Commercial Aerospace Market Size, Share & Industry Analysis, By Aircraft Type (Narrowbody (Single-aisle), Widebody (Twin-aisle), Regional Aircraft, Freighter Aircraft), By Technology (Propulsion & Power Systems, Avionics, Flight Deck & Connectivity, Aerodynamics, Structures & Materials, Flight Controls & Actuation, Landing Gear, Brakes & Wheels, & Others), By Engine Type (Turbofan, Turboprop, APU, Hybrid-electric Propulsion, Hydrogen Propulsion) By End User (Airlines, Cargo Operators, Aircraft Lessors / Asset Owners, & Others), and Regional Forecast, 2026-2034

Commercial Aerospace Market Size and Future Outlook

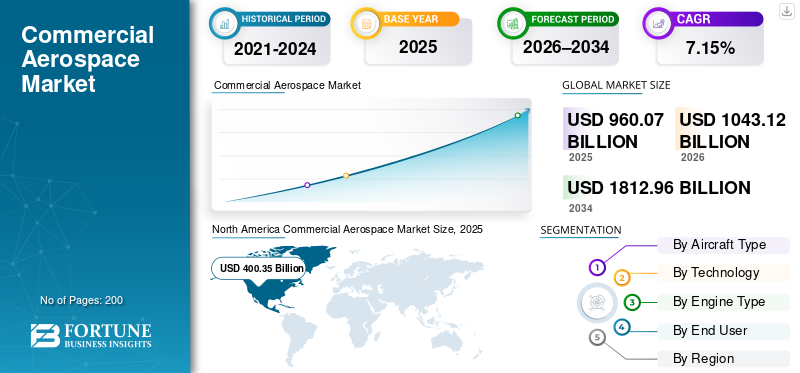

The global commercial aerospace market size was valued at USD 960.07 billion in 2025. The market is projected to grow from USD 1043.12 billion in 2026 to USD 1812.96 billion by 2034, exhibiting a CAGR of 7.15% during the forecast period. North America dominated the global commercial aerospace market with a market share of 41.70% in 2025.

Commercial aerospace refers to the segment of civil aviation involving the manufacture, operation, and support of aircraft for hire or remuneration, including passenger airliners, cargo planes, regional jets, business jets, engines, avionics, and maintenance services. End users primarily consist of airlines providing scheduled passenger and cargo services, aircraft lessors, and charter operators. Key driving factors include rising global air travel demand from expanding middle classes and urbanization, fleet renewal for efficiency, and e-commerce-fueled cargo growth.

Major players are Airbus SE, Boeing Company, Embraer S.A., Bombardier Inc., and COMAC. The key players are focused on post-pandemic recovery and sustainability pushes

Download Free sample to learn more about this report.

COMMERCIAL AEROSPACE MARKET TRENDS

Rising Usage of Digital Twin in Commercial Aviation Leads to New Market Trend

Digital twin technology is emerging as a pivotal market trend in commercial aviation, creating virtual replicas of aircraft, engines, and systems that mirror real-time operations using sensor data, AI, and simulations. In aviation, it enables predictive maintenance by forecasting failures, optimizing fuel efficiency through aerodynamic analysis, and streamlining fleet management to cut downtime and costs. Airlines and OEMs such as Airbus leverage it for lifecycle monitoring from design enhancements on the A350 XWB to in-service performance tweaks, reducing emissions and boosting safety amid rising air travel.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Air Travel Leads to Market Expansion of Commercial Aerospace

Rising air travel demand drives commercial aerospace market growth because airlines must expand fleets to accommodate surging passenger volumes, fueled by economic recovery and urbanization in emerging regions such as Asia-Pacific, the Middle East and Africa. Furthermore, stronger connectivity needs on international and domestic routes compel carriers to order new aircraft from OEMs such as Airbus and Boeing. At the same time, high load factors strain existing capacity and accelerate replacements for efficiency. Cargo volumes rise alongside e-commerce expansion, further boosting demand for wide-bodied and freighters. This persistent upward pressure sustains production rates, supply chain investments, and aftermarket services as operators prioritize scalability and reliability.

