Medium Altitude Long-Endurance UAV Market Size, Share & Industry Analysis by Type (Fixed Wing and Hybrid), By Component (Airframe, Avionics, Propulsion Systems, Software, Payload (Camera, Intelligence Payload, Radar, LiDAR, & Gimbal), Ground Control Systems, and Launch & Recovery Systems), By Range (Visual Line of Sight, Extended Visual LOS, and Beyond Visual LOS), By Operation Mode (Remotely Piloted, Semi-Autonomous/Optionally, and Fully Autonomous), By Function/Application (Border Surveillance, ISTAR, Inspection & Monitoring, & Others), By MTOW, By End User, and Regional Forecast, 2026-2034

Medium Altitude Long-Endurance UAV Market Size and Future Outlook

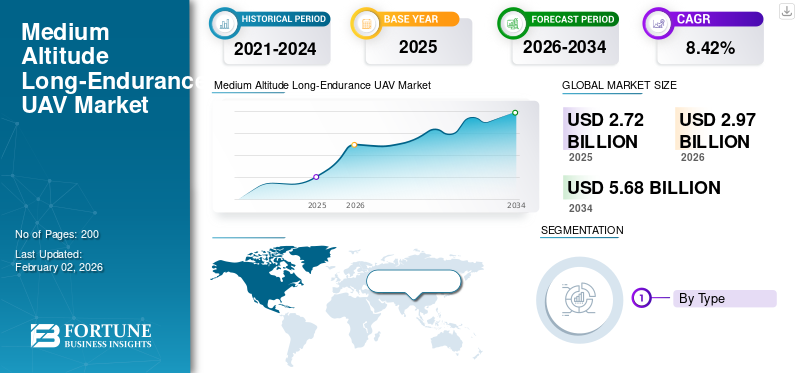

The global medium altitude long-endurance UAV market size was valued at USD 2,724.9 million in 2025. The market is projected to grow from USD 2,970.8 million in 2026 to USD 5,681.3 million by 2034, exhibiting a CAGR of 8.42% during the forecast period. North America dominated the medium altitude long-endurance UAV market with a market share of 41.31% in 2025.

MALE UAV is an unmanned aerial vehicle designed to operate at medium altitudes, typically between 10,000 and 30,000 feet. It can fly for long periods, often 24 hours or more. These UAVs are mainly used for intelligence, surveillance, target acquisition, and reconnaissance (ISTAR) missions. They also support communication relay and combat operations. Their endurance, altitude range, and payload capacity make them important tools for defense and law enforcement around the world. Higher global defense spending, a greater need for surveillance and reconnaissance, and the demand for cost-effective, long-endurance platforms in modern warfare are propelling the global market expansion.

Furthermore, the market encompasses several key players with General Atomics Aeronautical Systems, Baykar Teknoloji, Elbit Systems, and Israel Aerospace Industries at the forefront. This highly dynamic market is anticipated to witness technological advancements from both large multinationals and agile startups.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rising Procurement of MALE UAVs in Military Sector to Boost the Market Growth

The increasing demand for medium altitude long-endurance UAVs from militaries is greatly boosting the global unmanned aerial vehicle (UAV) market. Armed forces are looking for effective solutions for continuous surveillance, target acquisition, and intelligence gathering. MALE UAVs provide a dependable, long-endurance, and affordable option compared to traditional manned platforms. This is leading to their widespread use among defense forces worldwide. For instance, the U.S. Air Force continues to invest in future upgrades to its MQ-9 fleet, providing relevance until future UAV generations come into service. The European powers, with France and Italy taking the lead, Germany, and Spain, have combined resources under the Eurodrone program, focusing on sovereignty and interoperability for NATO.

For instance, in February 2022, Airbus Defence and Space, Dassault Aviation, and Leonardo were jointly awarded a contract by OCCAR (Organisation for Joint Armament Cooperation) to develop the Eurodrone MALE UAV, with a program value estimated at USD 8.2 billion. The move was aimed at delivering a sovereign European UAV capability by 2030.

