Broadband Services Market Size, Share & Industry Analysis, By Connection Type (Fixed Broadband and Mobile Broadband), By Technology (Fiber Optic (FTTH/FTTB/FTTC), Digital Subscriber Line (DSL), Cable Broadband, Satellite Broadband, and Fixed Wireless Access (FWA)), By End User (Residential, Commercial, and Government & Public Sector), and Regional Forecast, 2026-2034

Broadband Services Market Size and Future Outlook

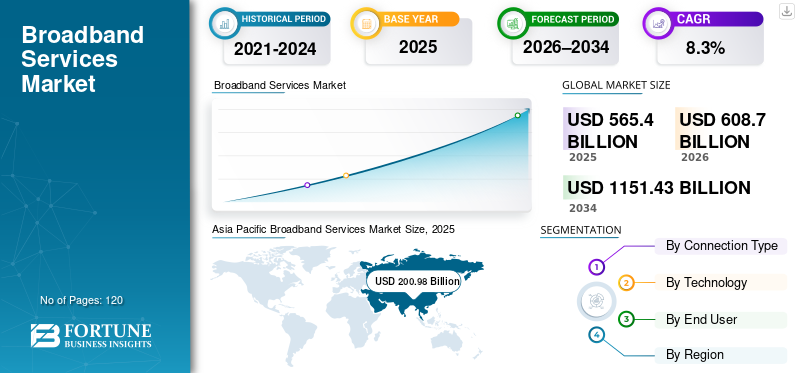

The global broadband services market size was valued at USD 565.40 billion in 2025. The market is projected to grow from USD 608.70 billion in 2026 to USD 1,151.43 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period. Asia Pacific dominated the broadband services market with a market share of 35.55% in 2025.

Broadband services are witnessing sustained growth driven by rising demand for broadband connectivity, accelerating digital consumption, and significant investments in fiber optic networks and next-generation wireless infrastructure. Growing numbers of internet users, increased reliance on remote work, and expanding use of cloud-based platforms are intensifying the demand for high speed internet with improved speed and reliability across residential, enterprise, and public-sector applications. In parallel, telecom operators are modernizing broadband infrastructure through fiber optic connectivity, high-speed cable upgrades, and expanded fixed wireless access to improve broadband accessibility and coverage. Government-backed initiatives to bridge the digital divide, along with long-term infrastructure planning, continue to support market growth and strengthen the position of leading companies in the global market.

- In 2024, AT&T accelerated its fiber expansion strategy, announcing plans to pass over 30 million locations with fiber by 2025, while Verizon expanded its 5G fixed wireless access footprint across multiple U.S. states to address underserved broadband markets.

AT&T Inc., Verizon Communications Inc., Comcast Corporation, China Mobile Ltd., and Deutsche Telekom AG are among the leading players holding a significant share of the global market. Extensive fixed and mobile network infrastructure, large-scale fiber and 4G/5G deployments, strong spectrum holdings, and diversified broadband portfolios spanning FTTH, cable, mobile broadband, and fixed wireless access underpin the competitive positioning of major operators.

Download Free sample to learn more about this report.

Broadband Services Market KEY TAKEAWAYS

- 2025 Market Size: USD 565.40 Billion

- 2026 Market Size: USD 608.70 Billion

- 2034 Forecast Market Size: USD 1,151.43 Billion

- CAGR: 8.3% from 2026–2034

- Asia Pacific dominated the broadband services market with a 35.55% share in 2025.

- Fixed broadband accounted for a significant share of the global broadband services market in 2025.

- Fiber optic (FTTH/FTTB/FTTC) held the largest share of the market by technology segment in 2025.

North America

North America generated USD 152.69 billion in revenue in 2025, supported by strong broadband penetration and advanced network infrastructure.

Europe

Europe continues to experience growth driven by FTTH rollout, cable network upgrades, and expansion of 5G-based broadband services.

Asia Pacific

Asia Pacific generated USD 200.98 billion in revenue in 2025 and remained the fastest-growing regional market.

U.S.

U.S. The market is projected to reach approximately USD 137.10 billion in revenue by 2026.

Japan

Japan The market is estimated to reach USD 24.93 billion in 2026.

