Cardiac Leads Market Size, Share & Industry Analysis, By Product (Pacing Leads, Defibrillation (ICD) Leads, and Cardiac Resynchronization Therapy (CRT) Leads), By Type (Active Fixation Leads and Passive Fixation Leads), By End-user (Hospitals and ASCs, Specialty Clinics, Cardiac Catheterization Laboratories, and Others), and Regional Forecast, 2026-2034

Cardiac Leads Market Size and Future Outlook

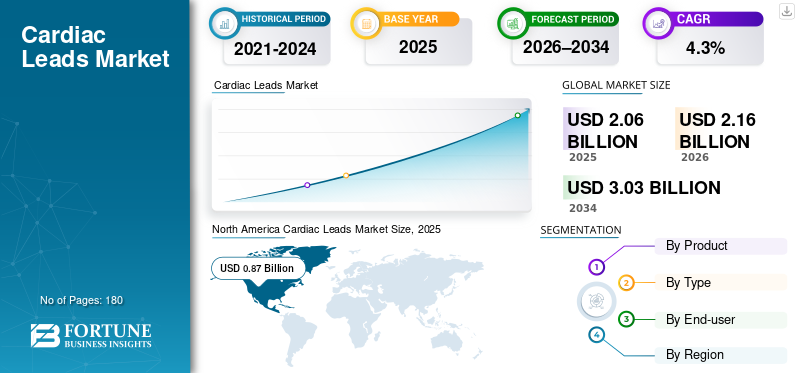

The global cardiac leads market size was valued at USD 2.06 billion in 2025. The market is projected to grow from USD 2.16 billion in 2026 to USD 3.03 billion by 2034, exhibiting a CAGR of 4.3% during the forecast period. North America dominated the global cardiac leads market with a market share of 42.23% in 2025.

Cardiac leads are thin, insulated wires that connect implantable cardiac rhythm devices (pacemakers, ICDs, and CRT systems) to the heart, enabling sensing and delivery of pacing or defibrillation therapy. Demand is rising as hospitals manage a growing pool of patients with arrhythmias and advanced heart disease, alongside longer life expectancy, which increases the lifetime likelihood of needing rhythm support. In day-to-day practice, leads are also being used in more targeted pacing strategies that aim to restore physiological conduction, which can expand the addressable implant base and drive replacement/upgrade cycles. As a practical indicator of the clinical need behind the market, the CDC notes atrial fibrillation is the most commonly treated arrhythmia.

- For instance, according to a Centers for Disease Control and Prevention report published in May 2024, 12.1 million people in the U.S. will have AFib by 2050.

Furthermore, Medtronic plc, Abbott, Boston Scientific, and BIOTRONIK SE & Co. KG held the largest market share, driven by growing investments and calculated initiatives, such as new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

CARDIAC LEADS MARKET TRENDS

Targeted Therapy Delivery, Slimmer Profiles, and Alternative Lead Pathways to Boost Overall Market

The trend line is clear that lead technology is being shaped around precision placement, long-term durability, and flexibility for emerging implant approaches. One visible direction is smaller-diameter or catheter-delivered lead concepts intended to support accurate placement while maintaining defibrillation performance.

In parallel, manufacturers are investing in solutions that aim to reduce the traditional pain points of transvenous leads, such as venous obstruction, lead infection, and complex revision burden, by exploring extravascular approaches. Taken together, these developments signal a market that’s still fundamentally “lead-based,” but increasingly segmented by technique, pathway (transvenous vs extravascular), and the infrastructure needed to support implantation and follow-up.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Arrhythmia Burden and Procedure Volumes are Pulling Lead Demand Upward

The strongest tailwind is the steady rise in treated rhythm disorders and advanced cardiovascular disease, which translates into more implants and more replacements. Atrial fibrillation, bradyarrhythmias, and ventricular arrhythmias climb sharply with age, and the addressable population keeps expanding as survival improves after myocardial infarction and heart failure admissions. As implant capacity expands, leads benefit directly as they are “per-procedure” consumables, a typical CRT implant uses multiple leads, and complex upgrades often require additional lead work. In Europe, the ESC Atlas continues to highlight the scale of device therapy and the gap between countries, with high-income settings reporting much higher pacemaker implantation rates than middle-income settings, reinforcing that procedure expansion remains a meaningful lever for growth.

