Carbon Fiber Reinforced Plastic Market Size, Share & Industry Analysis, By Type (Polyacrylonitrile (PAN) and Petroleum Pitch), By Resin Type (Thermosetting and Thermoplastic) By Application (Automotive, Electronics, Aerospace, Wind Turbines, Sports Equipment, Construction, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

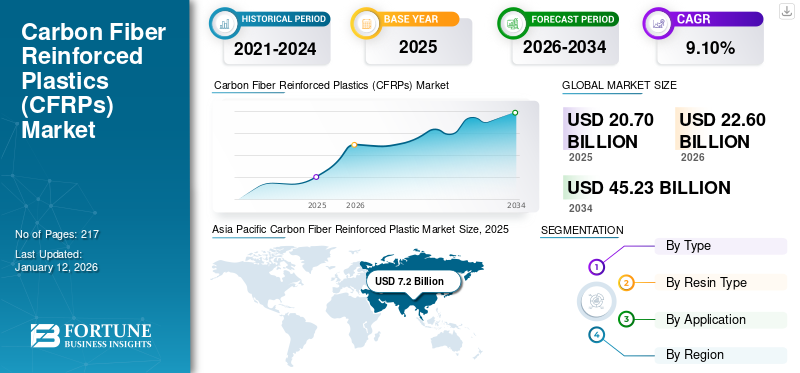

The global carbon fiber reinforced plastic market size was valued at USD 20.7 billion in 2025 and is projected to grow from USD 22.6 billion in 2026 to USD 45.23 billion by 2034 at a CAGR of 9.1% during the forecast period. Asia Pacific dominated the carbon fiber reinforced plastic market with a market share of 35% in 2025.

Carbon Fiber Reinforced Plastic (CFRP) is a composite material combining carbon fibers with a polymer matrix, typically epoxy resin, creating a lightweight yet extremely strong material for high-performance applications. The market growth is driven by its superior strength-to-weight ratio and diverse applications across industries such as aerospace, automotive, wind energy, and construction. Key players in the market are Hexcel Corporation, Toray Industries, SGL Carbon, Mitsubishi Chemical, and Solvay.

Download Free sample to learn more about this report.

GLOBAL CARBON FIBER REINFORCED PLASTIC (CFRP) MARKET OVERVIEW

Market Size & Forecast:

- 2025 Market Size: USD 20.7 billion

- 2026 Market Size: USD 22.6 billion

- 2034 Forecast Market Size: USD 45.23 billion

- CAGR: 9.1% from 2026–2034

Market Share:

- Asia Pacific dominated the market in 2025 with a 35% share, rising from USD 7.2 billion in 2025 to USD 7.9 billion in 2026.

- By type, PAN-based CFRP led due to strong mechanical properties and affordability.

- By resin, thermosetting held the largest share for its durability and aerospace usage.

- By application, aerospace remained the top segment, while wind turbines are projected to hold 9.4% share in 2024.

- In China, wind turbines alone are expected to account for 12.7% of the market in 2024.

Key Country Highlights:

- China: Strong wind energy deployment pushes wind turbine segment to 12.7% share in 2024.

- United States: High demand from aerospace, EVs, and infrastructure boosts CFRP usage.

- Germany: EV production and lightweighting regulations support steady growth.

- Japan: Advanced manufacturing and aerospace applications sustain market demand.

- Middle East & Africa: Growth supported by infrastructure and industrial expansion.

Carbon Fiber Reinforced Plastic Market Trends

Emission Regulations and Electric Vehicle Growth Propel Adoption in Automotive Manufacturing

The automotive industry is rapidly accelerating the adoption beyond premium vehicles into mainstream models. This shift is driven by stringent emissions regulations demanding aggressive light-weighting strategies and the electric vehicle boom requiring high-performance structural components. Manufacturing innovation in rapid-cure resins and automated fiber placement has dramatically reduced production cycle times, while increasing production volumes are gradually bringing costs down. These advancements position it as a strategic material solution for next-generation vehicles, balancing performance and sustainability requirements. Asia Pacific witnessed a carbon fiber reinforced plastics market growth from USD 5.88 Billion in 2023 to USD 6.50 Billion in 2024.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Aerospace Innovation Coupled with Weight Reduction Leads to Soaring Fuel Efficiency, Drive Demand

The aerospace sector is a primary driver of the high demand for carbon fiber reinforced plastic, with several key factors fueling this growth. Commercial aircraft manufacturers are increasingly incorporating carbon fiber reinforced plastic into their designs, with modern aircraft such as the Boeing 787 and Airbus A350 using up to 50% composite materials by weight. This trend is driven by the material’s exceptional strength-to-weight ratio, which significantly reduces aircraft weight and makes it fuel-efficient.