Read More

BROADBAND SERVICES MARKET TRENDS

Legacy Copper-Based Networks to Fiber- and Software-Defined Broadband Architectures Pose as Market Trend

Broadband operators are increasingly challenged by aging copper and hybrid access networks, rising maintenance costs, and limitations in meeting growing bandwidth and latency requirements. Many legacy DSL and cable-based broadband infrastructures are approaching end-of-life, driving accelerated investment in network modernization, particularly in dense urban and brownfield network environments where service continuity is critical. In response, service providers are prioritizing Fiber-To-The-Home (FTTH) deployments, software-defined access networks, and virtualized broadband platforms that enable higher capacity, improved reliability, and more efficient service provisioning. These modernization initiatives are designed to extend network lifecycles, reduce operational expenditure, and support advanced digital services while minimizing customer disruption during migration from legacy access technologies.

- For example, in October 2024, Deutsche Telekom announced the accelerated shutdown of legacy copper-based broadband infrastructure in selected European markets, expanding its FTTH rollout strategy to support long-term capacity requirements and improve network efficiency.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Dependence of Critical Infrastructure and Public Services on Always-On Broadband Connectivity Drives Market Growth

The increasing reliance of critical infrastructure and public services on continuous, high-availability broadband connectivity is a key driver of the broadband services market growth. Healthcare systems, utilities, transportation networks, emergency response services, and digital governance platforms are increasingly dependent on reliable, low-latency internet access to support real-time operations and service delivery. The expansion of telehealth, digital public services, smart grids, intelligent transport systems, and connected surveillance networks is raising minimum performance, security, and uptime requirements for broadband networks. As a result, governments and service providers are investing in resilient fixed and mobile broadband infrastructure, redundant network architectures, and expanded coverage to ensure uninterrupted connectivity for mission-critical applications across both urban and remote environments.

- For instance, in November 2024, Deutsche Telekom strengthened its secure broadband connectivity offerings for public administration and critical infrastructure operators in Germany, expanding fiber-based access and network redundancy to support emergency services, smart city platforms, and digital government applications.

MARKET RESTRAINTS

High Capital Expenditure and Deployment Complexity Constraining Broadband Network Expansion

Broadband network deployment often requires substantial upfront capital investment due to the cost of access infrastructure, last-mile connectivity, network equipment, and supporting civil works. In addition to infrastructure costs, integrating new broadband technologies with existing legacy networks, IT systems, and operational platforms can increase deployment complexity and overall project timelines. For operators serving low-density, rural, or price-sensitive markets, these high capital and integration requirements can delay network upgrades or limit coverage expansion. As a result, broadband adoption and service quality improvements may be constrained in regions where return-on-investment remains uncertain or where infrastructure modernization requires significant financial and operational commitment.

MARKET OPPORTUNITIES

Expansion of Broadband Access into Underserved and Semi-Urban Regions Creating New Growth Avenues

Broadband adoption is expanding beyond major urban centers into semi-urban, rural, and underserved regions, creating new growth opportunities for broadband service providers. These areas increasingly require affordable, scalable, and rapidly deployable connectivity solutions to support digital inclusion, remote work, online education, telehealth, and small business operations. Traditional fiber deployments are often constrained by cost and deployment timelines in such markets, encouraging operators to adopt alternative access technologies including fixed wireless access (FWA), hybrid fiber-wireless networks, and satellite broadband.

- For instance, in March 2024, Verizon Communications expanded its 5G fixed wireless access broadband services into additional rural and suburban U.S. markets, targeting households and small businesses lacking access to high-speed fixed broadband infrastructure.

MARKET CHALLENGES

High Network Integration Complexity and Skilled Workforce Requirements Increasing Deployment Time and Costs

Network integration complexity remains a major challenge in the market, as operators must ensure seamless interoperability across heterogeneous access technologies, legacy network infrastructure, core platforms, and service management systems. Broadband deployments often involve integrating fiber, cable, mobile, fixed wireless, and satellite networks with existing OSS/BSS platforms, cybersecurity frameworks, and customer provisioning systems. Even minor interoperability issues or configuration inconsistencies can lead to service disruptions, prolonged rollout timelines, and degraded customer experience. Deployments in brownfield network environments frequently require extensive network re-engineering, testing, and validation to maintain service continuity. In addition, advanced broadband networks demand specialized skills in network virtualization, software-defined networking, cybersecurity, and radio planning. Shortages of skilled network engineers, particularly in emerging and remote regions, further increase deployment complexity, operational costs, and time-to-market.

