Cloud Native Applications Market Size, Share & Industry Analysis, By Deployment (Public Cloud, Private Cloud, and Hybrid Cloud), By Enterprise Type (Large Enterprises and SMEs), By End User (BFSI, Government, Healthcare, Manufacturing, Retail, IT & Telecom, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

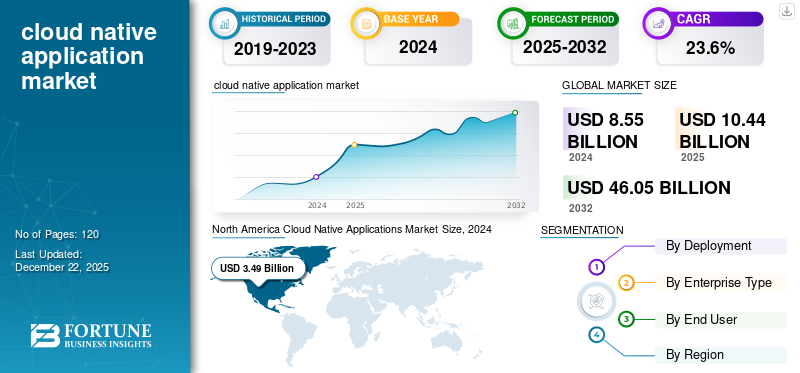

The global cloud native applications market size was valued at USD 10.44 billion in 2025. The market is projected to grow from USD 12.81 billion in 2026 to USD 59.83 billion by 2034, exhibiting a CAGR of 21.25% during the forecast period. North America dominated the global market with a share of 40.17% in 2025.

The cloud native applications market refers to the ecosystem of technologies, platforms, tools, and services designed specifically to build, deploy, and operate applications that fully leverage the scalability, elasticity, and resilience of cloud computing infrastructure. Growing adoption of hybrid and multi-cloud strategies, combined with DevOps automation and CI/CD pipelines, is enabling faster innovation while ensuring flexibility and compliance, thereby playing an important role in driving the growth of the market.

The widespread adoption of microservices, containerization (e.g., Docker), and orchestration platforms such as Kubernetes is transforming how applications are built and deployed. These cloud-native technologies provide scalability, portability, and resilience, making cloud-native solutions attractive for businesses across industries.

The market is dominated by established key players, such as Amazon Web Services, Inc., Alibaba Cloud, Microsoft Corporation, IBM Corporation, and Oracle Corporation. These players focus on partnerships with regional telecoms and governments, especially in Asia, to strengthen hybrid-cloud deployments and collaborate with local independent software vendors (ISVs) for compliance-driven solutions. Thus, this factor is anticipated to fuel market growth across the globe.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Surge in Cloud-Native Architectures to Support AI-driven Workloads Boosts Product Demand

Generative AI is significantly accelerating the adoption of cloud native architectures, as enterprises increasingly rely on containers, microservices, and Kubernetes to support AI-driven workloads at scale. The surge in AI applications requires elastic, GPU-enabled infrastructure, which is pushing organizations toward hybrid and multi-cloud strategies that cloud-native platforms naturally enable. Hyperscalers such as AWS, Microsoft, and Oracle are expanding cloud-native services ranging from managed Kubernetes to AI agent platforms to capture this demand. Cloud-native solutions are now the standard substrate for GenAI apps. For instance,

- In April 2025, as per the Cloud Native Computing Foundation (CNCF) latest annual survey, cloud-native technique adoption hit 89% in 2024.

MARKET DYNAMICS

Market Drivers

Rising Digital Transformation in Enterprises is Driving the Market Growth

The demand for enterprise digital transformation is an important growth driver for the market. Organizations across industries are under pressure to modernize their IT infrastructure to remain competitive, deliver faster product releases, and improve customer experiences. This shift requires replacing or re-architecting legacy monolithic applications with cloud-native architectures that are more agile, scalable, and cost-efficient.

Additionally, the shift toward hybrid and multi-cloud strategies is another factor driving the cloud native applications market growth. For instance,

- According to industry experts, global IT spending will increase by 7.9% in 2025, with data-center systems rising by 42.4% to support cloud and AI-native workloads.

