Bus Air Suspension System Market Size, Share & Industry Analysis, By Axle Coverage (Front Axle Air Suspension, Rear Axle Air Suspension, and Full Air Suspension (All Axles)), By System Type (Conventional Air Suspension and Electronically Controlled Air Suspension (ECAS)), By Bus Type (City/Transit Buses, Intercity Buses, Coach/Luxury Buses, and School Buses), By Component Type (Air Springs (Bellows), Air Compressors, Air Supply Units & Reservoirs, Height Control Valves/ECUs, and Shock Absorbers), and Regional Forecast, 2026-2034

Bus Air Suspension System Market Size and Future Outlook

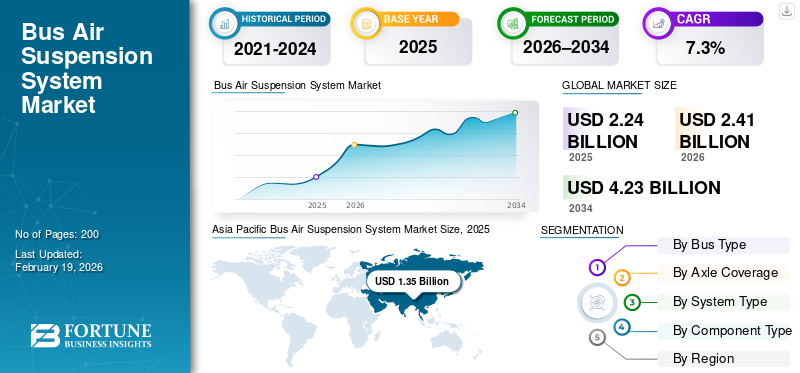

The global bus air suspension system market size was valued at USD 2.24 billion in 2025. The market is projected to grow from USD 2.41 billion in 2026 to USD 4.23 billion by 2034, exhibiting a CAGR of 7.3% during the forecast period. Asia Pacific dominated the bus air suspension system market with a market share of 60.27% in 2025.

A bus air suspension system uses compressed air-filled bellows instead of steel springs to support vehicle weight, absorb road shocks, maintain a constant ride height, and enhance comfort, stability, and safety under varying passenger loads. Rising urbanization, expansion of public transport fleets, and increasing demand for passenger comfort drive market growth. Electrification of buses, low-floor accessibility mandates, and stricter safety and ride-quality regulations further accelerate the adoption of air suspension and electronically controlled systems across city, intercity, and coach buses.

Leading major players such as ZF, Continental, Knorr-Bremse, Hendrickson, and Firestone focus on ECAS integration, lightweight air springs, and partnerships with electric bus OEMs. The market trend emphasizes advanced electronic controls, durability, and aftermarket expansion to support long-term fleet operations.

Download Free sample to learn more about this report.

Bus Air Suspension System Market Key Takeaways

- 2025 Market Size: USD 2.24 billion

- 2026 Market Size: USD 2.41 billion

- 2034 Forecast Market Size: USD 4.23 billion

- CAGR: 7.3% from 2026–2034

- Asia Pacific dominated the bus air suspension system market with a 60.27% share in 2025.

- The Full Air Suspension (All Axles) segment is projected to witness the fastest growth during the forecast period.

- The Electronically Controlled Air Suspension (ECAS) segment is projected to grow at a 9.9% CAGR during the forecast period.

Asia Pacific

Asia Pacific dominated the market with a 60.27% share in 2025.

North America

North America is expected to record the fastest regional growth during the forecast period.

Europe

Europe is expected to witness steady growth, supported by fleet electrification and advanced suspension technologies.

U.S

The market was valued at USD 0.13 billion in 2025.

Japan

The market is expected to grow steadily, supported by demand for advanced bus suspension technologies.

