BVLOS UAV Market Size, Share & Industry Analysis, By Platform Type (Fixed-Wing, Rotary-Wing, and Hybrid VTOL UAVs), By Component (Airframe & Structures, Propulsion & Power System, Avionics & Flight Control System, Surveillance & Detect-and-Avoid System, Payloads & Mission Systems, and Others), By Application (Infrastructure Inspection & Utilities, Precision Agriculture, Cargo, Parcel & Medical Delivery, Defense, ISR & Tactical Missions), By End User (Commercial Enterprises, Civil Government & Public Safety Agencies, and Defense & Military Users), and Regional Forecast, 2026-2034

BVLOS UAV Market Size and Future Outlook

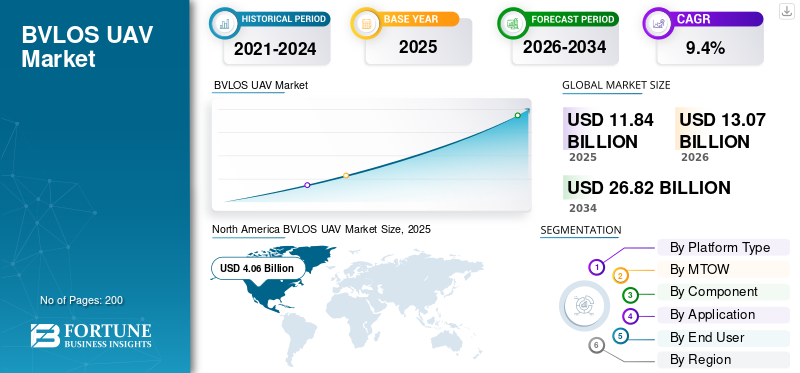

The BVLOS UAV market size was valued at USD 11.84 billion in 2025. The market is projected to grow from USD 13.07 billion in 2026 to USD 26.82 billion by 2034, exhibiting a CAGR of 9.4% during the forecast period. North America dominated the bvlos uav market with a market share of 34.29% in 2025.

The global BVLOS UAV market covers unmanned aerial systems that can operate beyond visual line of sight, rather than remaining within visual line of sight. The market is gaining momentum as demand rises for long-range missions, including infrastructure inspection, environmental monitoring, public safety, and defense surveillance. Additionally, growth is supported by improved regulatory pathways, advanced drone technologies, greater real-time data capabilities, and the need for operational flexibility at a large scale across sectors such as utilities, logistics, and government operations.

Key players in the market include General Atomics, Baykar, Airbus, Leonardo, and IAI. These companies are helping expand BVLOS drone operations through stronger platforms, endurance improvements, and better mission integration. These companies are driving the market by advancing global autonomous BVLOS drone capabilities, strengthening payload and surveillance performance, and supporting wider adoption across defense, commercial, and civil applications.

Download Free sample to learn more about this report.

BVLOS UAV Market KEY TAKEAWAYS

- 2025 Market Size: USD 11.84 billion

- 2026 Market Size: USD 13.07 billion

- 2034 Forecast Market Size: USD 26.82 billion

- CAGR: 9.4% from 2026–2034

- North America dominated the BVLOS UAV market with a 34.29% share in 2025.

- The Hybrid VTOL UAVs segment is projected to grow at the fastest CAGR of 14.2%.

- The 25 kg to 150 kg segment is expected to register the fastest CAGR of 11.5%.

North America

North America Led the market in 2025, supported by strong defense spending and expanding BVLOS regulations.

Asia Pacific

Asia Pacific Expected to witness the fastest growth at a CAGR of 10.7%, driven by rising defense investments and commercial UAV adoption.

Europe

Europe Held a 26.74% share in 2025, supported by strong defense demand and a maturing regulatory framework.

U.S.

U.S. USD 3.66 billion in 2025, growing at a CAGR of 8.3% during the forecast period.

Japan

Japan USD 0.41 billion in 2025, accounting for approximately 14.31% of Asia Pacific revenues.

Read More

BVLOS UAV MARKET TRENDS

Regulatory Normalization of Routine BVLOS Operations is Shaping Market Growth

One of the clearest BVLOS drone market trends is the shift from remote trial activity to a more structured path toward routine operations. The market is no longer shaped solely by platform endurance or payload capability; it is increasingly shaped by how quickly regulators develop workable operating frameworks for BVLOS systems. Once operators get clearer rules, the commercial case for monitoring infrastructure inspection, public safety, logistics, and other long-range missions becomes much stronger. As a result, the market is moving from experimental deployment to operational scaling, which is improving confidence among manufacturers, operators, and end users.

