Point-of-care Ultrasound Market Size, Share & Industry Analysis, By Product (Cart-based and Compact & Hand-held), By End User (Hospitals, Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

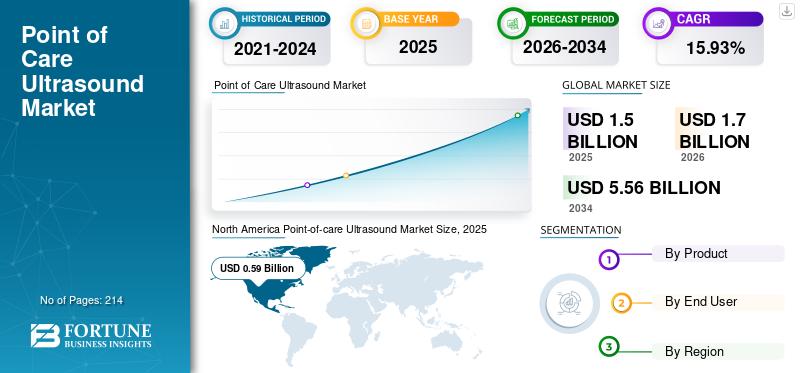

The global point-of-care ultrasound market size was valued at USD 1.5 billion in 2025. The market is projected to grow from USD 1.7 billion in 2026 to USD 5.56 billion by 2034, exhibiting a CAGR of 15.93% during the forecast period. North America dominated the point-of-care ultrasound market with a market share of 39.43% in 2025. Moreover, the U.S. point of care ultrasound market size is projected to grow significantly, reaching an estimated value of USD 1.46 billion by 2032, driven by demand for compact point-of-care ultrasound devices.

Point-of-care (POC) ultrasound plays an essential role in potential clinical applications such as accessing diagnostic imaging, and real-time imaging-guided interventions during surgical procedures, among others. The devices for point-of-care application aid in early bedside evaluation of primary treatment, and emergency screening among patients across specialty clinics, ambulatory surgical centers, and primary health centers.

In the current healthcare scenario, there is a greater transition towards outpatient care from inpatient care. This has resulted in stronger demand for the use of ultrasound devices at the point of care. Also, the demand for ultrasound devices for point-of-care applications has further escalated due to the need for emergency medicine, and intensive care, such as cardiology and obstetrics. Furthermore, the strong trend for cutting-edge R&D amongst prominent companies has encouraged the introduction of several technologically superior products.

- In March 2021, GE Healthcare launched Venue Fit, a streamlined and compact system, alongside artificial intelligence (AI) offering for cardiac imaging on Venue and Venue Go. The Venue Fit features a small footprint device designed to fit in point-of-care settings.

- In October 2021, NeuroLogica Corp., the U.S. healthcare subsidiary of Samsung, launched the V8; a new high-end ultrasound system that provides enhanced image quality, usability, and convenience for ultrasound professionals.

This trend of introducing new and advanced products, coupled with the increasing need for superior medical imaging in outpatient care settings, is expected to strongly surge the growth of the global market in developed and emerging regions during the forecast period.

The COVID-19 pandemic had disrupted healthcare accessibility for the global population due to travel restrictions and country lockdowns. However, after the outbreak of COVID-19, the market witnessed positive growth owing to an increase in diagnostic imaging tests among patients across the globe.

- According to a study published by the Royal Society of Tropical Medicine and Hygiene, in December 2020, half of all ultrasound examinations were delivered as point-of-care interventions out of the total medical inpatients examined at Queen Elizabeth Central Hospital.

High adoption of point-of-care imaging tests among the patient population across several clinical conditions other than COVID-19, propelled the market growth in 2020.

Moreover, the use of hand-held devices increased in emergency units of hospitals due to their convenient handling and less sterilization requirement, further stabilizing the market growth in 2021. Similarly, a downturn in the number of COVID-19 patients, and a substantial increase in uptake of ultrasound tests among the general population at homecare settings further propelled the market growth at a substantial pace in 2021.

- According to an article published by Diagnostic and Interventional Radiology in October 2021, the point-of-care ultrasound witnessed rapid growth owing to an increase in point-of-care ultrasound adoption at homecare settings for health visits and monitoring of patients.