Market Restraints

Shortage of Skilled Workforce May Hinder Market Growth

One of the major restraining factors of the cloud native applications market is the complexity of deployment and management, as enterprises often struggle to integrate microservices, containers, and Kubernetes into existing IT environments without specialized skills. The shortage of cloud-native talent, particularly in Kubernetes administration, DevSecOps, and container security, creates bottlenecks and increases dependence on third-party service providers. Security and compliance risks are another restraint, as cloud environments are highly dynamic and distributed, making them more vulnerable to misconfigurations, data breaches, and regulatory lapses.

Market Opportunities

Growing Demand for Hybrid and Multi-Cloud Deployments Creates Opportunities for SMEs to Manage their Services

The rising demand for hybrid and multi-cloud deployments offers vendors the chance to develop interoperability solutions that address compliance, data sovereignty, and vendor lock-in concerns. With SMEs increasingly adopting cloud native platforms due to their scalability and cost efficiency, there is a large untapped market for simplified, managed services tailored to smaller organizations. Additionally, the expansion of 5G and IoT ecosystems further creates opportunities for cloud-native applications at the edge, enabling low-latency and real-time processing for sectors such as manufacturing, automotive, and telecom. For instance,

- According to industry experts, over 50% of SMEs’ technology budgets are expected to be allocated to cloud services, highlighting strong growth potential by 2025.

Cloud Native Applications Market Trends

Rising Need for Platform Engineering Practices Adoption Fuels Industry Development

A significant trend reshaping the market is the rise of platform engineering, where organizations build internal developer platforms (IDPs) to streamline development workflows, reduce cognitive load, and improve developer productivity.

- For instance, a recent survey by N-iX indicates that 55% of organizations had adopted platform engineering practices by July 2025, signaling widespread recognition of its value in managing cloud-native complexity.

This approach treats platforms as products, with "golden path" templates that enable one-click service creation, enforce compliance, and accelerate onboarding, reducing developer time-to-market from weeks to days.

SEGMENTATION Analysis

By Deployment

Public Cloud Segment Led due to its Ability to Support Peak Traffic Management

Based on deployment, the market is categorized into public cloud, private cloud, and hybrid cloud.

Public cloud captured the largest cloud native applications market share 53.89% in 2026. Public cloud platforms provide virtually unlimited resources, enabling cloud-native applications to scale up or down instantly based on workload demands. This elasticity supports peak traffic management and cost optimization. For instance,

- In July 2025, according to an industry survey, 69% of businesses currently use public cloud infrastructure as their primary environment, illustrating its dominance over other deployment models in enterprise IT.

Hybrid cloud is expected to grow at the highest CAGR during the forecast period.

By Enterprise Type

Growing Demand for Autoscaling and Pay-As-You-Go Models Boosted Large Enterprises Segment Growth

Based on enterprise type, the market is bifurcated into large enterprises and SMEs.

Large enterprises captured the largest market share 65.87% in 2026. By leveraging autoscaling and pay-as-you-go models, large enterprises can optimize cloud spending. This reduces capital expenditure on on-premises infrastructure while aligning costs with actual usage. Additionally, cloud-native platforms enable large enterprises to easily integrate with AI, IoT, and big data analytics services, unlocking insights, improving decision-making, and enabling new business models.

SMEs are anticipated to grow at the highest CAGR during the forecast period.

By End User

To know how our report can help streamline your business, Speak to Analyst

Growing Demand for Advanced Security Features Encouraged the BFSI Segment Growth

Based on end user, the market is categorized into BFSI, government, healthcare, manufacturing, retail, IT & telecom, and others (education, energy & utilities, etc.).

Banking, financial services, and insurance (BFSI) accounted for the largest market share 21.94% in 2026. Cloud-native applications integrate advanced security features such as zero-trust architectures, encryption, and automated compliance checks. This helps BFSI institutions adhere to stringent regulatory requirements such as PCI DSS, GDPR, and local banking standards. For instance,

- In August 2025, according to a report by ZeroThreat, the adoption rate of Zero Trust security models in the BFSI sector ranges from 22% to 30%, reflecting a growing shift toward modern cloud-native security practices tailored for regulated industries.

