD 3.24 billion in 2025. The market is projected to grow from USD 3.46 billion in 2026 to USD 5.76 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period. Europe dominated the global biomass logistics service market with a market share of 36.11% in 2025.

The biomass logistics service industry is experiencing steady growth as renewable energy expansion accelerates worldwide and industries transition toward reducing carbon feedstocks. Efficient biomass logistics that comprise collection, aggregation, preprocessing, storage, handling, and transportation are becoming crucial in order to supply biomass to power plants, biofuel facilities, and industrial energy consumers. The increasing demand for sustainable and traceable biomass supply chains, coupled with policy support for decarbonization and circular economy initiatives, continues to strengthen the biomass logistics service market.

- In 2025, Europe’s renewable energy share in final energy consumption reached 24.5%, with biomass remaining a major contributor to both heating and power, reinforcing the importance of robust logistics networks to support the growing supply requirements.

Leading industry players, such as ENGIE, Vattenfall, Drax, and several specialized logistics integrators, are focusing on digitalization, multimodal transport networks, along sustainability-compliant tracking systems. These companies are also enhancing feedstock flow efficiency through real-time monitoring, automated handling systems, and traceability frameworks to meet tightening regulatory and certification standards.

- In 2025, SAEL Industries (India) signed an MoU with the state of Andhra Pradesh to develop 200 MW of biomass-based power capacity, creating substantial demand for agricultural-residue collection, storage, and long-haul transportation services to support continuous feedstock availability.

Download Free sample to learn more about this report.

Biomass Logistics Service Market Key Takeaways

- 2025 Market Size: USD 3.24 billion

- 2026 Market Size: USD 3.46 billion

- 2034 Forecast Market Size: USD 5.76 billion

- CAGR: 6.6% from 2026-2034

- Europe dominated the biomass logistics service market with a 36.11% share in 2025.

- The pre-processing/conditioning segment is projected to grow at a CAGR of 8.1% during the forecast period.

- The urban biomass waste segment is expected to register a CAGR of 7.4% during the forecast period.

North America

North America is projected to reach USD 0.92 billion in 2026, supported by abundant forest resources and a strong pellet export sector.

Asia Pacific

Asia Pacific is anticipated to register the highest CAGR during the forecast period, steadily increasing its market share.

Europe

Europe is projected to reach USD 1.24 billion in 2026, maintaining its leading position in the global market.

U.S.

Strong biomass power generation and industrial heating applications continue to support market growth.

Japan

Increasing biomass energy adoption and government support for renewable energy are driving market expansion.

Read More

IMPACT OF GENERATIVE AI

Implementation of Generative AI Capabilities to Fuel the Growth of the Biomass Logistics Service

Through the application of generative AI, current practice in biomass logistics has been refined in several areas, namely planning, forecasting, and automating operations using Artificial Intelligence (AI) generated algorithms (i.e., simulations of supply scenarios, optimizing routing decisions, automating documentation, and predicting feedstock availability), thus reducing transport costs, eliminating supply interruptions, enhancing moisture management, and enhancing compliance with sustainability and certification.

Additionally, the use of generative modelling enables the creation of a digital twin for the biomass supply chain, providing enhanced access to information and facilitating better decision-making throughout the supply chain, ultimately improving efficiency and profitability for both the transport/logistics provider and biomass producer.

- In 2024, digital biomass platforms in India began integrating AI-based pricing engines and automated logistics planning tools, enhancing transparency, improving feedstock traceability, and reducing transaction bottlenecks for biomass suppliers and industrial buyers.

MARKET DYNAMICS

BIOMASS LOGISTICS SERVICE MARKET TRENDS

Integration with Digital Platforms and Traceability Systems to be a Key Trend in the Market

The market for biomass service is witnessing strong traction toward digital platforms that enable real-time resource tracking, quality verification, and automated logistics coordination. As sustainability regulations become more stringent, digital traceability systems often supported by IoT sensors, cloud platforms, and blockchain are emerging as critical tools for monitoring biomass origin, moisture content, certification status, and inventory levels. These platforms enhance supply-chain transparency, reduce operational delays, and support large-scale industrial users who require consistent, verifiable feedstock quality. The integration of automated handling systems and multimodal logistics is further improving operational efficiency and lowering overall costs.

- In 2023, the Sustainable Biomass Program (SBP) deployed a fully digital transaction-verification and volume-tracking system across more than 35 countries, enabling power producers and pellet manufacturers to maintain transparent, audit-ready biomass supply data.

