Cling Wrap Market Size, Share & Industry Analysis, By Material Type (Polyethylene (PE), Polyvinyl Chloride (PVC), Bio-based & Biodegradable Films), By Product Type (Manual/Handheld Wrap and Machine Wrap), By Thickness (Below 10 Microns, 10–15 Microns, and Above 15 Microns), By Application (Food Packaging, Household Storage, Industrial Packaging), By End User (Residential/Households, Foodservice Industry, Supermarkets & Hypermarkets), By Distribution Channel (Convenience Stores, Online / E-Commerce, Hypermarkets / Supermarkets, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

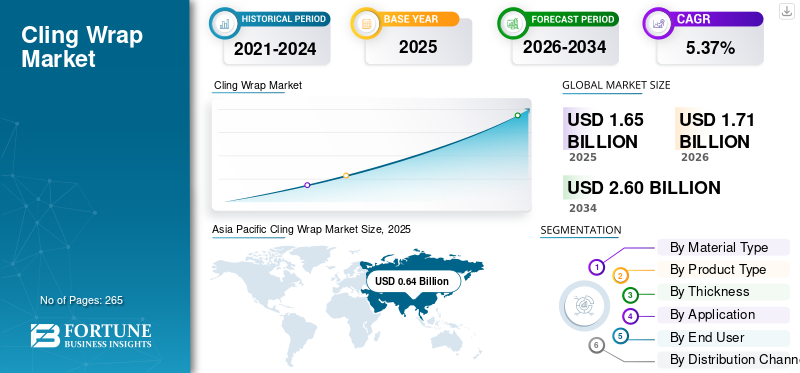

Cling Wrap Market Size and Future Outlook

The global cling wrap market size was valued at USD 1.65 billion in 2025. The market is projected to grow from USD 1.71 billion in 2026 to USD 2.60 billion by 2034, exhibiting a CAGR of 5.37% during the forecast period. Asia Pacific dominated the cling wrap market with a market share of 38.78% in 2025.

The market has been experiencing significant growth due to increased use in food preservation, convenience packaging, and reduced food waste in homes and food catering businesses. Common materials used for this purpose include polyethylene (PE) and polyvinyl chloride (PVC), which offer high moisture retention and extended food shelf life. Supermarket chains, precooked food products, and internet food delivery have also contributed to increased product consumption. According to estimates from the Food and Agriculture Organization, almost one-third of the world's food is wasted each year. Packaging manufacturers have been using eco-friendly packaging materials such as cling film, which meet legislative requirements and customer demand, particularly in North America and Europe.

A few prominent players in the market include Berry Global Inc., Amcor plc, Anchor Packaging, Mitsubishi Chemical Group Corporation, and Inteplast Group. Strategies such as extending sustainable packaging offerings, investing in innovative barrier technologies, and developing recyclable and bio-based cling films are adopted by these players to gain a strong foothold in the industry landscape. Further, partnerships with restaurants, supermarkets, cafes & delis, and e-commerce food delivery companies have shaped the industry growth curve.

Download Free sample to learn more about this report.

Cling Wrap Market Takeaways

- 2025 Market Size: USD 1.65 billion

- 2026 Market Size: USD 1.71 billion

- 2034 Forecast Market Size: USD 2.60 billion

- CAGR: 5.37% from 2026–2034

- Asia Pacific dominated the cling wrap market with a 38.78% share in 2025.

- Polyethylene (PE) segment led the market in 2025 due to its durability, flexibility, moisture resistance, and cost efficiency.

- Manual/handheld wrap segment dominated the market in 2025 owing to widespread household and retail usage.

North America

North America held the second-highest market share in 2025, reaching a valuation of USD 0.44 billion, driven by strong demand for convenient food preservation solutions.

Europe

Europe accounted for the third-largest market share in 2025, valued at USD 0.40 billion, representing 24.03% of the global market revenues.

Asia Pacific

Asia Pacific dominated the global cling wrap market in 2025, reaching a value of USD 0.64 billion, and is projected to grow at a CAGR of 6.46% during the forecast period.

U.S.

The U.S. cling wrap market reached USD 0.31 billion in 2025, accounting for approximately 18.99% of global market sales, supported by high adoption of packaged food and household storage products.

Japan

The Japan cling wrap market was valued at USD 0.11 billion in 2025, accounting for roughly 6.43% of global market revenues, supported by demand for efficient food preservation and organized retail availability.