Segmentation Analysis

By Connection Type

High-Capacity ande Reliability Requirements Driving Dominance of Fixed Broadband Services

Based on connection type, the market is segmented into fixed broadband and mobile broadband.

Fixed broadband accounts for a significant share of the global market due to its ability to deliver high-capacity, low-latency, and highly reliable connectivity, particularly in data-intensive residential, enterprise, and public-sector applications. FTTH, cable, and enterprise-grade fixed broadband connections are extensively deployed in markets where continuous connectivity, consistent speeds, and service-level guarantees are critical. This is especially as data consumption rises and applications such as cloud computing, video streaming, remote work, and digital public services expand.

Fixed broadband services offer superior bandwidth stability, higher average revenue per user, and better support for multi-device households and enterprise networks, making them well suited for environments requiring uninterrupted connectivity and predictable performance. These advantages are particularly important in dense urban areas, commercial districts, and critical infrastructure facilities where network reliability and capacity directly impact productivity and service quality. Mobile broadband continues to witness widespread adoption due to its flexibility, rapid scalability, and ability to extend connectivity to areas where fixed infrastructure deployment is limited or uneconomical. Mobile broadband enables on-the-move connectivity and serves as a primary access method in mobile-first and emerging markets.

- For instance, in April 2024, Deutsche Telekom accelerated its fiber broadband expansion across key European markets, strengthening fixed broadband capacity to support rising household and enterprise data demand.

Mobile broadband is projected to witness strong growth driven by expanding 4G and 5G coverage, declining cost per gigabyte, and increasing reliance on smartphones and wireless devices for internet access. The growing adoption of 5G-based mobile broadband and fixed wireless access (FWA) is further enhancing network capacity and enabling mobile networks to support home broadband, enterprise connectivity, and underserved regions.

To know how our report can help streamline your business, Speak to Analyst

By Technology

High-Capacity Fiber Infrastructure Driving Dominance of Fiber Optic Broadband

Based on technology, the market is segmented into fiber optic (FTTH/FTTB/FTTC), Digital Subscriber Line (DSL), cable broadband, satellite broadband, and Fixed Wireless Access (FWA).

Fiber optic (FTTH/FTTB/FTTC) accounts for the largest share of the global market due to its ability to deliver ultra-high bandwidth, low latency, and superior network stability. Fiber-based broadband infrastructure supports increasing demand for high-speed internet across residential, enterprise, and public-sector environments, particularly where data-intensive applications such as cloud computing, video streaming, remote work, and smart infrastructure require consistent performance. Ongoing investments in fiber-to-the-home (FTTH) deployments and copper network replacement programs continue to strengthen fiber’s market dominance.

Fixed Wireless Access (FWA) is projected to witness the highest growth, registering a CAGR of 9.6%, driven by rapid 5G deployment, lower rollout costs, and the ability to extend broadband accessibility in underserved and semi-urban regions. FWA offers a cost-effective alternative to fiber in areas where full fiber deployment is economically constrained, supporting market expansion across emerging economies and rural communities.

- For instance, in March 2024, Verizon Communications expanded its 5G-based Fixed Wireless Access broadband services across additional U.S. markets, targeting households and small businesses lacking fiber connectivity.

By End User

Expansion of Digital Lifestyles, Enterprise Connectivity, and Public Digital Infrastructure Driving Segmental Demand

Based on end user, the market is segmented into residential, commercial, and government & public sector.

The residential segment accounts for a significant share of the global market due to widespread household internet adoption and rising data consumption driven by video streaming, remote work, online education, gaming, and connected home devices. Increasing multi-device usage per household, demand for higher speeds, and the shift toward fiber and high-capacity wireless access are sustaining strong residential broadband demand across both developed and emerging markets.

