Business Software and Services Market Size, Share & Industry Analysis, By Offering (Software and Services), By Deployment (On-premises and Cloud), By Enterprise Type (Large Enterprises and SMEs), By Industry (BFSI, Retail, Manufacturing, IT & Telecom, Healthcare, and Others), and Regional Forecast, 2026-2034

BUSINESS SOFTWARE AND SERVICES MARKET SIZE AND FUTURE OUTLOOK

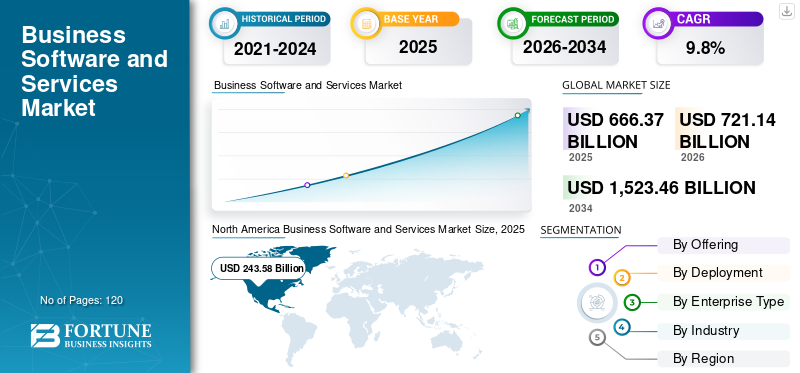

The global business software and services market size was valued at USD 666.37 billion in 2025. The market is projected to grow from USD 721.14 billion in 2026 to USD 1,523.46 billion by 2034, exhibiting a CAGR of 9.8% during the forecast period. North America dominated the global business software and services market with a market share of 36.55% in 2025.

Business software and services refer to all the digital applications and professional services that organizations use to manage, automate, and optimize their core business operations. The market is driven by cloud adoption, digital transformation, and AI-enabled automation. Organizations are modernizing legacy systems, and digitizing processes, such as finance, HR, supply chains, and customer engagement, creating sustained demand for enterprise software and related services. Also, the market continues to expand steadily across all major industries and regions.

The market is dominated by established key players, such as Microsoft Corporation, SAP SE, Oracle Corporation, Salesforce, Inc., and Workday, Inc. These players are continuously focusing on building large partner ecosystems, including Independent Software Vendors (ISVs), System Integrators (SIs), and hyperscalers, and app marketplaces around their platforms, often via deep alliances, such as Pega with AWS, Microsoft cloud ecosystem partners, so customers buy into an integrated stack rather than point solutions.

Download Free sample to learn more about this report.

Business Software and Services Market Key Takeaways

- 2025 Market Size: USD 666.37 billion

- 2026 Market Size: USD 721.14 billion

- 2034 Forecast Market Size: USD 1,523.46 billion

- CAGR: 9.8% from 2026–2034

- North America dominated the global business software and services market with a 36.55% share in 2025.

- The services segment is anticipated to grow at the highest CAGR of 10.9% during the forecast period.

- Cloud deployment is expected to grow at the highest CAGR of 11.0% during the forecast period.

North America

North America led the market with a valuation of USD 243.58 billion in 2025.

Asia Pacific

Asia Pacific is projected to reach USD 192.33 billion by 2026, supported by the highest regional CAGR of 12.4%.

Europe

Europe is expected to reach USD 181.73 billion by 2026, growing at a CAGR of 8.9%.

U.S.

The market is estimated to reach USD 180.56 billion in 2026, driven by strong cloud platform adoption.

Japan

Growing enterprise digital transformation initiatives are expected to support market expansion.

Read More

IMPACT OF GENERATIVE AI

Transformative Role of Generative AI in Business Software and Services Boosts Market Growth

Generative AI is reshaping the market by embedding “copilots” and intelligent agents directly into core applications such as ERP, CRM, HR, and productivity suites, turning them from passive systems of record into proactive systems of insight and action. Vendors are using GenAI to launch premium Stock-Keeping Units (SKUs), such as AI add-ons for office suites, CRM, and contact centers, which boosts Average Revenue Per User (ARPU) and helps justify higher business software and services spend. On the services side, GenAI accelerates coding, configuration, documentation, testing, and migration work, allowing consulting and SI firms to deliver transformations faster while repositioning themselves as AI strategy and change-management partners rather than pure implementers. It is also intensifying competition and consolidation, as players that quickly build strong AI capabilities, data platforms, and ecosystems gain a structural advantage over niche or legacy vendors that cannot keep pace. For instance,

- In March 2025, according to an industry experts survey, the global spending on generative AI would reach approximately USD 644 billion in 2025, marking a 76.4% increase from 2024 and underlining the rapid monetization of AI in business software and services.