Read More

CLING WRAP MARKET TRENDS

Rising Demand for Sustainable Cling Films to Drive Material Innovation

The need for environmental protection and the existence of strict rules on single-use plastic have led people to seek eco-friendly cling wraps in the packaging industry. The rising consumer awareness of the need for eco-friendly, compostable products is prompting players to invest more in manufacturing biodegradable polyethylene films. All this drives players to design products that are easier to recycle without compromising transparency, flexibility, or food safety. This tendency is further supported by companies in the food service industry's desire to choose sustainable packaging materials.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expanding Processed and Ready-to-Eat Food Consumption to Accelerate Product Demand

One of the main factors driving the popularity of cling films is the rapid rise in the consumption of processed and packaged foods. With changes in people's lifestyles and urbanization, there has been a great demand for the preservation and cleanliness of food. The wraps have proven to extend food shelf life, making them among the most popular choices for both customers and food suppliers. In addition, the product demand has risen significantly due to the rapid expansion of cafe & deli chains, restaurants & bakeries, and other food delivery services, which is propelling cling wrap market growth.

MARKET RESTRAINTS

Stringent Plastic Waste Regulations and Environmental Concerns May Limit Market Growth

Environmental issues related to plastic use as well as stringent government regulations to control plastic waste pose a major barrier to market growth. The traditional types of cling film, manufactured from PVC and non-biodegradable polyethylene, are dumped in landfills and pollute the oceans, prompting public criticism. Many countries have imposed bans or raised recycling standards or targets to reduce plastic use. While manufacturing more environmentally friendly cling films requires substantial investment, sourcing biodegradable inputs in large quantities is not readily available and profit margins may be reduced, leading some consumers to opt for reusable options.

MARKET OPPORTUNITIES

Growing Adoption of Bio-Based Packaging to Create New Revenue Opportunities

The gradual trend of sustainable consumer goods is presenting major growth opportunities for bio-based, compostable cling wrap. The growing conscious consumer, rising awareness of environmental issues, and more stringent government regulations advocating the use of circular packaging are prompting food packaging firms and retailers to move away from traditional plastic packaging films toward environmentally friendly alternatives. Innovation in the development of plant-based polymers, recyclable multilayer films, and biodegradable packaging is driving the increased production of sustainable food preservation materials.

MARKET CHALLENGES

Volatility in Raw Material Prices to Increase Operational Pressure

The ever-changing price trends of petroleum-based raw materials such as PE and PVC is a significant challenge for the industry. Due to their reliance on petrochemical derivatives, fluctuations in crude oil prices, supply chain disruptions, and geopolitical instability become significant factors affecting manufacturing costs. Any increase in resin prices can negatively impact manufacturers' bottom lines and raise the overall cost of products for consumers and businesses. Small-scale cling wrap manufacturers may face challenges stabilizing their prices and sourcing due to shortages of raw materials.

Segmentation Analysis

By Material Type

Cost Efficiency and High Durability to Drive the Polyethylene (PE) Segment Growth

By material type, the market is segmented into polyethylene (PE), polyvinyl chloride (PVC), bio-based & biodegradable films, and others.

The polyethylene (PE) segment led the market in 2025 due to its flexible nature, high durability, moisture repellence, and cost-effectiveness compared to other raw materials. The material is commonly used in food packaging as it ensures freshness and a long shelf life while providing a robust seal suitable for perishable goods.

The bio-based & biodegradable films segment is anticipated to rise at the fastest CAGR of 7.74% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Product Type

Widespread Household and Retail Usage to Drive Manual/Handheld Wrap Segment Growth

Based on product type, the market is divided into manual/handheld wrap and machine wrap.

The manual/handheld wrap segment dominated the market in 2025 mainly due to its extensive application in domestic settings, grocery stores, restaurants, and small catering establishments. The market enjoys immense popularity among consumers due to their inclination toward simple, affordable, and hassle-free packaging materials that do not need any specific tools or equipment. With the growing trend of consuming packaged leftovers, ready-to-eat meals, and fresh fruits and vegetables, the demand for perishable, hand-held cling film packaging has escalated.

The machine wrap segment is anticipated to rise at the fastest CAGR of 6.44% over the forecast period.

By Thickness

Balanced Cost Efficiency and Durability to Strengthen Growth of 10–15 Microns Segment

Based on thickness, the market is divided into below 10 microns, 10-15 microns, and above 15 microns.

