Bus Chassis & Body Components Market Size, Share & Industry Analysis, By Component (Frame & sub-frames/cross members, Axles, Suspension Systems, Body Structure, and Others), By Bus Type (City/Transit Buses, Intercity Buses, School Buses, and Others), By Propulsion (ICE and Electric), By Material Type (Steel, Aluminum, and Others), and Regional Forecast, 2026-2034

Bus Chassis & Body Components Market Size and Future Outlook

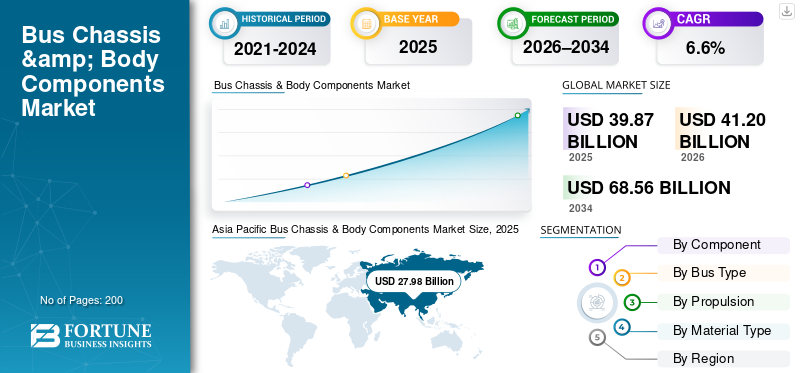

The global bus chassis & body components market size was valued at USD 39.87 billion in 2025. The market is projected to grow from USD 41.20 billion in 2026 to USD 68.56 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period. Asia Pacific dominated the Bus chassis & body components market with a market share of 70.18% in 2025.

The market comprises manufacturers and suppliers of structural frames, powertrain mounting systems, suspension, braking, steering, exterior panels, interiors, glazing, and electrical components used in bus assembly, customization, and refurbishment across public, private, and commercial transportation segments.

Key market drivers include rising public transportation demand, urbanization, government investments in mass transit, fleet replacement programs, growth in the number of electric and low-emission buses, stricter safety and emission regulations, increasing intercity travel, and demand for lightweight, durable, and cost-efficient bus structures and components.

The market is moderately consolidated, driven by OEM partnerships, technology upgrades, and regional manufacturing strength. Key players include Volvo Group, Daimler Truck, Tata Motors, Ashok Leyland, Scania, MAN Truck & Bus, Marcopolo, Alexander Dennis, and BYD Auto.

Download Free sample to learn more about this report.

BUS CHASSIS & BODY COMPONENTS MARKET Key Takeaways

- 2025 Market Size: USD 39.87 Billion

- 2026 Market Size: USD 41.20 Billion

- 2034 Forecast Market Size: USD 68.56 Billion

- CAGR: 6.6% from 2026–2034

- Asia Pacific dominated the bus chassis & body components market with a 70.18% share in 2025.

- The body structure segment held the largest market share in 2025.

- The city and transit buses segment accounted for the dominant market share in 2025.

Asia Pacific

Asia Pacific led the market, driven by urbanization, transit investments, and bus fleet expansion.

Europe

Europe held the second-largest share, supported by fleet upgrades and electric bus adoption.

North America

North America ranked third, driven by fleet upgrades and bus electrification programs.

U.S.

The bus chassis & body components market is estimated at USD 0.66 billion in 2026.

Japan

Investments in public transit and low-emission buses are driving component demand.

Read More

BUS CHASSIS & BODY COMPONENTS MARKET TRENDS

Increasing Focus on Passenger Comfort and Safety to Shape Design Trends

Bus operators are increasingly emphasizing passenger comfort, safety, and accessibility to improve ridership and service quality. This trend is driving demand for enhanced body components such as low-floor structures, improved seating layouts, better insulation, noise reduction systems, and advanced glazing. Safety-oriented features, including reinforced frames and crash-compliant body designs, are gaining traction. As buses become more passenger-centric, component innovation is shifting beyond durability and more towards user experience and regulatory compliance.