MARKET DYNAMICS

Market Drivers

Rapid Adoption of Cloud-Based Solutions Drives Market Growth

The rapid adoption of cloud based solutions is a major driver of the market as organizations move away from costly, rigid on-premise systems toward scalable, subscription-based platforms. Cloud delivery models such as SaaS enable faster deployment, automatic updates, and lower upfront investment, making enterprise applications more accessible to businesses of all sizes. This shift also supports remote work by providing access to critical systems such as Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Human Resources (HR), and collaboration tools. Additionally, cloud platforms integrate more easily with AI, analytics, and third-party applications, allowing companies to modernize operations and innovate more quickly. As a result, cloud adoption continues to accelerate digital transformation and long-term IT modernization across industries.

- In October 2025, DualEntry, a startup offering AI-native ERP for financial workflows, raised USD 90 million (Series A) and positioned itself as a challenger to legacy ERP vendors by enabling “next-day migration” from older systems to cloud-native platforms.

Market Restraints

Data Security, Privacy Concerns May Hinder Market Growth

Data security and privacy concerns remain a major restraint for the market because organizations are increasingly wary of storing sensitive financial, customer, and operational data on cloud-based or third-party platforms. High-profile cyberattacks, data breaches, and stricter regulations such as GDPR, HIPAA, and industry-specific compliance laws make companies cautious about adopting new digital systems. These concerns are even more pronounced in sectors such as BFSI, healthcare, and government, where data sensitivity is extremely high. As a result, businesses may delay migrations, limit cloud adoption, or choose partial implementations, slowing overall business software and services market growth.

Market Opportunities

Rising Use of AI, Automation & Analytics in Business Operations Creating Opportunities for Market Growth

The rising use of AI, automation, and analytics is creating a major opportunity in the market as organizations seek to shift from manual, reactive processes to intelligent, data-driven operations. AI and automation enable faster decision-making, improved forecasting, and reduced operational costs across functions such as finance, HR, supply chain, and sales. Also, adoption of AI in the software plays an important role to improve customer experience. Advanced analytics allows businesses to unify siloed data and extract actionable insights, boosting performance and competitiveness. Service providers are also capitalizing on this trend by offering AI-enabled transformation, process automation, and analytics consulting. As enterprises accelerate adoption of GenAI, predictive automation, and real-time analytics, demand for modern software platforms and expert services continues to surge.

- In June 2025, According to industry experts, agentic generative AI systems could automate between 60-70% of employee time in sectors such as banking and insurance, signaling a profound impact on workflow automation and business software demand.

Business Software and Services Market Trends

Rising Digital Transformation and Cloud Migration are Accelerating Market Growth

The rising adoption of business software in the retail sector is significantly fueling market growth as retailers modernize operations to meet evolving consumer expectations and intense competitive pressures. Retailers are increasingly deploying cloud-based POS, CRM, inventory management, and omnichannel commerce platforms to unify online and offline experiences. Advanced analytics and AI-driven tools help optimize pricing, personalize marketing, forecast demand, and improve supply-chain responsiveness. Additionally, workflow automation and integrated ERP systems enable retailers to streamline procurement, store operations, and last-mile logistics. As digital commerce expands and customer journeys become more complex, the need for scalable, data-driven retail software solutions continues to rise, driving overall market momentum.

- In July 2025, Walmart announced its rollout of “Super Agents,” advanced AI tools designed to serve customers, staff, and suppliers, highlighting how retail software and automation investments are now central to operational and customer-experience strategies.

Download Free sample to learn more about this report.

BUSINESS SOFTWARE AND SERVICES MARKET SEGMENTATION ANALYSIS

By Offering

Rising Investment in Cloud-based Software by Organizations Fuels Segment Growth

Based on offering, the market is divided into software (finance, sales & marketing, human resource, supply chain, others (collaboration & productivity, etc.)) and services.

Software captured the largest market share in 2025, estimated at USD 385.18 billion for 2025. Organizations prioritize investments in cloud-based ERP, CRM, HCM, analytics, and collaboration platforms to accelerate digital transformation and AI adoption. Additionally, vendors introduce new AI-enhanced and subscription-based software offerings that drive higher recurring revenues and faster upgrades compared to more service-heavy segments.