MARKET RESTRAINTS

Stringent Certification And Regulatory Requirements Are a Market Restraint

Stringent certification and regulatory requirements act as a significant market restraint in commercial aerospace because rigorous FAA and EASA approval processes for new aircraft designs, engines, and modifications impose lengthy timelines and high compliance costs on aircraft manufacturers. These rules demand exhaustive testing for safety, emissions, and noise standards, delaying market entry of innovative models amid evolving sustainability mandates such as net-zero goals.

MARKET OPPORTUNITIES

Proliferation of Low-Cost Carriers in Many Regions Creates New Market Opportunities

The proliferation of low-cost carriers across regions creates a prime market opportunity in commercial aerospace as these operators prioritize high-frequency, short-haul routes with fuel-efficient narrow-body jets to serve price-sensitive travelers. Budget airlines expand aggressively in middle-class populations in regions of Asia-Pacific, Latin America, and Africa, opening new domestic and regional networks where rising middle classes demand affordable connectivity without legacy infrastructure costs.

MARKET CHALLENGES

Supply Chain Disruptions Serve as a Major Market Challenge

Supply chain disruptions pose a significant market challenge in commercial aerospace because critical shortages of engines, avionics, forgings, and skilled labor halt aircraft assembly lines and delay deliveries from OEMs such as Airbus and Boeing. Airlines suffer grounded planes, escalating leasing costs, and forced reliance on aging fleets that burn more fuel and rack up maintenance bills. Geopolitical tariffs on metals and electronics, plus fragile supplier networks dependent on a few providers, amplify even minor issues into widespread production stalls. This fragility curbs fleet expansion, hampers sustainability progress, and squeezes profitability as carrier’s miss revenue from unmet demand.

Segmentation Analysis

By Aircraft Type

Low Operating Cost to Boost the Narrow-body (Single-aisle) Segmental Growth

Based on the aircraft type, the market is segmented into Narrow body (Single-aisle), Wide body (Twin-aisle), Regional Aircraft, and Freighter Aircraft.

The narrow-body (Single-aisle) segment is anticipated to account for the largest market share. The segmental growth is owing to the fact that narrow-body aircraft are very profitable for airlines running high-frequency, short-to-medium haul routes due to their lower operating costs per seat.

The wide-body (Twin-aisle) segment is anticipated to rise with a CAGR of 7.37% over the forecast period.

By Technology

High Structural Optimization to Boost Aerodynamics, Structures & Materials Segment Growth

Based on technology, the market is segmented into propulsion & power systems, avionics, flight deck & connectivity, aerodynamics, structures & materials, flight controls & actuation, landing gear, brakes & wheels, thermal, environmental & pneumatic systems, electrical wiring &more-electric systems, fuel & fluid systems, cabin & interior systems, and safety, monitoring & mission-critical protection.

In 2025, the aerodynamics, structures & materials segment accounted for the largest share of the global market. The growth is owing to the fact that this segment integrates with materials, which allows for thinner, higher-aspect-ratio wings and blended wing-body configurations. These shapes reduce induced drag and enhance lift, which further reduces overhead costs.

The fuel & fluid systems segment is projected to grow at a high CAGR of 7.80% over the forecast period.

By Engine Type

High Fuel Efficiency to Boost Turbofan Segment Growth

Based on the engine type, the market is segmented into Turbofan, Turboprop, APU (Auxiliary Power Unit), Hybrid-electric propulsion (emerging), and Hydrogen propulsion (R&D / early demos).

The Turbofan segment is anticipated to witness a dominating market share over the forecast period. High fuel efficiency boosts turbofan segment growth in commercial aerospace because high-bypass ratio designs significantly reduce fuel burn compared to older turbojets, enabling airlines to lower operating costs on high-frequency routes while meeting stringent emissions standards.

The Turboprop segment is projected to grow at a high CAGR of 7.30% over the forecast period.

By End User

To know how our report can help streamline your business, Speak to Analyst

Large Fleet Size to boost the Airlines (Passenger carriers) Segment

Based on end user, the market is segmented into Airlines (Passenger carriers), Cargo Operators, Aircraft Lessors / Asset Owners, Charter / ACMI Operators, and Government & Civil Operators (non-military).

