Climate Change Consulting Market Size, Share & Industry Analysis, By Service Type (Carbon & Emissions Management, Decarbonization & Net-Zero Strategy, Climate Risk & Resilience Consulting, Climate Policy & Regulatory Compliance, Climate Finance & Carbon Markets Advisory, and Others), By Organization Size (Large Enterprises, Mid-Sized Enterprises, Small & Medium Enterprises (SMEs), and Others), By End User (Energy & Utilities, Manufacturing & Heavy Industry, Financial Services, Government & Public Sector, Corporate Enterprises, and Others), Regional Forecast, 2026-2034

Climate Change Consulting Market Size and Future Outlook

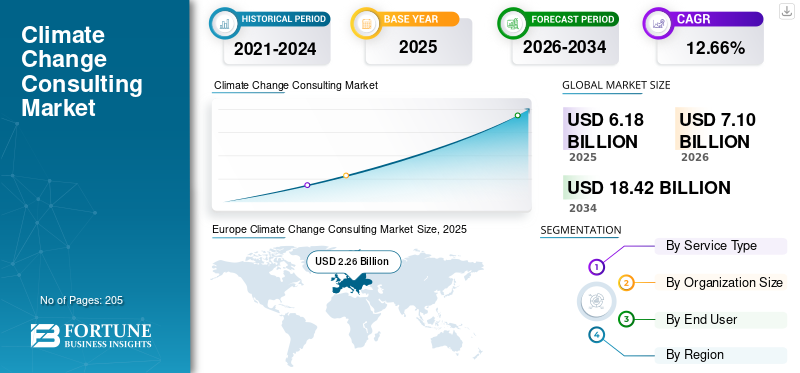

The global climate change consulting market size was valued at USD 6.18 billion in 2025. The market is projected to grow from USD 7.10 billion in 2026 to USD 18.42 billion by 2034, exhibiting a CAGR of 12.66% during the forecast period. Europe dominated the climate change consulting market with a market share of 56.77% in 2025.

Climate change consulting has emerged as a specialized advisory domain focused on helping organizations quantify emissions, comply with evolving climate regulations, and execute decarbonization strategies across complex value chains. Unlike broader sustainability consulting, it is highly technical, involving Scope 3 emissions modeling, climate scenario analysis, carbon pricing mechanisms, and alignment with frameworks such as CSRD, ISSB, and SBTi.

The market is increasingly driven by sectors with high transition exposure, such as manufacturing, energy, and financial services, where climate considerations are now embedded into capital allocation, risk management, and supply chain decisions. Consulting engagements are shifting from one-time assessments to multi-year implementation programs, reflecting the move from target-setting to execution. In addition, the rapid expansion of mandatory climate disclosures and supply chain accountability requirements, particularly in Europe and North America. Regulations such as EU CSRD are extending compliance obligations to thousands of mid-sized firms, forcing companies to engage consultants for emissions tracking, audit readiness, and reporting standardization.

- For instance, in March 2023, the European Commission advanced the implementation of the Corporate Sustainability Reporting Directive (CSRD), significantly expanding the number of companies required to disclose detailed climate risk-related data. This regulatory shift triggered a surge in demand for climate change consulting services, as organizations across Europe engaged consultants to support GHG emissions accounting, Scope 3 assessments, and compliance alignment. Consulting firms were increasingly mandated to assist clients in building robust reporting systems and ensuring audit-ready climate disclosures.

Some of the leading companies operating in the industry include Jacobs Solutions Inc., AECOM, WSP Global Inc., and others. Jacobs Solutions Inc. is a U.S.-based professional services firm specializing in engineering, consulting, and technical solutions across infrastructure, energy, and environmental sectors. The company provides advanced advisory services in sustainability, climate resilience, and decarbonization, supporting governments and corporations in addressing complex environmental and climate-related challenges.

Download Free sample to learn more about this report.

Climate Change Consulting Market Key Takeaways

- 2025 Market Size: USD 6.18 Billion

- 2026 Market Size: USD 7.10 Billion

- 2034 Forecast Market Size: USD 18.42 Billion

- CAGR: 12.66% from 2026–2034

- Europe dominated the climate change consulting market with a 56.77% share in 2025.

- The climate finance & carbon markets advisory segment is expected to grow at a CAGR of 13.95% during the forecast period.

- The financial services segment is expected to grow at a CAGR of 15.60% during the forecast period.

Asia Pacific

Asia Pacific generated USD 1.35 billion in 2025.

North America

North America reached USD 1.95 billion in 2025 and is expected to grow to USD 2.23 billion in 2026.