The market is anticipated to witness steady growth prospects over the forecast period (2024-2032) due to the strong demand for these products.

Download Free sample to learn more about this report.

Global Point-of-Care Ultrasound Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 1.5 billion

- 2026 Market Size: USD 1.7 billion

- 2034 Forecast Market Size: USD 5.56 billion

- CAGR: 15.93% from 2026–2034

Market Share:

- North America dominated the point-of-care ultrasound market with a 39.43% share in 2025, driven by the rising demand for compact ultrasound devices in emergency and outpatient care settings.

- By Product Type, the compact & hand-held segment is expected to retain its largest market share owing to increasing preference for portable, cost-effective devices that offer real-time imaging at the point of care.

Key Country Highlights:

- United States: Strong emphasis on the adoption of portable ultrasound devices in emergency departments and outpatient care to enhance clinical decision-making.

- Europe: Increasing use of point-of-care ultrasound in diagnostic screenings for cardiovascular and respiratory diseases across hospitals and specialty clinics.

- China: Growing demand for compact ultrasound systems due to the rising burden of chronic diseases and expanding healthcare infrastructure in urban and rural areas.

- Japan: Advancements in miniaturized ultrasound technologies are supporting increased use of point-of-care imaging in primary care and aging population healthcare services.

Point-of-care Ultrasound Market Trends

Potential Advantages of Ultrasound Devices for Point-of-Care Applications

The demand for ultrasound devices is high owing to rising diagnostic tests and screening among patients across the globe. Moreover, ultrasound has been an effective imaging method for the diagnosis of several chronic diseases, such as vascular disorders, cardiovascular disorders, and sports injuries.

- According to data published by NHS England in 2020, around 10.3 million ultrasound procedures were performed in the U.K. in 2020.

The conventional cart-based ultrasound equipment in routine diagnostic imaging produces detailed high-resolution images and has a varied application area across healthcare settings. However, certain limitations associated with conventional ultrasound systems such as the high cost of acquisition, and limited portability, are leading to an increasing preference for portable systems among health professionals. On the other hand, compact and hand-held devices are portable, safe, and economical to use, and provide immediate results for clinical decision-making. Moreover, the costs associated with hand-held devices are less than that of conventional ultrasound devices.

- According to an article published by Exo Imaging, Inc., the American Academy of Physician Associates (AAPA) stated that conventional ultrasound equipment costs around 15 times higher than a portable or point-of-care ultrasound.

- As per similar estimates, the standard ultrasound machines cost from USD 40,000 to USD 200,000. However, the portable ultrasound machine can range from USD 8,000 to USD 10,000 in the U.S.

Moreover, the use of compact devices is increasing among healthcare professionals for diagnostic imaging at patient bedside in intensive care units, and diagnosis of trauma and respiratory disorders across emergency departments. The high adoption was attributed to the potential advantages of these devices, such as non-invasiveness, high sensitivity, and high speed of ultrasound interpretation across health centers.

- According to an article published by NCBI in August 2022, a cohort study results revealed by Sharif et al., stated that the sensitivity of compact ultrasound devices in the diagnosis of appendicitis was 69.2%, and the specificity was 90.6%.

This is also increasing the presence and adoption of ultrasound devices in point-of-care applications areas such as cardiology, and gastroenterology, across developed countries, boosting its global demand. Similarly, compact ultrasound devices potentially have a positive impact on medical education and patient care, attributed to its benefits such as portability, and ease of use. Therefore, the high advantages of portable ultrasound over traditional devices cater to its adoption across various settings, which augmented the market growth.

Download Free sample to learn more about this report.

Point-of-care Ultrasound Market Growth Factors

High Emphasis of Key Players on Ultrasound Device Launches to Cater its Adoption

The demand for ultrasound systems for point of care applications is rising across healthcare specialties owing to benefits such as portability, comparatively lower cost, and improved clinical efficiency of these systems. Moreover, owing to these advantages, the preference for compact ultrasound devices is rising among healthcare professionals such as anesthesiologists and orthopedists in hospital emergency rooms and intensive care units.

- According to an article published by Viatom Technology Co., Ltd., the growth rate of adoption of portable ultrasound devices in developed countries is as high as 30.0% to 40.0%, showing good momentum.