MARKET RESTRAINTS

High Procurement and Lifecycle Costs May Impede the Market Growth

The high cost of buying and owning MALE UAV systems is significant. Unlike smaller tactical drones, MALE UAVs need complex ground control stations, SATCOM links, ISR payloads, trained personnel, and long-term maintenance contracts. The initial cost of one system, which usually includes a set of four UAVs and ground support, often amounts to hundreds of millions of dollars.

Over their 15–20 year service life, the sustainment and upgrade costs can surpass the initial acquisition cost, particularly when factoring in software updates, spare parts, and new payload integrations. For many developing or mid-tier defense spenders, the cost-benefit tradeoff becomes a sticking point. In contested airspaces, MALE UAVs are exposed to modern surface-to-air missiles (SAMs), electronic warfare (EW), and anti-drone systems.

· For instance, a full MQ-9 Reaper package (4 UAVs + ground control + sensors + support) has been valued around USD 120 to 130 million, making it one of the most expensive MALE UAV systems available.

MARKET OPPORTUNITIES

Indigenous MALE UAV Development for Strategic Autonomy Paves the Way for MALE UAVs Market Growth

India, similar to many countries, is focusing on being self-reliant in defense, especially for technologies considered essential, such as UAVs and the integration of artificial intelligence. The country has historically relied on imports for high-performance drones such as the Israeli Heron TP and the American MQ-9B Predator. However, these platforms are very expensive, require foreign approvals, technology controls, and may come with restricted access to software, sensors, and weapons integration. This creates a huge incentive to develop and field indigenous MALE UAVs.

For instance, the Kaala Bhairav MALE drone, unveiled in 2024 by Bengaluru-based Flying Wedge Defense and Aerospace offers over 30 hours of endurance, integrated artificial intelligence for autonomy, swarming capabilities, and indigenous payload integration. These features make it a direct, cost-effective alternative to foreign drones such as the MQ-9B.

MEDIUM ALTITUDE LONG-ENDURANCE UAV MARKET TRENDS

Strategic Proliferation of Armed MALE UAVs through Export is the Latest Trend in the Market

A growing number of countries are exporting armed MALE UAVs as a tool of foreign policy and defense industrial outreach. Turkey, China, and the UAE are leading this trend by offering cost-effective, combat-tested UAVs with strike capability, especially to countries with denied access to U.S.-made systems such as the MQ-9 Reaper. This is creating a new arms dynamic where middle powers acquire affordable force-multipliers, non-western suppliers gain strategic influence. Conflicts in Africa, the Middle East, and Eastern Europe are increasingly shaped by the presence of armed drones.

MARKET CHALLENGES

Export Restrictions and Political Barriers May Hamper the Market Growth

Tight export control regulations are in place under international regimes such as the Missile Technology Control Regime (MTCR) and national frameworks such as the U.S. ITAR (International Traffic in Arms Regulations). These restrictions are designed to prevent the proliferation of UAVs capable of carrying payloads over 500 kg and ranges exceeding 300 km a category where most MALE UAVs fall. These factors are likely to hinder the medium altitude long-endurance UAV market growth.

Russia Ukraine War Impact

High Defense Expenditure and Economic Impact during the War Affected the MALE UAV Industry

The Russia-Ukraine war has had a complex and multifaceted impact on the medium altitude long-endurance market, primarily through its effects on global supply chains, defense spending, and overall economic conditions. The Russia-Ukraine war has fundamentally reshaped how militaries perceive the utility of MALE UAVs. While these systems were once seen as indispensable for long-endurance ISR and strike, the conflict highlighted their vulnerability against modern air defense and electronic warfare systems. Both sides lost medium-altitude drones to surface-to-air missiles, anti-drone guns, and jamming, pushing militaries to rethink investment strategies.

Hamas and Iran Conflict Impact on the Market

The Israel–Hamas war highlighted the critical role of persistent ISR (Intelligence, Surveillance, and Reconnaissance) and precision strike capabilities in urban and asymmetrical warfare. Regional militaries saw how UAVs can provide round-the-clock surveillance, target acquisition, and precision engagement against irregular forces.