- In August 2025, the Federal Aviation Administration (FAA) unveiled its proposed BVLOS rule, describing it as a framework for safely normalizing beyond visual line of sight drone operations, with detailed requirements covering operations, aircraft manufacturing, separation from other aircraft, authorizations, security, reporting, and recordkeeping.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Long-range, Real-time Surveillance and Infrastructure Monitoring is Driving Market Growth

A major driver of global BVLOS UAV market growth is the rising need for BVLOS-capable platforms that can deliver real-time intelligence for long-range missions without being limited to visual line-of-sight operations. End users demand more from BVLOS drone operations that improve operational flexibility across public safety, emergency response, border surveillance, and infrastructure inspection. In environments where operators need to cover wide geographies at scale, BVLOS plays an important role, as conventional line-of-sight BVLOS missions are restrictive for routine industrial and government use. As a result, demand is shifting toward more advanced drone technologies that can support persistent, data-rich operations over the forecast period.

- In April 2025, the U.K. government announced over USD 8 million to support new flight technologies, including USD 21.3 million for the Civil Aviation Authority to help build the regulatory pathway for drones and routine BVLOS use cases. The linked U.K. BVLOS roadmap specifically highlights priority applications, including the NHS, emergency services, infrastructure surveying, and commercial delivery operations, underscoring that real-world mission demand is driving the market forward.

MARKET RESTRAINTS

Regulatory Complexity and Airspace-Integration Requirements Continue to Restrain Growth

Many BVLOS-capable drones are technologically ready, but the market's growth is restrained by an operating environment, including regulatory frameworks and traffic management systems that are not yet fully ready for BVLOS systems. In Europe, BVLOS-type operations generally fall under a specific category, where operators need an operational authorization from the national authority before flying, while other markets are still building step-by-step pathways toward routine use. That slows commercial-scale-up, delays large-scale deployment, and makes it harder for operators to fully use long-range and real-time mission capabilities across infrastructure, logistics, and public safety use cases.

MARKET OPPORTUNITIES

Expansion of Commercial Delivery, Remote Inspection, and Public-service Corridors is Creating a Major Opportunity

A major market opportunity lies in turning BVLOS capability into repeatable commercial operations, especially in delivery, remote asset inspection, utility monitoring, and emergency response support. The opportunity is significant, as many end users no longer want drones only for pilot projects; they seek BVLOS-capable systems that can operate at scale, generate real-time data, and support long-range missions with greater operational flexibility than conventional visual line-of-sight systems can offer. As regulators open wider pathways for routine BVLOS drone operations, the addressable market becomes much larger for infrastructure operators, logistics providers, healthcare networks, and public agencies. That shift gives the market a strong expansion opportunity over the forecast period; importantly, in the area of monitoring infrastructure inspection and delivery, the economics are already clear.

MARKET CHALLENGES

Testing Setbacks and System Reliability Risks Remain a Major Challenge for Market Growth

A major challenge in the global market is proving consistent system reliability during testing and transition to operational use. Hypersonic programs must operate under extreme thermal stress, high-speed maneuvering, and stringent accuracy requirements, making validation difficult. Even with strong demand for precision strike capability, failed or delayed tests can slow the development and deployment of hypersonic weapon systems and raise insecurity across the hypersonic weapons industry.

- In October 2025, Australia’s Civil Aviation Safety Authority (CASA) launched its broad-area BVLOS trial, allowing operators to plan and fly over larger areas with fewer approvals and greater flexibility. CASA also said the new pathways are likely to support emergency services, agriculture, infrastructure inspection, and environmental monitoring.

Impact of Ongoing Conflicts

Ongoing Conflicts are Accelerating Demand for Persistent Surveillance and Long-range ISR, Driving Market

Ongoing conflicts drive the market by increasing demand for BVLOS-capable systems that can deliver real-time intelligence, surveillance, and tactical awareness in long-range operating environments. In a conflict-driven environment, operators need platforms that can remain airborne longer, cover wider areas beyond visual line of sight, and support border monitoring, force protection, target tracking, and battlefield ISR without relying only on manned assets. This is pushing governments toward higher-value BVLOS UAV procurement, stronger payload integration, and more resilient command-and-control architectures. As a result, conflicts are not just lifting short-term demand, they are also accelerating structural investment in unmanned capability across Europe, the Middle East, and parts of Asia Pacific.