Europe

Europe generated USD 2.26 billion in 2025 and is projected to grow at a 12.92% CAGR.

U.S.

The climate change consulting market reached USD 1.75 billion in 2025.

Japan

The climate change consulting market reached USD 0.30 billion in 2025.

Read More

CLIMATE CHANGE CONSULTING MARKET TRENDS

Shift from Disclosure-focused Engagement to Execution-Led Climate Consulting is the Key Market Trend

The climate change consulting market growth is driven by a clear transition from disclosure-focused engagements to execution-driven advisory services. While early demand was centered on carbon footprinting and compliance with frameworks such as TCFD (Task Force on Climate-related Financial Disclosures) and CDP (Carbon Disclosure Project), organizations are now moving toward implementing decarbonization strategies, particularly Scope 3 emissions reduction, and supply chain transformation. This shift is driven by tightening regulations such as the EU CSRD (Corporate Sustainability Reporting Directive), which require not just reporting but verifiable action plans and measurable progress.

Consulting firms are increasingly engaged in multi-year programs involving abatement pathway design, supplier engagement models, and integration of climate metrics into financial decision-making. Additionally, there is a growing need for scenario-based climate risk modeling linked to capital allocation and asset valuation, especially among financial institutions and asset-heavy industries.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Scope 3 Accountability Drives Market Expansion

A key driver in the climate change consulting market is the rapid expansion of Scope 3 emissions accountability across global value chains, which is significantly increasing the complexity of corporate climate strategies. Unlike Scope 1 and Scope 2 emissions, Scope 3 requires companies to collect, verify, and manage emissions data from suppliers, logistics partners, and end-use phases, often spanning multiple geographies and regulatory environments.

This has created strong demand for consulting services focused on supplier engagement frameworks, emissions data standardization, and value chain decarbonization roadmaps. Large corporations are increasingly mandating emissions disclosure and reduction targets for their suppliers, particularly in sectors such as automotive, consumer goods, and electronics. As a result, even mid-tier suppliers are being pulled into structured climate programs, accelerating consulting adoption in emerging markets.

MARKET RESTRAINTS

Data Availability and Standardization Challenges Across Value Chains to Hamper Market Demand

A major restraint in the market is the lack of reliable, standardized emissions data across complex value chains, which limits the effectiveness of consulting engagements. Scope 3 emissions, in particular, depend on supplier-level data that is often incomplete, inconsistent, or based on estimates rather than actual measurements. This creates significant challenges in building accurate decarbonization strategies and undermines confidence in reported outcomes.

Additionally, differences in reporting frameworks, methodologies (GHG Protocol vs regional standards), and data collection capabilities across geographies lead to inconsistencies in analysis and benchmarking. Many mid-sized firms and suppliers lack the internal systems required for real-time emissions tracking, increasing dependency on assumptions and proxies.

MARKET OPPORTUNITIES

Growing Demand for Advisory Services to Present Several Market Opportunities

A significant opportunity in the climate change consulting market lies in the integration of climate metrics into financial planning, investment decisions, and corporate valuation frameworks. As organizations increasingly link climate performance with access to capital, cost of financing, and investor expectations, there is a growing demand for advisory services that bridge sustainability and finance. Consultants are now supporting companies in embedding climate-adjusted financial models, shadow carbon pricing, and climate scenario analysis into capital expenditure (CAPEX) planning and portfolio management.

In addition, the rise of sustainability-linked loans (SLLs) and green bonds is creating demand for third-party validation, impact assessment, and performance tracking, expanding the scope of consulting services. This convergence of finance and climate strategy opens new revenue streams, as organizations seek data-driven insights to balance profitability with decarbonization commitments, positioning climate consulting as a critical enabler of long-term financial resilience.

MARKET CHALLENGES

Lack of Technical Expertise to Hinder Market Growth

A critical challenge in the market is the limited availability of skilled professionals with deep technical expertise in climate science, carbon accounting, and sector-specific decarbonization pathways. Unlike traditional consulting, climate advisory requires a combination of domain knowledge (e.g., energy systems, industrial processes), regulatory understanding, and advanced data analytics capabilities, which are not widely available in the talent pool.

As demand accelerates, consulting firms face difficulties in scaling teams capable of delivering complex engagements such as Scope 3 modeling, climate scenario analysis, and integration of climate metrics into financial systems. This talent shortage leads to higher project costs, longer delivery timelines, and inconsistent quality across regions, particularly in emerging markets.