MARKET DYNAMICS

MARKET DRIVERS

Growing Urban Public Transport Investments to Drive Market Demand

Rapid urbanization and increasing commuter volumes are pushing governments to expand and modernize public transportation systems. Large-scale investments in city buses, BRT corridors, and intercity fleets are directly boosting demand for bus chassis and body components. New fleet additions require complete structural assemblies, while specification upgrades increase the use of advanced suspension, braking, and body modules. Emerging economies are prioritizing bus-based mobility due to cost efficiency, further supporting sustained component demand across OEM and body builder ecosystems.

- For instance, In November 2025, the U.S. DOT/FTA announced over USD 2 billion in transit bus and bus-facility grants across many providers an example of public funding directly translating into new bus procurement and retrofit demand for chassis and body components.

MARKET RESTRAINTS

High Customization and Tooling Costs to Limit the Entry of New Entrants

Bus chassis and body components often require region-specific designs, safety compliance, and customer-driven customization, resulting in high engineering, tooling, and validation costs. Smaller suppliers face challenges in achieving economies of scale while meeting diverse regulatory and operator requirements. Long term development cycles and dependency on OEM approvals further restrict rapid market entry, limiting supplier diversification and slowing innovation adoption across price-sensitive markets.

MARKET OPPORTUNITIES

Rising Electric Bus Adoption to Create Lightweight Component Opportunities

The global shift toward electric buses is creating strong demand for lightweight and modular chassis and body components. Battery integration demands optimized frames, advanced materials, and redesigned mounting systems to offset added vehicle weight. Suppliers offering aluminum structures, composite panels, and integrated body-chassis solutions can gain competitive advantage. Additionally, electric platforms encourage platform standardization, enabling component suppliers to scale production while supporting OEM electrification roadmaps.

- For instance, in January 2026, Dubai’s RTA launched new Zhongtong electric buses as part of a broader fleet add plan (including electric units), reinforcing demand for optimized frames, mounts, and lightweight body structures to accommodate electrified architectures.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Price Fluctuations to Challenge Profit Margins

The bus chassis and body components market growth faces challenges from volatile raw material prices and supply chain disruptions. Steel, aluminum, and composite material costs directly impact component pricing and profitability. Global sourcing dependencies and logistics uncertainties can delay production schedules and strain OEM–supplier relationships. Managing cost pressures while maintaining quality, compliance, and delivery timelines remains a critical challenge, particularly for suppliers operating on long-term, fixed-price contracts.

Segmentation Analysis

By Component

Passenger Safety, Customization, and Regulatory Compliance Drives Body Structure Segment’s Dominance

Based on component, the market is classified into frame & sub-frames/cross members, axles, suspension systems, body structure and others.

The body structure segment dominates the bus chassis & body components market share due to its critical role in passenger safety, durability, and regulatory compliance. Bus bodies integrate exterior panels, interiors, glazing, doors, and crash-resistant structures, making them the most value-intensive component set. Growing demand for low-floor designs, enhanced comfort, and city-specific customization further drives higher spending per vehicle.

The frame & sub-frames/cross members, the second-largest segment, is projected to grow at a CAGR of 6.8% over the forecast period. Increasing adoption of electric buses and heavier powertrain systems is driving demand for reinforced, lightweight structural frames to support battery integration and load-bearing efficiency.

By Bus Type

Rising Urban Mobility Demand and Government Transit Programs to Sustain City/Transit Bus Segment’s Dominance

In terms of bus type, the market is categorized into city/transit buses, intercity buses, school buses, and others.

City and transit buses dominate the market due to large-scale public transport deployment, frequent stop-and-go operations, and high annual utilization. These buses require robust body structures, suspension systems, axles, and interior components to withstand intensive daily use. Continuous fleet expansion, replacements, and refurbishment driven by urbanization and government-backed mass transit initiatives sustain consistent component demand across OEMs and body builders.

