Cardiovascular Ultrasound Market Size, Share & Industry Analysis, By Product (Systems and Accessories & Consumables), By Application (Cardiac Structure and Function Assessment, Valvular Heart Disease Assessment, Heart Failure and Cardiomyopathy Evaluation, Coronary and Vascular Imaging Guidance, Congenital Heart Disease Assessment, and Others), By End-user (Hospitals & ASCs, Specialty Clinics, Diagnostic Imaging Centers, and Others), and Regional Forecast, 2026-2034

Cardiovascular Ultrasound Market Size and Future Outlook

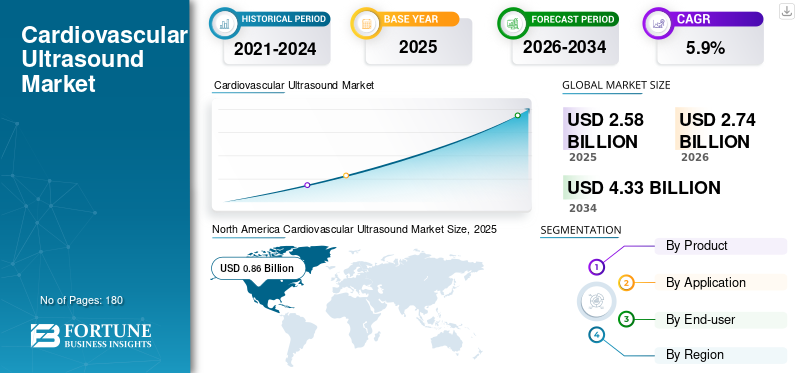

The global cardiovascular ultrasound market size was valued at USD 2.58 billion in 2025. The market is projected to grow from USD 2.74 billion in 2026 to USD 4.33 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period. North America dominated the cardiovascular ultrasound market with a market share of 33.33% in 2025.

Cardiovascular ultrasound refers primarily to echocardiography and related ultrasound-based cardiac imaging used to visualize heart anatomy, chamber size, wall motion, valve function, blood flow, and hemodynamics in a noninvasive, real-time manner. The market is growing because the rising burden of cardiovascular disease is driving sustained demand for earlier diagnosis, repeat monitoring, and procedural guidance.

Furthermore, GE HealthCare, Koninklijke Philips N.V., and Siemens Healthineers AG held the highest market share in 2025 due to their broad portfolios and strong worldwide distribution networks.

Download Free sample to learn more about this report.

CARDIOVASCULAR ULTRASOUND MARKET Key Takeaways

- 2025 Market Size: USD 2.58 billion

- 2026 Market Size: USD 2.74 billion

- 2034 Forecast Market Size: USD 4.33 billion

- CAGR: 5.9% from 2026–2034

- North America dominated the cardiovascular ultrasound market with a market share of 33.33% in 2025.

- Hospitals & ASCs are projected to hold a 65.3% market share in 2026, making them the leading end-user segment.

- Cardiac structure and function assessment is expected to account for a 32.7% market share in 2026, leading the application segment.

North America

North America held USD 0.86 billion in 2025, driven by strong adoption of advanced diagnostic imaging technologies and well-established hospital infrastructure.

Europe

Europe is anticipated to grow at a CAGR of 5.3% during the forecast period, supported by a strong network of diagnostic imaging centers and expanding product availability.

Asia Pacific

Asia Pacific is projected to reach USD 0.80 billion by 2026, driven by expanding healthcare infrastructure, rising cardiovascular disease prevalence, and increasing investments in diagnostic imaging.

U.S.

The market is projected to reach USD 0.80 billion by 2026, accounting for approximately 29.2% of the global cardiovascular ultrasound market.

Japan

The market is expected to generate around USD 0.15 billion in revenue by 2026, representing nearly 5.3% of the global market.

Read More

CARDIOVASCULAR ULTRASOUND MARKET TRENDS

AI-enabled Automation Becoming Central to Product Differentiation to Emerge as a Key Trend

Currently, there has been a significant shift from image-acquisition hardware alone to AI-enabled cardiovascular platforms that automate measurements, improve reproducibility, and integrate imaging with reporting and procedural workflows. Moreover, key players are increasingly competing on workflow compression, repeatability, and decision support across the cardiac-care continuum.

- For instance, in June 2024, Koninklijke Philips N.V. launched FDA-cleared AI applications integrated into its EPIQ CVx and Affiniti CVx cardiovascular ultrasound systems, including the first automated segmental wall motion scoring for rapid detection of coronary artery disease and cardio-oncology issues, as well as fully automated 3D quantification of mitral regurgitation.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Cardiovascular Disease Burden and Need for Faster Diagnosis to Fuel the Market Expansion

Over the past few years, there has been an expanding burden of cardiovascular disease, which is increasing the volume of patients needing screening, diagnosis, follow-up, and interventional imaging support.

