Cardiovascular Information System Market Size, Share & Industry Analysis, By Component (Software and Services), By Deployment (Web based, On-premise, and Cloud-based), By Application (Cardiac Device Management, Data Management, Cardiological Visit Management, Cardiovascular Image Management, Workflow Management, Analytics, Registry & Quality Reporting, and Others), By End User (Hospitals & ASCs, Diagnostic Laboratories, Specialty Clinics, and Others), and Regional Forecasts, 2026-2034

Cardiovascular Information System Market Size and Future Outlook

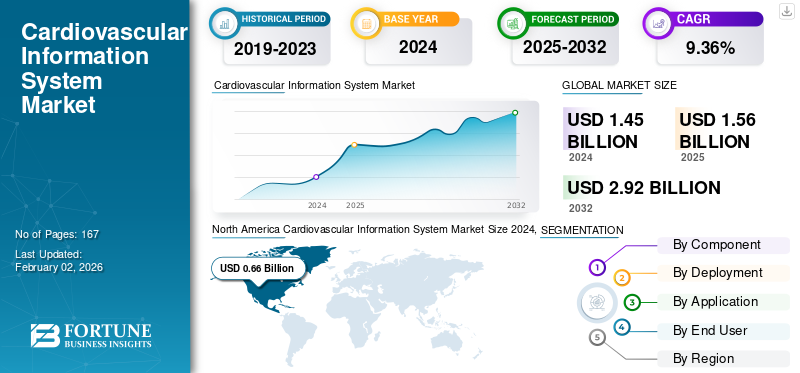

The global cardiovascular information system market size was valued at USD 1.56 billion in 2025. The market is projected to grow from USD 1.69 billion in 2026 to USD 3.62 billion by 2034, exhibiting a CAGR of 9.97% during the forecast period. North America dominated the global cardiovascular information system market with a market share of 45.56% in 2025.

Cardiovascular diseases account for a significant portion of the patient pool due to changing lifestyles and poor dietary habits. With the increasing prevalence of cardiovascular diseases, the demand for cardiovascular information systems is also rising to manage the data of the growing patient population and support market development. The market is poised for significant growth in the upcoming years due to technological advancements and numerous strategic collaborations among key players.

- In June 2024, Anumana collaborated with InfoBionic.Ai, a digital health company specializing in remote cardiac monitoring and diagnostic solutions, to develop and commercialize the next-generation ECG-AI technology and InfoBionic.Ai’s MoMe ARC platform of remote cardiac care solutions.

Key industry players, such as Intelerad, Koninklijke Philips N.V., GE HealthCare, FUJIFILM Holdings Corporation, and Siemens Healthineers AG, are investing strongly in technological advancements, followed by new product launches.

Download Free sample to learn more about this report.

CARDIOVASCULAR INFORMATION SYSTEM MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.56 Billion

- 2026 Market Size: USD 1.69 Billion

- 2034 Forecast Market Size: USD 3.62 Billion

- CAGR: 9.97% from 2026–2034

- North America dominated the cardiovascular information system market with a 45.56% share in 2025.

- The software segment is projected to lead the market with a 59.11% share in 2026.

- The hospitals & ASCs segment is projected to account for 77.74% of the market in 2026.

North America

North America generated USD 0.71 billion in 2025 and is expected to reach USD 0.77 billion in 2026.

Europe

Europe accounted for USD 0.41 billion in 2025 and is projected to reach USD 0.44 billion in 2026.

Asia Pacific

Asia Pacific held a 20.19% market share in 2025, reaching USD 0.32 billion, and is forecast to grow to USD 0.35 billion in 2026 due to rising healthcare investments.

U.S.

The U.S. cardiovascular information system market was valued at USD 0.69 billion in 2026.

Japan

The Japan market is valued at USD 0.08 billion in 2026, driven by growing digitalization and modernization of healthcare infrastructure.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Burden of Cardiovascular Diseases to Drive Market Growth

The primary factor driving the global cardiovascular information systems market growth is the increasing prevalence of cardiovascular diseases. With an increasing patient population, the need for specialized software to manage patient data, imaging data, and workflow rise. Furthermore, to fulfill the growing demand, various key players are focusing on new product launches and strategic collaborations, in turn driving the overall cardiovascular information system market growth.