- According to an article published by NCBI in 2023, in a cohort study in hospitals in Rwanda, the use of ultrasound devices changed medications administered in 42.0% of medical cases and admission decisions in 30.0% of patient visits.

Thus, owing to high demand, the major key players are now focusing on the development of technologically advanced products across the globe. Moreover, the high emphasis of market players on the launch and expansion of ultrasound devices in point-of-care applications across developing countries increases the presence, and adoption of ultrasound devices, further augmenting market growth.

- In June 2023, at the 2023 American Society of Echocardiography Event held in Maryland, U.S., Koninklijke Philips N.V. unveiled its Ultrasound Compact 5500CV. With this product, the company broadened its care offerings to deliver diagnostic quality echocardiography in a compact form, aiming to boost the clinical confidence at the point of care.

- In January 2023, the FUJIFILM Sonosite, Inc., specialists in developing cutting-edge point-of-care ultrasound, announced the launch of a new Sonosite PX ultrasound system in India. In July 2020, the company had launched the system in the U.S.

- In February 2021, GE HealthCare launched a new hand-held ultrasound device, Vscan Air, an update to its first-generation Vscan device, released in 2010. The device is commercially available in the U.S. and Europe.

Also, several emerging players are focusing on R&D of technically advanced solutions and platforms for easy accessibility, and enhanced diagnostic tools for better results among patients. Thus, the integration of such developed platforms with devices for point of care applications further expands its accessibility across several indications, such as assessments of the heart and the lungs.

- In February 2023, Koninklijke Philips N.V., announced the FDA clearance and launch of a new version of its point-of-care hand-held ultrasound, 5000 compact series for cardiovascular and other applications.

- In April 2022, Exo Imaging, Inc., launched Exo Works, an intelligent and intuitive point-of-care ultrasound workflow solution that enables physicians to easily document, review, bill and manage quality assurance all from one platform in seconds.

RESTRAINING FACTORS

Limitations Associated with Portable Devices in Point of Care Applications to Hamper the Adoption

Certain limitations associated with using hand-held devices have been a point of concern related to the adoption of these devices. The currently available ultrasound devices, such as Lumify and Vscan Air, are designed for diagnosis of certain medical conditions such as cardiovascular disorders, and trauma among the patients. Thus, these devices cannot support all aspects of the patient's physical examination, including 3D and 4D imaging. Moreover, factors such as low sensitivity and specificity, and deferred image quality of compact devices may limit the diagnosis and clinical guidance of diseases among patients.

Another factor limiting the use of hand-held devices is the lack of experienced technicians. The expansion of the hand-held ultrasound market will increase the number of new users performing ultrasound scans through hand-held equipment, thereby resulting in poor imaging results and incorrect disease assessment. Also, the limited presence of training and certification courses by national and international organizations for the use of these devices is limiting their adoption among radiologists, further restricting the market.

- In July 2022, the Society of Hospital Medicine published an observational study of all Veterans Affairs (VA) medical centers conducted between August 2019 and March 2020. The most common barriers to ultrasound devices use for point-of-care application among all hospital medicine groups (HMGs) were a lack of trained providers (87%), lack of ultrasound equipment (54%), and lack of training opportunities (53%).

- According to an article published by NCBI in August 2022, a survey conducted by the University of Vermont demonstrated that only 5.0% of family medicine providers use ultrasound devices for point-of-care applications in their practice.

In addition, several barriers hinder the adoption of point-of-care ultrasound (POCUS) devices in primary care clinics. Some of these barriers include a lack of trained providers, insufficient funding for training, limited availability of ultrasound equipment, and the absence of a physician or clinician champion.

Moreover, the lack of knowledge regarding hand-held devices in emerging countries such as China, and India, among others, also tends to limit their adoption. The above-mentioned limiting factors associated with using hand-held ultrasound devices and limited awareness regarding these devices tend to restrict their adoption, thereby limiting the market growth.

Point-of-care Ultrasound Market Segmentation Analysis

By Product Analysis

Rising Demand for Hand-held Ultrasound Devices to Boost Segment Growth during 2024-2032

On the basis of product, the market is segmented into cart-based, and compact & hand-held segments. The cart/trolley segment led the market accounting for 67.33% market share in 2026. The dominance is due to the greater adoption of cart-based devices for point-of-care interventions such as emergency medicine, anesthesia, vascular access, and the increasing trend of market players focusing on introducing new and innovative systems for point-of-care applications.