The intercity buses segment, the second-largest, is expected to grow at a CAGR of 5.9% over the forecast period. Rising intercity travel, tourism recovery, and demand for long-distance comfort features are driving higher-value chassis and body component requirements.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Type

ICE Segment Dominates Due to Established Fleet Base and Preference in Cost Efficient-Regions

Based on propulsion type, the market is segmented into ICE and electric.

The ICE segment dominates the market due to its vast installed base and continued preference across cost-sensitive and developing regions. ICE buses benefit from established fueling infrastructure, proven chassis architectures, and standardized body designs, ensuring steady demand for frames, suspension, axles, and body structures. Ongoing fleet replacements, refurbishments, and incremental efficiency upgrades continue to support strong component demand without major platform redesigns.

The electric bus segment is the fastest-growing, expanding at a CAGR of 8.0% over the forecast period. Government incentives, emission mandates, and urban transit electrification programs are accelerating their adoption, driving demand for lightweight chassis, reinforced frames, and redesigned body components.

By Material Type

Steel Segment Takes the Lead Due to Its Structural Strength, Cost Advantage, and Manufacturing Familiarity

Based on material type, the market is segmented into steel, aluminum, and others.

Steel dominates the market due to its high structural strength, durability, and cost efficiency across mass-production platforms. OEMs and body builders widely prefer steel for frames, body structures, and load-bearing components because of established fabrication processes, repair ability, and regulatory acceptance. Its ability to withstand heavy-duty operating conditions and long service cycles sustains its consistent demand across city and intercity bus applications.

The aluminum segment is projected to grow at a CAGR of 8.9% over the forecast period. Increasing focus on light weighting, electric bus range optimization, and corrosion resistance is driving aluminum adoption in body panels, frames, and sub-structures.

Bus Chassis & Body Components Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World

Asia Pacific

Asia Pacific Bus Chassis & Body Components Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is also the fastest-growing region, driven by rapid urbanization, population density, and heavy reliance on bus-based public transport. Governments across China, India, and Southeast Asia are investing aggressively in city buses, electric fleets, and intercity connectivity. High-volume procurement, localized manufacturing, and frequent fleet replacement cycles generate strong demand for body structures, frames, axles, and suspension systems are supporting the region’s highest growth momentum globally.

China Bus Chassis & Body Components Market

The China market in 2026 is estimated around USD 15.77 billion, accounting for a dominant global share. Growth is driven by massive urban bus fleets, electric bus leadership, and high-volume domestic manufacturing.

India Bus Chassis & Body Components Market

The India market in 2026 is estimated around USD 7.42 billion, emerging as the fastest-growing market in the region. Expansion is supported by public transport investments, fleet replacement, electrification programs, and strong domestic OEM presence.

Europe

Europe represents the second-largest market share, supported by mature public transport systems and strong regulatory focus on emissions and safety. The region is witnessing steady replacement of aging ICE fleets with low-emission and electric buses, driving demand for advanced chassis and lightweight body components. Investments in intercity and cross-border transport, combined with high-quality standards for passenger comfort and safety, are expected to drive the regional market growth at a CAGR of 6.5% over the forecast period.

Germany Bus Chassis & Body Components Market

The Germany market in 2026 is estimated to be around USD 1.50 billion, reflecting steady demand. Growth is supported by electric bus adoption, strict safety regulations, and continuous fleet modernization across urban and intercity networks.

U.K. Bus Chassis & Body Components Market

The U.K. market in 2026 is estimated to be around USD 1.02 billion, driven by zero-emission bus mandates, government funding, and replacement of aging transit and regional bus fleets.

North America

North America ranks as the third-largest market, driven primarily by public transit fleet modernization and federal and state-level funding programs. Demand is supported by replacement of aging city and school bus fleets, growing adoption of electric buses in urban centers, and refurbishment of existing vehicles. While overall bus volumes are lower than Asia Pacific and Europe, higher per-vehicle component value and strict safety standards leads to consistent demand for chassis, body structures, and suspension components.

U.S. Bus Chassis & Body Components Market

The U.S. market in 2026 is valued around USD 0.66 billion, supported by transit funding, school bus electrification, and gradual replacement of aging public transportation fleets.