- In October 2024, the World Health Organization (WHO) reported that every year, about 805,000 people in the U.S. have a heart attack. Thus, this rising burden of cardiovascular diseases is expected to drive the demand for cardiovascular information systems to manage the increasing patient volumes.

MARKET RESTRAINTS

Data Cybersecurity Concerns and Rigid Compliance Regulations May Restrict Market Growth

Data security concerns and stringent compliance regulations pose significant restraints for the cardiovascular information system market. Regulatory bodies impose stringent laws to protect sensitive patient information. These factors can increase the complexity and cost of implementation. Moreover, any data breach or non-compliance can result in severe financial penalties and a loss of trust.

- For instance, in July 2023, the American Hospital Association reported that the Cybersecurity & Infrastructure Security Agency warned of a significant, high-risk vulnerability in Medtronic’s Paceart Optima System, used to compile and manage patients’ cardiac device data.

MARKET OPPORTUNITIES

Technological Advancements Utilizing Artificial Intelligence to Offer Significant Growth Opportunities

Technological advancements in the field, such as the integration of artificial intelligence, offer lucrative growth opportunities. The integration of AI enables enhanced data analytics, predictive diagnostics, and automated workflows, thereby improving clinical decision-making and operational efficiency. As healthcare systems continue to adopt digital and AI-driven solutions, the demand for advanced cardiovascular information systems is expected to rise substantially. Furthermore, to capitalize on this opportunity, various key operating players are directing their resources toward new product launches.

- In August 2025, GE HealthCare launched the Vivid Pioneer, an AI-powered cardiovascular ultrasound system designed to support clinicians with imaging in 2D, 4D, and color flow, streamline workflow, and enhance diagnostics.

MARKET CHALLENGES

Lack of Interoperability to Pose a Significant Challenge for Market Growth

A key challenge in the cardiovascular information system market is the lack of interoperability across healthcare platforms. Many hospitals and cardiac centers use diverse information systems, imaging software, and EHR platforms that are often not fully compatible. This fragmentation hinders seamless data exchange and introduces inefficiencies into clinical workflows. It also increases integration costs and implementation time for new CVIS solutions. As a result, healthcare providers struggle to achieve a unified view of patient data, which hinders real-time decision-making and reduces the overall effectiveness of digital cardiovascular care systems.

- In May 2025, AHA Scientific Journal published an article titled ‘Data Interoperability and Harmonization in Cardiovascular Genomic and Precision Medicine’ that reported challenges in interoperability of these systems.

CARDIOVASCULAR INFORMATION SYSTEM MARKET TRENDS

Rising Use of Advanced Imaging and 3D Visualization for Complex Cardiovascular Diagnostics is a Prominent Market Trend

One of the significant global trends in the cardiovascular information system market is the emerging use of advanced imaging and 3D visualization. These technologies enable clinicians to obtain detailed and accurate views of cardiac structures, improving diagnosis and treatment planning. This integration of 3D visualization enhances precision, improving patient outcomes. Such increasing adoption of these 3D visualizations for complex cardiovascular diagnostics is a prominent trend.

- For instance, in May 2025, Koninklijke Philips N.V. launched its VeriSight Pro 3D Intracardiac Echocardiography (ICE) catheter in Europe, which enables 3D imaging directly inside the heart, helping physicians perform procedures with greater clarity.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Increasing Product Launches for Software to Propel Segmental Growth

Based on the component, the market is divided into software and services.

To know how our report can help streamline your business, Speak to Analyst

The software segment is projecteed to dominate the market with a share of 59.11% in 2026. The growing adoption of cloud-based and AI-driven solutions further strengthens the demand for advanced software platforms. Additionally, continuous software updates and analytics tools help healthcare providers enhance diagnostic accuracy and patient outcomes.

- For instance, in August 2025, DESKi launched in the U.S., enabling healthcare professionals to conduct diagnostic-quality heart ultrasounds.

By Deployment

Customization Advantages for On-Premise Deployment to Lead Segment Growth

Based on deployment, the market is segmented into web based, on-premise, and cloud-based.