- In August 2020, Hologic, Inc., announced the U.S. launch of the SuperSonic MACH 40 ultrasound system, expanding its portfolio of ultrasound technologies with its cart-based system. The system featured excellent image quality and standard-setting imaging modes, and was designed to enhance efficiency and accuracy.

The hand-held segment is anticipated to register a higher CAGR in the forecast period. This is primarily due to newer hand-held devices' launches by key players and high demand of hand-held devices across healthcare settings. Moreover, the diverse application areas of hand-held ultrasound equipment across several clinical conditions will drive the point-of-care ultrasound systems in developed countries from 2024-2032.

- As per GE HealthCare estimates in March 2021, owing to high product demand, the market for hand-held ultrasound devices will grow at USD 1.0 billion in the coming years.

- For instance, in February 2022, Koninklijke Philips N.V., launched Lumify, a hand-held point-of-care ultrasound that offered hemodynamic assessment and measuring capabilities. The new product allows clinicians to quantify the blood flow in several point-of-care diagnostic and therapeutic applications, comprising cardiology, abdominal, vascular, obstetrics, urology, and gynecology.

Furthermore, the rise in popularity of hand-held ultrasound devices is mainly attributed to their ease of use and efficiency in swiftly capturing images at the point of care settings. Hand-held ultrasound devices distinguish themselves from other ultrasound machines for their compact size, often small enough to be carried in a clinician’s pocket. This portability makes clinicians able to capture patient images virtually anywhere.

- For instance, as per data published by Mindray DS USA, Inc. in July 2023, hand-held ultrasound devices provide various benefits in terms of point-of-care settings, including affordability, ergonomics, real-time imaging, accessibility, and portability.

These are some of the factors accountable for segment growth over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User Analysis

Increase in the Number of Patient Visits at Emergency Departments to Propel Hospital Segment Share

Based on end-user, the market is segmented into hospitals, clinics, and others.

The Hospitals segment dominated the market accounting for 63.18% market share in 2026. The hospital segment is projected to account for the largest market share during the forecast period because of the strong demand for ultrasound imaging in hospitals' emergency care and intensive care units (ICUs). Also, the rising number of hospital admissions in ICU, trauma & emergency departments, owing to high global disease prevalence, is driving the demand for ultrasound systems in point-of-care applications, further propelling segment share.

- According to World Health Organization data, about 422.0 million population worldwide suffers from diabetes.

- As per National Center for Health Statistics data in 2020, the U.S. witnessed 131.3 million emergency department visits across hospitals.

The clinics segment accounted for a considerable share of the global market, and are expected to register a higher CAGR during the forecast timeframe, owing to the increasing number of clinics offering ultrasound tests and the rising adoption of ultrasound devices in specialty clinics to enhance patient care delivery across the globe.

- According to United States Census Bureau and National Center for Health Statistics (NCHS) data, in March 2023, there were about 2,000 retail health clinics (RHCs) in the U.S., between 2018 and 2020 that provided convenient health services to the U.S. population.

REGIONAL INSIGHTS

On the basis of region, the global market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Point-of-care Ultrasound Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 0.59 billion in 2025, representing 39.43% of the global market landscape, and is expected to reach USD 0.67 billion in 2026. The dominance is attributed to leading players engaged in the introduction of innovative and compact ultrasound devices in the market. Moreover, rising awareness and adoption of ultrasound devices by healthcare professionals for point-of-care applications, further augmented the North America market growth. The U.S. market is projected to reach USD 0.63 billion by 2026.

- In February 2024, Butterfly Network unveiled the commercial debut of its third-generation hand-held point-of-care ultrasound system, the Butterfly iQ3, in the U.S.

- According to a data published by Cureus in April 2021, Moore et al., and Sanders et al. research estimated that POCUS devices availability in the U.S. community Emergency Department increased from 19% to 52% over a six-year period from 2014 to 2020.