MARKET RESTRAINTS

Lead-related Complications and Lifetime Management Risks to Limit Market Growth

Leads are durable but not permanent. Over a patient’s lifetime, they can fracture, dislodge, fail electrically, or become a nidus for infection, risks that rise with multiple revisions and long dwell times. These clinical realities create a “hesitation factor” in borderline cases, especially when patients are young, have high infection risk, or may require multiple future generator changes. The compliance and vigilance burden is also real, as device- and system-safety actions can disrupt implant schedules, trigger additional follow-up, and heighten hospital scrutiny of vendor selection.

- For example, the FDA issued a Class I recall for certain Medtronic ICD and CRT-D devices in July 2023, highlighting the critical importance of reliability when high-voltage therapy is needed.

Even when the issue is not the lead itself, such events raise the bar for documentation, post-market surveillance, and shared decision-making, often slowing conversions and extending procurement cycles. Separately, clinical teams must weigh the downstream complexity of lead extraction, which is technically demanding and concentrated in specialist centers; this can influence physician preference toward strategies that minimize future lead burden, especially in health systems with constrained access to extraction expertise.

MARKET OPPORTUNITIES

Conduction System Pacing and Next-Generation Lead Designs to Create Significant Growth Opportunities

A major opportunity sits in the shift toward Conduction System Pacing (CSP), including left bundle branch area pacing, where clinicians seek more physiological activation than traditional right ventricular pacing. As CSP becomes routine in more centers, there is incremental demand for leads designed or labeled to support these techniques, both in new implants and in upgrades.

As more electrophysiology labs gain confidence in these workflows, manufacturers have room to win share through “procedure-enabling” ecosystems (leads, delivery tools, training, and evidence). Over time, this can expand the eligible population, particularly patients who may have been borderline candidates for standard pacing due to concerns about pacing-induced cardiomyopathy, supporting higher-value lead mixes and more frequent upgrades.

MARKET CHALLENGES

Access Gaps, Training Intensity, and Reimbursement Variability to Hinder Market Growth

The availability of implant-capable centers, trained electrophysiologists, and stable reimbursement for device therapy ultimately constrains cardiac lead demand. Even within advanced health systems, therapy adoption can be uneven, driven by hospital budgets, catheterization/EP lab capacity, and regional referral patterns. The ESC Atlas continues to document disparities in cardiovascular service provision and device implantation rates, with large differences between higher- and middle-income settings, which is a practical reminder that clinical need does not automatically translate into procedures.

Another challenge is the learning curve: CSP and complex CRT workflows can be operator-dependent, and scaling them requires structured training plus consistent access to imaging, delivery tools, and technical support. Finally, long-term follow-up creates an operational burden, including device checks, remote monitoring workflows, and management of suspected lead issues, all of which matter to hospitals under staffing pressure. Demographics will keep pushing demand upward, but translating that demand into implants depends on health-system throughput; the UN’s World Population Prospects 2024 underlines that population aging is a structural force, yet the ability to deliver high-quality EP care will remain uneven across regions.

Segmentation Analysis

By Product

Large Install Base of Pacing Leads to Drive Segment Growth

Based on product, the market is segmented into pacing leads, defibrillation (ICD) leads, and Cardiac Resynchronization Therapy (CRT) leads.

Pacing leads typically hold the largest cardiac leads market share as they anchor the biggest installed base, standard pacemakers remain widely used for bradycardia, AV block, and sinus node dysfunction, and pacing capability also underpins many ICD and CRT implants. Clinically, pacing is often the “first-line implant” for rhythm support, so volumes are resilient even when higher-end therapies face tighter reimbursement or limited specialist capacity.

Additionally, the Cardiac Resynchronization Therapy (CRT) leads segment is projected to grow at a CAGR of 6.5% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Type

Wide Utilization of Active Fixation Leads in Several Applications to Propel Segment Growth

By type, the market is classified into active fixation leads and passive fixation leads.

Active fixation leads tend to dominate as they give implanters more control over placement and stability. A screw-in mechanism can be valuable in patients with challenging anatomy, when repositioning is needed, or when physicians want precise placement to support strategies such as CSP. As pacing approaches become more targeted, the ability to fine-tune lead location becomes a practical advantage, supporting the long-term adoption of active fixation. Moreover, the segment is projected to hold a 62.9% share in 2026.