- In April 2025, SIPRI reported that world military expenditure reached USD 2.718 trillion in 2024, with the sharp rise in Europe largely driven by the ongoing Russia-Ukraine war, and in the Middle East by the war in Gaza and wider regional tensions.

Segmentation Analysis

By Platform Type

Fixed-wing Segment Led Market Due to Long-Endurance Mission Capability and Wide-area Surveillance Efficiency

In terms of platform type, the market is categorized into fixed-wing, rotary-wing, and hybrid VTOL UAVs.

The fixed-wing segment dominated the market in 2025 as it is better suited for long-range operations, persistent ISR, border surveillance, maritime monitoring, and large-area monitoring infrastructure inspection missions than rotary-wing platforms. In a BVLOS environment, endurance, coverage radius, and mission economics are more important than hover capability alone, and that gives fixed-wing systems a structural advantage. This is especially true in defense, civil government, and industrial use cases, where operators need BVLOS-capable platforms that can stay airborne longer, cover wider corridors, and deliver more efficient, real-time intelligence over large-scale operating areas.

- In October 2025, OCCAR announced that the Eurodrone program had completed its Critical Design Review (CDR), confirmed the maturity of the system design, and enabled the start of prototype production and ground tests. OCCAR describes Eurodrone as the first fully European MALE RPAS, built for worldwide ISTAR missions, which directly supports the continued dominance of fixed-wing systems in the market.

The Hybrid VTOL UAVs segment is expected to grow at a CAGR of 14.2% over the forecast period.

By MTOW

Above 150 kg Dominated Market Due to Longer Endurance, Payload Capacity, and Mission Suitability for Long-Range ISR Operations

On the basis of MTOW, the market is classified into less than 25 kg, 25 kg to 150 kg, and above 150 kg.

The above 150 kg segment held the largest global BVLOS UAV market share in 2025, as BVLOS missions at the high end are driven by endurance, sensor payload, and insistent coverage rather than compact size alone. Additionally, larger platforms are better suited for long-range surveillance, border security, maritime patrol, defense ISR, and wide-area monitoring infrastructure inspection; in these applications, operators need stronger payload integration and sustained flight performance. As a result, heavier BVLOS-capable systems continue to hold the leading share, especially in defense- and government-led programs where real-time intelligence and multi-mission flexibility are more important than small-platform portability.

The 25 kg to 150 kg segment is expected to grow the fastest, with a CAGR of 11.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Airframe & Structures Dominated Market Due to Their Direct Impact on Endurance, Payload Integration, and Structural Reliability

Based on component, the market is segmented into airframe & structures, propulsion & power system, avionics & flight control system, communication, command & control (C2), navigation, surveillance & detect-and-avoid system, payloads & mission systems, and others.

Airframe & structures dominated the market in 2025, as in BVLOS operations, the platform’s structural design determines aerodynamic efficiency, endurance, payload accommodation, and mission stability. Additionally, for BVLOS-capable systems operating over long-range distances, the airframe is not just a housing element; it is the foundation that enables continuous ISR, wide-area monitoring, infrastructure inspection, and other missions that require reliable performance beyond visual line of sight. As a result, the component continues to hold the leading share, particularly in the fixed-wing and larger UAV categories, where structural efficiency directly affects operational value.

The navigation, surveillance & detect-and-avoid system is the fastest-growing segment and is expected to grow at a CAGR of 12.5% over the forecast period.

By Application

Defense, ISR & Tactical Missions Dominated Market Due to Persistent Surveillance Demand and Higher-value Defense-led Procurement

Based on application, the market is segmented into infrastructure inspection & utilities, mapping & surveying, precision agriculture, cargo, parcel & medical delivery, defense, ISR & tactical missions, and others.

Defense, ISR & tactical missions dominated the market in 2025, as BVLOS UAV adoption is still led by missions that require persistent coverage, secure command-and-control, and real-time intelligence over long-range operating areas. In this market, the highest-value programs are usually tied to border surveillance, battlefield ISR, maritime monitoring, and tactical overwatch rather than short-duration civilian flights. That gives defense-led applications a structural advantage, especially for BVLOS-capable platforms operating beyond visual line of sight, where endurance, payload integration, and mission reliability matter most. Moreover, the continued emphasis on MALE-class and certifiable ISR platforms also reinforces the view that this application segment will remain the largest across the forecast period.