Broadband services play a critical role in enabling daily digital activities and service delivery across all end-user segments. In the commercial sector, enterprises and small businesses rely on high-performance broadband connectivity to support cloud computing, digital collaboration, e-commerce platforms, point-of-sale systems, and data-intensive operations. Growing adoption of SaaS platforms, remote workforce models, and digital supply chains is increasing demand for reliable, scalable, and secure broadband connections across offices, retail locations, and distributed business environments.

The government & public sector segment is expected to witness faster growth relative to the overall market, driven by expanding digital government initiatives, smart city deployments, and increased reliance on broadband for public service delivery. Investments in e-governance platforms, telehealth, digital education, public safety networks, and connected infrastructure are driving demand for resilient fixed and mobile broadband connectivity across municipal, regional, and national government agencies.

Broadband Services Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Broadband Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for over USD 152.69 billion revenue generated in 2025, supported by strong demand across residential, enterprise, and public-sector users. The region benefits from high broadband penetration, advanced fixed and mobile network infrastructure, and widespread availability of fiber, cable, and 5G-based broadband services. Strong adoption of cloud computing, data-intensive enterprise applications, video streaming, and remote work continues to drive broadband consumption. In addition, large-scale investments in FTTH expansion, 5G fixed wireless access, and network modernization are strengthening service capacity and coverage. The presence of leading broadband operators, high average revenue per user, and ongoing upgrades of legacy networks further support sustained broadband market growth across North America.

U.S. Broadband Services Market

U.S. to dominate the North American market with a revenue of about USD 137.10 billion in 2026, driven by its large consumer base, high broadband penetration, and strong demand for high-speed connectivity across residential, enterprise, and public-sector users. Widespread adoption of cloud computing, data-intensive enterprise applications, video streaming, and remote work continues to support market leadership. The presence of major broadband service providers, extensive fiber and cable infrastructure, and early adoption of 5G-based mobile broadband and fixed wireless access further strengthen the U.S. market position.

Europe

The European market is supported by strong demand from residential users, enterprises, and public-sector digital initiatives across major economies. The region’s emphasis on digital inclusion, sustainable infrastructure development, and compliance with stringent data protection and service quality regulations is driving continued investment in high-capacity broadband networks. Ongoing rollout of FTTH, upgrades of cable infrastructure, and expansion of 5G-based mobile broadband are strengthening network performance and coverage. In addition, large-scale investments in digital government platforms, smart city initiatives, and enterprise cloud adoption particularly across countries such as Germany, France, Italy, Spain, and Netherlands are contributing to sustained broadband market growth across Europe.

U.K. Broadband Services Market

The U.K. market in 2026 is estimated at around USD 22.31 billion, representing roughly 3.7% of global revenues.

Germany Broadband Services Market

Germany’s market is projected to reach approximately USD 27.75 billion in 2026, equivalent to around 4.6% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing broadband services market share, generating revenue of USD 200.98 billion in 2025 globally. Within the region, China and Japan are projected to reach approximately USD 76.09 billion and USD 24.93 billion, respectively, by 2026. Market growth is driven by large population bases, rapid digitalization, and rising demand for high-speed connectivity across residential, enterprise, and public-sector users in China, Japan, South Korea, India, and ASEAN countries. Accelerated rollout of FTTH, expanding 4G and 5G mobile broadband coverage, and increasing adoption of fixed wireless access are supporting broadband expansion across both urban and semi-urban areas. In addition, government-led digital inclusion programs, smart city initiatives, and investments in national digital infrastructure continue to reinforce Asia Pacific’s leadership in the market growth.

China Broadband Services Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 76.09 billion, representing roughly 12.5% of global sales.

Japan Broadband Services Market

The Japan market in 2026 is estimated at around USD 24.93 billion, accounting for roughly 4.1% of the global market.

India Broadband Services Market

The India market in 2026 is estimated at around USD 35.42 billion, accounting for roughly 5.8% of global revenues.