The on-premise segment is projecteed to dominate the market with a share of 44.33% in 2026. The segment's dominant market share is attributed to its strong data control, security, and customization advantages. Additionally, these on-premises systems offer improved accuracy and data security, especially among large and well-funded hospitals.

- RSNA published a study titled ‘Diagnostic Accuracy of On-Premise Automated Coronary CT Angiography Analysis Based on Coronary Artery Disease Reporting and Data System 2.0’that reported on-premise AI accurately ruled out obstructive coronary artery disease at CCTA and achieved substantial to near-perfect agreement with human experts for CAD-RADS 2.0 stenosis severity and plaque burden. This highlights the increasing adoption of on-premise solutions in hospital settings.

In addition, cloud-based cardiovascular information systems are projected to grow at a CAGR of 13.68% during the study period.

By Application

New Product Launches and Wide Applications to Drive Growth of Cardiovascular Image Management

Based on application, the market is segmented into cardiac device management, data management, cardiological visit management, cardiovascular image management, workflow management, analytics, registry & quality reporting, and others.

The cardiovascular image management segment is projecteed to dominate the market with a share of 31.99% in 2026 due to the increasing volume of cardiac imaging procedures and the critical need for efficient storage of imaging data. Cardiovascular departments generate vast amounts of data requiring advanced systems for accurate interpretation and timely diagnosis. As cardiac imaging becomes more data-intensive and technology-driven, key companies are launching new products in the segment to capitalize on growing adoption.

- In February 2025, Intelerad partnered with SolutionHealth for the seamless integration of the health system’s imaging system, supporting exceptional patient care and enhancing operational efficiency.

In addition, the analytics application segment is projected to grow at a CAGR of 13.10%, during the study period.

By End User

High Patient Volume in Hospitals & Ambulatory Centers to Lead Segment Growth

On the basis of end user, the market is segmented into hospitals & ASCs, diagnostic laboratories, specialty clinics, and others.

The hospitals & ASCs segment is projecteed to dominate the market with a share of 77.74% in 2026. These are the primary sites for numerous cardiovascular procedures, generating immense data. These factors create a need for efficient cardiovascular information systems. Also, with their broader infrastructure and higher budgets, they are better positioned to invest in advanced cardiovascular information systems.

- In March 2025, Apollo Hospitals partnered with 3M to further develop its AI tool for predicting cardiovascular disease risks. The partnership enabled Solventum Health Information Systems to use its patient classification and quality methodologies to enhance cardiovascular care.

The specialty clinics segment is projected to grow at a CAGR of 12.61% during the study period.

Cardiovascular Information System Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

In 2025, North America held 45.56% of the global market share, reaching a valuation of USD 0.71 Billion, and is projected to grow to USD 0.77 Billion in 2026. The regional market is poised for robust growth due to the increasing prevalence of cardiovascular diseases, resulting in a large patient pool. Furthermore, technological advancements and the rapid adoption of these information systems are expected to drive market growth. Underscoring this growth opportunity, various companies are participating in strategic acquisitions to expand product offerings.

North America Cardiovascular Information System Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

- In June 2025, MultiCare Health System, comprising 13 hospitals and more than 300 clinics, selected Merge to deliver cloud-based enterprise imaging services. The increasing adoption of these information systems is driving growth in the region. In 2025, the U.S. market is valued at USD 0.69 billion by 2026.

Europe

Europe accounted for USD 0.41 billion in 2025, representing 26.08% of the global market revenue, and is projected to reach USD 0.44 billion in 2026. The region’s growth is supported by continuous new product launches from leading market participants and rising adoption across key end-use industries. A robust regulatory environment, strong innovation ecosystem, and well-established healthcare and research infrastructure continue to facilitate market expansion. Growing investments in advanced technologies and product development further strengthen demand across the region. The U.K. is expected to reach USD 0.10 billion in 2026, followed by Germany at USD 0.09 billion by 2026 and France at USD 0.08 billion.

Asia Pacific

Asia Pacific contributed approximately USD 0.32 Billion to the global market in 2025, accounting for 20.19% share, and is expected to reach USD 0.35 Billion in 2026. Regional growth is primarily driven by increasing healthcare expenditure, expanding industrial capabilities, and rising investments across emerging economies. Supportive government initiatives, improving access to healthcare services, and ongoing expansion of research and manufacturing facilities are contributing to market development. Demand continues to strengthen as organizations increase spending on advanced products and technologies to address evolving industry requirements. The Japan market is valued at USD 0.08 billion by 2026, the China market is valued at USD 0.10 billion by 2026, and the India market is valued at USD 0.05 billion by 2026.