The focus on fuel efficiency is particularly crucial as airlines seek to reduce operating costs and meet stricter environmental regulations. Each kilogram of weight reduction in an aircraft can lead to substantial fuel savings over its operational lifetime. Its durability also means lower maintenance requirements and longer service life compared to traditional materials.

In the defense sector, military modernization programs are driving adoption in fighter aircraft, Unmanned Aerial Vehicles (UAVs), and military transport vehicles. The carbon fiber reinforced fiber plastic’s high strength and impact resistance make it ideal for military applications where performance is critical. Additionally, the growing space exploration sector, including satellite manufacturing and launch vehicles, relies heavily on CFRP to meet strict weight requirements while maintaining structural integrity in extreme conditions.

MARKET RESTRAINTS

High Production Cost and Technical Complexities Hinders Market Growth

High production costs present a major barrier to the carbon fiber reinforced plastic market growth, with raw material expenses being a primary concern. The carbon fiber itself accounts significant share of the total cost in CFRP, while specialized manufacturing processes and equipment add significant overhead. The energy-intensive nature of carbon fiber production, requiring precise temperature control and specialized ovens, further drives up costs. This makes carbon fiber reinforced plastic less accessible for mass-market applications.

Technical limitations also pose significant challenges. The complex repair procedures require specialized knowledge and equipment, often making repairs expensive and time-consuming. Quality control issues during manufacturing can lead to inconsistencies in the final product, affecting reliability and performance.

MARKET OPPORTUNITIES

EV Battery & High Performance Cars Spark Innovations

High-performance and electric vehicles are creating significant opportunities for the market through multiple avenues. In high-performance vehicles, carbon fiber reinforced plastic’s exceptional strength-to-weight ratio enables manufacturers to achieve superior acceleration, handling, and fuel efficiency. The material’s ability to be molded into complex shapes also allows for aerodynamic designs that enhance vehicle performance, making it increasingly popular in premium and sports goods segments.

In the electric vehicle sector, it plays a crucial role in offsetting battery weight. As EVs carry heavy battery packs, reducing weight in other components becomes essential for extending the range and improving efficiency. Manufacturers are incorporating CFRP in body panels, chassis components, and battery enclosures. The material’s high strength also provides excellent crash protection, addressing safety concerns in EVs.

The growing demand for both vehicle segments is driving innovations in carbon fiber reinforced plastic manufacturing processes, leading to more cost-effective production methods. This trend is particularly significant as automakers scale up their electric vehicle production, creating a sustained demand for lightweight materials.

MARKET CHALLENGES

CFRP Recycling Complexity Threatens Market Growth as Environmental Standards Tighten

The recycling technology of carbon fiber reinforced plastic materials presents a major technical challenge due to the intricate bonding between carbon fibers and polymer matrices. Current separation processes require intensive energy consumption and specialized equipment, leading to high operation costs that make recycling economically unfeasible for many manufacturers.

Furthermore, the recovered carbon fibers often suffer from reduced mechanical properties and inconsistent quality, limiting their application in high-performance products. This creates a significant barrier for companies striving to meet growing sustainability requirements and circular economy goals.

Trade Protectionism & Geopolitical Dynamics

Rising trade protectionism has significantly disrupted the market, with major economies implementing tariffs, local content requirements, and enhanced security of foreign investments in advanced materials, imposing substantial tariffs on Chinese-origin products while expanding domestic manufacturing incentives through the Inflation Reduction Act. Similarly, the European Union has strengthened anti-dumping measures against Asia carbon fiber producers while providing substantial subsidies for regional manufacturing capacity expansion.

Intensifying geopolitical tensions have transformed the market through export controls restricting technology transfer between China and Western economies. China’s self-sufficiency initiatives target both domestic needs and developing markets, creating parallel technology paths and diverging standards globally.

SEGMENTATION ANALYSIS

By Type

Polyacrylonitrile (PAN) Segment Dominated Market Owing to Its Use in Wide Range of Automotive and Aerospace Applications

Based on type, the market is classified into Polyacrylonitrile (PAN) and petroleum pitch.

Polyacrylonitrile (PAN) based carbon fibers is expected to hold dominant carbon fiber reinforced plastic market share of 98.32% in 2026, driven by their optimal balance of performance and cost. PAN-based fibers offer excellent mechanical properties, including high tensile strength and modulus, making them suitable for a wide range of applications from automotive to aerospace. The manufacturing process for PAN-based fibers is well-established, leading to more consistent quality and better supply chain reliability. The lower production costs compared to pitch-based fibers have made PAN the preferred choice for mass-market applications.