Cargo, parcel & medical delivery is the fastest-growing segment in the market and is expected to grow at a CAGR of 15.4% during the forecast period.

By End User

Defense & Military Users Dominated Market Due to Higher Procurement Intensity and Sustained Defense Modernization

Based on end user, the market is segmented into commercial enterprises, civil government & public safety agencies, and defense & military users.

Defense & military users dominated the market in 2025 as the BVLOS UAV value pool is still led by missions that demand persistent surveillance, secure command-and-control, and long-range coverage rather than short-duration commercial flights. Additionally, military end users are funding larger BVLOS-capable platforms, higher-end payload integration, and more advanced real-time ISR capabilities for operations beyond visual line of sight. That keeps defense demand ahead of civil and commercial adoption, especially in border security, maritime surveillance, tactical overwatch, and broader intelligence missions.

The commercial enterprises segment is expected to show the fastest market growth, registering a CAGR of 11.9% over the forecast period.

BVLOS UAV Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America BVLOS UAV Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Dominates Market Due to Strong Defense-Backed Demand, Early Regulatory Normalization, and Faster Commercial Scaling

North America dominates the market, as the region combines the world’s deepest defense-UAV demand base with the most advanced push toward routine BVLOS-capable operations. The U.S. continues to anchor high-value demand for long-range ISR and tactical systems, while the wider regional ecosystem is also moving faster toward commercial and civil adoption for public safety, logistics, and infrastructure inspection. Additionally, North America leads because it is not relying on a single growth engine; it has military procurement strength, regulatory momentum, and improving operating frameworks for BVLOS drone operations, all working in tandem. SIPRI’s 2024 military expenditure data shows that North America accounted for 38% of global military spending, while the FAA has already initiated formal rulemaking for routine BVLOS integration.

U.S. BVLOS UAV Market

Based on the strong contribution of North America to the market and the dominance of the U.S. within the region, the U.S. market stood at around USD 3.66 billion in 2025, growing at a CAGR of 8.3% over the forecast period.

Europe

Europe remains a major market and held around 26.74% of the global market in 2025, as the region combines high defense demand with a steadily maturing regulatory and industrial base. For this study, Europe includes Russia, which further strengthens the region’s weight in long-endurance ISR, border surveillance, and military-grade unmanned systems. The market is also supported by autonomous platform development, with Eurodrone reaching a major program milestone in October 2025, while the European Union Aviation Safety Agency is continuing to build a structured pathway for BVLOS adoption in higher-risk drone operations.

France BVLOS UAV Market

The market in France reached approximately USD 0.48 billion in 2025, equivalent to around 15.11% of global revenues.

Russia BVLOS UAV Market

Russia's aggressive deployment and testing schedule have put it ahead in the immediate regional race, with its market standing at around USD 0.68 billion in 2025, roughly 21.41% of global revenues.

Asia Pacific

Asia Pacific is one of the most important growth regions in the market and is anticipated to grow at the highest CAGR of 10.7% over the forecast period, as it blends heavy defense demand with expanding opportunities for civil and industrial deployment. SIPRI’s 2024 data shows that Asia and Oceania accounted for USD 629 billion in military expenditure, with China alone accounting for 50% of that regional total, underscoring the scale of long-range surveillance and defense-linked UAV demand. Additionally, countries such as Japan and Australia are reinforcing the region’s operational momentum.

For instance, in November 2024, Japan selected the MQ-9B SeaGuardian for long-endurance maritime missions, and in October 2025, Australia launched its broad-area BVLOS trial to make approvals for wider-area operations more flexible. That mix makes Asia Pacific a region where military modernization and broader expansion of BVLOS use cases are advancing together.

China BVLOS UAV Market

China is experiencing rapid growth, driven by expansion in drone logistics, inspection, and defense, with the drone delivery sector projected to be one of the largest in Asia Pacific. In 2025, revenues stood at around USD 0.99 billion, representing roughly 34.92% of the global sales.

Japan BVLOS UAV Market

The Japanese market in 2025 stood at around USD 0.41 billion, accounting for roughly 14.31% of global revenues.

Rest of the World

The Rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share. Still, it is expected to grow at a CAGR of 8.9% during the forecast period. Defense, border security, and surveillance drive growth in the Middle East & Africa region, while agriculture, utilities, mining, and industrial inspection use cases are more important in Latin America. SIPRI's 2024 data shows that the Middle East spent USD 243 billion on the military, Africa around USD 52.1 billion, and Latin America USD 53.6 billion.