The Airlines (Passenger carriers) segment dominated the commercial aerospace market share. The segmental growth is because they operate the vast majority of the global fleet for scheduled high-volume services, driving consistent demand for new aircraft, engines, and MRO to support expanding routes and passenger loads.

In addition, Charter / ACMI Operators are projected to grow at a high CAGR of 7.70% during the study period.

Commercial Aerospace Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Commercial Aerospace Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 370.15 billion, and also maintained the leading share in 2025, with USD 400.35 billion. North America leads commercial aerospace with major OEMs such as Boeing driving production and innovation in fuel-efficient jets.

U.S Commercial Aerospace Market

Based on North America’s substantial contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 262.19 billion in 2026, accounting for roughly 7.43% CAGR. The U.S. dominates as Boeing's home base, with high aircraft deliveries supporting extensive airline networks and cargo growth. Regulatory oversight by the FAA ensures safety while spurring tech upgrades amid the post-recovery travel surge.

Europe

Europe is projected to record a steady growth rate during the forecast period of 6.89%, which is the second highest among all regions, and reach a valuation of USD 212.83 billion by 2026. Europe emphasizes sustainability, with Airbus leading deliveries and strict EU emissions rules pushing green tech adoption.

U.K Commercial Aerospace Market

The U.K. market in 2026 is estimated at around USD 63.58 billion, representing roughly 7.21% CAGR during the study period. The U.K. leverages post-Brexit trade deals to boost aerospace exports while British Airways modernizes its widebodies.

Germany Commercial Aerospace Market

Germany’s market is projected to reach approximately USD 56.58 billion in 2026. Germany excels in engines via MTU and avionics, supporting Lufthansa's fleet renewal and MRO hub status. Industry clusters drive innovation in composites and digital maintenance.

Asia Pacific

The Asia Pacific region is estimated to reach USD 286.10 billion in 2026 and secure the position of the third-largest region in the market and fastest growing during the study period. Asia Pacific sees rapid growth from booming air travel in high-density routes, led by low-cost carriers and infrastructure builds. Emerging economies drive narrow-body demand as connectivity expands across the region.

Japan Commercial Aerospace Market

The Japanese market in 2026 is estimated at around USD 52.60 billion, accounting for roughly 7.81% of the compound annual growth rate (CAGR) during the forecast period. Japan focuses on efficient regional jets and engine tech via Mitsubishi and IHI, supporting All Nippon and Japan Airlines' modernization.

China Commercial Aerospace Market

China’s market is projected to be one of the largest in the Asia Pacific, with 2026 revenues estimated at around USD 82.57 billion. China advances through COMAC's C919 entering service, reducing import reliance while state-backed airlines expand international routes.

India Commercial Aerospace Market

The Indian market in 2026 is estimated at around USD 64.49 billion. India experiences explosive aviation growth with IndiGo and Air India ordering hundreds of aircraft for domestic and international expansion.

Rest of the World

The rest of the world includes the Middle East & Africa, and Latin America. Middle East hubs such as Dubai and Doha thrive on transit traffic with Emirates and Qatar Airways fueling widebody orders. Latin America expands low-cost networks with carriers including Azul and Viva Aerobus targeting regional connectivity. The Middle East & Africa and Latin America market is set to reach a valuation of USD 67.06 billion and USD 42.01 billion in 2026, respectively.

COMPETITIVE LANDSCAPE

Key Industry Players

Rising Technological Innovations by Key Market Players Drive Market Development

The commercial aerospace market remains consolidated, dominated by Airbus SE and The Boeing Company, which command the majority of aircraft orders through superior manufacturing scale and global delivery networks.

Technological innovations fuel growth as Airbus rolls out the A321XLR with extended range for transatlantic efficiency and ZEROe hydrogen concepts targeting net-zero emissions. At the same time, Boeing advances the 777X folding wingtips and the 737 MAX 10 for high-density short-haul dominance. Embraer enhances E195-E2 with reduced noise profiles for urban airports, Bombardier refines Challenger jets for VIP sustainability, and COMAC scales C919 production with LEAP-1C engines for domestic dominance. These innovations meet airline demands for fuel savings, regulatory compliance, and expanded route flexibility.