- The wind turbines segment is expected to hold a 9.4% share in 2024.

Petroleum pitch-based carbon fibers, while occupying a smaller market share, serve crucial roles in specialized applications where thermal management is critical. These fibers exhibit superior thermal conductivity and high modulus, making them ideal for aerospace and high-performance industrial applications. The higher cost of pitch-based fibers has limited their widespread adoption, but they maintain a strong position in niche markets where their unique properties justify the premium price point.

By Resin Type

Thermosetting to Dominate Market Owing to Their Superior Mechanical Properties and Established Processing Techniques

Based on resin type, the market is classified into thermosetting and thermoplastic.

Thermosetting resins will maintain their leadership position in the market with share of 89.55% in 2026, primarily due to their superior mechanical properties and established processing techniques. The aerospace industry heavily relies on thermosetting CFRP for structural components, while the wind energy sector utilizes these materials for blade manufacturing due to their durability and fatigue resistance.

Thermoplastic resins are experiencing rapid growth in the market, driven by increasing demand for recyclable and sustainable materials. These resins offer advantages in terms of faster processing times, better impact resistance, and the ability to be remolded and recycled. The automotive industry is particularly interested in thermoplastic CFRP due to its potential in high-volume manufacturing and end-of-life vehicle recycling. The development of new thermoplastic matrices with improved properties is further accelerating adoption across various sectors.

By Application

To know how our report can help streamline your business, Speak to Analyst

Aerospace Holds Largest Market Share Due to High Demand for Lightweight Materials in Aircraft Manufacturing

In terms of application, the market is segmented into automotive, electronics, aerospace, wind turbines, sports equipment, construction, and others.

The aerospace sector is projected to represent the highest value segment in the market with share of 55.29% in 2026, driven by the critical need for lightweight materials in aircraft manufacturing. CFRP's high strength-to-weight ratio and excellent fatigue resistance make it indispensable in both commercial and military aircraft. The increasing focus on fuel efficiency and reduced emissions continues to drive adoption in new aircraft programs, with applications ranging from primary structures to interior components.

In the wind turbines industry, the material's high strength and stiffness enable the production of longer, more efficient wind turbine blades. As countries push for renewable energy adoption, the demand for larger wind turbines is driving increased consumption. Manufacturers are focusing on optimizing design and production processes to reduce costs while maintaining performance.

The automotive sector continues to be one of the major adopters. As manufacturers transition toward EVs and seek to reduce vehicle weight, it is increasingly used in battery enclosures, structural supports, body panels, and crash structures. Europe leads in lightweighting and emissions compliance, especially among luxury brands such as BMW and Audi. Asia Pacific, especially China, is scaling up CFRP use in high-volume EV platforms.

CARBON FIBER REINFORCED PLASTIC MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Carbon Fiber Reinforced Plastic Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 35.00% to the global market in 2025, with a valuation of USD 7.2 billion, and is projected to reach USD 7.9 billion in 2026. The region presents the fastest-growing market, led by China’s government-backed expansion of domestic carbon fiber manufacturing capacity and application development. The region is characterized by rapidly developing aerospace sectors, including China’s COMAC program and Japan’s established aerospace manufacturing. The region leads in cost-competitive manufacturing approaches aimed at expanding CFRP accessibility beyond premium applications. Wind energy creates massive demand volumes, with China representing the world’s largest wind turbine market. The region's sporting goods manufacturing, both for domestic consumption and export markets, maintains consistent product demand. Industrial automation applications are expanding rapidly, particularly in Japan, South Korea, and increasingly in China. The Japan market is projected to reach USD 1.03 billion by 2026, the China market is projected to reach USD 5.38 billion by 2026, and the India market is projected to reach USD 0.36 billion by 2026.

- In China, the wind turbines segment is estimated to hold a 12.7% market share in 2024.

To know how our report can help streamline your business, Speak to Analyst

North America

In 2025, North America represented USD 6.7 billion, accounting for 32.00% of the worldwide market, and is projected to grow to USD 7.2 billion in 2026. North America’s demand is primarily driven by the aerospace sector, with Boeing’s commercial aircraft programs and defense platforms requiring significant volumes of aerospace-grade carbon composites. The region is leading in recycling technology development, addressing end-of-life concerns. Recent infrastructure investment legislation is opening new civil engineering applications across bridges, buildings, and transportation infrastructure. In the U.S., growing demand for lightweight vehicles, and increasing aerospace requirements for high-strength materials are driving the product consumption. Carbon neutrality goals and sustainable technology advancements further accelerate adoption across industries. The U.S. market is projected to reach USD 6.65 billion by 2026.