Read More

BUS AIR SUSPENSION SYSTEM MARKET TRENDS

Rising Electrification and Advanced Vehicle Architectures Accelerate Suspension System Evolution

The global bus market is increasingly electrifying, with electric buses rapidly being adopted in urban fleets worldwide. This shift is driving demand for advanced air suspension systems in buses that support the unique weight distribution and ride dynamics of battery-electric buses, and aid comfort, stability, and energy efficiency. Electrified fleets often require electronically controlled air suspension systems to optimize load balancing and passenger comfort across varying conditions. This trend heightens the integration of smart sensors and adaptive controls into air suspension products, enhancing system responsiveness and durability in modern buses.

- In January 2026, Europe recorded over 6,400 battery-electric bus registrations across member states, a 49% increase over the previous year, signaling rapid electrification and technology adoption in public transit.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Urban Public Transport Networks Drive Market Growth

Buses globally are increasingly expected to offer higher ride quality and safety, especially in dense urban and long-distance intercity operations. Air suspension systems provide smoother rides, reduced vibration, and improved stability compared to traditional spring systems, enhancing passenger comfort and reducing driver fatigue. Such benefits are particularly valued on uneven urban roads and during frequent stop-start operations, fueling larger fleet investments in air-suspension-equipped vehicles. Enhanced safety features associated with electronically controlled air suspension systems also appeal to operators focused on minimizing accidents and wear on vehicle components.

MARKET RESTRAINTS

High Initial System Costs Limit Penetration in Cost-Sensitive Markets

Air suspension systems, especially electronically controlled variants, cost significantly more upfront than conventional leaf- or coil-spring alternatives, which can strain fleet-acquisition budgets, particularly for smaller operators. Additionally, the technical complexity of air suspension systems requires specialized maintenance skills and infrastructure. These factors can slow adoption in cost-sensitive regions or among operators with limited technical staff, potentially constraining market growth. The high entry cost and the burden of skilled maintenance remain significant barriers to wider uptake, particularly in developing markets where transport budgets are constrained. This is hindering the bus air suspension system market growth.

MARKET OPPORTUNITIES

Integration of Smart Control and Predictive Maintenance Creates New Growth Avenues

Innovation in smart and adaptive air suspension represents a significant growth opportunity. Next-generation systems that adjust in real time to road conditions, load distribution, and operational parameters can deliver superior comfort, energy efficiency, and predictive maintenance insights. Integration with telematics and fleet management systems enables operators to achieve enhanced vehicle uptime, data-driven maintenance scheduling, and optimized suspension performance. As cities pursue smarter transit ecosystems, suppliers offering connected, adaptive suspension platforms can capture a greater share of the market.

- In January 2026, significant increases in battery-electric bus deployments in Europe underscored the need for advanced, adaptive technologies to support modern transit fleets.

MARKET CHALLENGES

Limited Maintenance Infrastructure Challenges Large-Scale Adoption in Emerging Regions

Transitioning to advanced air suspension systems alongside the adoption of electric buses often requires substantial upgrades to infrastructure and workforce competencies. Fleet electrification requires compatible charging infrastructure, diagnostic tools, and trained technicians. Without sufficient infrastructure and technical capacity, operators may delay or under-invest in advanced suspension systems, even when they offer long-term operational benefits. This challenge can impede modernization in regions lacking robust support systems or workforce training programs, slowing the pace of adoption despite overall market potential.

Download Free sample to learn more about this report.

Segmentation Analysis

By Axle Coverage

Front Axle Air Suspension Leads Due to Cost-Balanced Comfort Solutions

Based on axle coverage, the market is divided into front axle air suspension, rear axle air suspension, and full air suspension (all axles).

The front axle air suspension segment dominates the global market as it balances improved ride comfort, enhanced steering stability, and cost efficiency for city and medium-distance buses. Front axle systems reduce road vibrations for drivers and front passengers and support kneeling functions common in public transit buses. Their relatively lower cost compared to full air suspension makes them widespread across emerging and developed markets. Adoption is strong in fleets that prioritize driver comfort and operational savings without full system complexity. The segment is supported by its use in retrofit upgrades of older buses that aim for progressive comfort improvements without a complete system replacement.