LIST OF KEY COMMERCIAL AEROSPACE COMPANIES PROFILED

- Airbus SE (France)

- Boeing Company (U.S.)

- Embraer S.A. (Brazil)

- Bombardier Inc. (Canada)

- COMAC (Commercial Aircraft Corporation of China) (China)

- GE Aerospace (U.S.)

- Pratt & Whitney (U.S.)

- Rolls-Royce Holdings (U.K.)

- Safran Aircraft Engines (France)

- Textron Aviation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Beginning in February 2026, Lufthansa Cargo will introduce two additional destinations as part of its network expansion for short- and medium-haul freight. Rome-Fiumicino (FCO) will be part of the airline's regular freighter flight schedule.

- November 2025: At the Dubai Airshow 2025, Emirates announced orders for eight more Airbus A350-900 aircraft with Rolls-Royce Trent XWB84 engines, valued at USD 3.4 billion.

- March 2025: Jackson Square Aviation (JSA) has announced that it has placed its first direct order with Airbus, obtaining fifty aircraft from the A320neo family. This critical agreement enhances JSA's collaboration with Airbus and advances its plan to provide fuel-efficient narrow-body fleet solutions to airlines worldwide.

- August 2024: At Frankfurt Airport, Lufthansa Cargo welcomed its eighteenth B777 freighter. The cargo airline's most significant hub received the long-haul freighter straight from the Boeing plant in Everett, U.S.

- June 2023: IndiGo placed a record firm order for 500 A320 Family aircraft (mix of A320neo, A321neo, and A321XLR) at Paris Air Show, valued at USD 50 billion, marking the most significant single aircraft purchase by any airline with Airbus.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.15% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Aircraft Type, Technology, Engine Type, End User, and Region |

|

By Aircraft Type |

· Narrowbody (Single-aisle) · Widebody (Twin-aisle) · Regional Aircraft · Freighter Aircraft |

|

By Technology |

· Propulsion & Power Systems · Avionics, Flight Deck & Connectivity · Aerodynamics, Structures & Materials · Flight Controls & Actuation · Landing Gear, Brakes & Wheels · Thermal, Environmental & Pneumatic Systems · Electrical Wiring & More-Electric Systems · Fuel & Fluid Systems · Cabin & Interior Systems · Safety, Monitoring & Mission-Critical Protection |

|

By Engine Type |

· Turbofan · Turboprop · APU (Auxiliary Power Unit) · Hybrid-electric propulsion (emerging) · Hydrogen propulsion (R&D / early demos) |

|

By End User |

· Airlines (Passenger carriers) · Cargo Operators · Aircraft Lessors / Asset Owners · Charter / ACMI Operators · Government & Civil Operators (non-military) |

|

By Region |

· North America (By Aircraft Type, Technology, Engine Type, End User, and Country) o U.S. (End User) o Canada (End User) · Europe (By Aircraft Type, Technology, Engine Type, End User, and Country/Sub-region) o U.K. (End User) o Germany (End User) o France (End User) o Russia (End User) o Italy (End User) o Rest of Europe (End User) · Asia Pacific (By Aircraft Type, Technology, Engine Type, End User, and Country/Sub-region) o China (End User) o India (End User) o Japan (End User) o South Korea (End User) o Australia (End User) o Rest of Asia Pacific (End User) · Rest of the World (By Aircraft Type, Technology, Engine Type, End User, and Country/Sub-region) o Middle East & Africa (End User) o Latin America (End User) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 960.07 billion in 2025 and is projected to reach USD 1812.96 billion by 2034.

In 2025, the market value stood at USD 400.35 billion.

The market is expected to grow at a CAGR of 7.15% during the forecast period of 2026-2034.

By aircraft type, the Narrowbody (Single-aisle) segment is expected to dominate the market.

Rising air travel is anticipated to drive market growth.

Airbus SE (France), Boeing Company (US), Embraer S.A. (Brazil), Bombardier Inc. (Canada), COMAC (Commercial Aircraft Corporation of China) (China), and others are a few key players in the global market.

North America dominated the market in 2025

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us