Impact of Tariff War on Supply Chain & Manufacturing

Tariff wars (e.g., U.S.–China trade tensions) increase the cost of critical materials and disrupt global supply chains, strategic re-shoring, and localization. This results in countries imposing tariffs to reduce dependency on foreign defense suppliers. Furthermore, OEMs shift to local manufacturing and joint ventures to bypass tariffs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

High Reliability of Fixed-Wing Long Endurance UAVs in Military Operations Fosters Segmental Growth

On the basis of segmentation by type, the market is classified into fixed wing and hybrid.

The fixed wing segment dominated the global medium altitude long-endurance UAV market share in 2024. Fixed-wing MALE UAVs (e.g., MQ-9 Reaper, Heron TP, Hermes 900, Bayraktar TB2, and Wing Loong II) have been active in service for decades. They are combat-proven in multiple areas (Iraq, Afghanistan, Syria, Libya, Ukraine, and Gaza), giving militaries confidence in reliability and performance. The fixed wing segment is projected to dominate the market with a share of 96.33% in 2026.

The hybrid segment is anticipated to expand at a CAGR of 10.1% over the forecast period.

By Component

Design Innovation, Lifecycles Replacements and Upgrades Fuels the Growth of Airframe Segment

In terms of component, the market is categorized into airframe, avionics, propulsion systems, software, payload, ground control systems, and launch & recovery systems.

The airframe segment captured the largest share of the market in 2024. In 2024, the segment is anticipated to dominate with 26.83% share. It accounts for the largest share of program cost and weight. Most design innovation, including composite structures and modular wings, is focused on the airframe. Additionally, it generates ongoing revenue through lifecycle replacements and upgrades, such as airframe fatigue life extensions, structural health monitoring, and payload hard-point integrations. This makes it the most critical component compared to avionics, propulsion, or payload subsystems. The airframe segment is projected to dominate the market with a share of 26.5% in 2026.

The software segment is expected to grow at the fastest CAGR of 10.8% over the forecast period.

By Range

Higher Operational Efficiency Supported the Growth of the Beyond Visual Line of Sight (BVLOS) Segment

Based on range, the market is segmented into Visual Line of Sight (VLOS), Extended Visual Line of Sight (EVLOS), and Beyond Visual Line of Sight (BVLOS).

The Beyond Visual Line of Sight (BVLOS) segment held the dominating position in the market in 2024. BVLOS operations allow UAVs to be flown well beyond the operator’s visual range, typically enabled through satellite communications (SATCOM), secure datalinks, and autonomous navigation systems. For MALE UAVs, BVLOS is the defining operational mode, unlocking their endurance and strategic value. The beyond visual LOS (BVLOS) segment is expected to lead the market, contributing 78.59% globally in 2026.

To know how our report can help streamline your business, Speak to Analyst

The EVLOS segment is poised to grow at a CAGR of 7.9% over the forecast period.

By Operation Mode

Remotely Piloted Segment to Grow with Need for Solutions with High Situational Awareness

Based on operation mode, the market is segmented into remotely piloted, semi-autonomous/optionally, and fully autonomous.

The remotely piloted segment held the dominating position in 2024. In defense operations, remotely piloted systems such as the MQ-9 Reaper, Bayraktar TB2, and Wing Loong II remain the backbone of global medium altitude long-endurance UAV fleets. They provide militaries with high situational awareness and real-time control, which is essential in contested environments where autonomous decision-making may not yet be trusted. The remotely piloted segment will account for 88.04% market share in 2026.

The fully-autonomous segment is set to flourish with a growth rate of 11.3% during the forecast period.

By Function/Application

ISTAR Segment Leads with Rising Deployment for Border Security Applications

Based on function/application, the market is segmented into border surveillance, intelligence, surveillance, target acquisition & reconnaissance (ISTAR), inspection & monitoring, surveying & mapping, swarm technologies, search & rescue, and communication relay.