- For instance, according to the Global Cancer Observatory (GLOBOCAN), in 2020, it was estimated that the U.S. would record approximately 2,281,658 new cancer cases by 2020.

Europe

Europe contributed 26.34% to the global market in 2025, with a valuation of USD 0.39 billion, and is expected to reach USD 0.45 billion in 2026. Europe is anticipated to be the second-largest market in the forecast period. The growth is attributed to factors such as rising number of patients undergoing diagnostic screening for several ailments, such as cardiovascular and respiratory diseases across the region. Moreover, increasing number of regional diagnostic centers, and hospitals offering point-of-care applications further propelled the regional market. The UK market is projected to reach USD 0.07 billion by 2026, while the Germany market is projected to reach USD 0.12 billion by 2026.

- According to the annual statistical release by National Health Service, in 2020, approximately 9.5 million ultrasound procedures are carried out annually in England.

Asia Pacific

Asia Pacific accounted for USD 0.43 billion in 2025, representing 28.67% of the global market share, and is expected to reach USD 0.49 billion in 2026. The Asia Pacific market is anticipated to register the highest CAGR in the forecast period due to increasing prevalence of chronic disorders across the region and rising potential patient population undergoing ultrasound tests across healthcare settings. The Japan market is projected to reach USD 0.18 billion by 2026, the China market is projected to reach USD 0.18 billion by 2026, and the India market is projected to reach USD 0.04 billion by 2026.

- According to data revealed by Dove Press Ltd, in September 2022, the prevalence of COPD in China was estimated as 13.7%, equating to approximately 99.9 million patients with COPD in 2020.

- According to a cohort study published by BioMed Central Ltd, in January 2023, about 5,900,818 ultrasound examinations in Australia were performed in 2020.

Latin America and Middle East & Africa

The emerging markets of Latin America, and the Middle East & Africa accounted for a comparatively lower market share but are expected to witness strong growth prospects in the forecast period due to the increasing number of outpatient healthcare centers offering diagnostic tests across the region. In 2025, Middle East & Africa held 2.36% of the global market, reaching a valuation of USD 0.04 billion, and is projected to grow to USD 0.04 billion in 2026. Latin America contributed approximately USD 0.05 billion to the global market in 2025, accounting for 3.20% share, and is expected to reach USD 0.05 billion in 2026. Moreover, the rising number of surgeries needing therapeutic interventions such as point-of-care across developing countries, further boosts the regional market growth.

- For instance, as per the United Arab Emirates Ministry of Health and Prevention, in 2020, there were around 5,369 private and public healthcare centers in UAE. Additionally, as per a similar source, the outpatient service visits in Abu Dhabi tallied up to 5,866,316 in the year 2020.

- According to an article published by Havard Review of Latin America in 2021, around 1.5 million surgical procedures are performed in Brazil annually.

List of Key Companies in Point-of-care Ultrasound Market

Robust Portfolio of GE Healthcare and Koninklijke Philips N.V. to Support Market Dominance

The global market's competitive landscape reflects the dominance of certain key players, such as GE HealthCare, Siemens Healthineers, and Koninklijke Philips N.V., which have always been prominent players in medical imaging. The rising emphasis of key players on collaborations and acquisitions with other leading players to develop technologically advanced solutions further boosted the point-of-care ultrasound market growth.

These leading players are also engaged in various R&D initiatives for the launch of technologically advanced product offerings.

- In May 2022, GE HealthCare announced to invest up to USD 50.0 million in Pulsenmore to accelerate the global adoption of ultrasound solutions and pursue FDA clearance and commercial expansion.

- In June 2020, Koninklijke Philips N.V. announced the commercial launch of Lumify in Japan, a point-of-care ultrasound system.

Some of the other key players exerting dominance on the global market include Shenzhen Mindray Bio-Medical Electronics Co., Ltd., and Hitachi Ltd., owing to their diversified and robust product portfolio for ultrasound systems in point-of-care applications. Furthermore, some of the global market's emerging companies are China-based, including, CHISON Medical Technologies Co., Ltd., and EDAN Instruments. These companies’ strategic executions such as high emphasis on technological advancements, and expansion of existing product portfolios are anticipated to aid their efforts to drive their market revenue share in the forecast period.