Middle East & Africa

The Middle East & Africa market is shaped by a mobile-first connectivity model and rapid network leapfrogging in regions with limited legacy fixed infrastructure. Subsea cable investments, national data hub development, and aggressive 4G/5G rollouts are expanding international bandwidth and improving network resilience. In parallel, fiber deployment is accelerating in high-income urban markets, particularly across GCC countries and Israel. These dynamics are enabling broadband expansion across government services, enterprises, and consumers despite affordability and infrastructure constraints.

GCC Broadband Services Market

The GCC market is projected to reach around USD 16.86 billion in 2026, representing roughly 2.8% of the global market.

South America

The South America market is shaped by mobile-first usage patterns and uneven fixed infrastructure deployment, particularly in Brazil and Argentina. While large-scale fiber rollout remains limited, expanding 4G and 5G coverage, spectrum refarming, and selective metro fiber investment are steadily improving broadband availability and service quality across the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Network Modernization, Converged Connectivity, and Service Innovation to Scale Broadband Services

The market is moderately consolidated, characterized by the presence of a limited number of large global and regional telecommunications operators with extensive fixed and mobile network infrastructure. Key players such as AT&T, Verizon Communications, Comcast Corporation, Charter Communications, China Mobile, China Telecom, China Unicom, Deutsche Telekom, Reliance Jio, and Vodafone Group hold significant market positions due to their large subscriber bases, strong spectrum holdings, and diversified broadband portfolios spanning fiber, cable, mobile broadband, and fixed wireless access.

Leading operators are strengthening their competitive positioning through continuous investment in network modernization, including large-scale FTTH deployment, 5G expansion, and virtualization of access and core networks. In parallel, companies are enhancing service differentiation through bundled offerings, flexible pricing models, enterprise-grade connectivity solutions, and improved customer experience platforms. Strategic partnerships, infrastructure sharing, selective acquisitions, and geographic expansion are being leveraged to balance capital efficiency with capacity growth, enabling operators to address both mature urban markets and high-growth underserved regions.

- For instance, in 2024, Reliance Jio expanded its JioFiber and AirFiber (5G fixed wireless access) services across multiple Indian cities and semi-urban markets, strengthening its converged fiber-wireless broadband strategy to scale high-speed connectivity while optimizing deployment costs.

LIST OF KEY BROADBAND SERVICES COMPANIES PROFILED

- Comcast Corporation (U.S.)

- Charter Communications (U.S.)

- China Mobile Hong Kong Company Limited (China)

- China Telecom Global Limited (China)

- AT&T Intellectual Property (U.S.)

- Verizon Communications Inc. (U.S.)

- China Unicom Limited (Hong Kong)

- Deutsche Telekom AG (Germany)

- Reliance Jio (India)

- Vodafone Group (U.K.)

KEY INDUSTRY DEVELOPMENTS

- April 2024: AT&T Inc. announced the acceleration of its fiber network expansion program, increasing planned fiber passes to support rising residential and enterprise demand for high-speed, low-latency broadband services across major U.S. markets.

- March 2024: Verizon Communications Inc. expanded its 5G fixed wireless access (FWA) broadband footprint, targeting underserved suburban and rural areas as a cost-effective alternative to traditional fixed broadband deployment.

- February 2024: China Mobile Ltd. strengthened its gigabit broadband strategy by expanding FTTH and 5G-based broadband services, supporting China’s national digital infrastructure initiatives and growing enterprise connectivity requirements.

- January 2024: Reliance Jio scaled its JioFiber and AirFiber (5G FWA) offerings, extending high-speed broadband access across additional urban and semi-urban regions in India to accelerate digital inclusion and household connectivity.

- November 2023: Vodafone Group expanded its fiber and gigabit broadband partnerships across Europe, leveraging infrastructure-sharing models to improve coverage, enhance network efficiency, and optimize capital expenditure.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Connection Type, Technology, End User, and Region |

| By Connection Type |

|

| By Technology |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 565.40 billion in 2025 and is projected to reach USD 1,151.43 billion by 2034.

In 2025, the market value stood at USD 200.98 billion.

The market is expected to exhibit a CAGR of 8.3% during the forecast period.

By end user, the residential are expected to dominate the market.

The rising data intensity and digital service complexity driving demand for advanced broadband services.

Comcast Corporation, Charter Communications, China Mobile, China Telecom, AT&T, and Verizon Communication are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us