The full air suspension (all axles) segment is projected to grow at a 11.4% CAGR over the forecast period.

By Bus Type

City/Transit Buses are Central to Market Volume Due to Urban Transit Growth

Based on bus type, the market is categorized into city/transit buses, intercity buses, coach/luxury buses, and school buses.

The city/transit buses segment dominates the market due to its high volume in global production and deployment, especially in densely populated regions. Urban transit authorities increasingly specify air suspension to enhance rider comfort, meet kneeling requirements, and improve safety in stop-and-go traffic. City buses also operate on a wider range of road surfaces, increasing the value drivers place on suspension performance. This segment captures the most consistent demand from OEM and aftermarket channels, driven by expanding urban mobility infrastructure and public transit electrification priorities.

Intercity buses are projected to grow at a CAGR of 9.7% over the forecast period.

- In December 2025, Europe recorded more than 6,400 new electric city bus registrations across member states, signaling both rising transit electrification and the adoption of advanced vehicle systems.

To know how our report can help streamline your business, Speak to Analyst

By System Type

Conventional Air Suspension Maintains Dominance with Broad Adoption

Based on system type, the market is bifurcated into conventional air suspension and electronically controlled air suspension (ECAS).

Conventional air suspension holds the largest share as it provides reliable ride leveling and shock absorption at a lower initial cost than electronically controlled systems. It is widely used across city transit, school, and intercity buses in both mature and developing markets where fleets prioritize purchase cost over advanced dynamic control. Operators value its proven durability, easier maintenance, and broad technician familiarity, which lowers operational disruptions. This segment benefits from large installed fleets that retain conventional systems and performance expectations that align with daily passenger service needs, without the need for sophisticated electronics.

The Electronically Controlled Air Suspension (ECAS) segment is projected to grow at a 9.9% CAGR over the forecast period.

By Component Type

Air Compressors Lead Market as They are a Key Source of Pressurized Air

By component type, the market is segmented into air springs (bellows), air compressors, air supply units & reservoirs, height control valves/ECUs, and shock absorbers.

Air compressors are dominating the market as they are the primary source of pressurized air required for the operation of all suspension systems. Every air suspension system, front, rear, or full, depends on a robust compressor to supply and maintain pressure under varying load conditions. Compressors are subject to wear from duty cycles, driving regular aftermarket replacement and service demand. Their performance directly affects system responsiveness and reliability, making them focal points of both OEM design and maintenance planning.

Shock absorbers are projected to grow at a CAGR of 9.1% over the forecast period.

BUS AIR SUSPENSION SYSTEM MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Bus Air Suspension System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global bus air suspension system market share due to rising bus production and deployment. Rapid urbanization, large-scale public transport programs, and expanding electric bus fleets underpin strong OEM demand. While average system prices are lower than in Europe and North America, the region’s scale ensures the largest absolute market size, with growth sustained by both new installations and aftermarket replacement.

China Bus Air Suspension System Market

China is the largest country market globally, valued at USD 0.74 billion in 2025, supported by massive city bus fleets and world-leading electric bus deployment. Air suspension systems are widely adopted in urban and intercity buses to manage heavy battery loads, enhance ride comfort, and enhance durability. Strong domestic manufacturing capacity ensures high installation volumes and a growing aftermarket base.

Japan Bus Air Suspension System Market

The market in Japan was valued at USD 0.20 billion in 2025. Japan’s market emphasizes advanced engineering, ride comfort, and reliability. Buses commonly feature high-quality air suspension systems, particularly in urban and intercity applications. Adoption of electronically controlled systems is strong, driven by passenger comfort expectations and stringent operational standards, resulting in higher value per bus despite lower production volumes.