Latin America and the Middle East & Africa

The Middle East & Africa region captured 3.86% of the global market in 2025, generating USD 0.06 Billion in revenue, and is projected to reach USD 0.06 Billion in 2026. In 2025, Latin America generated USD 0.07 Billion, contributing 4.31% to global market revenue, and is projected to grow to USD 0.07 Billion in 2026 owing to advancing healthcare infrastructure and the rising adoption of digital technologies. In the Middle East & Africa, the GCC will record USD 0.03 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Strategic Acquisitions by Key Players to Capitalize Market Share and Propel Market Growth

The global cardiovascular information system market has a semi-consolidated market structure, comprising prominent players such as Intelerad, Koninklijke Philips N.V., GE HealthCare, FUJIFILM and Holdings Corporation, among others. The significant share of these companies is due to numerous strategic activities, such as new product launches, collaborations, and strategic acquisitions.

- In July 2021, Intelerad Medical Systems acquired Lumedx, a leading provider of healthcare analytics and Cardiovascular Information Systems (CVIS), to expand its product offering and further position the company as a leader in the cardiovascular space.

Other notable players in the global market include Siemens Healthineers AG, Esaote SPA, and Merative. These companies prioritize new product launches and collaborations to boost their global cardiovascular information system market share.

LIST OF KEY CARDIOVASCULAR INFORMATION SYSTEM COMPANIES PROFILED

- Intelerad. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare. (U.S.)

- FUJIFILM Holdings Corporation (Japan)

- Siemens Healthineers AG (Germany)

- Esaote SPA (Italy)

- Merative (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: YorLabs, Inc. received 510(k) clearance for the company's YorLabs Intracardiac Imaging System—an ultrasound platform designed to simplify workflow, reduce costs, and enhance procedural efficiency inside the cath lab.

- October 2025: Lupin Digital Health launched VITALYFE, an AI-powered cardiometabolic wellness platform designed to extend hospital-grade cardiac expertise to preventive wellness for its users.

- October 2025: Medtronic Cardiac Surgery launched its Extracorporeal Membrane Oxygenation (ECMO) system called the VitalFlow system, in Europe. The system bridges the gap between bedside care and intra-hospital transport.

- August 2025: LivaNova PLC launched the Essenz Perfusion System in China for LivaNova heart-lung machines (HLMs). The Essenz Perfusion System enabled a patient-tailored perfusion approach, aiming to improve clinical workflows during life-saving Cardiopulmonary Bypass (CPB) procedures.

- May 2024: Boston Scientific Corporation collaborated with Koninklijke Philips N.V. and Siemens Medical Solutions to enable the use of its iLab Ultrasound Imaging System with the Philips Allura Xper and the Siemens AXIOM Artis and Artis zee interventional X-ray systems. These innovative systems are designed to provide physicians with a 360-degree view inside the heart and coronary vessels, assisting with diagnosis and generating a more accurate image.

REPORT COVERAGE

The global cardiovascular information system market analysis provides a detailed study of the market size & forecast by all the market segments included in the report. The report also provides insights into market dynamics and trends expected to drive the market during the forecast period. The report also comprises key aspects, such as an overview of technological advancements, product launches, insights on strategic partnerships, mergers & acquisitions, and key industry developments by key regions. Additionally, it also provides a detailed competitive landscape, including market share and profiles of major industry players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attribute | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.97% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Application |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights states that the global market value stood at USD 1.56 billion in 2025 and is projected to reach USD 3.62 billion by 2034.

In 2025, North America’s market value stood at USD 0.71 billion.

The market is expected to exhibit a CAGR of 9.97% during the forecast period of 2026-2034.

The software segment led the market in terms of component.

The increasing prevalence of cardiovascular diseases and large patient pools are driving market growth during the forecast period.

Intelerad, Koninklijke Philips N.V., GE HealthCare, and FUJIFILM Holdings Corporation are some of the major players in the global market.

North America dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us