The intelligence, surveillance, target acquisition & reconnaissance (ISTAR) segment dominated the global medium altitude long-endurance UAV market in 2024. The segment accounted for 53.17% market share in 2024. MALE UAVs are increasingly deployed for persistent border security and monitoring cross-border activities, leveraging long endurance and wide-area coverage. Their ability to carry EO/IR, radar, and SIGINT payloads allows the detection of unauthorized crossings, smuggling, and infiltration attempts, resulting in the dominance of this segment.

The swarm technologies segment is set to flourish with a growth rate of 10.8% during the forecast period.

By MTOW

Heavy-Weight (Above 550 kg) Segment to Lead Due to its Wide Range of Applications

By MTOW, the market is fragmented into light-weight (below 100 kg), medium-weight (100 - 550 kg), and heavy-weight (above 550 kg).

The heavy-weight (above 550 kg) segment dominated the global market in 2024 and is anticipated to be the fastest growing segment during the forecast period. The segment accounted for 49.06% market share in 2024. The segment is dominant as most combat-proven platforms fall into this category. With endurance of 20-40+ hours, payloads up to several hundred kilograms, and altitudes of 25,000-30,000 ft., these UAVs serve as the backbone of strategic ISR and strike operations, resulting in the segment’s fast pace growth.

The medium-weight (100 - 550 kg) segment is anticipated to be second-fastest growing segment with a CAGR of 8.7% during the forecast period

By End User

Rise in UAV Adoption for Long-range Targeting and Monitoring Pushed the Leadership of the Military Segment in 2024

Based on end user, the market is segmented into military, commercial, and homeland security & government agencies.

The military segment dominated the global medium altitude long-endurance UAV market in 2024. The segment accounted for 86.99% market share in 2024. The military sector is the largest and most established user of MALE UAVs. They use these drones for their endurance, altitude, and payload capacity in missions such as intelligence, surveillance, reconnaissance (ISR), precision strike, and electronic warfare. Militaries focus on MALE UAVs for ongoing monitoring, battlefield awareness, and long-range targeting. They often deploy these drones in challenging environments. This has led to their dominance in the segment.

The homeland security & government agencies segment is set grow at a CAGR of 9.9% over the forecast period.

Medium Altitude Long-Endurance UAV Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, the Middle East, and the rest of the World.

North America

North America Medium Altitude Long-Endurance UAV Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 1.05 billion in 2025, representing 38.41% of total market revenue, and is projected to reach USD 1.14 billion in 2026. The North America held the leading share in 2023, valuing at USD 886.1 million, and also recorded the dominating share in 2024 with USD 965.1 million. North America leads the MALE UAV market due to the U.S.’s high defense spending and early adoption. The country has a strong industrial base and research and development ecosystem. It also has solid SATCOM/C4ISR infrastructure, accessible test ranges, and effective export channels to allied nations. In 2025, the The U.S. market is valued at USD 920 million by 2026.

Europe, Asia Pacific, and the Middle East

Other regions such as Europe, Asia Pacific, and the Middle East are expected to see significant growth in the medium altitude long-endurance UAV market in the coming years. During the forecast period, the Asia Pacific region is projected to have a growth rate of 10.7%, which is the highest among all regions. This growth is mainly due to increased investment in unmanned aerial vehicles for military use. The Japan market is forecast to attain USD 60 million by 2026, the China market is set to reach USD 420 million by 2026, and the India market is anticipated to achieve USD 190 million by 2026.

Following Asia Pacific, the market in Europe contributed approximately USD 0.54 billion to the global market in 2025, accounting for 19.77% share, and is expected to reach USD 0.58 billion in 2026. In this region, both the the UK market is expected to reach USD 130 million by 2026, while the Germany market is assessed at USD 120 million by 2026. Middle East & Africa maintained a strong presence in the global market, reaching USD 0.24 billion in 2025, accounting for 5.06% share, and is expected to reach USD 0.26 billion in 2026. In 2025, the Asia Pacific market stood at USD 0.77 billion, representing 28.09% of global demand, and is projected to grow to USD 0.85 billion in 2026.

