Chocolate Flavors Market Size, Share & Industry Analysis, By Type (Dark, White, Milk, and Others), By Nature (Natural and Synthetic), By Form (Liquid, Powder, and Paste), By Application (Bakery Products, Dairy Products, Beverages, Frozen Desserts, Snacks, and Others), and Regional Forecast, 2026-2034

(Offer valid till 31st Jul 2026)

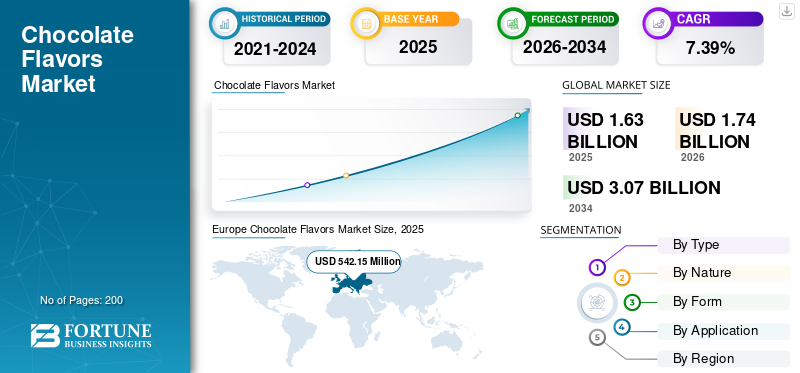

Chocolate Flavors Market Size and Future Outlook

The global chocolate flavors market size was valued at USD 1,630.74 million in 2025. The market is projected to grow from USD 1,740.17 million in 2026 to USD 3,079.38 million by 2034, exhibiting a CAGR of 7.39% during the forecast period. Europe dominated the chocolate flavors market with a market share of 33.25% in 2025.

Chocolate flavors are widely used across bakery, confectionery, dairy, beverage, and snack applications to enhance taste, aroma, and product appeal. The market is witnessing steady growth driven by the increasing consumption of processed and indulgent food products, rising demand for premium and clean-label ingredients, and continuous innovation in flavor formulations. Additionally, manufacturers are focusing on natural cocoa-based extracts and customized flavor profiles to meet the evolving consumer preferences for authentic and rich taste experiences.

The global market is led by key companies, including Givaudan, Firmenich SA, International Flavors & Fragrances Inc. (IFF), Symrise AG, and Sensient Technologies Corporation. These companies are competing through innovation in natural flavors, clean-label formulations, and customized application-specific solutions.

Download Free sample to learn more about this report.

Chocolate Flavors Market KEY TAKEAWAYS

- 2025 Market Size: USD 1,630.74 million

- 2026 Market Size: USD 1,740.17 million

- 2034 Forecast Market Size: USD 3,079.38 million

- CAGR: 7.39% from 2026–2034

- Europe dominated the chocolate flavors market with a 33.25% share in 2025.

- The dark chocolate segment is projected to grow at the fastest CAGR of 8.31% during the forecast period.

- The natural segment held the largest market share in 2025 and is projected to grow at the fastest CAGR of 8.42%.

Asia Pacific

Asia Pacific reached USD 388.96 million in 2025 and is the fastest-growing region due to rising processed food consumption and disposable incomes.

North America

North America reached USD 454.87 million in 2025, supported by strong demand for premium bakery and confectionery products.

Europe

Europe reached USD 542.15 million in 2025, driven by its established confectionery industry and high chocolate consumption.

U.S.

The market reached USD 358.11 million in 2025, fueled by demand for flavored snacks, beverages, and dairy products.

Japan

The market is supported by strong demand for premium chocolates, seasonal confectionery, and innovative flavor formulations.