MARKET DRIVERS

Rising Adoption of Renewable Energy to Propel the Market Growth

At a global level, there is a rapid shift towards renewable energy sources, and this is consequently increasing the need for biomass logistics services. Biomass is still at the forefront of energy production, industrial heating, CHP, and the making of advanced biofuels. To meet the energy-transition objectives and also to cut down the use of fossil fuels, several regions are planning to increase their biomass capacity. When the government offers cleaner energy sources in the form of incentives and mandates, the power plants and industrial users will be in need of biomass supply chains that are both reliable and economically reasonable. So, this has attracted an increasing number of professional logistics providers who will be managing the transport of high-volume and long-distance biomass, guaranteeing feedstock consistency and overcoming the challenges of seasonal fluctuations.

- In 2024, the USDA emphasized the need for resilient biomass supply chains to support the U.S. bioeconomy, highlighting expanded opportunities for farmers, forest landowners, and logistics operators as federal clean-energy initiatives accelerate.

MARKET RESTRAINTS

High Logistics Costs Hindering Biomass Logistics Market Growth

One of the main factors that limit the expansion of biomass logistics services is high logistics costs, which have remained a major barrier despite the increasing demand. Biomass itself has a low energy density, is heavy and takes up a lot of space, and in most cases, it has to undergo purification or densing before being transported, all of which add tremendously to the operational cost. Furthermore, the different seasons when it can be harvested, varying moisture content, and degradation in storage all complicate the supply planning process. On top of that, keeping up with the sustainability regulations, like EU RED II, SBP, and soon-to-come rules denying the existence of deforestation in the supply chain, necessitates the continuous expenditure on monitoring, certification, and data management. All these challenges weigh heavily on small and mid-sized suppliers, who might find it difficult to compete cost-wise while trying to comply with the very high quality and traceability standards.

- In 2025, several European pellet producers reported higher logistics and certification costs, driven by new sustainability reporting requirements under EU regulatory updates that affected biomass imports and supply-chain transparency.

MARKET OPPORTUNITIES

Expansion of Bioenergy and Advanced Biofuels to Create Lucrative Growth Opportunities

The worldwide increase in the use of bioenergy, which includes wood-based biomass, agricultural residues, and waste-derived feedstocks, is already having a positive impact on the logistics service providers' businesses. The introduction of advanced biofuels, biogas, and BECCS (Bioenergy with Carbon Capture and Storage) projects is the main reason for the very high demand for the creation of large, consistent, and traceable biomass flows; thus, the logistics services will be needed for a long time. Digital marketplaces and rural aggregation networks are also being viewed as important growth drivers, since they allow farmers and small sellers to be in direct contact with the large industrial buyers, thus leading to the reduction of supply fragmentation and the improvement of price discovery. The development of infrastructure for storage terminals, pelletization capacity, and multimodal transport hubs will further strengthen the market potential.

- In 2024, digital biomass trading platforms in Asia and Europe expanded their logistics partnerships to integrate finance, certification, and automated transport booking, resulting in stronger buyer–seller connectivity and more efficient biomass supply chains.

Segmentation Analysis

By Service Type

Strong Market Dominance of Transportation Services Fuels Expansion of the Biomass Logistics Service

Based on service type, the market is classified into transportation, collection & aggregation, storage & handling, pre-processing/conditioning, and others.

To know how our report can help streamline your business, Speak to Analyst

Transportation services dominate the biomass logistics service market due to the need to move large quantities of low-density biomass from dispersed agricultural, forestry, and municipal sources to processing and energy-generation facilities. The reliance on extensive road, rail, and, in some regions, waterway networks, coupled with the high frequency of deliveries required for continuous plant operations, drives significant logistics activity and operational spending in this segment. For instance,

- In 2024, several European biomass distributors expanded their cross-border transport fleets to meet rising pellet and feedstock demand from large-scale utility plants.

The pre-processing/conditioning segment is expected to grow at a CAGR of 8.1% over the forecast period.

By Feedstock Type

Forestry Residues Leads the Market Due to Availability of Wood Chips, and Other Forest-Derived Materials

In terms of feedstock type, the market is categorized into agricultural residues, forestry residues, energy crops, urban biomass waste, and others.

Forestry residues captured the largest biomass logistics service market share in 2025. In 2026, the segment is anticipated to dominate the market with around 2/3rd share, since the availability of wood chips, sawmill waste, bark, and other forest-derived materials continues to support large-scale, consistent biomass supply chains. Further, the expansion of pellet production, rising demand for co-firing in utility plants, and increasing use of woody biomass for heating applications and CHP systems contribute to the segment’s strong position. For instance,

- In 2024, major pellet producers in Europe and North America reported increased reliance on sustainably sourced forestry byproducts to meet rising demand from global energy markets.