The 10–15 micron segment dominated the cling wrap market share in 2025 primarily due to its optimal balance of stretchability, durability, and cost efficiency. Several households, food retailers, and food service providers prefer this thickness as it provides sufficient strength for wrapping food products while maintaining excellent transparency and cling performance. Moreover, the rising demand for extended shelf-life solutions and secure food packaging has boosted the adoption of medium-thickness wraps.

The above 15 microns segment is anticipated to rise at the second-fastest CAGR of 5.02% over the forecast period.

By End User

Rising Daily Food Storage Needs to Drive Residential/Households Segment Growth

Based on end user, the market is divided into residential/households, foodservice industry, supermarkets & hypermarkets, and others.

The residential/households segment dominated the global market share in 2025, driven by increased urbanization, changes in lifestyle habits, and a rise in the consumption of cooked or leftover food, which has greatly boosted the product demand among household consumers. Cling wrap’s primary function is to extend shelf life and is, therefore, widely used to keep food fresh, prevent contamination, and extend the longevity of fruits, vegetables, and ready-to-eat foods in households. The increasing availability of affordable wraps via supermarket and retail channels has boosted household uptake worldwide.

The foodservice industry segment is anticipated to rise at the fastest CAGR of 6.22% over the forecast period.

By Application

Rising Adoption for Food Preservation to Drive Food Packaging Segment Growth

Based on application, the market is divided into food packaging, household storage, industrial packaging, and others.

The food packaging segment dominated the market share in 2025 due to its extensive use for preserving food freshness, maintaining hygiene, and extending the shelf life of perishable food items. The growing use of packaged foods, convenience meals, fresh produce, and takeaway items has greatly enhanced the need for robust food wrapping options within homes, grocery stores, and restaurants. The cling film helps retain moisture and prevents contamination, making it ideal for preserving meat, fruits, vegetables, and baked goods.

The industrial packaging segment is anticipated to rise at the second-fastest CAGR of 5.31% over the forecast period.

By Distribution Channel

Expanding E-Commerce Penetration and Convenience to Boost Online Retail Segment Growth

Based on distribution channel, the market is segmented into convenience stores, online/e-commerce, hypermarkets/supermarkets, and others.

The hypermarkets/supermarkets segment held the dominant market share in 2025, driven by the strong availability of household and food packaging products under organized retail environments. Rapid urbanization and the expansion of modern retail chains have increased product sales through these large-format stores. Thus, consumers broadly prefer purchasing cling wraps given that these stores offer multiple brands, bulk packaging options, and competitive pricing in a single location.

The online/e-commerce segment is projected to grow at the fastest CAGR of 7.27% during the forecast period. The rapid expansion of online grocery platforms and home-delivery food services is significantly increasing the wrap demand in food protection, freshness preservation, and secure packaging during transportation.

Cling Wrap Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Cling Wrap Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific dominated the global market in 2025, reaching a value of USD 0.64 billion, and is anticipated to grow at a CAGR of 6.46% over the analysis period. The factors driving the Asia Pacific market include rapid urbanization, rising consumption of packaged and ready-to-eat foods, and the expansion of supermarket and food delivery industries across countries such as China, India, and Japan. Increasing disposable incomes and the growing demand for convenient food storage solutions are further accelerating the regional market expansion.

Japan Cling Wrap Market

The Japan market was valued at USD 0.11 billion in 2025, accounting for roughly 6.43% of the global market revenues. Factors contributing to the growth of the Japanese market include the country’s high consumption of packaged convenience foods, bento meals, and fresh seafood products as well as strong consumer emphasis on food hygiene and premium-quality food preservation packaging.

China Cling Wrap Market

The China market was valued at USD 0.27 billion in revenues in 2025, representing roughly 16.18% of the global market sales.

India Cling Wrap Market

The India market was valued at USD 0.12 billion in 2025, accounting for roughly 7.06% of the global market revenues.

North America

North America has emerged as a significant region, with the second-highest market share among all regions, reaching a valuation of USD 0.44 billion in 2025. It is projected to grow at a CAGR of 4.59% over the analysis period. The regional market is driven by the high demand for processed and ready-to-eat food items in the U.S. and Canada, fueled by hectic lifestyles and the emergence of food delivery services. Moreover, the presence of an extensive supermarket and hypermarket chain in the region increases the demand for food packaging and storage products.