Read More

Chocolate Flavors Market Trends

Growing Demand for Premium and Clean-Label Flavor Ingredients to Shape Industry Trends

Consumers are increasingly seeking premium-quality food products with authentic taste and clean-label ingredients, which is significantly influencing the market. The shift toward natural and minimally processed ingredients has encouraged manufacturers to develop cocoa-based natural extracts and organic flavor formulations. In addition, the growing popularity of artisanal bakers, gourmet desserts, and premium beverages is further driving the demand for chocolate flavors. Companies are also investing in advanced flavor encapsulation technologies and plant-based formulations to cater to evolving dietary preferences and sustainability trends.

- For instance, in October 2024, Puratos launched a new plant‑based, whippable Ambiante Chocolate Flavor designed specifically for toppings and fillings in patisserie and desserts. It is a 100% dairy‑free, ready‑to‑whip topping with no artificial flavors or colors (NAFNAC), using cocoa powder from Puratos’s Cacao‑Trace sustainable cocoa program.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Global Consumption of Processed and Confectionery Products to Support Market Growth

The chocolate flavors market growth is closely tied to the expanding global consumption of processed foods, particularly confectionery, bakery, and ready-to-eat products. Chocolate remains one of the most universally preferred flavors, making it a core ingredient across multiple food categories. Urbanization and changing lifestyles are further accelerating the consumption of packaged foods. As consumers increasingly opt for convenient, indulgent, and ready-to-consume products, manufacturers are incorporating chocolate flavors extensively to enhance product appeal and differentiation.

- According to the Food and Agriculture Organization (FAO), the global cocoa production exceeded 5.0 million metric tons in 2023, reflecting sustained demand from chocolate and cocoa-based industries. The USDA highlights that global chocolate consumption continues to grow steadily, with emerging markets in Asia and Latin America witnessing higher per capita consumption growth rates compared to mature markets.

Market Restraints

Volatility in Cocoa Prices and Climate-Driven Supply Risks to Restrict Market Growth

One of the most critical challenges in the market is the volatility in cocoa prices, which directly impacts production costs, ethical sourcing, and pricing strategies. Such volatility affects profitability and also creates uncertainty in long-term supply contracts and pricing structures. Smaller manufacturers are particularly impacted due to their limited ability to absorb cost fluctuations.

- According to the International Cocoa Organization (ICCO), cocoa production is highly concentrated, with Côte d’Ivoire and Ghana accounting for nearly 60% of the global supply, making the market vulnerable to regional disruptions.

Market Opportunities

Rising Demand from Emerging Foodservice and QSR Sectors to Bring New Growth Avenues

The escalating demand from emerging foodservice and quick-service restaurant (QSR) sectors is a structurally significant growth driver for the market, supported by expansion in out-of-home consumption, menu innovation, and the scaling of standardized ingredient procurement.

- According to USDA estimates and industry databases, the global foodservice sales exceeded USD 3.5 to 4.0 trillion in 2024, with developing regions contributing a disproportionately higher growth rate (5–8% annually).

As international and regional chains expand their footprint, the need for consistent and scalable chocolate flavor solutions is expected to increase.

SEGMENTATION ANALYSIS

By Type

Milk Chocolate Segment Dominated the Market Due to Wide Application across Bakery, Dairy, and Confectionery Products

Based on type, the market is segmented into dark, white, milk, and others.

The milk chocolate segment dominated the global chocolate flavors market share, valued at USD 835.31 million in 2025. The dominance is supported by its balanced sweetness, creamy profile, and strong consumer preference across mass and premium product categories. It is extensively used in bakery products, flavored milk, confectionery, and snacks, making it the most commercially viable flavor type.

The dark chocolate segment is projected to grow at the fastest CAGR of 8.31% during 2026–2034, driven by an increasing demand for high-cocoa, antioxidant-rich, and premium formulations.

To know how our report can help streamline your business, Speak to Analyst

By Nature

Natural Segment Dominated the Market Due to Rising Demand for Clean-Label and Organic Ingredients

On the basis of nature, the market is segmented into natural and synthetic.