Additionally, the passive fixation leads segment is estimated to grow at a CAGR of 2.0% during the forecast period.

By End-user

Advanced Healthcare Infrastructure in Hospitals & ASCs to Propel Segment Growth

On the basis of end-user, the market is classified into hospitals and ASCs, specialty clinics, cardiac catheterization laboratories, and others.

Hospitals and ASCs account for the bulk of cardiac lead use as implants are procedure-driven and require sterile operating environments, imaging, trained EP teams, and access to emergency backup. Complex ICD/CRT cases, revisions, and infection management are typically concentrated in hospitals. At the same time, ASCs can support selected device implants in markets where outpatient pathways are well established, and payers encourage site-of-care shifts. Furthermore, the segment is set to hold 71.1% share in 2026.

In addition, the cardiac catheterization laboratories segment is projected to grow at a CAGR of 7.0% during the forecast period.

Cardiac Leads Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cardiac Leads Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 0.84 billion, and reached USD 0.87 billion in 2025. North America grows on the back of a large installed base of pacemakers/ICDs/CRT systems, strong reimbursement coverage, and a deep network of electrophysiology (EP) labs capable of handling new implants and long-term replacements. An ageing population and higher rates of atrial fibrillation (AF) keep referrals steady; in the U.S., T Product innovation also supports premium lead mix and upgrades. Together, higher spending capacity and continuous product availability sustain mid-single-digit regional growth.

U.S. Cardiac Leads Market

In 2026, the U.S. market is forecasted to represent USD 0.82 billion, capturing 38.0% of total global revenue.

Europe

Europe is expected to achieve a 2.8% growth rate in the coming years, the second-highest globally, reaching USD 0.55 billion by 2026. Europe’s growth is anchored in broad access to cardiac device therapy, with demand supported by ageing demographics and persistent CVD burden. The region also benefits from structured cardiology pathways and an expanding base of interventional/EP resources, although adoption differs widely by country. The ESC Atlas 2023 highlights major cross-country variability in cardiovascular burden and healthcare system capacity, which matters as procedure availability directly determines lead volumes. Over time, diffusion of newer pacing approaches and steady replacement cycles in mature markets keep the lead market expanding even where pricing pressure is higher than in the U.S.

U.K. Cardiac Leads Market

The U.K. market is projected to reach USD 0.08 billion by 2026, accounting for 3.6% of the global market revenue.

Germany Cardiac Leads Market

Germany's market is forecasted to reach about USD 0.10 billion by 2026, representing roughly 4.8% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market value is predicted to be valued at USD 0.53 billion, ranking as the third-largest globally. Asia Pacific is the fastest-growing region as it combines a large and aging population with improving access to advanced cardiac care in China, India, and parts of Southeast Asia. Growth is also reinforced by local product availability and regulatory momentum.

Japan Cardiac Leads Market

Japan is projected to generate approximately USD 0.09 billion in revenue by 2026, contributing nearly 4.2% to the global market.

China Cardiac Leads Market

China’s market is forecasted to reach approximately USD 0.15 billion by 2026, contributing about 7.0% to global revenues.

India Cardiac Leads Market

India is forecast to contribute approximately USD 0.06 billion to the market by 2026, corresponding to about 2.5% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate cardiac leads market growth, with Latin America expected to reach around USD 0.11 billion by 2026. Latin America’s lead market grows from a smaller base, driven by the gradual expansion of implant-capable centers, rising detection of arrhythmias and heart failure, and a slow shift toward more complex device therapy in large economies.

GCC Cardiac Leads Market

By 2026, the GCC is expected to generate approximately USD 0.02 billion in the market, accounting for nearly 0.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce Market Position of Prominent Players

The competitive landscape in cardiac leads is fairly consolidated at the top as leads are typically sold as part of a broader Cardiac Rhythm Management (CRM ecosystem, such as pacemakers/ICDs/CRT devices, delivery tools, software, clinical support, and long-term follow-up infrastructure. Medtronic, Abbott, and Boston Scientific anchor much of the premium segment globally, with BIOTRONIK SE & Co. KG and MicroPort Scientific provide strong alternatives in select geographies.