The urban biomass waste segment is expected to grow at a CAGR of 7.4% over the forecast period.

By End User

Usage in Utility-Scale Heat and Power Generation Fuels Power & Utility Plants Segment’s Growth

Based on end-user segmentation, the biomass logistics service market is classified into bioenergy producers, biofuel manufacturers, power & utility plants, pulp & paper industry, and others.

The power & utility plants segment captured the largest market share in 2025. In 2026, the segment is projected to dominate as biomass continues to be widely used for utility-scale heat and power generation, particularly in co-firing applications where consistent feedstock volumes are essential. These plants depend on reliable logistics operations to ensure uninterrupted biomass supply throughout the year, further strengthening the segment’s demand for transportation, storage, handling inventory management services. For instance,

- In 2024, multiple utility companies in Europe increased their biomass procurement capacities to support decarbonization initiatives, resulting in heightened logistics activity across the supply chain.

The biofuel manufacturers segment is expected to grow at a CAGR of 8.1% over the forecast period.

Biomass Logistics Service Market Regional Outlook

By region, the biomass logistics service market is categorized into Europe, North America, Asia Pacific, South America, and Middle East & Africa.

Europe

Europe Biomass Logistics Service Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Europe holds the largest share of the biomass logistics service market in 2025, which is majorly driven by its mature bioenergy landscape, stringent sustainability regulations, along its established biomass supply chains. Extensive use of woody biomass for power generation, district heating, and industrial applications further strengthens logistics demand across the region. The market is projected to reach USD 1.24 billion by 2026, owing to its advanced infrastructure, growing pellet production, and increasing cross-border biomass trade. Key contributors include countries such as Germany (USD 0.18 billion) and the U.K. (USD 0.30 billion), which maintain strong biomass consumption tied to decarbonization policies. For instance,

- In 2024, several European utilities expanded long-term biomass procurement agreements to support co-firing initiatives, further boosting demand for integrated logistics networks across the region.

Download Free sample to learn more about this report.

North America

North America has the second-largest market share owing to its abundant forest resources, robust pellet export sector, and extensive use of biomass for power generation and industrial heating. Advanced logistics capabilities, sophisticated transportation networks, and growing investments in sustainable biomass certification and traceability are all advantageous to the region. The market is expected to reach USD 0.92 billion by 2026, with the U.S. contributing USD 0.62 billion, reflecting its significant role in pellet exports and domestic bioenergy projects across the Southeast and Midwest.

Asia Pacific

The Asia Pacific region is anticipated to attain the highest CAGR and is steadily increasing its share of the market during the forecast period. The prominent growth in this region is attributed to its increasing energy demand, progressive waste-to-energy projects, and more agricultural residues being used for power generation. Moreover, China (USD 0.32 billion) and India (USD 0.18 billion) are the countries with the highest biomass market due to the implementation of supportive policies for renewable energy, growing industrial energy needs, and the availability of vast feedstock resources. For instance,

- In 2024, multiple Asian nations expanded agricultural-residue collection and biomass co-firing programs in coal-fired plants, increasing demand for organized logistics and pre-processing services.

Middle East & Africa

The Middle East & Africa region is anticipated to experience gradual growth and attain USD 0.24 billion by 2026 as a result of increased interest in waste-to-energy solutions, governmental sustainability programs, and expanding use of biomass in industrial heating. The forecast for the GCC countries is USD 0.14 billion, backed by diversification policies and the establishment of renewable energy projects in the area.

- According to regional energy reports, several Middle East & African countries launched large-scale organic waste management initiatives in 2023, contributing to higher demand for biomass collection and transport services.

South America

Meanwhile, South America is projected to reach USD 0.14 billion by 2026, driven by abundant forestry resources, expanding sugarcane and agricultural-residue utilization, and increasing investments in bioenergy and pellet manufacturing. Growing adoption of biomass in industrial sectors across Brazil and Chile continues to support biomass logistics service market growth, further strengthening logistics requirements for storage, handling, and long-distance transport.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated Supply Chains and Sustainable Logistics Solutions Propel Market Leaders

The biomass logistics service sector is driven by companies that specialize in end-to-end biomass supply chain management, offering integrated solutions that ensure reliable feedstock delivery, sustainability compliance, and operational efficiency. Leading players such as Drax Group, Veolia, ENGIE, Vattenfall, Enviva, and major regional logistics integrators dominate the competitive landscape by providing comprehensive services ranging from feedstock sourcing and aggregation to transport, storage, handling, and pre-processing.