The natural segment held the leading position, reaching USD 934.93 million in 2025, and is expected to grow at the fastest CAGR of 8.42% during the forecast period. The segment growth is driven by soaring consumer preference for clean-label, minimally processed, and plant-based ingredients. Regulatory support and increasing awareness regarding artificial additives are further supporting segment growth.

The synthetic segment accounted for a substantial share of the global market, valued at USD 695.81 million in 2025. This is driven primarily by its cost-effectiveness and consistent flavor profile across large-scale food production.

By Form

Liquid Segment Dominated the Market Due to Ease of Application and High Usage across Food and Beverage Products

On the basis of form, the market is segmented into liquid, powder, and paste.

The liquid segment dominated the global market with a value of USD 676.91 million in 2025. The dominance is owing to its superior solubility, ease of blending, and widespread use in beverages, dairy products, and processed foods. Liquid chocolate flavors excel in versatility, allowing seamless integration into beverages, bakery items, dairy products, and confectionery without needing reconstitution, unlike powders that can clump or lose potency during processing. Manufacturers favor them for their convenience as ready-to-use ingredients, reducing production time and equipment needs while ensuring homogeneous mixing and consistent taste in end products such as sauces, coatings, and frozen desserts.

The paste segment is projected to grow at the fastest CAGR of 8.11% during 2026–2034. The segment is supported by the increasing demand in premium confectionery and artisanal bakery products where rich texture and concentrated flavor are essential.

By Application

Bakery Products Segment Dominated the Market Due to High Demand for Chocolate-Flavored Baked Goods

On the basis of application, the market is segmented into bakery products, dairy products, beverages, frozen desserts, snacks, and others.

The bakery products segment dominated the market, valued at USD 348.01 million in 2025. This is driven by the strong global demand for cakes, pastries, cookies, and other chocolate-based baked items. High bakery consumption outpaces other applications such as confectionery or dairy, as baked goods are staples in households and foodservice worldwide, with chocolate flavors boosting appeal in items such as muffins, brownies, and bread. Chocolate's heat-stable properties make it ideal for baking processes, where it integrates evenly for consistent flavor and texture, unlike more volatile uses in beverages.

The beverages segment is expected to witness the fastest CAGR of 8.75% during the forecast period.

Chocolate Flavors Market Regional Outlook

Regionally, the market has been studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe Chocolate Flavors Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The Europe market accounted for the largest share, valued at USD 542.15 million in 2025, and is projected to reach USD 951.66 million by 2034. The market is likely to register a CAGR of 6.52% over 2026–2034. The region benefits from a strong chocolate consumption culture and an established confectionery industry.

Germany Chocolate Flavors Market

The Germany market was valued at approximately USD 138.89 million in 2025, supported by the high consumption of chocolate confectionery and bakery products.

U.K. Chocolate Flavors Market

The U.K. market reached around USD 84.66 million in 2025, driven by the demand for premium desserts and flavored beverages.

North America

North America was valued at USD 454.87 million in 2025 and is projected to reach USD 891.82 million by 2034, growing at a CAGR of 7.84% during 2026–2034. The segment growth is driven by the high consumption of bakery and confectionery products, along with strong demand for premium and clean-label ingredients.

U.S. Chocolate Flavors Market

The U.S. dominates the region, valued at approximately USD 358.11 million in 2025. This is supported by the strong demand for flavored snacks, beverages, and dairy products, along with continuous innovation in premium chocolate-based formulations.

Asia Pacific

The Asia Pacific market was valued at USD 388.96 million in 2025 and is projected to reach USD 809.77 million by 2034, growing at a CAGR of 8.56% over 2026–2034, making it the fastest-growing region. The regional expansion is supported by the rising disposable incomes, urbanization, and expanding processed food consumption.

China Chocolate Flavors Market

The China market accounted for the largest market in the region, valued at approximately USD 142.86 million in 2025. The dominance is driven by the growing demand for confectionery and western-style bakery products.