Rest of the World

The Rest of the World market, including South America, the Middle East, and Africa, is witnessing gradual growth supported by expanding urban transport systems and improving road connectivity. Government-led transit projects, rising intercity travel, and tourism recovery are increasing demand for buses and related components. Although procurement volumes remain uneven, growing emphasis on durable, cost-efficient body structures and localized assembly is steadily strengthening the regional market growth.

COMPETITIVE LANDSCAPE

OEMs, Body Bus Manufacturers, and Tier-1 Component Suppliers Are Fostering Competitiveness in the Market

The market is dominated by established global OEMs and tier-1 suppliers such as Volvo Group, Daimler Truck, Tata Motors, Ashok Leyland, Scania, MAN Truck & Bus, ZF Friedrichshafen, Meritor (Cummins), Hendrickson, Marcopolo, and Alexander Dennis. These players leverage integrated chassis platforms, strong engineering capabilities, and long-term relationships with transit authorities and fleet operators. Their portfolios span frames, axles, suspension systems, body structures, and modular assemblies, enabling end-to-end vehicle solutions.

Competitive strategies increasingly focus on lightweight materials, electric-bus-ready architectures, and modular designs to support customization and regulatory compliance. Strategic partnerships with battery suppliers, material specialists, and regional body builders, along with high capacity expansion and localization, are strengthening global competitiveness amid rising electrification and public transport investments.

LIST OF KEY BUS CHASSIS & BODY COMPONENTS MARKET COMPANIES PROFILED

- Volvo Group (Sweden)

- Daimler Truck AG (Germany)

- Ashok Leyland Limited (India)

- BYD Company Ltd. (China)

- Tata Motors Limited (India)

- Yutong Group Co., Ltd (China)

- New Flyer Industries (Canada)

- Motor Coach Industries (U.S.)

- Blue Bird Corporation (U.S.)

- IC Bus (U.S.)

- Anhui Ankai Automobile Co., Ltd (China)

- Alexander Dennis (U.K.)

- Neoplan (Germany)

- Plaxton (England)

- Solaris Bus & Coach (Poland)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Ashok Leyland announced extensive capacity expansions for its bus and LCV production, boosting annual bus output from 12,000 to over 20,000 units through facility upgrades in Andhra Pradesh and a new Lucknow plant, positioning the company to meet rising chassis and body component demand. Investments include R&D and advanced manufacturing, reflecting confidence in long-term market growth.

- October 2025: Busworld Europe 2025 showcased next-gen bus technologies, with global OEMs and tier suppliers unveiling electric, hydrogen, and advanced drivetrain innovations in chassis and body systems, underlining industry focus on sustainable public transport solutions.

- October 2025: Scania unveiled a new high-floor battery-electric bus and coach platform at Busworld Europe, expanding its electric offerings.

- October 2025: Ashok Leyland secured a major order from Tamil Nadu State Transport Undertakings for 1,937 buses valued at USD 73.96 million (INR 669 crore), reinforcing its leadership in supplying BS VI diesel bus chassis and fully built low-floor buses across the state’s public transport network. Deliveries span late 2025 to early 2027, demonstrating strong demand for reliable chassis and body systems in India’s mass transit expansion.

- September 2025: Volvo Buses launched a new Volvo BZR Electric coach chassis with up to 720 kWh battery capacity and 700 km range, enabling longer electric routes and modular axle configurations.

- April 2025: Scania extended its battery-electric bus portfolio with a three-axle 6×2*4 electric chassis for city/suburban routes.

- March 2024: Volvo Buses launched its global BZR electric bus platform, extending its electrification strategy with a flexible chassis platform for city, intercity, and commuter applications.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.6% from 2025-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Component

By Bus Type

By Propulsion

By Material Type

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 39.87 billion in 2025 and is projected to reach USD 68.56 billion by 2034.

In 2025, the market value stood at USD 27.98 billion.

The market is expected to exhibit a CAGR of 6.6% during the forecast period.

The city/transit buses segment led the market by bus type.

Growing urban public transport investments to drive component demand.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us