Latin America BVLOS UAV Market

The market in Latin America reached around USD 0.55 billion, accounting for roughly 31.02% of global revenues, in 2025.

Middle East & Africa BVLOS UAV Market

Due to ongoing regional conflicts and the need for advanced precision strike capabilities. The Middle East & Africa market stood at around USD 1.22 billion in 2025 and is expected to reach USD 2.49 billion by 2034, representing roughly 68.98% of global revenues in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Established Defense UAV Leaders and Export-driven Manufacturers are Shaping Market Competition

The global Beyond Visual Line of Sight (BVLOS) UAV market is highly competitive and fragmented, driven by rapid advancements in autonomy, AI, and regulatory approvals. Key industry players are increasingly focused on hybrid airframes, long-endurance platforms, and "drone-in-a-box" (DiaB) solutions for both defense and commercial applications. General Atomics, IAI, Baykar, Airbus, and Leonardo remain among the most important players, as competition centers on platforms capable of supporting long-range surveillance, border security, maritime monitoring, and tactical operations beyond visual line of sight. The market is therefore being shaped less by low-cost drone volume and more by platform reliability, system maturity, and the ability to support complex BVLOS drone operations.

Recent platform and program developments are also driving competitive momentum. Baykar reported USD 2.2 billion in exports in 2025, highlighting its growing international presence, while Airbus announced in June 2025 that the first SIRTAP prototype was ready for ground testing.

LIST OF KEY BVLOS UAV COMPANIES PROFILED

- General Atomics Aeronautical Systems, Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Baykar Technologies (Türkiye)

- Israel Aerospace Industries Ltd. (Israel)

- Elbit Systems Ltd. (Israel)

- Airbus SE (Netherlands)

- Leonardo S.p.A. (Italy)

- Turkish Aerospace Industries, Inc. (Türkiye)

- Boeing Company/Insitu Inc. (U.S.)

- AeroVironment, Inc. (U.S.)

- Safran Electronics & Defense (France)

- Lockheed Martin Corporation (U.S.)

- Parrot Drones SAS (France)

- Quantum-Systems GmbH (Germany)

- Delair SAS (France)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Germany's Federal Office of Bundeswehr Equipment, Information Technology and In-Service Support (BAAINBw) and the NATO Support and Procurement Agency (NSPA), announced the procurement of eight MQ-9B SeaGuardian remotely piloted aircraft systems (RPAS) from General Atomics Aeronautical Systems, Inc.

- October 2025: Elbit Systems announced a contract worth approximately USD 120.00 million to supply Hermes 900 unmanned aerial systems for long-range maritime surveillance to an international customer.

- October 2025: OCCAR announced that Eurodrone had completed its Critical Design Review (CDR), closed the design phase, and cleared the program for prototype production and ground testing; value not disclosed.

- June 2025: Airbus announced that the first SIRTAP prototype had completed assembly and was ready to begin ground testing in Getafe, Spain, with maiden flight planned for late 2025 and first delivery to Spain targeted for 2027; value not disclosed.

- June 2025: The Royal Air Force announced that Protector RG Mk1 had entered service, marking the first remotely piloted air system authorized to fly in U.K. airspace; value not disclosed.

- April 2025: AeroVironment secured a USD 46.60 million contract from the Italian Ministry of Defense for the JUMP 20 VTOL aircraft system, including air vehicles, engineering services, initial sustainment, and onsite technical support.

- February 2025: AeroVironment, through Arcturus UAV, won a contract worth USD 181.00 million from Denmark’s Defense Acquisition and Logistics Organization to deliver the JUMP 20 medium uncrewed aircraft system under a 10-year program of record for the Danish Armed Forces.

REPORT COVERAGE

The global BVLOS UAV market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advances, new product launches, key industry developments, and details on strategic partnerships and mergers & acquisitions. The research report also encompasses a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Platform Type

|

|

By MTOW

|

|

|

By Component

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.84 billion in 2025 and is projected to reach USD 26.82 billion by 2034.

In 2025, the market value in North America stood at USD 4.06 billion.

The market is expected to exhibit a CAGR of 9.4% during the forecast period.

The fixed-wing segment led the market by platform type.

Rising demand for long-range, real-time surveillance and infrastructure monitoring is driving growth.

Key players in the market include General Atomics Aeronautical Systems, Northrop Grumman, Baykar Technologies, Israel Aerospace Industries (IAI), Airbus, and Elbit Systems.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us