- In June 2021, CHISON Medical Technologies Co., Ltd., launched the updated version of XBit 90 to compete with the new generation devices in the market. The updated version was configured with Artificial intelligence, Wave Matching, and Noise Reduction for cutting-edge resolution imaging.

Moreover, other existing players such as FUJIFILM Sonosite, Inc., and TERASON DIVISION TERATECH CORPORATION with a robust focus on R&D initiatives with other organizations to support the market, further propelled the global point-of-care ultrasound market share.

- In September 2020, FUJIFILM Sonosite, Inc., announced a research grant with the CHEST Foundation to investigate the role of point-of-care ultrasound technology in COVID-19 patients. The company announced two grants of USD 30,000 to the CHEST Foundation in support of the joint program and also donated Sonosite PX ultrasound systems to the selected research award sites.

LIST OF KEY COMPANIES PROFILED:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- FUJIFILM Sonosite, Inc. (U.S.)

- ALPINION MEDICAL SYSTEMS Co., Ltd. (South Korea)

- Hitachi Ltd. (Japan)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- EDAN Instruments (China)

- TERASON DIVISION TERATECH CORPORATION (U.S.)

- CHISON Medical Technologies Co., Ltd. (China)

- Healcerion Co., Ltd. (South Korea)

- Butterfly Network, Inc. (U.S.)

- Becton, Dickinson, and Company (U.S.)

- Zimmer MedizinSysteme GmbH (Germany)

- Teknova Medical Systems Co., Ltd. (China)

- Advanced Instrumentations (Florida)

- DRE Medical (U.S.)

- DRAMIŃSKI S. A. (Poland)

- Shenzhen AnaSonic Bio-Medical Technology Co., Ltd. (China)

- Clarius (Canada)

KEY INDUSTRY DEVELOPMENTS:

- November 2022 - Koninklijke Philips N.V., launched a compact premium quality cart-based point-of-contact ultrasound ‘Compact 5000’ at the Radiological Society of North America (RSNA), annual meeting.

- September 2022 - FUJIFILM Sonosite, Inc., announced the launch of Sonosite LX in Europe.

- February 2022 - Butterfly Network, Inc., introduced Butterfly Blueprint in U.S., which includes a set of optional services and software, including Caption Health’s AI-guided software. This software helps healthcare professionals without sonography expertise to capture and interpret cardiac ultrasound images for early detection of disease.

- October 2020 – Butterfly Network Inc., announced the launch of its next-generation Butterfly iQ+ point-of-care-ultrasound technology that can turn a smartphone into a diagnostic imaging system.

- October 2020 – Shenzhen Mindray Bio-Medical Electronics Co., Ltd., announced the launch of their latest ultrasound product, the ME8 Ultrasound System. The product offering has a weight and thickness of just 6.6 pounds and 1.7 inches, respectively, and the product’s main unit is one of the industry's lightest and thinnest laptop-based machines.

REPORT COVERAGE

The global market research report provides a detailed analysis of the market. It focuses on key aspects such as disease burden - cancer, the incidence of prostate cancer – by key region, disease burden – cardiovascular diseases, healthcare overview – selective countries, number of hospital admissions – key countries, aging population data, and key mergers, acquisitions & partnerships. Besides this, the report offers insights into the market trends and highlights vital industry dynamics. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the global market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 15.93% from 2026-2034 |

|

Unit |

Value (USD billion), and Volume (Units) |

|

Segmentation |

By Product

|

|

By End user

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.5 billion in 2025 and is projected to reach USD 5.56 billion by 2034.

In 2025, the North America market stood at USD 0.59 billion.

Growing at a CAGR of 15.93%, the market will exhibit steady growth over the forecast period (2026-2034).

Cart-based segment is expected to be the leading segment in this market during the forecast period.

Increasing demand for point-of-care imaging, increasing technological advancements in these product offerings, and new product launches are major factors driving the markets growth.

GE Healthcare and Koninklijke Philips N.V., are the major players in the global market.

North America dominated the market in 2026.

New product launches by key companies, increasing shift from inpatient to outpatient care, and a strong prevalence of chronic diseases necessitate effective imaging. These factors are expected to drive the adoption of products in the global market.

- 2021-2034

- 2025

- 2021-2024

- 214

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us