Rest of the World

Rest of the World recorded a market size of USD 0.14 billion in 2025, capturing 8.68% of the global market share, and is projected to reach USD 0.15 billion in 2026. Over the forecast period, the market in the rest of the world (Africa and Latin America) is expected to experience moderate growth. This expansion is driven by ongoing defense modernization and border security needs. However, it faces challenges from budget limitations, export controls, and infrastructure gaps.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Emphasize Localization and Software Updates to Maintain their Market Share

The MALE UAV market is dominated by a few key players, with a tiered regional structure. Global leaders and emerging challengers compete on endurance, SATCOM/BLOS connectivity, multi-payload integration, and lifecycle support. Established companies such as General Atomics (U.S.) and Israel’s IAI and Elbit benefit from large installed bases, reliable C4ISR ecosystems, and software-driven upgrades. Meanwhile, Baykar and TAI (Türkiye), Leonardo (EU), and EDGE/ADASI (UAE) grow by using cost-benefit advantages and localization agreements. Chinese firms such as AVIC/CAIG and CASC have a strong advantage due to domestic medium altitude long-endurance UAV market demand and government-supported exports.

Export regulations (ITAR/non-ITAR), interoperability needs in alliances, and technology transfer offers affect market access. These factors create significant entry barriers linked to certification, secure communications accreditation, and support networks. In short, successful companies combine durability and reliable communications with quick software updates and attractive localization and offset packages.

LIST OF KEY MEDIUM ALTITUDE LONG-ENDURANCE UAVS COMPANIES PROFILED

- General Atomics Aeronautical Systems (U.S.)

- Baykar Teknoloji (Türkiye)

- Elbit Systems Inc. (Israel)

- Northrop Grumman Corp. (U.S.)

- Leonardo S.p.A (Italy)

- Aviation Industry Corporation of China (China)

- Thales Group (France)

- EDGE Group / ADASI (UAE)

- Israel Aerospace Industries (IAI) (Israel)

- Hinaray Technology Co., Ltd (China)

- AeroVironment Inc. (U.S.)

- Turkish Aerospace Industries (Türkiye)

- China Aerospace Science and Technology Corporation (China)

KEY INDUSTRY DEVELOPMENTS

- In December 2023, the Government of Canada awarded General Atomics Aeronautical Systems (GA-ASI) a contract worth USD 1.86 billion to supply 11 MQ-9B SkyGuardian RPAS, certified ground control stations, and support.

- In June 2023, the Government of Kuwait awarded Baykar a contract worth USD 367 million to supply Bayraktar TB2 MALE UAVs including training, ground control stations, and support.

- In February 2023, Indonesia’s Ministry of Defence awarded Turkish Aerospace Industries (TAI) a contract worth USD 300 million to procure 12 Anka MALE drones with training and support.

- In April 2023, Romania’s Ministry of National Defense awarded Baykar a contract worth USD 321 million to supply three Bayraktar TB2 systems (18 aircraft) with training, munitions, and support.

- In September 2022, Thailand awarded Elbit Systems a contract worth USD 120 million to supply Hermes 900 Maritime UAS and training capabilities.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size, company profiling, and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.42% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation

|

Type, Component, Range, Operation Mode, Function/Application, MTOW, End User |

|

By Type

|

|

|

By Component

|

|

|

By Range

|

|

|

By Operation Mode

|

|

|

By Function/Application

|

|

|

By MTOW

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2,724.9 million in 2025 and is projected to reach USD 5,681.3 million by 2034.

In 2025, the North America market value stood at USD 1050 million.

The market is expected to exhibit a CAGR of 8.42% during the forecast period of 2026-2034.

In 2025, the fixed wing segment led the market by type.

The growing procurement of MALE UAVs in the military sector is a key factor boosting the market expansion.

General Atomics Aeronautical Systems, Baykar Teknoloji, Elbit Systems Inc., Leonardo S.p.A, Aviation Industry Corporation of China, EDGE Group/ADASI, Israel Aerospace Industries (IAI), Turkish Aerospace Industries, and China Aerospace Science and Technology Corporation are some of the prominent players in the market.

North America dominated the market with a share of 38.41% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us