- For instance, according to the data from the Journal of the American College of Cardiology (JACC), there were 315.0 million prevalent cases of coronary artery disease in 2022.

In such a scenario, echocardiography is widely used because it is noninvasive, repeatable, relatively accessible, and suitable across emergency, inpatient, outpatient, and peri-procedural settings. This is anticipated to drive the global cardiovascular ultrasound market growth.

MARKET RESTRAINTS

Rising Skilled Operator Dependency Leads to Market Restriction

Despite significant adoption of cardiovascular ultrasound, it still depends heavily on operator skill, protocol consistency, and post-exam interpretation, especially in advanced echo, valve assessment, and procedural guidance. In such a scenario, limited training and a smaller number of key professionals may lead to additional delays in procedures, limiting the adoption of cardiovascular ultrasound. This is anticipated to hamper the market expansion.

- For instance, in March 2025, the Radiological Society of North America (RSNA) stated that by 2034, projections indicate a physician shortage ranging from 37,800 to 124,000, including several thousand radiologists.

MARKET OPPORTUNITIES

AI, Handheld Ultrasound, and Expansion into New Care Settings to Create Growth Opportunities

In recent years, AI-guided acquisition and handheld devices have lowered the expertise threshold for basic cardiac assessment and triage. These developments are creating room for market expansion in underserved geographies, outpatient pathways, and preventive cardiology, while also supporting faster referral decisions and earlier disease detection. This is expected to support the market expansion over the forecast period.

- For instance, in April 2024, GE HealthCare launched Caption AI on its Vscan Air SL wireless handheld ultrasound system, providing real-time AI guidance for probe positioning and automated ejection fraction calculation to help clinicians, even non-experts, capture diagnostic-quality cardiac images quickly at the point of care.

MARKET CHALLENGES

Increasing High Cost of Advanced Systems to Challenge Market Expansion

Despite the significant demand for cardiovascular ultrasound systems, the high cost of advanced systems remains a significant barrier to widespread adoption, particularly in emerging markets and smaller healthcare facilities. Premium systems equipped with AI capabilities, 3D/4D imaging, and interventional guidance features require substantial upfront capital investment, as well as ongoing maintenance, software upgrades, and training costs.

Hospitals often prioritize multi-modality imaging investments, limiting budget allocation for ultrasound upgrades. Such a scenario is anticipated to challenge the cardiovascular ultrasound market expansion.

Segmentation Analysis

By Product

Expanding Number of Healthcare Facilities to Boost the Systems Segmental Growth

Based on product, the market is segmented into systems and accessories & consumables.

To know how our report can help streamline your business, Speak to Analyst

The systems segment accounted for the largest global cardiovascular ultrasound market share in 2025. The segment’s growth is attributed to increasing launches of advanced systems and the expanding number of healthcare facilities, driving the need for systems.

Additionally, the accessories & consumables segment is projected to grow at a 7.5% CAGR during the forecast period.

By Application

Widespread Usage of Cardiac Ultrasound in Cardiac Structure and Function Assessment to Boost the Segment’s Growth

By application, the market is classified into cardiac structure and function assessment, valvular heart disease assessment, heart failure and cardiomyopathy evaluation, coronary and vascular imaging guidance, congenital heart disease assessment, and others.

The cardiac structure and function assessment segment accounted for the largest market share in 2025. Cardiac structure and function assessment is the foundational use case for cardiovascular ultrasound across nearly all care settings. In this case, standard cardiac ultrasound routinely evaluates chamber size, ventricular function, wall motion, and overall cardiac morphology, which is expected to boost demand and contribute to the segment’s growth. Moreover, the segment is projected to hold a 32.7% share in 2026.

Additionally, the valvular heart disease assessment segment is expected to grow at a 6.1% CAGR during the forecast period.

By End-user

Large Number of Hospitals & ASCs in Developed Countries to Propel the Segment’s Growth

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics, diagnostic imaging centers, and others.

In 2025, hospitals & ASCs dominated the market as end users. The growth is attributed to the high concentration of acute cardiac cases, inpatient echo demand, perioperative imaging, and structurally complex interventions in these settings. As a result, the surge in the number of hospitals and ASCs is expected to further increase the adoption of cardiovascular ultrasound. This is expected to fuel the segment’s growth. Furthermore, the segment is set to hold 65.3% share in 2026.

- For instance, according to the American Hospital Association (AHA) Fast Facts, as of early 2026, there were around 6,100 total hospitals in the U.S.

In addition, the specialty clinics segment is projected to grow at a 7.1% CAGR over the forecast period.

Cardiovascular Ultrasound Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Cardiovascular Ultrasound Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 0.80 billion, and held USD 0.86 billion in 2025. The growth is driven by strong adoption of advanced diagnostic imaging technologies and well-established hospital infrastructure, which favor higher purchase rates of cardiovascular ultrasound in the region.