Europe

The Europe market generated USD 5.4 billion in 2025, representing 26.00% of the global market landscape, and is expected to reach USD 5.8 billion in 2026. Europe maintains a strong position in the market, driven by its advanced automotive and aerospace industries. Strict emissions regulations have accelerated the adoption of lightweight materials, while the region's leadership in wind energy continues to drive demand. European manufacturers are at the forefront of developing innovative CFRP applications and processing technologies. The UK market is projected to reach USD 0.69 billion by 2026, and the Germany market is projected to reach USD 1.4 billion by 2026.

Latin America

The market in Latin America reached USD 1.1 billion in 2025, representing 5.00% of total market revenue, and is projected to reach USD 1.2 billion in 2026. Latin America's market is showing steady growth driven by emerging automotive manufacturing and renewable energy sectors. Infrastructure modernization projects and increasing industrial development are creating new opportunities for CFRP applications. The region's growing focus on sustainable development is expected to drive further adoption of advanced materials such as CFRP.

Middle East & Africa

The Middle East & Africa market was valued at USD 0.4 billion in 2025, capturing 2.00% of global revenue, and is estimated to reach USD 0.5 billion in 2026. The Middle East & Africa region shows promising growth potential, primarily driven by infrastructure development and increasing industrial applications. Government investments in the aerospace and construction sectors are creating new opportunities for CFRP adoption. The region's focus on economic diversification is expected to drive product demand further.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Strategic Investment and Partnerships Drive Innovation and Growth in the Market

CFRP market players are focusing on adopting various strategic initiatives. Hexcel Corporation is expanding its manufacturing capacity for aerospace demand. Toray Industries has strengthened its automotive segment through partnerships with major OEMs. SGL Carbon is investing in thermoplastic CFRP technologies and recycling solutions. Mitsubishi Chemical has focused on wind energy applications through new product developments. Solvay has emphasized aerospace qualification of new materials and automotive partnerships for EV applications. Key players in the market are Hexcel Corporation, Toray Industries, SGL Carbon, Mitsubishi Chemical, and Solvay.

LIST OF KEY MARKET PLAYERS PROFILED IN THE REPORT

- Hexcel Corporation (U.S.)

- TORAY INDUSTRIES, INC. (Japan)

- SGL Carbon (Germany)

- Mitsubishi Chemical Group Corporation. (Japan)

- TEIJIN LIMITED. (Japan)

- Solvay (Belgium)

- Formosa Plastics (Taiwan)

- DowAksa (Turkey)

- Zhongfu Carbon Fiber Core Cable Technology Co., Ltd (China)

- HS HYOSUNG ADVANCED MATERIALS (South Korea)

KEY INDUSTRY DEVELOPMENTS

- March 2025: Hexcel and FIDAMC have partnered to advance composite materials for aerospace and industrial applications. Their collaboration focuses on developing innovative manufacturing processes to enhance lightweight, high performance composites. This partnership aims to improve efficiency and sustainability in composite production.

- November 2024: Toray advanced composites expanded its thermoplastic composites portfolio by acquiring Gordon Plastics assets in Colorado. The new 47,000 sq.ft facility enhances R&D and scalable production of high-performance composite tapes for aerospace, sports, oil & gas, and industrial markets.

- October 2024: Hexcel is advancing high-rate composite manufacturing for aerospace, focusing on automation, cost efficiency, and next-gen aircraft, including single-aisle planes, AAM vehicles, and high-performance materials.

- January 2024: SGL Carbon introduced a climate-friendly carbon fiber that reduces CO2 emissions by up to 50% compared to conventional fibers. This significant reduction is achieved through the use of renewable energy sources at their production facilities.

- February 2023: Toray Industries announced the development of a rapid integrated molding technology for Carbon Fiber Reinforced Plastic (CFRP) components in mobility applications. This innovation significantly reduces molding time, enhancing production efficiency for the automotive and aerospace industries.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, types, compositions used to produce these products, and end-use industries of the product. Besides this, it offers insights into the market and current industry trends, and highlights key industry developments. In addition to the factors mentioned above, it encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) and Volume (Kiloton) |

|

Growth Rate |

CAGR of 9.1% from 2026 to 2034 |

|

Segmentation |

By Type

|

|

By Resin Type

|

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 22.6 billion in 2026 and is projected to record a valuation of USD 45.23 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 7.2 billion.

Recording a CAGR of 9.1%, the market will exhibit steady growth during the forecast period.

The aerospace application is the leading segment in the market.

The automotive industrys evolution propels the growth of the market.

Asia Pacific held the highest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 217

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us