U.S. Cling Wrap Market

With North America’s strong contribution and the U.S. dominance in the region, the U.S. market reached USD 0.31 billion in 2025, accounting for roughly 18.99% of the global market sales. The high consumption of packaged and ready to eat foods products, supported by a large foodservice industry and strong demand for hygienic food preservation solutions, drives the market growth in the country.

Europe

The Europe market held the third-largest share in 2025, valued at USD 0.40 billion and accounting for 24.03% of the global market. The regional market growth is bolstered by the high demand for sustainable, recyclable food packaging products, driven by strict environmental regulations in the region. Furthermore, investments in bio-based packaging and circular economies are prompting manufacturers in Europe to produce environmentally friendly cling films.

U.K. Cling Wrap Market

The U.K. market reached a value of USD 0.07 billion in 2025, representing roughly 4.46% of the global market revenues.

Germany Cling Wrap Market

The Germany market reached a valuation of USD 0.09 billion in 2025, equivalent to around 5.32% of the global market sales.

South America and the Middle East & Africa

The South America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The South America market reached USD 0.10 billion in 2025. The rising consumption of packaged food products, expanding supermarket chains, and growing urban populations demanding convenient food storage solutions boost product adoption in the South America market. In the Middle East & Africa, the UAE reached USD 0.02 billion in 2025.

South Africa Cling Wrap Market

The South Africa market reached USD 0.02 billion in 2025, representing roughly 0.99% of the global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Product Innovation and Sustainability to Reinforce their Market Positions

High competition is evident in the market, with most major firms focusing on sustainable innovations, product differentiation, and geographical expansion to enhance their presence. Most firms have been developing recyclable, biodegradable, and bio-based cling wraps to comply with stringent environmental regulations and consumer demand. The development of strategic collaborations with foodservice providers, supermarkets, and online retailers is enhancing the firms' production capabilities. Moreover, the firms have been increasing production capacity to enhance the high performance of their wraps in food preservation. Other growth strategies include mergers, acquisitions, and brand expansion.

LIST OF KEY CLING WRAP COMPANIES PROFILED

- Berry Global Inc. (U.S.)

- Amcor plc (Switzerland)

- Mitsubishi Chemical Group Corporation (Japan)

- Inteplast Group (U.S.)

- Anchor Packaging LLC (U.S.)

- Bunzl plc (U.K.)

- POLIFILM Group (Germany)

- KARAT by Lollicup (U.S.)

- Reynolds Consumer Products (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Amcor plc expanded its polyethylene (PE) shrink and overwrap film manufacturing capabilities across North America following its combination with Berry Global, strengthening supply capacity for cling film and food overwrap applications

- June 2025: Amcor plc launched a more sustainable Perflex® shrink bag packaging solution for Butterball, reducing packaging material use and improving operational efficiency for food packaging

- April 2025: Berry Global Inc. showcased its Omni Xtra+ recyclable polyethylene cling film and other circular flexible packaging solutions at Foodex 2025, focusing on mono-material and recyclable food packaging technologies.

- December 2024: Berry Global Inc. increased its use of post-consumer recycled polyethylene by 36% across flexible film products to strengthen sustainable cling film and food wrap production capabilities.

- November 2024: Amcor plc and Berry Global Inc. announced an all-stock merger agreement to expand global flexible packaging operations and accelerate recyclable cling film innovation.

REPORT COVERAGE

The global cling wrap market analysis includes a comprehensive study of the market and forecast by all the market segments included in the report. This qualitative and quantitative report includes details on the market dynamics and trends that are expected to drive the market over the forecast period. It provides information on key aspects, including technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, acquisitions, and key industry developments. The global research report combines the market outlook with a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.37% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material Type, Product Type, Thickness, Application, End User, Distribution Channel, and Region |

| By Material Type |

|

| By Product Type |

|

| By Thickness |

|

| By Application |

|

| By End User |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 1.65 billion in 2025 and is projected to reach USD 2.60 billion by 2034.

In 2025, the North America market value stood at USD 0.44 billion.

The market is expected to grow at a CAGR of 5.37% over the forecast period.

By material type, the polyethylene (PE) segment led the market in 2025.

Rising demand for packaged and ready-to-eat foods, increasing food safety awareness, and growing need for effective food preservation solutions across households and the commercial foodservice sector are key factors driving the market.

Berry Global Inc., Amcor plc, Anchor Packaging, Mitsubishi Chemical Group Corporation, and Inteplast Group are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 265

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us