Services are anticipated to grow at the highest CAGR of 10.9% during the forecast period. Businesses are increasingly depending on consulting, integration, managed services, and AI-driven transformation support to deploy, optimize, and scale their rapidly expanding cloud and enterprise software ecosystems.

By Deployment

Growing Need for Cost-Efficient and Scalable Solution Drive Cloud-based Software Adoption

Based on deployment, the market is segmented into cloud and on-premises.

Cloud captured the largest market share in 2025, estimated at 452.52 billion. Organizations are rapidly shifting from legacy on-premise systems to scalable, cost-efficient SaaS, and cloud-native platforms that offer faster deployment and lower maintenance burdens. The growing use of AI, analytics, and remote-work technologies, most of which are optimized for cloud environments, further strengthen enterprises’ preference for cloud-based deployments.

Cloud deployment is expected to grow at the highest CAGR of 11.0% during the forecast period. As cloud deployment supports rapid integration with third-party applications, low-code tools, and API ecosystems, making it easier for companies to innovate quickly.

By Enterprise Type

Extensive Digital Transformation Needs Lead Large Enterprises to Dominate

Based on enterprise type, the market is classified into large enterprises and SMEs.

Large enterprises captured the largest market share in 2025 with an estimated revenue of USD 401.07 billion. They have substantial budgets, complex operational requirements, and long-term digital transformation programs that demand advanced ERP, CRM, analytics, and AI-driven platforms. They also invest heavily in customization, integration, and multi-cloud deployments, resulting in significantly higher software and services spending compared to mid-sized and small businesses.

SMEs are expected to grow at the highest CAGR of 11.8% during the forecast period. Increasing access to affordable cloud-based software, automation tools, and AI-driven applications enables smaller firms to digitize operations rapidly and scale more efficiently than before.

By Industry

High Compliance Needs Result in Stronger Software Adoption in BFSI

Based on industry, the market is categorized into BFSI, retail, manufacturing, IT & telecom, healthcare, and others (government, transportation, etc.).

BFSI accounted for the largest market share of USD 158.21 billion in 2025, as BFSI continues to prioritize investments in core banking platforms, digital payments, risk management, compliance, and customer experience software. The sector’s high regulatory demands and rapid shift toward AI-driven automation, fraud detection, and omnichannel services further accelerate spending on advanced business software and related services.

Healthcare is projected to grow at the highest CAGR of 12.6% during the forecast period. Hospitals, clinics, and healthcare networks accelerate adoption of digital health records, telemedicine, AI-driven diagnostics, and integrated patient management systems to improve efficiency, compliance, and care outcomes.

To know how our report can help streamline your business, Speak to Analyst

BUSINESS SOFTWARE AND SERVICES MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America

North America held the largest business software and services market share in 2024, valued at USD 228.82 billion, and also maintained the leading share in 2025, with USD 243.58 billion. The region has a highly mature digital ecosystem, with enterprises investing heavily in cloud platforms, AI-enabled applications, and advanced analytics across all major industries. Additionally, the strong presence of leading software vendors, widespread adoption of SaaS models, and continuous technology innovation further strengthen North America’s dominance in the market. For instance,

- In April 2025, Google LLC announced it would slash business-software pricing by 71% for U.S. federal agencies, a move aimed at increasing penetration into the government software market and challenging entrenched players.

North America Business Software and Services Market Size, 2025

To get more information on the regional analysis of this market, Download Free sample

In 2026, the U.S. market is estimated to reach USD 180.56 billion driven by rapid enterprise adoption of cloud platforms, AI-driven applications, and advanced analytics across sectors such as BFSI, healthcare, retail, and manufacturing. Additionally, the presence of major technology vendors, high digital maturity, and strong investment in modernization, cybersecurity, and automation continues to accelerate domestic demand for enterprise software and IT services.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is anticipated to witness a moderate growth of 8.9% CAGR in the coming years over the forecast period. This fourth highest growth rate amongst other regions will assist Europe in achieving USD 181.73 billion in 2026. Strong government initiatives, data-sovereignty policies, and rising investments in cybersecurity and cross-border digital infrastructure are pushing enterprises to adopt more advanced business software and services. Backed by these factors, the U.K. expected market size for 2026 is USD 35.65 billion, while Germany will record USD 33.81 billion, followed by France at USD 28.73 billion in 2026.

Asia Pacific

Asia Pacific is estimated to reach USD 192.33 billion in 2026 by exhibiting the highest CAGR of 12.4% during the forecast period. Expanding SME digital investments, government-led technology initiatives, and increasing deployment of AI, automation, and mobile-first solutions are driving widespread adoption of business software and services across the region. In 2026, India and China are estimated to achieve USD 26.28 billion and USD 40.57 billion, respectively.