India Bus Air Suspension System Market

India represents a rapidly growing market and is expected to rise at a CAGR of 11% over the forecast period, as urban transit networks expand and state transport undertakings modernize fleets. Adoption of air suspension is increasing in city and intercity buses, particularly under government-supported public transport programs. While penetration remains lower than in developed markets, rising comfort expectations and electrification are accelerating demand.

North America

North America represents the fastest-growing regional market for bus air suspension systems, driven by accelerated public transit fleet renewal and electrification. The increasing replacement of aging buses, combined with stricter accessibility and ride-comfort requirements, is driving up air-suspension penetration across new procurements. The region also benefits from a higher average system value per bus, driven by greater adoption of electronically controlled air suspension and premium components, supporting faster market-value growth.

U.S. Bus Air Suspension System Market

The U.S. market was valued at USD 0.13 billion in 2025. Large municipal transit fleets drive the U.S. market, federal clean transportation funding, and a growing pipeline of electric and low-floor buses. Transit agencies increasingly specify air suspension to improve passenger comfort, enable kneeling, and enhance vehicle stability. Strong aftermarket demand arises from the sizable installed base of buses operating under high utilization, supporting sustained replacement of compressors, air springs, and shock absorbers.

Europe

Europe represents a mature but technology-intensive market characterized by high regulatory standards for safety, emissions, and accessibility. Air suspension adoption is well established across city, intercity, and coach buses, with a strong shift toward electronically controlled systems. Growth is supported by fleet electrification, cross-border coach travel, and continuous replacement demand, keeping the region a stable contributor to global revenues.

Germany Bus Air Suspension System Market

The market in Germany was valued at USD 0.15 billion in 2025. Germany leads the European market due to its strong domestic bus manufacturing base and early adoption of advanced suspension technologies. High penetration of ECAS, premium coach fleets, and electric city buses drives higher system value per vehicle. German operators prioritize ride quality, vehicle stability, and lifecycle efficiency, supporting consistent OEM and aftermarket demand.

U.K. Bus Air Suspension System Market

Urban fleet upgrades and low-emission public transport initiatives drive the U.K. market. The market was valued at USD 0.06 billion in 2025. City buses are increasingly adopting air suspension to meet accessibility requirements and improve the passenger experience. Continued replacement of diesel fleets with electric and hybrid buses supports steady demand for modern air suspension systems and related components.

Rest of the World

The Rest of the World market, including Latin America and the Middle East & Africa, shows gradual growth driven by selective fleet modernization. Air suspension adoption is concentrated in city and intercity buses in major urban centers. Market expansion is paced by infrastructure readiness and maintenance capability, with steady long-term potential as public transport investment increases.

COMPETITIVE LANDSCAPE

Key Industry Players

Integrated System Engineering, Electrification Readiness, and OEM Partnerships Define Bus Air Suspension Competition

System integration capabilities, durability engineering, and close collaboration with bus OEMs and transit authorities shape the global bus air suspension system market trends. Leading players such as ZF (WABCO), Knorr-Bremse, Continental, Hendrickson, Firestone, Trelleborg, and Hitachi Astemo compete through advanced air springs, high-efficiency compressors, and electronically controlled air suspension (ECAS) platforms tailored for city, intercity, and electric buses. Competitive differentiation increasingly centers on lightweight designs, improved lifecycle performance, consumer preferences, and compatibility with electric and low-floor bus architectures. Suppliers strengthen market position by expanding localized manufacturing, enhancing aftermarket service networks, and forming long-term supply agreements with global bus manufacturers. Strategic focus also includes digital diagnostics, predictive maintenance features, and modular suspension architectures to reduce the total cost of ownership for fleet operators.

- In June 2024, ZF expanded its commercial vehicle chassis technology portfolio to support electric bus platforms, reinforcing its air suspension and ECAS capabilities for next-generation urban transit fleets.

LIST OF KEY BUS AIR SUSPENSION SYSTEM COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Continental AG (Germany)

- Knorr-Bremse AG (Germany)

- Hendrickson USA, L.L.C. (U.S.)

- Firestone Industrial Products (U.S.)