Segmentation Analysis

By Service Type

Decarbonization & Net-Zero Strategy Segment Dominated Due to Increasing Regulatory Mandates

Based on service type, the market is classified into carbon & emissions management, decarbonization & net-zero strategy, climate risk & resilience consulting, climate policy & regulatory compliance, climate finance & carbon markets advisory, and others.

In 2025, the decarbonization & net-zero strategy captured the dominant market share due to the urgent need for organizations to transition from target-setting to measurable emissions reduction pathways. With increasing regulatory mandates such as EU CSRD (Corporate Sustainability Reporting Directive) and global net-zero commitments, companies are required to develop detailed, time-bound decarbonization roadmaps rather than standalone disclosures.

The climate finance & carbon markets advisory segment is expected to grow at a CAGR of 13.95% during the study period.

To know how our report can help streamline your business, Speak to Analyst

By Organization Size

Large Enterprises Dominated Due to Their Greater Exposure to Regulatory Requirements

Based on organization size, the market is classified into large enterprises, mid-sized enterprises, Small & Medium Enterprises (SMEs), and others.

In 2025, the large enterprises segment dominated the global market due to their greater exposure to regulatory requirements, investor scrutiny, and global supply chain pressures. These organizations operate across multiple geographies, making them subject to complex frameworks such as EU CSRD (Corporate Sustainability Reporting Directive), ISSB (International Sustainability Standards Board), and TCFD (Task Force on Climate-related Financial Disclosures).

The mid-sized enterprises segment is expected to grow at a CAGR of 14.34% during the study period.

By End User

Manufacturing & Heavy Industry Segment Dominated Due to Increasing Regulatory Scrutiny

On the basis of the segmentation of the end user, the market is classified into energy & utilities, manufacturing & heavy industry, financial services, government & public sector, corporate enterprises, and others.

In 2025, the manufacturing & heavy industry segment dominated the global market due to its significant contribution to global greenhouse gas emissions and increasing regulatory scrutiny. Sectors such as steel, cement, chemicals, and automotive face intense pressure to decarbonize operations while maintaining cost competitiveness, requiring specialized consulting support. These industries have complex production processes and high energy intensity, making emissions reduction technically challenging and capital-intensive.

The financial services segment is expected to grow at a CAGR of 15.60% during the study period.

Climate Change Consulting Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the Middle East & Africa, and Latin America.

North America

Europe Climate Change Consulting Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market in 2025 was valued at USD 1.95 billion and is expected to maintain its significant share in 2026 with USD 2.23 billion. North America’s market is primarily driven by the expansion of SEC climate disclosure requirements, which are compelling companies to develop audit-ready emissions reporting systems and integrate climate risk into financial filings. Additionally, increasing pressure from institutional investors and ESG-linked financing mechanisms is pushing organizations to incorporate climate metrics into capital allocation and valuation models.

U.S. Climate Change Consulting Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.75 billion in 2025, accounting for roughly 28.32% of the global market size.

Europe

Europe dominates the market and is projected to record a CAGR of 12.92% in the coming years. The market reached a valuation of USD 2.26 billion in 2025. Europe’s market is driven by the implementation of the Corporate Sustainability Reporting Directive (CSRD), which significantly expands the number of companies requiring detailed, auditable climate disclosures. Additionally, the EU Taxonomy regulation is pushing firms to align investments with sustainable activity classifications, increasing demand for technical advisory.

Germany Climate Change Consulting Market

The German market in 2025 reached around USD 0.60 billion 2025 and is estimated at around USD 0.69 billion by 2026, representing roughly 9.57% of the global revenues. Market demand is driven by its high concentration of energy-intensive industries such as automotive, chemicals, and manufacturing, which require complex decarbonization pathways.

Asia Pacific

Asia Pacific reached USD 1.35 billion in 2025, driven by increasing alignment with global supply chain decarbonization requirements, particularly in export-oriented economies. Additionally, countries such as Japan and Australia are advancing mandatory climate disclosures and net-zero policies, while emerging markets such as India and Southeast Asia are witnessing rising demand for Scope 3 and transition advisory.

India Climate Change Consulting Market

The Indian market in 2025 stood at around USD 0.22 billion, accounting for roughly 3.64% of global revenues. Market demand is increasing due to growing pressure from global clients to meet Scope 3 emissions and ESG compliance requirements, particularly in the manufacturing and IT sectors.

China Climate Change Consulting Market

China’s market is projected to be significant worldwide, with 2025 revenues standing at around USD 0.39 billion, representing roughly 6.33% of the global market.

Japan Climate Change Consulting Market

The Japanese market in 2025 stood at around USD 0.30 billion, accounting for roughly 4.89% of global revenues.