The healthcare segment is projected to grow at the highest CAGR during the forecast period.

CLOUD NATIVE APPLICATIONS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America Cloud Native Applications Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

The North America market accounted for USD 4.19 billion in 2025, representing 40.17% of the global industry, and is expected to reach USD 5.07 billion in 2026. with USD 5.07 billion. The factors fostering the dominance of the region include robust digital infrastructure and high Kubernetes adoption rates, with strong broadband and shared tech ecosystems underpinning innovation. Additionally, the region has an advanced IT infrastructure, including widespread, high-speed connectivity, that supports scalable data-intensive workloads. In 2026, the U.S. market is estimated to reach USD 3.67 billion. The presence of a vast data center footprint positions the U.S. as the backbone of global cloud-native application deployment, ensuring low latency, scalability, and resilience for enterprises. For instance,

- In May 2025, the U.S. alone had approximately 5,426 data centers, offering unmatched digital infrastructure to support high-speed, scalable cloud-native workloads.

Download Free sample to learn more about this report.

Europe

Europe recorded a market size of USD 2.52 billion in 2025, capturing 24.11% of the global market share, and is projected to reach USD 3.07 billion in 2026. Europe is anticipated to witness a notable growth in the coming years. During the forecast period, the European region is anticipated to record a growth rate of 22.9%, which is the fourth highest amongst all the regions, and reach the valuation of USD 2.52 billion in 2025. This is primarily due to the presence of sustainability goals and energy-efficient IT operations in the region. In addition, the European Union’s collaborative infrastructure initiatives, such as Gaia-X, also foster cloud-native adoption by offering a federated, trusted framework for data sharing and cloud interoperability. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 0.61 billion, Germany to record USD 0.59 billion, and France to record USD 0.40 billion in 2026.

Asia Pacific

In 2025, Asia Pacific represented USD 2.65 billion, accounting for 25.39% of the worldwide market, and is projected to grow to USD 3.34 billion in 2026. The regional growth is fueled by accelerated enterprise digital transformation and strong government cloud adoption initiatives across countries such as China, India, and Singapore. In the region, India and China are both estimated to reach USD 0.53 billion and USD 0.71 billion, respectively, in 2026.

South America

South America is expected to witness significant growth in the cloud native applications market. The South American market in 2025 is set to record USD 0.46 billion, driven by its strong investment in cloud infrastructure, with hyperscalers such as AWS and Microsoft committing multi-billion-dollar projects in countries such as Chile and Brazil to expand data center capacity and enable scalable cloud-native workloads.

Middle East & Africa

Middle East & Africa contributed 5.98% to the global market in 2025, with a valuation of USD 0.62 billion, and is projected to reach USD 0.77 billion in 2026. The Middle East & Africa is expected to grow at a prominent growth rate in the coming years, owing to increasing investments in cloud infrastructure by hyperscalers and the rise of fintech & e-government services requiring agile, cloud-native solutions. In the region, GCC is set to attain the value of USD 0.20 billion in 2025.

Competitive Landscape

KEY INDUSTRY PLAYERS

Wide Range of Product Offerings coupled with the Strong Geographic Presence by Key Companies to Support their Leading Position

The global cloud native applications market shows a semi-concentrated structure with numerous small-to-mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Amazon Web Services, Inc., Alibaba Cloud, Microsoft Corporation, IBM Corporation, and Broadcom are some of the dominating players actively creating advanced solutions to cater to customer demands. Additionally, they focus on collaboration, acquisitions, and partnerships with regional players to maintain dominance across regions.

Apart from this, other prominent players in the market include Oracle Corporation, Infosys Limited, Red Hat, Inc., Google Cloud, and others. These companies are undertaking various strategic initiatives such as investments in R&D, geographic expansion, and product launches, to bolster their product offerings.