- Trelleborg AB (Sweden)

- Hitachi Astemo Ltd. (Japan)

- Mando Corporation (South Korea)

- Dongfeng Electronic Technology Co., Ltd. (China)

- BWI Group (Luxembourg)

- ITT Enidine Inc. (U.S.)

- CVG (Commercial Vehicle Group, Inc.) (U.S.)

- Sanhua Automotive (China)

- FSS (Fuwa Suspension Systems) (China)

- Wabco India Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Ashok Leyland secured a contract to supply 1,937 buses to the Tamil Nadu State Transport Undertakings, with many urban low-entry and semi-low-floor buses featuring air suspension systems to enhance ride comfort and passenger accessibility on city and mofussil routes. This order reinforces Ashok Leyland’s leadership in bus technology and supports modern public transport upgrades.

- June 2025: ZF announced series production of its fifth-generation OptiRide Electronically Controlled Air Suspension (ECAS) for Hyundai Motor Company, featuring a lean architecture that consolidates solenoid valves and pressure sensors into a Smart Pneumatic Actuator to reduce components and integration effort supporting bus OEMs’ push for smarter, lighter suspension control.

- June 2025: Hendrickson unveiled new STEERTEK NXT advancements on select Blue Bird school bus models, positioning them as the platform for SOFTEK and AIRTEK suspension systems. The update targets weight reduction and efficiency gains for student transportation fleets, reinforcing supplier OEM collaboration around front-end ride/handling improvements.

- September 2024: Hendrickson partnered with International Trucks to launch an expanded PRIMAAX EX rear air suspension variant, adding configurations such as 12-inch ride height and air disc brake clearance. While vocational-focused, the launch reflects ongoing heavy-duty air-suspension innovation that influences shared platform learnings across commercial vehicle segments, including buses.

- August 2024: Continental introduced the N7 commercial-vehicle air spring as an original-equivalent aftermarket spare part designed for one-to-one replacement of Tough RuNR air springs. The company positioned the N7 for fleet and workshop customers, supporting uptime and lifecycle economics, an important aftermarket lever for bus operators managing high utilization and scheduled replacements.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.3% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Bus Type, By Axle Coverage, By System Type, By Component Type, and By Region. |

|

By Axle Coverage |

· Front Axle Air Suspension · Rear Axle Air Suspension · Full Air Suspension (All Axles) |

|

By System Type |

· Conventional Air Suspension · Electronically Controlled Air Suspension (ECAS) |

|

By Bus Type |

· City/Transit Buses · Intercity Buses · Coach/Luxury Buses · School Buses |

|

By Component Type |

· Air Springs (Bellows) · Air Compressors · Air Supply Units & Reservoirs · Height Control Valves/ECUs · Shock Absorbers |

|

By Region |

· North America (By Bus Type, By Axle Coverage, By System Type, By Component Type, and By Country) o U.S. (By Bus Type) o Canada (By Bus Type) o Mexico (By Bus Type) · Europe (By Bus Type, By Axle Coverage, By System Type, By Component Type, and By Country) o Germany (By Bus Type) o U.K. (By Bus Type) o France (By Bus Type) o Rest of Europe (By Bus Type) · Asia (By Bus Type, By Axle Coverage, By System Type, By Component Type, and By Country) o China (By Bus Type) o Japan (By Bus Type) o India (By Bus Type) o South Korea (By Bus Type) o Rest of Asia Pacific (By Bus Type) · Rest of the World (By Bus Type, By Axle Coverage, By System Type, and By Component Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.24 billion in 2025 and is projected to reach USD 4.23 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 1.35 billion.

The market is expected to grow at a CAGR of 7.3% during the forecast period from 2026 to 2034.

By system type segment, the conventional air suspension segment led the market.

Expanding urban public transport networks drive market growth.

Key market players include ZF, Continental, Knorr-Bremse, Hendrickson, and Firestone.

Asia Pacific accounted for the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us