Moreover, other key players, such as Lepu Medical, Integer Holdings, MEDICO S.p.A., and Shree Pacetronix Ltd, compete through ongoing technological advancements, the growing demand for improved healthcare infrastructure, and efforts to improve therapy outcomes.

LIST OF KEY CARDIAC LEADS COMPANIES PROFILED

- Medtronic plc (Ireland)

- Abbott (U.S.)

- Boston Scientific (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- MicroPort Scientific (France)

- Lepu Medical (China)

- Integer Holdings (U.S.)

- MEDICO S.p.A. (Italy)

- Shree Pacetronix Ltd. (India)

- OSYPKA (Germany)

KEY INDUSTRY DEVELOPMENTS

- January 2026: BIOTRONIK is marking a significant achievement at its Asia Pacific Hub (BIOHUB) in Singapore with the production of three million CRM leads. Since beginning operations in late 2017, BIOTRONIK has experienced significant growth in Singapore.

- September 2025: Medtronic plc announced the initiation of a pivotal study evaluating the use of elevated and personalized cardiac pacing rates for the treatment of patients with Heart Failure with preserved Ejection Fraction.

- September 2025: BIOTRONIK announced the market release of Solia CSP S, the latest innovation in its growing portfolio of Conduction System Pacing (CSP) solutions. Solia CSP S is the first and only pacing lead worldwide that combines a fixed screw design with a stylet-driven implantation approach, offering physicians a new solution designed to simplify CSP procedures while enhancing control and precision.

- April 2025: Medtronic plc received U.S. Food and Drug Administration (FDA) approval for the OmniaSecure defibrillation lead for placement within the right ventricle.

- February 2025: The innovative product "Implantable Cardiac Pacing Lead" of MicroPort Sorin CRM (Shanghai) Co., Ltd. is approved for marketing by the China NMPA.

- September 2024: BIOTRONIK announced it has received U.S. Food and Drug Administration (FDA) labeling approval of its Selectra 3D catheter in conjunction with its Solia S lead for use in left bundle branch area pacing (LBBAP). The two products represent the first and only FDA-approved stylet-driven lead and dedicated delivery catheter system approved for LBBAP.

- September 2024: Boston Scientific Corporation has received U.S. Food and Drug Administration (FDA) approval to expand the indication for current-generation INGEVITY+ Pacing Leads, thin wires placed inside the heart and connected to an implantable device, to include Conduction System Pacing (CSP) and sensing of the left bundle branch area (LBBA) when connected to a single- or dual-chamber pacemaker.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Type, End-user, and Region |

|

By Product |

· Pacing Leads · Defibrillation (ICD) Leads · Cardiac Resynchronization Therapy (CRT) Leads |

|

By Type |

· Active Fixation Leads · Passive Fixation Leads |

|

By End-user |

· Hospitals and ASCs · Specialty Clinics · Cardiac Catheterization Laboratories · Others |

|

By Region |

· North America (By Product, By Type, By End-user, and By Country) o U.S. (By Product) o Canada (By Product) · Europe (By Product, By Type, By End-user, and By Country/Sub-region) o Germany (By Product) o U.K. (By Product) o France (By Product) o Spain (By Product) o Italy (By Product) o Scandinavia (By Product) o Rest of Europe (By Product) · Asia Pacific (By Product, By Type, By End-user, and By Country/Sub-region) o China (By Product) o Japan (By Product) o India (By Product) o Australia (By Product) o Southeast Asia (By Product) o Rest of Asia Pacific (By Product) · Latin America (By Product, By Type, By End-user, and By Country/Sub-region) o Brazil (By Product) o Mexico (By Product) o Rest of Latin America (By Product) · Middle East & Africa (By Product, By Type, By End-user, and By Country/Sub-region) o GCC (By Product) o South Africa (By Product) o Rest of the Middle East & Africa (By Product) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.06 billion in 2025 and is projected to reach USD 3.03 billion by 2034.

In 2025, the market value stood at USD 0.87 billion.

The market is expected to exhibit a CAGR of 4.3% during the forecast period.

The pacing leads segment led the market by product.

The key factors driving the market are the rising arrhythmia burden and procedure volumes.

Medtronic plc, Abbott, Boston Scientific, and BIOTRONIK SE & Co. KG are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us