Long List of Cloud Native Applications Companies Profiled

- Amazon Web Services, Inc. (U.S.)

- Alibaba Cloud (China)

- Microsoft Corporation (U.S.)

- IBM Corporation (U.S.)

- Broadcom (U.S.)

- Oracle Corporation (U.S.)

- Infosys Limited (India)

- Alphabet Inc. (Google LLC) (U.S.)

- Red Hat, Inc. (U.S.)

- SAP SE (Germany)

- Larsen & Turbo Infotech (India)

- Apexon (U.S.)

- Bacancy Technology (India)

- Citrix Systems, Inc. (U.S.)

- Ecko (Ireland)

- Huawei Technologies Co. Ltd. (China)

- Cognizant Technology (U.S.)

- R Systems (U.S.)

- Scality (U.S.)

- Sciencesoft (U.S.)

….and more

KEY INDUSTRY DEVELOPMENTS

- September 2025: AWS and Reuters unveiled a cloud-native, AI-powered news distribution system based on the Time-Addressable Media Store (TAMS) framework. The solution leverages AWS Bedrock and other cloud services to enable real-time, scalable workflows for the media sector.

- July 2025: AWS launched Amazon Bedrock AgentCore at its New York Summit, a production-grade platform designed for building and deploying AI agents at scale. The service integrates observability, memory, identity, and tool support, reinforcing AWS’s role in cloud-native AI innovation.

- July 2025: SAP expanded its sovereign cloud offerings across Europe. Through this new offering, the company aims to deliver compliant, AI-capable cloud services to regulated markets.

- April 2025: Alibaba Cloud unveiled a suite of AI models and platform enhancements to expand its global cloud-native capabilities. Additionally, the company announced plans to open a second data center in South Korea by June 2025.

- April 2025: EPAM announced an expanded strategic collaboration agreement with AWS to focus on generative AI and cloud-native transformation. The partnership aims to accelerate application modernization and AI adoption for enterprise clients.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 21.25% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Deployment · Public Cloud · Private Cloud · Hybrid Cloud By Enterprise Type · Large Enterprises · SMEs By End User · BFSI · Government · Healthcare · Manufacturing · Retail · IT & Telecom · Others (Education, Energy & Utilities, etc.) By Region · North America (By Deployment, By Enterprise Type, By End User, and By Country) o U.S. o Canada o Mexico · South America (By Deployment, By Enterprise Type, By End User, and By Country) o Brazil o Argentina o Rest of South America · Europe (By Deployment, By Enterprise Type, By End User, and By Country) o U.K. o Germany o France o Italy o Spain o Russia o Benelux o Nordics o Rest of Europe · Middle East & Africa (By Deployment, By Enterprise Type, By End User, and By Country) o Turkey o Israel o GCC o North Africa o South Africa o Rest of Middle East & Africa · Asia Pacific (By Deployment, By Enterprise Type, By End User, and By Country) o China o India o Japan o South Korea o ASEAN o Oceania Rest of Asia Pacific |

|

Companies Profiled in the Report |

· Amazon Web Services, Inc. (U.S.) · Alibaba Cloud (China) · Microsoft Corporation (U.S.) · IBM Corporation (U.S.) · Broadcom (U.S.) · Oracle Corporation (U.S.) · Infosys Limited (India) · Alphabet Inc. (Google LLC) (U.S.) · Red Hat, Inc. (U.S.) · SAP SE (Germany) |

Frequently Asked Questions

The market is expected to reach USD 59.83 billion by 2034.

In 2025, the market was valued at USD 10.44 billion.

The market is projected to grow at a CAGR of 21.25% during the forecast period.

By end user, BFSI led the market.

Rising digital transformation in enterprises is driving the market growth.

Amazon Web Services, Inc., Alibaba Cloud, Microsoft Corporation, IBM Corporation, Broadcom, Oracle Corporation, Infosys Limited, Alphabet Inc. (Google LLC), Red Hat, Inc., and SAP SE are the top players in the market.

North America held the highest market share.

By end user, the healthcare segment is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us