These industry leaders differentiate themselves through advanced logistics infrastructure, strong supplier networks, and the adoption of digital technologies that enhance transparency and efficiency within biomass supply chains. Their capabilities include real-time monitoring systems, sustainability certification support, automated handling equipment, and optimized multimodal transportation networks designed to serve large-scale bioenergy and industrial facilities. For example, Drax’s extensive pellet supply chain, Enviva’s certified biomass export operations, Veolia’s waste-to-energy logistics frameworks, and ENGIE’s integrated biomass procurement systems collectively strengthen the industry’s ability to deliver consistent, verifiable, and cost-efficient biomass logistics services across the global market.

LIST OF KEY BIOMASS LOGISTICS SERVICE COMPANIES PROFILED

- Drax Group plc (U.K.)

- Enviva Inc. (U.S.)

- Veolia Environnement S.A. (France)

- ENGIE S.A. (France)

- Vattenfall AB (Sweden)

- Ørsted A/S (Denmark)

- CM Biomass Partners A/S (Denmark)

- Stora Enso Oyj (Finland)

- Mondi plc (U.K.)

- SUEZ S.A. (France)

KEY INDUSTRY DEVELOPMENTS

- August 2025: CM Biomass Partners launched a terminal for biomass handling and export in Northern Europe, which will allow them to handle large-volume shipments more easily and, at the same time, will support the international pellet trade that is growing.

- June 2025: Veolia opened up a new processing unit for organic waste, which is the first step in the expansion of their waste-to-biomass operations, so there will be more biomass collection needed in the region.

- April 2025: Enviva has entered into a long-term strategic partnership with a major utility company in Asia, which is going to be supplied with certified woody biomass, and the company has also invested in expanded port-side storage, upgraded shipment logistics, and bulk transport to make the whole process faster.

- March 2025: ENGIE launched an integrated biomass sourcing and logistics initiative across Europe, with an objective to improve feedstock traceability, optimize transport routes, and support renewable heat projects in key industrial clusters.

- January 2025: Drax Group announced a new multi-year investment program to expand its sustainable biomass supply chain, which includes upgrades to pellet production facilities and enhancements to long-haul logistics infrastructure supporting global exports.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2024 |

|

Growth Rate |

CAGR of 6.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type, Feedstock Type, End User, and Region |

|

By Service Type |

· Transportation · Collection & Aggregation · Storage & Handling · Pre-processing / Conditioning · Others |

|

By Feedstock Type |

· Agricultural Residues · Forestry Residues · Energy Crops · Urban Biomass Waste · Others |

|

By End User |

· Bioenergy Producers · Biofuel Manufacturers · Power & Utility Plants · Pulp & Paper Industry · Others |

|

By Region |

· North America (By Service Type, By Feedstock Type, By End User, and By Country) o U.S. (By Feedstock Type) o Canada (By Feedstock Type) o Mexico (By Feedstock Type) · Europe (By Service Type, By Feedstock Type, By End User, and By Country) o U.K. (By Feedstock Type) o Germany (By Feedstock Type) o France (By Feedstock Type) o Italy (By Feedstock Type) o Spain (By Feedstock Type) o Rest of Europe · Asia Pacific (By Service Type, By Feedstock Type, By End User, and By Country) o China (By Feedstock Type) o India (By Feedstock Type) o Japan (By Feedstock Type) o South Korea (By Feedstock Type) o Rest of Asia Pacific · Middle East and Africa (By Service Type, By Feedstock Type, By End User, and By Country) o GCC (By Feedstock Type) o South Africa (By Feedstock Type) o Rest of Middle East & Africa · South America (By Service Type, By Feedstock Type, By End User, and By Country) o Brazil (By Feedstock Type) o Argentina (By Feedstock Type) o Rest of South America |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.24 billion in 2025 and is projected to reach USD 5.76 billion by 2034.

In 2025, the market value stood at USD 0.93 billion.

The market is expected to exhibit a CAGR of 6.6% during the forecast period of 2026-2034.

The power & utility plants segment led the market by End User.

Rising adoption of renewable energy is driving the market growth.

Drax Group plc, Enviva Inc., Veolia Environnement S.A., and Vattenfall AB are some of the prominent players in the market.

Europe dominated the market in 2025.

The biofuel manufacturers are expected to grow with the highest CAGR.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us