South America and the Middle East & Africa

The South America market reached USD 131.46 million in 2025 and is projected to reach USD 245.22 million by 2034, registering a CAGR of 7.25% over 2026–2034. The Middle East & Africa market was valued at USD 113.31 million in 2025 and is projected to reach USD 180.91 million by 2034, expanding at a CAGR of 5.39% over the forecast period.

UAE Chocolate Flavors Market

The UAE market was valued at approximately USD 28.08 million in 2025, driven by strong demand for premium bakery products, desserts, and chocolate-based beverages.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Natural Ingredients, Flavor Innovation, and Customization Strategies to Strengthen their Footing

The global chocolate flavors market is moderately fragmented, with leading flavor manufacturers competing through innovation in natural formulations, customized solutions, and application-specific flavor development. Companies are investing in R&D to develop clean-label and sustainable flavor solutions while expanding their presence in emerging markets.

Key Players in the Chocolate Flavors Market

|

Rank |

Company Name |

|

1 |

Givaudan S.A. |

|

2 |

Firmenich SA |

|

3 |

International Flavors & Fragrances Inc. (IFF) |

|

4 |

Symrise AG |

|

5 |

Sensient Technologies Corporation |

List of Key Chocolate Flavors Companies Profiled

- Givaudan (Switzerland)

- Firmenich SA (Switzerland)

- International Flavors & Fragrances Inc. (U.S.)

- Symrise AG (Germany)

- Sensient Technologies Corporation (U.S.)

- Takasago International Corporation (Japan)

- Mane SA (France)

- Kerry Group plc (Ireland)

- Archer Daniels Midland Company (U.S.)

- Döhler Group (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Mondelēz International partnered with Aston University to pioneer membrane-based filtration technologies for chocolate innovation. This collaboration applies advanced biological membrane proteins to filter and refine food compounds, enabling high-cocoa chocolate with enhanced flavors and no added sugar.

- February 2026: Puratos USA announced plans to launch the world's first professional chocolate products made with cultured cocoa, targeting full commercial availability in the late 2026 U.S. market. This product complements traditional cocoa farming by addressing climate-related supply challenges through cellular agriculture techniques that replicate cocoa's flavor, melting behavior, viscosity, and performance.

- December 2025: General Mills recently launched Reese’s Puffs Dark Chocolate Naturally Flavored cereal, marking the first major flavor change for the brand since its 1994 debut. This variant builds on the classic peanut butter and chocolate taste by incorporating Hershey’s cocoa and real Reese’s Peanut Butter for a richer, deeper dark chocolate profile while keeping the signature crunchy texture.

- October 2024: Cargill launched a new cocoa production line at its Gresik facility in Indonesia on October 1, 2024, to address the rising Asian demand for indulgent foods such as bakery items, ice cream, chocolate confectionery, and café-style beverages.

- April 2024: Barry Callebaut launched its MALEO cocoa powder line across Asia Pacific to deliver enhanced indulgence with reduced usage amid high cocoa prices. The standard 10/12 MALEO variant provides intense brown color, richer chocolatey flavor, and long-lasting cocoa sensation for visually appealing applications.

REPORT COVERAGE

The global chocolate flavors market report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.39% from 2026 to 2034 |

| Unit | Value (USD Million) |

|

Segmentation |

By Type

|

|

By Nature

|

|

|

By Form

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 1,630.74 million in 2025 and is anticipated to reach USD 3,079.38 million by 2034.

The global market will exhibit steady growth at a CAGR of 7.39% over the forecast period.

By form, the liquid segment led the market in 2025.

Europe held the largest market share in 2025.

The rising global consumption of processed and confectionery products is a key factor supporting market growth.

Givaudan, Firmenich SA, International Flavors & Fragrances Inc. (IFF), Symrise AG, and Sensient Technologies Corporation are the leading players in the market.

The growing demand for premium and clean-label flavor ingredients is a key industry trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 31st Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us