U.S. Cardiovascular Ultrasound Market

In 2026, the U.S. is anticipated to reach USD 0.80 billion, accounting for approximately 29.2% of the global market.

Europe

Europe is projected to record a 5.3% CAGR during the forecast period, the third-highest globally, reaching USD 0.72 billion by 2026. The growth is attributed to a significant network of diagnostic imaging centers and radiologists, attracting key players to expand their product offerings in the region.

- For instance, according to the Royal College of Radiologists (RCR) 2024 census, there were 4,699 whole-time equivalent (WTE) consultant clinical radiologists working in the U.K.

U.K Cardiovascular Ultrasound Market

The U.K. market is projected to reach USD 0.12 billion by 2026, representing approximately 4.5% of global revenues.

Germany Cardiovascular Ultrasound Market

Germany's market is expected to reach USD 0.15 billion by 2026, accounting for approximately 5.6% of global revenue.

Asia Pacific

By 2026, the Asia Pacific market is projected to reach approximately USD 0.80 billion, making it the second-largest market worldwide. The growth is attributed to improving healthcare infrastructure, rising cardiovascular disease burden, growing medical tourism, and increasing investments in diagnostic imaging technologies.

Japan Cardiovascular Ultrasound Market

Japan is projected to generate approximately USD 0.15 billion in revenue by 2026, representing nearly 5.3% of the global market.

China Cardiovascular Ultrasound Market

China’s market is anticipated to reach around USD 0.28 billion by 2026, accounting for nearly 10.1% of global revenues.

India Cardiovascular Ultrasound Market

India’s market is expected to reach approximately USD 0.11 billion by 2026, accounting for around 4.2% of global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate growth, with the Latin America market estimated to reach approximately USD 0.19 billion by 2026. The growth is driven by improved access to cardiac diagnostics and increased awareness of the importance of early heart disease detection.

GCC Cardiovascular Ultrasound Market

By 2026, the GCC market is estimated to reach approximately USD 0.05 billion, representing around 1.9% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad Product Range and Strategic Initiatives to Strengthen the Market Presence of Major Players

In 2025, GE HealthCare, Koninklijke Philips N.V., and Siemens Healthineers held the largest global market share in cardiovascular ultrasound. The dominance of these companies is mainly due to strong brand reputation, widespread distribution network, and a broad portfolio of advanced cardiovascular ultrasound systems.

Moreover, other prominent players are intensifying competition by offering products at competitive prices. Also, they are focusing on expanding market presence through strategic initiatives such as partnerships, acquisitions, and collaborations.

LIST OF KEY CARDIOVASCULAR ULTRASOUND COMPANIES PROFILED

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Siemens Healthineers (Germany)

- Canon Medical Systems Corporation (Japan)

- FUJIFILM Holdings Corporation (Japan)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Esaote SPA (Italy)

- SonoScape Medical Corp (China)

- Butterfly Network, inc (U.S.)

- Konica Minolta, Inc. (Japan)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Koninklijke Philips N.V. launched Transcend Plus for EPIQ CVx and Affiniti CVx, featuring image-quality and FDA-cleared AI enhancements in cardiovascular ultrasound.

- March 2025: FUJIFILM Holdings Corporation partnered with Us2.ai to integrate AI-automated echocardiography analysis into the LISENDO cardiovascular ultrasound workflow.

- August 2024: Siemens Healthineers announced FDA clearance of ACUSON Origin and the AcuNav Lumos 4D ICE catheter for cardiovascular imaging and procedures.

- June 2024: Koninklijke Philips N.V. announced next-generation AI-enabled cardiovascular ultrasound with new FDA-cleared tools for wall-motion scoring and automated mitral-regurgitation analysis.

- April 2024: Fujifilm Holdings Corporation launched the OPIE transducer for on-pump intracardiac echocardiography imaging in septal myectomy.

- January 2024: Butterfly Network, inc announced FDA clearance of Butterfly iQ3, its next-generation handheld ultrasound system.

- October 2023: GE HealthCare launched Caption AI on Vscan Air SL for rapid cardiac assessments and automated ejection-fraction estimation.

REPORT COVERAGE

The report offers a detailed evaluation of all market segments, highlighting key growth drivers, emerging trends, opportunities, major restraints, and challenges shaping the market landscape. It also covers technological advancements, the incidence of major diseases, significant industry developments, comprehensive market share insights, recent product launches, and thorough profiles of leading market players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.9% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.58 billion in 2025 and is projected to reach USD 4.33 billion by 2034.

In 2025, the market value stood at USD 0.86 billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period.

The systems segment led the market by product.

The key factor driving the market is the rising cardiovascular disease burden.

GE HealthCare, Koninklijke Philips N.V., and Siemens Healthineers are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us