Latin America

The Latin America market reached a valuation of USD 0.20 billion in 2025 and is expected to witness moderate growth in this market during the forecast period. The market is driven by growing participation in voluntary carbon markets and increasing demand for carbon offset project validation, particularly in Brazil and Chile.

Brazil Climate Change Consulting Market

Brazil's market reached around USD 0.97 billion in 2025, representing roughly 1.57% of the market.

Middle East & Africa

The Middle East & Africa market reached a valuation of USD 0.41 billion in 2025 and is expected to witness significant growth in this market during the forecast period, driven by large-scale national decarbonization initiatives and energy transition programs, particularly in the GCC countries, focusing on hydrogen and carbon management. Additionally, increasing climate financing and infrastructure resilience projects across Africa are creating demand for policy advisory and emissions management consulting.

GCC Climate Change Consulting Market

The GCC market reached around USD 0.21 billion in 2025, representing roughly 3.35% of the global market sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Major players focus on Collaborations to boost their Market Share

The global market holds a consolidated market structure, constituting prominent players such as Jacobs Solutions Inc., AECOM, WSP Global Inc., and others. Companies operating in the market are adopting targeted growth strategies focused on strengthening their product portfolio, technical capability, expanding manufacturing presence, and other areas.

- For instance, in June 2023, Jacobs Solutions Inc. expanded its climate consulting portfolio by supporting U.S. federal agencies in developing climate resilience and decarbonization strategies for infrastructure systems. The engagement focused on integrating climate risk modeling and emissions reduction pathways into large-scale infrastructure planning.

Other key players in the global market include PwC (PricewaterhouseCoopers), Ernst & Young (EY), KPMG International, McKinsey & Company, Boston Consulting Group (BCG), and others. These companies are expected to prioritize new product launches and collaborations to increase their global climate change consulting market share during the forecast period.

LIST OF KEY CLIMATE CHANGE CONSULTING COMPANIES PROFILED

- Jacobs Solutions Inc. (U.S.)

- AECOM (U.S.)

- WSP Global Inc. (Canada)

- Stantec Inc. (Canada)

- Ramboll Group A/S (Denmark)

- Accenture plc (Ireland)

- Deloitte Touche Tohmatsu Limited (U.K.)

- PwC (PricewaterhouseCoopers) (U.K.)

- Ernst & Young (EY) (U.K.)

- KPMG International (Netherlands)

- McKinsey & Company (U.S.)

- Boston Consulting Group (BCG) (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2024: WSP Global Inc. announced its involvement in delivering climate transition advisory services for industrial clients in North America, focusing on Scope 3 emissions and supply chain decarbonization strategies. The project included emissions data modeling, supplier engagement frameworks, and integration of climate targets into corporate strategy, reinforcing WSP’s capabilities in complex, multi-stakeholder climate consulting engagements.

- January 2024: Ramboll Group A/S supported European industrial clients in implementing decarbonization roadmaps aligned with EU climate regulations, including the Corporate Sustainability Reporting Directive (CSRD). The consulting engagement focused on carbon accounting, abatement cost analysis, and regulatory compliance strategies, highlighting Ramboll’s expertise in navigating complex European climate policy frameworks.

- November 2023: Accenture expanded its climate consulting capabilities by launching advanced AI-driven carbon intelligence solutions to support enterprises in real-time emissions tracking and net-zero strategy execution. The initiative aimed to help organizations integrate climate data into operational and financial systems, enhancing decision-making and accelerating decarbonization efforts across global supply chains.

- September 2023: AECOM was selected to provide climate adaptation and sustainability consulting services for major urban infrastructure projects in Europe. The company focused on net-zero pathway development, carbon footprint analysis, and climate risk mitigation strategies for cities undergoing green transitions.

- August 2023: Stantec Inc. partnered with municipal authorities in Canada to provide climate risk assessment and net-zero transition consulting for public infrastructure. The project emphasized climate scenario analysis, emissions reduction planning, and resilience integration into urban development.

REPORT COVERAGE

The global climate change consulting market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.66% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, Organization Size, End User, and Region |

| By Service Type |

|

| By Organization Size |

|

| By End User |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.18 billion in 2025 and is projected to reach USD 18.42 billion by 2034.

In 2025, the market value stood at USD 2.26 billion.

The market is expected to exhibit a CAGR of 12.66% during the forecast period.

By service type, the decarbonization & net-zero strategy segment led the market.

Expansion of scope 3 accountability is the key factor driving the market.

Jacobs Solutions Inc., AECOM, WSP Global Inc., and others are some of the top players in the market.

Europe dominates the market.

Shift from disclosure-focused engagement to execution-led climate consulting is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us