South America

South America is expected to witness significant growth and log USD 37.28 billion in 2026 as increasing startups and tech ecosystems are prompting SMEs and digital-native businesses to adopt scalable SaaS solutions from the outset.

Middle East & Africa

The Middle East & Africa will achieve a market size of USD 46.07 billion in 2026 owing to rising digital-transformation initiatives across government, banking, telecom, and energy sectors, supported by national strategies that prioritize cloud adoption, e-government services, and AI deployment. Additionally, increasing investments in data centers, expanding enterprise IT budgets, and the modernization needs of rapidly developing economies are driving greater demand for business software and IT service solutions. In the region, GCC is set to attain USD 14.68 billion in 2026.

Competitive Landscape

KEY INDUSTRY PLAYERS

Established Firms are Rolling-out AI-Driven Platforms and Industry-Specific Cloud Solutions to Gain Edge

Leading companies in the market are broadening their portfolios by integrating advanced AI capabilities, verticalized cloud platforms, and intelligent automation tools to address the evolving needs of enterprises. These vendors are increasingly embedding generative AI assistants, predictive analytics, and real time automation into ERP, CRM, HCM, and collaboration suites to enhance decision-making and streamline complex workflows. Additionally, major providers are launching industry-tailored cloud solutions for sectors such as healthcare, BFSI, retail, and manufacturing, enabling faster deployment and improved regulatory compliance. Many firms are also expanding their managed services and consulting capabilities to support large-scale digital transformation projects and maximize customer value. To strengthen their market position, key players are entering strategic partnerships with hyperscalers, acquiring niche SaaS innovators, and investing heavily in cybersecurity and data-governance enhancements.

LIST OF KEY COMPANIES PROFILED:

- Microsoft Corporation (U.S.)

- SAP SE (Germany)

- Oracle Corporation (U.S.)

- Salesforce, Inc. (U.S.)

- Workday, Inc. (U.S.)

- Intuit Inc.(U.S.)

- IBM Corporation (U.S.)

- Accenture(Ireland)

- Tata Consultancy Services (India)

- Infosys Limited (India)

- Adobe, Inc. (U.S.)

- ServiceNow (U.S.)

- Alphabet, Inc. (Google LLC) (U.S.)

- Wipro Limited (India)

- HCL Tech (India)

- Capgemini (France)

- Cognizant (U.S.)

- DXC Technology (U.S.)

- NTT Data (Japan)

- Fujitsu (Japan)

….and more

KEY INDUSTRY DEVELOPMENTS:

- November 2025: Tata Consultancy Services (TCS) announced a partnership with regional firms Sybyl and iXAfrica Data Centre Limited to accelerate “sovereign cloud” adoption in East Africa, underscoring how cloud-based enterprise software and services are expanding into emerging regions.

- October 2025: Adobe Inc. launched its “LLM Optimizer” tool for businesses, designed to help organizations stay competitive in a digital environment increasingly dominated by generative-AI-powered interfaces and content creation ecosystems.

- October 2025: Amazon committed over USD 1.63 billion to its Netherlands operations to expand both its cloud-infrastructure arm and retail technology capabilities, underscoring the convergence of cloud services and retail applications in driving next-gen retail software adoption.

- October 2025: TCS announced the acquisition of US-based ListEngage for USD 72.8 million to strengthen its Salesforce and AI advisory capabilities globally.

- July 2025: Anjani Food & Beverages Lda, a prominent African beverage company, successfully went live with SAP S/4HANA Cloud ERP, implemented by partner SAVIC Inc., marking a significant core-ERP migration to the cloud in a challenging operating context.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of business software and services market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.8% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Offering

By Deployment

By Enterprise Type

By Industry

By Region

|

| Companies Profiled in the Report |

|

Frequently Asked Questions

The market is expected to reach USD 1,523.46 billion by 2034.

In 2025, the market was valued at USD 666.34 billion.

The market is expected to grow at a CAGR of 9.8% during the forecast period.

The BFSI industry holds the leading position in the market.

Rapid adoption of cloud-based solutions drives the market growth.

Microsoft Corporation, SAP SE, Oracle Corporation, Salesforce, Inc., Workday, Inc., Intuit Inc., IBM Corporation, Accenture, Tata Consultancy Services, and Infosys Limited are the top players in the market.

North America dominates by holding the highest market share.

By industry, the healthcare sector is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us